Transcription

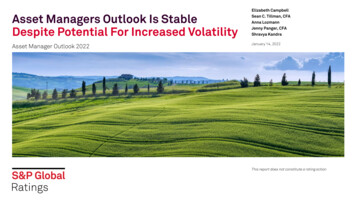

Asset Managers Outlook Is StableDespite Potential For Increased VolatilityAsset Manager Outlook 2022Elizabeth CampbellSean C. Tillman, CFAAnna LozmannJenny Panger, CFAShravya KandraJanuary 14, 2022This report does not constitute a rating action

Key Takeaways– Our outlook on both the traditional and alternative asset managers remains stable for 2022.– We are assigning a stable outlook to wealth managers for 2022.– We believe that the upsides and downsides are roughly balanced across subsectors--albeit for different reasons--and expect an equalnumber of upgrades and downgrades prospectively, consistent with our rating actions over 2021. That said, we believe that alternativeasset managers are better positioned compared with their traditional peers.– In our view, wealth managers are uniquely positioned within the sector because their business model is highly dependent upon clientrelationships. They offer a variety of services, and outperformance relative to benchmarks is only one small component. Consequently,they have a stickier asset base than traditional asset managers, though they are similarly vulnerable to market movements.– Mergers and acquisitions (M&A) remain a focal point. 2020 and 2021 saw a series of large acquisition announcements, both within thesector and involving banks and insurance companies. While the size of the deals may taper, we expect M&A to be a key strategy in thesector as firms reach for greater scale, capital, and capabilities.– In the U.S., which represents the largest pool of assets under management (AUM) and where the majority of rated asset managers arebased, S&P Global Economists expect 3.9% U.S. real GDP growth in 2022, after 5.5% growth in 2021. U.S. unemployment is forecast todecline to 4.0% by the end of 2022, after ending 2021 at 5.4%. Given the high inflation readings, the Federal Reserve is expected tospeed up tapering; we now expect three rate hikes in 2022. The average S&P 500 value is projected to be approximately 4,690 in 2022 –essentially flat, on average, for the year. Ongoing supply bottlenecks and pickup in COVID-19 cases continue to pose a downside risk.

Global Asset Managers 2021 Rating ActionsCompanyDateRating/Outlook ActionsMariner Wealth Advisors, LLCDecember 2021Downgraded to 'B-'; Outlook StableCORESTATE Capital HoldingsNovember 2021'BB-' Ratings Placed on CreditWatch NegativeVictory Capital Holdings, Inc.November 2021Outlook revised to Stable from Positive at 'BB-'Carlyle GroupOctober 2021Outlook Revised to Positive from Stable at 'BBB 'Vida Capital Inc.September 2021Downgraded to 'B-'; Outlook NegativeVirtus Investment PartnersSeptember 2021Upgraded to 'BB '; Outlook StableNoah Holdings Ltd.August 2021Outlook revised to Stable from Negative at 'BBB-'Waddell & Reed Financial, Inc.August 2021Upgraded to 'BBB'; Outlook StableBrightSphere Investment Group Inc.August 2021Downgraded to 'BB '; Outlook StableIntermediate Capital Group PLCJuly 2021Outlook revised to Positive from Stable at 'BBB-'Mariner Wealth Advisors, LLCJuly 2021Assigned 'B' Rating; Outlook StableHunt Cos. Inc.June 2021Outlook revised to Stable from Negative at 'BB-'Grosvenor Capital Management Holdings, LLLPJune 2021Outlook revised to Negative from Stable at 'BBB'Clipper Acquisitions (TCW)June 2021Outlook Revised to Positive from Stable at 'BB 'Blue Owl Capital Inc.May 2021Assigned 'BBB' Rating; Outlook StableApollo Global ManagementMay 2021Outlook Revised to Positive from Stable at 'A-'BrightSphere Investment Group Inc.May 2021'BBB-' Ratings Placed on CreditWatch NegativeFEH Inc.April 2021Outlook Revised to Negative from Stable at ‘BB’Allspring Buyer LLCApril 2021Assigned 'BB-' Rating; Outlook StableHightower Holding LLCApril 2021Assigned 'B-' Rating; Outlook StableCORESTATE Capital HoldingsMarch 2021Downgraded to 'BB-'; Outlook StableEaton Vance Corp.March 2021Downgraded to 'BBB '; Outlook StableCompass Diversified Holdings Group LLCFebruary 2021Outlook revised to Stable from Negative at 'B 'Victory Capital Holdings Inc.February 2021Outlook revised to Positive from Stable at 'BB-'Grosvenor Capital Management Holdings, LLLPFebruary 2021Assigned 'BB ' Rating; Outlook StableBrightSphere Investment Group Inc.February 2021Outlook revised to Stable from Negative at 'BBB-'KKR & Co.February 2021'A' Ratings Affirmed, Removed from CreditWatch Negative; Outlook StableFinCo I LLC (Fortress)January 2021Outlook revised to Stable from Negative at 'BB'Virtus Investment PartnersJanuary 2021Outlook revised to Positive from Stable at 'BB'Source: S&P Global Ratings.3

Key Takeaways – Traditional Asset Managers– We maintain our stable outlook on the traditional asset managers, which we assigned at the beginning of 2021.– The stable outlook reflects our belief that, over the next year, prolonged industry headwinds will be roughly offset by elevated--albeitmore volatile--asset prices, supporting AUM levels and margins.– To be clear, we do not expect the decades-long headwinds to the traditional asset managers to wane in 2022. Our view stillincorporates a further shift to passive investing, contributing to fee compression and outflows, offset by record valuations acrossasset classes.– There are growing market risks from supply bottlenecks, high inflation, fading of global central banks’ monetary stimulus, and risingCOVID-19 cases, which could impact global markets and provide a headwind for traditional asset managers. We believe that theserisks will be expressed through higher realized volatility rather than outright equity market declines or outsized spread widening.

Key Takeaways – Alternative Asset Managers– We maintain our stable outlook on the alternative asset managers, which we initially assigned in 2020.– We continue to believe that alternative asset managers are less exposed to many of the challenges facing the traditional managerssince their AUM is largely locked up, and strategies are harder to index. Alternative asset managers have seen significant net inflowsas a result of good investment returns and general expansion--both in size of average fund and broadening platforms.– Our areas of focus for 2022 include realization activity and investment performance, both of which we expect to be strong.Furthermore, 2020 and 2021 witnessed high levels of capital deployment, and we will be monitoring if the pace can continue in 2022.Finally, we believe fundraising could become more mixed as investors focus on performance, fees, and their allocation levels toalternatives.– The majority of large alternative managers have already formed partnerships with insurance companies and, as such, we believe thatmost large deals are behind us. That said, we expect these partnerships to begin to grow through pension risk transfer or blockacquisitions as well as organically.– We believe that smaller--not covered alternative asset managers--could be targets of large, traditional asset managers seeking tobroaden their capabilities.

Key Takeaways - Wealth Managers– We are assigning a stable outlook on the wealth management segment.– The stable outlook reflects our belief that the strengths of their client-focused business model--which provide a sticky asset base andconsequently recurring revenues--are largely offset by highly levered balance sheets, aggressive inorganic growth, and elevated assetprices.– Due to the nature and range of wealth manager services (including investment advisory, tax planning, estate planning, insuranceguidance, etc.), managers are less exposed to the headwinds that the traditional asset managers face, namely clients’ focus oninvestment performance. As a result, wealth managers’ net flows are generally more stable.– Risks to the sector stem from the rapid pace of inorganic growth using increasing amounts of leverage. The industry remains highlyfragmented with growth almost entirely driven by M&A. Although integration risk is low, near-term operating costs could remainelevated. Finally, heightened competition for acquisitions has increased the multiples paid for advisors.– Additionally, wealth advisors are exposed to the same market risk that traditional asset managers face.

Industry–Specific Items We Are Monitoring– We are monitoring several focal points for active management: performance, lowering leverage, M&A, and environmental, social, andgovernance (ESG).– Outperformance continues to be elusive while the shift to passive has pressured fees and fund flows. With both monetary and fiscalpolicy supporting markets, beta has eclipsed alpha over the past decade, providing a strong boost to passive strategies. 2022 could bemore of a transition year as our expectation for higher volatility may translate into greater alpha generation for active managers.– Few companies have repaid debt over the past several years; instead, they have relied on market appreciation to lower leverage on theirbalance sheets. We continue to prioritize lowering leverage through repayment over EBITDA growth.– The industry has seen strong M&A activity in recent years, and we expect this trend to continue. We expect consolidation within theindustry, though cross-sector activity may also continue.– We expect increased focus on ESG factors in response to evolving investor preferences and public interest. Many asset managers haveaddressed this at a company level through board or employee diversity initiatives, as well as at an investment level through ESGfocused funds and conducting ESG ratings on existing investments.– We recently published our ESG credit indicators for global investment holding companies. Our ESG credit indicators provide additionaldisclosure and transparency at the entity level and reflect our opinion of the influence that ESG factors have on our credit ratinganalysis. They are not a sustainability rating or an S&P Global Ratings ESG evaluation.

Company–Specific Items We Are MonitoringRating actions will continue to be idiosyncratic as different companies will be better able to navigate the headwinds.– Given ratings positioning, market levels, and idiosyncratic changes in leverage, we could see some ratings upside over 2022. That said,we continue to view lowering leverage through debt repayments as a stronger catalyst for financial profile improvement versus loweringleverage through rising EBITDA, which may prove less sustainable through a market cycle.– The need for scale, broader capabilities, and client portfolio customization has been a key driver for recent M&A activity. Dependingupon how acquisitions are financed and executed, ratings could be affected.– Larger asset managers are seeing increased scrutiny around their investment stewardship practices. ESG investment products are anincreasing focal point.– For companies with key-person risk, management transition and succession planning remain a credit consideration.– Some asset managers have large cash balances. Because we net surplus cash from funded debt in our view of leverage, projections ofhow and when this cash is deployed could affect our view of leverage.– Share repurchases and debt-funded dividend activity, although not widespread, could erode liquidity and increase leverage.

Rating And Outlook SnapshotRatings DistributionAA-, 2%A , 4%A-, 8%A , 15%BBB , 13%BBB, 9%BBB-, 4%BB , 9%BB, 9%BB-, 11%B , 4%B, 2%B-, 8%CCC ,2%Outlook DistributionCW Negative, 2%Negative, 13%Positive, 8%Stable, 77%As of Jan. 3, 2022. Includes asset managers and investment holding companies. Source: S&P Global Ratings.9

Traditional Asset Managers Credit OverviewOur credit outlook for traditional asset managers is stable.Key rating factors:– Mixed investment performance of active managers (particularly in equities) relative to benchmarks.– Passive offerings continue to gain market share.– Fee pressure for active managers driven by growth of passive strategies.– Redemption risk, as AUM is not locked-in.– Exposure to fluctuations in financial markets absent organic growth.– Potential for outsized (e.g., relative to free-cash-flow) share repurchases and dividends.Mitigating factors:– Continued economic recovery and easing supply bottlenecks could support financial markets in 2022.– Highly flexible operating structure along with financial policy flexibility.– Few maturities coming due in 2022.– Very low refinancing risk as most managers have already capitalized on low interest rates and refinanced near-term maturities.– Ratings positioning adequately captures the risks of the traditional sector, in our view.Outlook triggers:– Sustained and prolonged market declines, debt-fueled M&A or capital distributions, or significantly weaker operating performance ornet flows could cause us to revert to a more negative view of the sector.– Conversely, we could consider a more positive view of the sector if we see improving investment performance and organic growth andlower leverage driven by debt repayment amid a benign macro economic backdrop.

Alternative Asset Managers Credit OverviewOur credit outlook for alternative asset managers is stable.Key rating factors:– Credit metrics for alternative asset managers, while largely stable, are unlikely to strengthen.– Realization activity should remain strong in 2022.– The investment landscape remains very competitive, and AUM growth this cycle is reflected in larger fund sizes andnewer strategies that may not have seasoned track records.– Fee generation prospects (growth in capital not yet earning fees) and earnings mix toward more stable sources(management fees versus performance fees) provide visibility into future earnings.– Liquidity for many is very high, but prospects are uncertain regarding ultimate deployment.– Investors or regulators could bring more attention to return disclosures.Positive outlook trigger:– A larger portion of fee-related earnings, successful performance during a downturn--particularly with newer strategies-and relatively conservative financial policies would be considerations for a more favorable view of the sector.Negative outlook trigger:– Protracted severe market dislocation could quickly pressure EBITDA and, ultimately, leverage. Increasingly shareholderfriendly financial policies could weaken financial profiles. Stumbles in newer strategies or riskier investment pursuitspose risks as well.

Wealth Managers Credit OverviewOur credit outlook for wealth managers is stable.Key rating factors:– We don’t expect a material improvement in credit metrics over 2022.– We expect the pace of M&A to continue in 2022 and believe that debt will be the primary means to fund inorganic growth,potentially stretching leverage metrics.– With access to cheap abundant capital, deals have become more competitive.– Wealth advisory focuses on an array of services - of which investment performance is one small component – leading tohigh client retention, and consequently, strong recurring revenues.– Market declines or spread widening could result in lower client balances.Positive outlook trigger:– We could take a more positive view of the sector if companies de-levered their balance sheets through repayment of debt,not EBITDA growth alone.– A slowing of the pace of M&A would provide greater transparency into true operating power and margins, allowing forbetter assessment of business sustainability through a cycle.Negative outlook trigger:– Protracted severe market dislocation could quickly pressure EBITDA, and ultimately, leverage. Additional, debt fundedacquisitions could result in downgrades as current leverage levels are among the highest within the broader assetmanagement space.

M&A Landscape Smaller Deals Ahead?We expect M&A activity could shift toward smaller acquisitions, as opportunities for large-sized deals have largely played out over the pastseveral years.We believe that large “mergers of equals” among asset managers may be less common as the strategic rationale for cost-savings oradditional capabilities among large firms has already been played out, in our view.– That said, Janus Henderson and Invesco could undergo significant M&A over 2022 since Trian Partners--an activist investor--has largestakes in both firms.Moreover, we believe that alternative asset managers acquiring insurance companies is now in the rearview mirror.– KKR/Global Atlantic, Apollo/Athene, etc. (see next page for more details).From our perspective, the most likely path forward for M&A is for traditional asset managers to acquire smaller, not-rated, alternative assetmanagers, in order to diversify AUM while providing locked-up capital.– We witnessed this at the end of 2021 with Franklin acquiring Lexington Partners, T. Rowe Price (not rated) acquiring Oak Hill, and VictoryCapital acquiring New Energy Capital Partners, for example.Growth through acquisition will be the primary means to scale within the wealth management subsector. As previously mentioned, the wealthmanagement industry is highly fragmented, with growth almost entirely driven by debt-fueled acquisitions. As long as market values remainelevated and credit remains abundant and cheap, we expect the pace of M&A to continue during 2022. We expect competition to increase,which could result in higher acquisition multiples and heightened latency risk should market values decline from present levels.13

Recent M&A Asset Managers And InsurersAsset ManagerInsurance CompanyDate AnnouncedDate closed or expected to closeApollo Global Management Inc.Athene Holding Ltd.March 8, 2021January 3, 2022Blackstone Group Inc.Allstate Life Insurance Company(ALIC; renamed Everlake Life Insurance January 26, 2021post-close)November 1, 2021OwnershipPost close, Apollo's current shareholders willown 76% of the combined entity.The remaining 24% will be owned by Athene'scurrent shareholders.To be majority owned by an investmentvehicle managed by Blackstone.Blackstone will enter into an assetmanagement agreement for ALIC'sinvestments.AUM*All of Athene's US 175 billion GrossInvested Assets are already managed byApollo, as of December 31, 2020.US 28 billionIn connection with the transaction,Blackstone entered a long-term strategicBlackstone purchased a 9.9% equity interest asset management partnership within the parent company of AIG's Life &AIG's life and retirement business, inRetirement business.which it will manage an initial 50 billionof assets, increasing to 92.5 billion overthe next six years.BAM will ultimately acquire an aggregateBrookfield Asset Management Partners19.9% ownership in AEL's common equity(BAM's reinsurance and annuityand will become a reinsurance counterparty subsidiary) may ultimately reinsure upof AEL.to 10 billion in annuity liabilities.We believe there may be opportunitiesBrookfield Reinsurance (a subsidiary of BAM) for BAM to enhance the yield in Americanwill acquire American National for 5.1 billion National's investment portfolio, butin an all-cash transaction.there is still uncertainty around thedetails of the exact investment strategy.Blackstone Group Inc.AIG's Life & Retirement businessJuly 14, 2021November 2, 2021Brookfield Asset Management Inc.(BAM)American Equity Investment LifeHolding Company (AEL)October 18, 2020October 11, 2021Brookfield Asset Management Inc.(BAM)American National Group Inc.August 9, 2021First half of 2022Ares Management Corp.Aspida Life Re Ltd. (f/k/a F&GReinsurance Ltd.)September 30, 2020December 18, 2020100% owned by Aspida Holdings Ltd., anUS 2 billionindirect subsidiary of Ares Management Corp.February 1, 2021KKR owns a controlling interest in GAFG ofapproximately 60%.Remaining 40% owned by new and previousGAFG investors and leadership team.US 90 billion at time of close.June 2, 202071.5% owned by Carlyle and a Carlylemanaged fund (including 19.9% stakeacquired by Carlyle in November 2018),25% owned by T&D Holdings, and3.5% owned by AIG.At the time of the close, Fortitude Re hadapproximately US 34 billion in AUM, ofwhich Carlyle expects to manage US 6billion.KKR & Co. Inc.The Carlyle Group Inc.Global Atlantic Financial Group Ltd.Fortitude Reinsurance Company Ltd.July 8, 2020November 25, 2019*Incremental AUM from the Insurance Company at transaction close (or at announcement if transaction has not been completed yet). Source: Company data, S&P Global Ratings.14

Industry Headwinds Remain UnabatedU.S. Equity Cumulative FlowsCumulative active flowCumulative passive flow– Capital is being allocated from activedomestic equity toward passiveproducts.Cumulative passive ETF2,000– Exchange-traded funds (ETFs)dominate this shift.1,000– Low or no fees, as well as performance,have been key drivers.Bil. 0– Active managers have largely beenunable to consistently outperform netof 201220132014201520162017201820192020Source: Investment Company Institute, S&P Global Ratings.15

Fee And Cost Pressure ContinuesU.S. Mutual Fund Expense RatiosEquityHybridBondMoney market1.201.00– Alternative asset managers are lessexposed to fee pressure. However, theymay experience average lower fees ifthey offer discounts to large investors.0.80%– Traditional asset managers have facedsignificant fee pressures from the shiftto passive.0.60– Traditional asset managers’ revenuesare highly correlated to market values.In contrast, alternatives benefit fromfees earned based on committed orinvested capital, which is not sensitiveto market 999199819970.00Source: Investment Company Institute, S&P Global Ratings.16

Alternatives Continue To GrowBenefiting From Strong Investor AppetitePrivate equityReal estateInfrastructurePrivate debt– The search for yield is one driver of thegrowth in AUM allocated to alternativeinvestments.Natural resources6,000– Fees for this asset class are lesssubject to pressure because of thecomplexity of replicating thesestrategies in passive vehicles.5,000Bil. 4,000– Competition for good deploymentopportunities is growing as alternativeasset managers broaden capabilities.3,0002,000– Many alternative asset managers haveexpanded their private credit/directlending business, and we expect this tocontinue to be a growth area in 92020Source: Preqin, S&P Global Ratings.17

Ratings With Heightened Downside RiskGlobal Asset Managers And Holding CompaniesCompanyCI Financial Corp.CORESTATE Capital Holding S.A.Long-term issuer creditrating/outlookBB-/Watch NegBB/NegativeIcahn Enterprises L.P.BB/NegativeResolute Investment Managers, Inc.Russell Investments Cayman Midco, Ltd.Vida Capital, Inc.Performance fee orientedSpeculative gradeBBB/NegativeFEH, Inc.Grosvenor Capital Management Holdings LLLPEquity orientedXXBB /NegativeXB /NegativeBB-/NegativeB-/NegativeX2021 forecasted leverageDownside trigger3.0-3.53.0X4.5-5.54.0X4.4-4.75.0X 60%*60%*X 3.03.0X4.8-5.25.0X4.0-5.05.0X6.0-6.5-*LTV ratio. Source: S&P Global Ratings.– We view these ratings at risk because of rising leverage, either through additional debt or weaker performance, significant net outflows,pressure on interest coverage due to earnings compression, liquidity pressure, or weakening competitive advantage.– Although not (yet) included on this list, we consider those traditional asset managers with persistent sizeable net outflows (see next slide)as potentially vulnerable to negative outlook or rating actions longer term.– Valuations across asset classes and geographies are extremely elevated by historical standards over a multitude of metrics. Systemic (i.e.,beta) changes in investor risk appetites could bring about a swift decline in asset prices, providing a catalyst for ratings actions.– Regulation is increasing globally on average; however, changes in the regulatory landscape remains an idiosyncratic risk among countries.18

Persistent Net Outflows – Selective Names– By no means an exhaustive list, we highlight that several large traditional asset managers have struggled with persistent net outflowsover the past several years.– Our expectation is for this to continue, on average, over 2022.– We also believe that increasing volatility could create a more positive backdrop for active management – particularly in equity strategies.Net Flows As Percentage Of Previous Year’s Ending AUM201820192020Sept. 30, 20215%0%-5%-10%-15%-20%Affiliated Managers Group,Inc.1)Franklin Resources Inc.Calculations for W&R excludes wealth management assets.Franklin Resources fiscal year end is Sept. 30.Calculation for Invesco excludes its cash management AUM.The acquisition of W&R by Macquarie Group was completed on Apr. 30, 2021Source: Company data, S&P Global Ratings.Invesco Ltd.Janus Henderson Group PLCLazard Group LLCVirtus Investment PartnersInc.Waddell & Reed FinancialInc.

Traditional Asset Managers Rating Factor AssessmentsCompanyBusinessRisk ProfileFinancialRisk ProfileFinal gement& GovernancePeerAdjustmentSACPGroup StatusICROutlookAffiliated Managers Group, gSatisfactoryFavorablebbb BBB StableAllianceBernstein FS-5AdequateFairNeutralbb-Not applicableStrategicallyimportantNot xceptionalStrongNeutralaa-Not applicableAA-StableAllspring Buyer LLC (Wells Fargo Asset Management)BlackRock, Inc.BrightSphere Investment Group Inc.CI Financial Corp.Clipper Acquisitions Corp.FEH Inc.FIL Ltd.WeakModestbb NeutralNeutralStrongFairNeutralbb Not applicableBB quateSatisfactoryNeutralbbbNot applicableBBBNegativeFairIntermediatebb NeutralNeutralExceptionalFairNeutralbb Not applicableBB vorablebbNot tralNeutralExceptionalFairNeutralbbbNot xceptionalFairNeutrala Not applicableA StableFranklin Resources atisfactoryNeutralaAStableIGM Financial Inc.SatisfactoryModestbbb Invesco gSatisfactoryFavorablebbb Not applicableModeratelystrategicNot applicableBBB StableFMR toryFavorablebbb Not applicableBBB StableLazard Group LLCSatisfactoryModestbbb NeutralNeutralExceptionalSatisfactoryNeutralbbb Not applicableBBB StableNeuberger Berman Group LLCSatisfactoryModestbbb NeutralNeutralExceptionalSatisfactoryNeutralbbb BBB StableNuveen Finance LLCSatisfactorySignificantbb Aggressiveb NeutralFS-5AdequateFairNeutralb Not applicableStrategicallyimportantNot applicableB utralbb-Not xceptionalSatisfactoryNeutrala-Not b-Not applicableCCC StableJanus Henderson Group PLCResolute Investment Managers, Inc.Russell Investments Cayman Midco, Ltd.abrdn plc (f/k/a Standard Life Aberdeen PLC)Victory Capital Holdings, FS-5AdequateFairNeutralbb-Not applicableBB-StableVirtus Investment Partners Inc.FairIntermediatebb NeutralNeutralStrongFairNeutralbb BB StableWeakMinimalbb NeutralNeutralStrongFairFavorablebbb-Not in Parent Holdco LLCWaddell & Reed Financial Inc.VulnerableSource: S&P Global Ratings.20

Alternative Asset Managers Rating Factor AssessmentsCompanyBusinessRisk ProfileFinancialRisk ProfileFinal gement &GovernancePeerAdjustmentApollo Asset Management Inc.SatisfactoryModestbbb NeutralNeutralExceptionalSatisfactoryAres Management Corp.SatisfactoryModestbbb FairMinimalbbbNeutralStrongIntermediatebbb Citadel Limited PartnershipFairModestEIG Management Company, LLCFairFinco I LLCGroup StatusICROutlookFavorablea- Not applicableA-PositiveSatisfactoryNeutralbbb Not applicableBBB StableExceptionalStrongUnfavorablea Not applicableA StableNeutralStrongFairNeutralbbb Not gNeutrala- Not actoryFavorablebbb Not uateFairNeutralbb Not Franklin Square Holdings LPFairIntermediatebb NeutralNeutralAdequateFairUnfavorablebb Not applicableBBStableGrosvenor Capital Management Holdings LLLPFairIntermediatebb NeutralNeutralAdequateFairNeutralbb Not applicableBB NegativeIntermediate Capital Group gSatisfactoryNeutralbbb- Not applicableBBB-PositiveKKR & Co. Inc.SatisfactoryModestbbb PositiveNeutralExceptionalSatisfactoryFavorablea Not applicableAStableOaktree Capital Group, atisfactoryNeutralModeratelystrategicA-StableThe Carlyle Group Inc.SatisfactoryModestbbb NeutralNeutralExceptionalSatisfactoryNeutralbbb Not applicableBBB irNeutralb- Not applicableB-NegativeBlackstone Group Inc.Blue Owl Capital Inc.Brookfield Asset Management Inc.Vida Capital Inc.SACPa-Source: S&P Global Ratings.21

Wealth Managers Rating Factor AssessmentsCompanyFocus Financial Partners Inc.BusinessRisk ProfileFinancialRisk iquidityManagement &GovernancePeerAdjustmentSACPGroup quateFairNeutralbb-Not b- Not ralb-Not applicableB-StablebNeutralFS-6AdequateFairNeutr

KKR & Co. February 2021 'A' Ratings Affirmed, Removed from CreditWatch Negative; Outlook Stable FinCo I LLC (Fortress) January 2021. Outlook revised to Stable from Negative at 'BB' Virtus Investment Partners: . - The majority of large alternative managers have already formed partnerships with insurance companies and, as such, we believe .