Transcription

163 South Willard StreetP.O. Box 670Burlington, .edu/cfl2014 Annual ReportThe Center forFINANCIAL LITERACYat Champlain CollegePreparing students &adults to make sound decisions14 MISC 0304 2/15 600CHAMPLAIN.EDU/CFL

Advisory Board Joseph BergeronPresident, Association ofVermont Credit Unions enee Bourget-Place RPartner, KPMG, LLP omas Brownell ThPresident and CEO,Sentinel AssetManagement Inc. Jeanne ChenowethPrincipal, JBCConsulting J eanne CollinsSuperintendent ofSchools, RutlandNortheastSupervisory Union hilip Daniels PMarket President,Vermont, TD Bank Scott GilesPresident, VermontStudent AssistanceCorporation Supporters eborah Healey DHead Trader/Partner,Champlain InvestmentPartners LLC Kelley JordickVice President/Market Manager,Merchants Bank Joyce JudyPresident, CommunityCollege of Vermont onald Laackman D(ex-officio), President,Champlain College David LambertiEconomics and PersonalFinance Teacher,Burlington High School Thomas LeavittPresident & ChiefExecutive Officer,Northfield Savings Bank Susan LeonardSenior Vice President/Chief Financial Officer,New England FederalCredit Union Robert MangiacottiCFP, ResidentDirector/First VicePresident-Investments,Merrill Lynch WealthManagement Greg MorganChair, EssexEconomicDevelopmentCommission Michael SeaverDivision Presidentfor Vermont, People’sUnited Bank Art WoolfAssociate Professorof economics at theUniversity of Vermont,President of theVermont Council onEconomic Education Association of VermontCredit Unions People’s United Bank Angelo Pizzagalli Champlain InvestmentPartners LLC State Street Corporation DST Systems, Inc. TD Bank Hanson & Doremus United Way ofChittenden County KeyBank KPMG LLP Merchants Bank Merrill Lynch WealthManagement, Bank ofAmerica Corp. Vermont Associationof Realtors Vermont BusinessRoundtable ermont Department of VFinancial Regulation National Endowmentfor Financial Education Vermont MutualInsurance Group National Life Group Vermont StudentAssistance Corporation ew England Federal NCredit Union Northfield Savings Bank John and Leigh Pelletier Windham Foundation Anonymous donors

Letter from the DirectorIn the words of former President Bill Clinton, financial literacy is “a very fancyterm for saying spend it smart, don’t blow it, save what you can, and know how theeconomy works.”Right he is. But fancy term or not, achieving financial literacy is no small task. Ibelieve that in the four years the Center for Financial Literacy has been in existence,we have made considerable progress. We have made a compelling case for the need forpersonal finance education. We have helped create awareness that financial illiteracyis a national problem that needs to be formally addressed by our schools, colleges andcommunities, and we have developed a number of successful initiatives to begin tomake that needed education a reality.THE PROBLEMS WE FACE ARE DAUNTING: nly 40 percent of states require personal finance education for high Oschool graduation.ABOUT DIRECTORJOHN PELLETIERJohn Pelletier has more than20 years of experience inthe investment managementindustry. He has served aschief operating officer andchief legal officer at some ofthe largest asset managementfirms in the United States.champlain.edu/cfl n an international financial literacy test of 15-year-olds, the U.S. ranked Oin the bottom third behind China, the Czech Republic, Poland and Latvia,and was statistically tied with Russia—what a “Sputnik” moment. S even in ten college students from the class of 2013 graduated withstudent debt that averaged 28,400 and delinquency rates on studentloans continue to soar. our out of ten adults give themselves a grade of C, D or F on their Fpersonal finance knowledge—and it shows; more than a one-third ofadults have no retirement savings and more than half have subprimecredit, meaning they will pay a lot more in interest on all types of loans,credit cards and mortgages.A NEW TASK FORCE FOR FINANCIAL LITERACYThe achievement I’m most proud of this past year was launching the VermontFinancial Literacy Task Force, made up of 20 leaders in education, government,business and the nonprofit sector. Their mission is to help policymakers understand thebroad ramifications of financial illiteracy and to make recommendations (which you’llread more about in this report) that would provide a path for all Vermonters to obtainthe personal finance knowledge and skills that they need to succeed. Although thisinitiative is very specific to Vermont, I believe the task force structure and many of itsfindings can easily be applied to other states.TRAINED TEACHERS MAKE A DIFFERENCEThe other initiative of 2014 I would like to highlight is the High School Pilot Program.Its goal is to compare the knowledge and behaviors of high school students that havetaken a personal finance course taught by highly-trained educators (trained by ourCenter’s Summer Institute program) with a control group of students that have notreceived classroom instruction on this important topic. We are in our second academicyear of gathering hard data by following trained teachers in their classrooms. A reporton this effort will be issued in the fall of 2015.The Center for Financial LiteracyGOALS FOR 2015Each year, I look forward to expanding our innovative programs and reaching morestudents and adults in our own state and nationally. Following are some of our plansI’m excited about: reating a standardized assessment to measure high school and college Cstudents’ financial literacy. I ssuing an update to our 2013 highly regarded National Report Card onState Efforts to Improve Financial Literacy in High Schools. inding partners to help us transform Awesome Island, our award Fwinning personal finance board game for middle and high schoolstudents, into a free, online educational game available to teachers andstudents across the country. aunching a website in the fall of 2015 created by high school educators Lto give their peers access to vetted and trusted financial literacy tools andcurricula that they can confidently use in their classrooms. inding ways to bring free, online personal finance curricula, educational Fvideos and tools to young adults across the nation.YOU CAN MAKE A DIFFERENCEWe believe our initiatives at the Center are transforming personal finance educationin Vermont and across the United States. Our efforts are greatly aided by the Center’saffiliation with Champlain College. The backing of Champlain President Donald J.Laackman, our advisory board, Vermont’s state government, and business, nonprofitand education leaders makes it possible for us to continue this significant work.In summary, we believe we are making an impact on improving financial literacy atevery level, from kindergarten through college and on into the adult years. But onlywith your support can we continue to pursue pioneering educational initiatives thatwill lead to a more financially sophisticated population. Our work is made possible byindividual, corporate and foundation donors, as well as grants. Please help us achieveour goal of personal finance skills and knowledge for all of our citizens.Thank you for your support of the Center.Sincerely,Sincerely,John Pelletier, DirectorThe Center for Financial Literacy at Champlain CollegeSpring 2015YEAR IN REVIEW–5

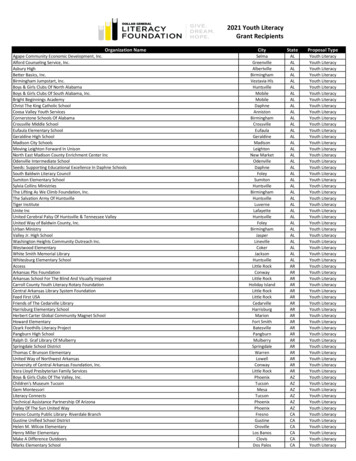

COLLEGEFINANCIAL LITERACYCOLLEGEFINANCIALLITERACYK-12 FINANCIAL LITERACYK-12 FINANCIAL LITERACYVERMONT DCalling on a diverse cross-section of leaders from education, government, businessand the nonprofit sector, the Center established a Financial Literacy Task Force thatrecommended ways to improve the financial literacy of all Vermonters. In DecemberK-12 FINANCIAL LITERACY2014, the Task Force issued its report and recommendations.Recommendations from the Vermont Financial Literacy Task Force12 . 18 . 2014 DK-12FINANCIAL LITERACYLITERACYK-12FINANCIALLITERACY10%POLANDNEW 2RUSSIALATVIALATVIAPOLANDK-12 FINANCIAL LITERACYPOLANDCZECH REPUBLICCZECH REPUBLICAUSTRALIACNEW ZEALAND NEW ZEALANDBESTONIAAAUSTRALIAMore than half ofthe states receiveda grade of A, B or C.BELGIUMeffortstohasimproveVermonta “D”financialgrade in aliteracynationalin highcardschools.reporton stateESTONIACCHINABBELGIUMAgrade in a nationalREPORTCARDreport card on stateCHINA DREPORTCARDVermont has a “D”USA D11%2012OECD PISA international financial literacy test Update Vermont’s existing personal economics andcareer choicesof 15-year-olds– U.S. ranked 9th out of 13countries regardedparticipating inthe exam andeducation standards to be more consistent with highlynationalstatistically tied with Russia. 2012 nsure that all Vermont high school students have access to a personal Ehighschools in Vermont (7 out of 65) haveADULTFINANCIALLITERACYfinancecourse. ROUGHLY10% ofa financialliteracy graduation requirement.of high schoolsin Vermont(7 outof 65)havepersonalfinancetraining Providea financial literacy graduation requirement.41%opportunities toOnlyK-1227educators.percent of parents inADULT FINANCIAL LITERACYshowsVermonthaveset aside funds for reate an onlineSurveyclearinghouseof vetted and trustedfinancialliteracy Cthat even at high schoolsthat as many sresources for Vermont K-12 educators.That survey also shows41 30 3441 11 34U.S. indicatedOF U.S. ADULTS% OF U.S. ADULTS%%COLLEGE %FINANCIALLITERACY% in the% of adultsOF U.S. ADULTSC, D or F on their personal34%Only 27 percent of parents inVermont have set aside funds fortheirchild’s that as many as30%%30Survey showsthat as many as10%30%RUSSIALATVIAPOLANDCZECH REPUBLICNEW ZEALANDAUSTRALIAESTONIABELGIUMROUGHLY 10%CHINAREPORT CARD2012report card on stateoffered,highcollegeschooltheiroflife– to attend college or kedof 9th out of 13education.of15-year-olds– U.S.of high schools in Vermont of(7out65)improvehaveeffortstoof parents inAVERAGE LOAN DEBTadministratorsestimateMorethanOnlyhalfof27 percenta financialgraduationrequirement.That literacysurvey alsoshowsstudyor careerchoice mandUPONGRADUATION:the states Vermontreceivedthancountriestwo-thirdsthat morehavesetasideparticipatingfunds for in thethat even at high schoolsa grade of A,ofB orC.studentsstatisticallythegraduatetied with Russia.esshighthanschools.50 percent of Vermontworkersparticipateinan employment is Lintheirchild’scollegeeducation.where the electiveof Vermont high schools may noteven offer a personal finance electivecourse for their students to take.of Vermont high schools may noteven offer a personal finance electivecourse for their students to take. 28,299 28,299offered,high alsoschoolofshowsVermonthigh schoolsplan,may andnot only 36withoutThat surveybased retirementpercentachievingof adults have a rainy daycompetence in financialevenoffer a personal finance electiveadministratorsestimatethateven at necessities.literacy topics.coursefor their students to take.two-thirdsthat morewherethe thanelectiveisofthestudentsgraduateoffered, high schoolVermont graduates of four-year collegeswithout achievingadministratorsestimatefrom the class of 2012 who had loanscompetencein two-thirdsfinancialmore thanthatleft college with an average of 28,299of high schools in Vermont (7 out of 65) haveliteracytopics.of the studentsgraduateWhenthey graduate, Vermont high school students should understand how creditin student loan debt.47%47% 28,29911%% 9,667. 0062 OFOF62%50%These Vermonters pay a lot more for all credit: auto and home loans and credit card debt.BIG BANK63 percentof VermontFROM THEADULT COMMITTEECREDIT SCOREAverage credit carddebt of adult Vermonter.adults witha wide varietypersonal finance learning opportunities. Providecollegeseniorsin oftheNationally, nearly00graduated2012 I ncrease9,667.E low-incomeR M O NVermontersT A D UtoLTthe opportunitiesincentivesVforsaveSclassof 2012andBIG BANKVermontgraduates of four-year collegesfrom the class of 2012 who had loansAverage credit cardleft collegewith an average of 28,299andassets.debtbuildof adultVermonter.in student loan debt.11 percent of all studentloanborrowersLESSTHAN wereof Vermont workersdelinquentin theirdo nothave aparticipate in anemployment-based“rainypaymentsby daymorefund,”thanretirement plan.whoOFare90savingfor Increase the percentage of Vermont employeesIN CASEliquidemergencydaysa asof retirement.June2014.Average credit uldLESSTHANdebt of adult Vermonter.BREAK PIGFINANCIAL LITERACY 101participate in an“rainyday fund,”cover threemonthsemployment-basedINCASEDEBTOFa liquidemergencyVermont graduates of four-year colleges Only uationrequirement.EMERGENCY,retirementplan.without achievingfrom the class of 2012 who had loansof Vermont workers UPON GRADUATION:that wouldLESS THANPIGworks, how to budget, and how to save and invest. College graduates shouldOnceimplemented,recommendationsof the BREAKTask ForcewillfundmateriallyincreaseVermonthaveset asidethefundsforcompetence in financialparticipate in anleft college with an average of 28,299cover three monthsunderstand those concepts,in addition to the connection between income and tomakepositivechangesin theiremployment-based10literacy topics.theirchild’scollegeeducation.in student loan debt.of life’s necessities.retirement plan.and how student loans work. Vermont adults need to understand the importance ofROUGHLY 10%Survey showsthat as 10many asThat survey also showsrainy day and retirement funds, and the amounts they willthatneedeveninatthosehighfunds.schools30%of Vermont high schools may noteven offer a personal finance electivecourse for their students to take.The Center for Financial Literacywhere the elective isoffered, high schooladministrators estimatethat more than two-thirdsof the students graduatewithout achievingcompetence in financialliteracy topics.with student00loan debt. 9,667.V E R M O N T A D U LT S50%50% 28,299personal and professional lives. Vermonters need the skills and tools to take control oftheir financial lives. The path forward is education. Financial literacy means a moreprosperous and stronger economy for all of us. Go to financialfunkVT.org to view thereport and a short video.Vermont graduates of four-year collegesfrom the class of 2012 who had loansleft college with an average of 28,299in student loan debt.gCfNationally, nearly11 percent of all stloan borrowers we 28,299UPON GRADUATION:4delinquent in theipayments by more90 days as of JuneAVERAGE LOAN DEBTUPON GRADUATION: 28,2Tof adults in theU.S. indicatedthat ADULTtheyhaveFINANCIALnoADULTFINANCIALVermont graduates of four-year cfrom the class of 2012 who had loretirement savings.left college with an average of 28in student loan debt.ofadultsthenothatthey inhaveVermont graduates of four-year collegesfrom the class of 2012 who had loansU.S.indicatedretirement savings.OF ADULT VERMONTERSleft college with an average of 28,299%in studentloan debt.that they have noHAVE SUBPRIMECREDIT.retirement savings.4711%90 days as of June 2014.34541%of adiOFOF U.S.62U.S.%ADULTSthatThese Vermonters pay a lot more for all credit: auto and home loans and credit card debt.of 15-year-olds – U.S. ranked 9th out of 13loan borrowers wereclassof 2012graduated63 percentof Vermontcolleges in the state.More than half ofof high schoolsin Vermont (7ofoutof 65) haveK-12 FrameworkStandards Financial literacy topics in Vermont’sfinance knowledge.delinquentin their of parents incountries participating in the exam e states receiveda financial literacy graduationrequirement.withstudentloandebt.OF ADULTVERMONTERScollegeseniorsin thepaymentsbythana grade of A, B or C.GRADUATION:and Learning Opportunities on personal finance topicshavenot beenevelopa partnershipamong allVermont colleges to create a Virtual11 percenthaveof moreall studentstatistically tied with Russia.Vermontsetaside funds for DUPON90daysas of sof2012graduatedupdated since the year 2000. Only seven Vermont high schools haveCareerCenter.BIG BANKtheirchild’scollegeeducation.SCREDIT SCOREdelinquent in theirThese Vermonters pay a lot more for all credit: auto and home loans and credit card .Thatsurvey alsowithshows student loan sABCof high schools in Vermont (7 out of 65) havepayments by more thanCreateapilotChildSavingsAccountProgram. Onlypercentparents inAVERAGE LOAN DEBTthat27evenat highofschoolsa financial literacy graduationrequirement.gradein a nationalgave themselves90 days as of June 2014.thatasHAVE SUBPRIME CREDIT.UPON GRADUATION:igh manyschool studentsmake one ofVermontthemostimportantfinancialdecisions Hashaveset alfinancialliteracy testROUGHLY 10%O11%RUSSIALATVIAPOLANDCZECH REPUBLICNEW ANDCZECH REPUBLICNEW ZEALANDVermont has a “D”A B Cin a nationalOECD PISA international gradefinancialliteracy testreport card on stateof 15-year-olds – U.S. ranked9thof 13effortsto outimproveMore than half ofliteracycountries participating infinancialthe examandthe states receivedin high schools.a grade of A, B or C.offered, high schoolThat survey also showsadministrators estimate E stablishgrantsfor K-12 schools to launch new financialliteracy eventhatat highschoolsthat more than two-thirdsthat as many asgrade in a nationalgave themselvesa grade ofwhereeducationthe electiveisgraduateprograms or to improve existing ones.of the report card on statewithoutC,achievingD or F on their personaloffered, high schoolof Vermont high schools may notof 15-year-olds – U.S. ranked 9th out of 13efforts to improvecompetence in financialU63 percent ofadministratorsVermont estimateeven offer a personal finance electiveVERMONTANPLANNOWthanACTIONhalf ofknowledge.S NEEDSMoreliteracyfinancetopics.financial literacycountries participating in the exam andcoursefor theirstudents to take.Nationally,nearlythe states receivedAthanCOLLEGEtwo-thirds COMMITTEEthat morecollege seniorsinTHEtheIn today’sworld, knowinghowsave,spendand investresponsiblyin high schools.a gradeof A,toB orC.FROM11 percent of all studentstatisticallytied withRussia. is an essentialgavethemselvesa grade ofof thestudentsgraduateloan borrowerswereclass of 2012OECD PISA internationalliteracy testlife skill, financialandUVermontjust hasn’t done enough to prepare its citizens for success. Too Offer access to robustfinancialliteracy education opportunities to all graduatedwithoutC, Dachievingor F on their nt in theirof 15-year-olds–U.S.ranked9thoutof13Amany Vermonters are in a financial funk starting at an earlyVermontcollege students.63 age.percent of Vermonteven offer a personal ectivefinance knowledge.payments by more thancountries participating in the exam andNationally, nearlygavethemselves a gradeofof June 2014.literacytopics.days asstudents to take.OECD PISA internationalfinancialliteracytestSomeof themajorchallengeshighlighted in the report: college seniors in thecourse for theirResource and Training Center for use by all Create a Financial 90Literacy11 percent of all studentstatisticallytiedwith Russia.VERMONTefforts to improvefinancial literacyin high schools.REPORT CARDCHINA DSREPORTCARDA63 percent of Vermont63 percent of VermontNationally,nearlycollegeseniorsin thecollegeseniorsintheADULTFINANCIAL11 percent of all studentstatisticallytied d internationalfinancial literacy standards that have beenADULTadoptedby FINANCIALclass of 2012 graduatedloan borrowers wereclass of 2012 graduatedmany states.with delinquentstudentinloandebt.theirwith student loan debt.payments by more thanMore than half ofthe states receiveda grade of A, B or C.To accomplish this, they recommended that the Governor and/or the legislatureUestablish a Vermont Financial Literacy Commission with representationfrom business,SSurvey showsAeducation,andVermont governmenthas a “D”A nonprofitB C organizations.Center for Financial LiteracyCDFROM THE K-12 COMMITTEECOLLEGE gnizing the lack of personal finance education in our schools and colleges,high VERMONTlevels of college student debt, and a lackof adequate retirementand rainy dayLITERACYCOLLEGEFINANCIALLITERACYfunds, the Task Force emphasized that it was imperative to address these problemsin a timely manner.CZECH REPUBLICK-12FINANCIALK-12FINANCIALH E LPI NG VE R MON T E RSBE AT F I NANC IAL F U N Kgrade in a nationalreport card on stateefforts to improvefinancial literacyin high schools.AAUSTRALIAA VERMONT TASK FORCE TAKES ON THE CHALLENGE OF FINANCIAL ILLITERACYVermont has a “D”ESTONIAREPORT CARDCHINAACTION PLANRECOMMENDATIONSVERMONTThe task force divided intothree sub-committees to address the needs of the various to adulthood, and issued recommendations appropriateage groups, from kindergartenfor each sector.UBELGIUMWill Policy Makers MobilizeTo Fight Financial Funk?VERMONT’S FINANCIAL LITERACYCOLLEGEFINANCIAL LITERACYCOLLEGEFINANCIALLITERACCREDIT SCORE15a grade ofVONT personalA D U LT SC, EDRorMF ontheirdo not have afinance knowledge.IN CASE OFEMERGENCY,BREAK PIG47%Lretire“rainy day fund,”a liquid emergencyfund that wouldcover three monthsof life’s necessities.OF ADULT VERMONHAVE SUBPRIME CRThese Vermonters pay a lot more for all credit:22 auto and home loans and62BIG BANK 9,667. 00VERAverage credit carddebt of adult Vermonter.LESS THAN50%of Vermont workersparticipate in anemployment-basedretirement plan.YEAR IN REVIEW–7IN CAEMERBRE

PRE-CLASS,39%OF TEACHERS AGREEDOR STRONGLY AGREED WITHTHE STATEMENT BELOW.Each year, participantsresponded to the statement“I have the knowledgenecessary to effectively teachmy students about personalfinance”with one of thefollowing: strongly disagree,disagree, neutral, agree orstrongly agree.POST-CLASS,94%OF TEACHERS AGREEDOR STRONGLY AGREED WITHTHE STATEMENT ABOVE,AN INCREASE OF 141%OVER PRE-TEST RESULTS.EXPONENTIAL RESULTSNearly 100 teachers from78 percent of Vermont’ssupervisory unions haveparticipated in the highschool financial literacyeducation pilot program.That may not sound like a lotbut the trickle down effect isexponential. Within a decade,more than 37,000 students canbe expected to benefit fromtheir knowledge.High School Pilot ProgramFinancial Literacy AssessmentTHE PROGRAM’S FINAL PHASE WILL SHOW THAT HIGHLYA STANDARDIZED TEST IS NEEDED TO MEASURE PERSONAL FINANCE EDUCATIONTRAINED EDUCATORS MAKE A DIFFERENCEThe Center believes that trained teachers are the key to solid personal financialeducation. A five-year educator training and high school financial literacy educationpilot program was begun in 2011. The program was set up so that it would be possibleto compare the knowledge and behaviors of high school students who have taken apersonal finance course taught by highly-trained educators with a control group ofstudents who have not received classroom instruction on this important topic. Theresults will be released in the fall of 2015 with our partner on this project, the NationalEndowment for Financial Education (NEFE).TRAINING THE TRAINERThe first step was to train teachers. For the first three years of the program, MerchantsBank funded a Summer Institute at Champlain College for middle and high schooleducators. This financial literacy boot camp covered saving and investing, creditreports and scores, credit and debt, managing risk, income and careers—in short, thefinancial knowledge needed to navigate daily life. The Summer Institute was one ofthe few places in the nation where an educator could earn a master’s degree creditin learning how to teach personal finance. The Summer Institute educator trainingprogram was also recognized by the White House in a report issued in 2012.If we can obtain funding, we would like to offer this graduate degree training toeducators again in the near future.TAKING MEASUREMENTSThe next two years were spent following 11 teachers in the classroom in order toquantify the results of the training. The Center is currently in the final phase ofgathering data and will publish the results this fall. We already know that trainedteachers feel significantly more confident. Pre-class training, only 39 percent ofteachers felt they had the knowledge to effectively teach personal finance, whereas afterthe class, 94 percent felt qualified. An added benefit is that participating teachers alsoreported changing their own financial habits in a positive way as a direct consequenceof their training.CREATING A PROFESSIONAL COMMUNITYAlthough the training program was Vermont-based, the ultimate goal is to make thistype of educator training available nationally. The Center is developing a websitethat will go live in November 2015 as a high school resource for educators created byeducators. This will be a trusted source that will enable teachers to see what their peerswho have successfully taught personal finance are doing and what works for them.The site will include recommendations from teachers at the pilot schools about bestpractices and effective instructional tools.FROM ELECTIVE TO REQUIREMENTAll of the pilot high schools involved in the program have made personal financeeducation a graduation requirement. Ideally, this subject would be a high schoolgraduation requirement nationwide.The Center for Financial LiteracyCurrently, there is no unbiased assessment vehicle to measure what high school andcollege students are learning in personal finance courses. The types of standardizedassessments that are used for math, history, social studies, science, etc., have not beenwritten for personal finance. Ironically, there is an international test (OECD PISA testfor 15-year-olds) but not a national one in the U.S.The Center is in the process of developing a financial literacy assessment for highschool seniors and first-year college students. The purpose of the assessment is todetermine the financial skill level of students as they prepare to graduate high schoolor enter college. We have completed the first phase of this project. We have createdapproximately 400 assessment questions, covering more than 40 topic areas, with thehelp of a nationally recognized assessment firm. The questions have also been reviewedby a group of expert high school and college educators.The next phase of the project is to use these questions with students in the classroom.Before that occurs, the Center must obtain additional funding for a multistate fieldtest and validation study.PUTTING FINANCIALLITERACY TO THE TESTThe Center is developing afinancial literacy assessment forhigh school seniors and firstyear college students.TESTING FINANCIAL SAVVYThe primary goal is to have an assessment exam for high school teachers to use.However, it could also be used by colleges to assess incoming first-year students, andagain with college seniors to determine their financial preparedness. An effective testwill measure the full range of knowledge and skills identified as critical to being aparticipant in the economy without relying on any specific curriculum or instructionalmodel. An assessment test will let educators know what is working in the classroomand what areas students are struggling with. A strong assessment tool will helpeducators be much more effective when teaching these topics.Baby StepsRESEARCH SHOWS EARLY SAVINGS MAKE COLLEGE ATTAINABLEChildren can be guided toward the path for saving smart right from birth. John Pelletierparticipated in a roundtable on Children’s Savings Accounts at the Federal Reserve Boardof Boston which focused on research showing that low- and moderate-income childrenwith savings—even when under 500—were three times as likely to enroll in college andfour times as likely to graduate than such children with no savings.EARLY SAVINGS GENERATE HOPEThe roundtable enlisted experts from around the country to discuss this kind of assetbuilding as an antidote to poverty. It’s believed that these accounts not only makecollege appear more attainable but also can have a positive effect on an entire family’smotivation to accumulate assets. Perhaps such accounts can even have an effect onbreaking the cycle of poverty. The Center is an active supporter of efforts to help morelow- and moderate-income students open such saving accounts.A PENNY SAVEDIMPACTS LIKELIHOOD OFCOLLEGE GRADUATESChildren with savings accountsare three times as likely toenroll in college and four timesas likely to graduate.YEAR IN REVIEW–9

CHAMPLAIN COLLEGENational Report CardThe Center forFinancial LiteracyMOST STATES WOULD NOT TAKE THEIR REPORT CARDS HOME TO MOM & DADNationalReportCardWhen it comes to report cards, everyone wants an A. But when the Center graded 50states on their financial literacy education, only seven states earned an A. Sadly, 30states received grades of C, D or F.on State Efforts to ImproveFinancial Literacy in High SchoolsThe first “National Report Card on State Efforts to Improve Financial Literacy in HighSchools” was issued in 2013, and the Center will release another one in 2015. The goalis to produce a “National Report Card” every other year.MAKING BETTER GRADESBy John PelletierSummer 2013WHICH STATESMEET THE MARK?Only seven states earnedan A, while most received aC or lower.

with student loan debt. Nationally, nearly 11 percent of all student loan borrowers were delinquent in their payments by more than Vermont graduates of four-year colleges from the class of 2012 who had loans le college with an average of 28,299 in student loan debt. AVERAGE LOAN DEBT 28,299 UPON GRADUATION: 1% 2012 Only 27 percent of parents in