Transcription

Magic Quadrant for CRM and CustomerExperience Implementation Services,WorldwidePublished: 1 December 2016ID: G00299019Analyst(s): Patrick J. Sullivan, Ed ThompsonCustomer experience and CRM implementation services continue to be inhigh demand, fueled by digital business transformation. Here, we positionthe largest customer experience and CRM consulting and implementationservice providers to help enterprises identify providers that best fit theirneeds.Strategic Planning AssumptionsThrough 2019, the total market for consulting and implementation services for CRM and customerexperience (CX) will be 1.4 times the market for CRM software, with the ratio of service to softwaregrowing over that time.By 2018, more than half of organizations will implement significant business model changes in theirefforts to improve CX.Market Definition/DescriptionGartner defines the CRM and CX implementation service market as project-based services to helpform a customer relationship or CX strategy and/or design, build, integrate and deploy processchange and technology solutions that improve interactions between organizations and theircustomers.These projects have goals set out by sales, marketing, customer service, field service and digitalcommerce leaders, such as improving customer satisfaction, acquiring new customers, retainingexisting customers, creating a single view of the customer, cross-selling or upselling to customers,improving campaign response rates, driving up customer advocacy or referrals, and gaining bettermargins through improved pricing.There are seven primary differences between CRM and CX:1.The roles involved with CRM in an organization are a subset of those involved with CX.

2.The permanence of CX operational capability differs from the transience of a CRM project.3.A CX initiative typically coordinates several projects, while a CRM project stands alone.4.More time is needed to demonstrate the benefits of a superior CX.5.The association with technology is greater in CRM.6.The focus for CRM is on actions taken; in CX, it is the customer's perception of the actions.7.A rational approach is more important in CRM; in CX, the customer emotions matter more.For more, see "How to Tell the Difference Between Customer Experience and CRM Projects."CRM projects tend to focus on more-traditional CRM technology implementations for sales,marketing, customer service, field services and digital commerce. They primarily first deploy coreCRM system-of-record applications and then add supporting technologies to enhance the core.Over 80% of these projects involve the deployment of technology, and over 75% of these projectsutilize CRM packaged software (rather than building custom solutions). The CRM softwarepackages that are the most typical systems of record include Salesforce, Microsoft Dynamics CRM,SAP CRM, Oracle Siebel, Oracle CX Cloud, SAP Hybris, Adobe Marketing Cloud, Pegasystems andIBM Commerce. Salesforce and Microsoft Dynamics CRM together account for 54% of the CRMimplementation service projects, with the remaining 46% spread across all other CRM packages.This part of the market includes projects that upgrade or adapt existing CRM applications,particularly when extending this to improve usability and analytics.CX projects encompass a far wider range of activities that are enterprisewide initiatives reachingbeyond sales, marketing and customer experiences and extend into operations, supply chain,billing, logistics and other departments. Only 50% of these projects involve the deployment oftechnology (see "Survey Analysis: Customer Experience Management Leadership"). They are oftendriven to change or transform the business operations and modes of interaction with customers.The goals of these projects are aiming to increase customer satisfaction, loyalty and advocacy (see"The Definition of Customer Experience Management"). The skills needed for these projects tend tobe more creative and design-oriented, but it also requires analytics and process skills, includingbusiness process transformation, digital commerce knowledge, information architecture/migration,customer analytics and digital design.This market includes the work done by digital agencies as part of CRM or CX implementationefforts, but it excludes work done by brand agencies for chief marketing officers in branding, mediabuying, image projection and strategic marketing initiatives.Page 2 of 37Gartner, Inc. G00299019

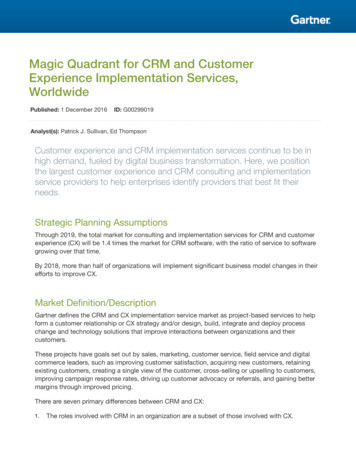

Magic QuadrantFigure 1. Magic Quadrant for CRM and Customer Experience Implementation Services, WorldwideSource: Gartner (December 2016)Gartner, Inc. G00299019Page 3 of 37

Vendor Strengths and CautionsAccentureAccenture is positioned in the Leaders quadrant due to market presence, vision and digitalorientation. Accenture leverages resources across business units, with Accenture Strategy settingthe vision, Accenture Consulting leading in business transformation and Accenture Digital providingdesign, digital marketing and analytics, while Accenture Technology takes the lead on CRMtechnology integration. Accenture is a good fit for large enterprises needing complex or industryspecific transformational efforts requiring multiple disciplines. Gartner estimates that Accenture isthe largest CRM and CX service provider, with revenue estimated to be 3 billion (around 10% ofAccenture's total revenue and 20% of its consulting and implementation revenue). The top fiveindustries for its CRM and CX services are banking, retail, consumer goods, telecom/media andutilities/energy.Strengths Digital business transformation and CX vision — Accenture is strongest at the intersection ofbusiness and technology with a focus on digital and CX services. It has steadily invested insolutions, skills, practitioners and practices that encompass business, technical and domainskills across all major CRM software and CX. Accenture perceives CX services to be outcomedriven, requiring end-to-end services to improve clients' business results. Accenture is strong atleveraging resources across business units, with Accenture Consulting leading businesstransformation, Accenture Interactive providing design, digital marketing and analytics, andAccenture Technology providing CRM technology integration. Accenture conducts extensivemarket research enabling the firm to identify new patterns of demand, set out a vision for CXand then innovate its services to match. Market presence and scale — Accenture leads the market in terms of revenue and staff, aswell as being referenced most frequently on competitive bids according to references thatreported shortlist candidates. Accenture has the ability to support global and multinationalaccounts due to its extensive scale and global breadth. Partnership with CRM software providers — Accenture has the largest practices in terms ofboth staff and revenue for most of the major CRM software platforms (Salesforce, Siebel,Pegasystems, Adobe and SAP). Accenture is also the largest Microsoft Dynamics CRM providerdue to the Avanade relationship (a joint venture with Microsoft). Accenture works closely with allthese software firms to develop industry- and process-specific solutions.Cautions Price — If pricing is a top criterion for selection, then evaluate Accenture with care. Amongcompanies named as references by other providers, most companies that evaluated but did notselect Accenture said the reason for not selecting Accenture was that the price was too high.References also rated Accenture below average for the total cost for the contracted services.Page 4 of 37Gartner, Inc. G00299019

Flexibility and resource allocation — References praised Accenture for vision, thoughtleadership and consulting competencies, but some also desired Accenture to be more flexiblein the approach to projects and to manage scope change. Clients also noted that, at times,Accenture would utilize junior staff both onshore and offshore who were not as skilled asexpected. Smaller stand-alone CRM implementations — Accenture is optimized for large complexengagements that include business change. The average scale and costs of its engagementsare large relative to most other providers. Accenture is not typically the best fit for small CRMimplementation projects unless there are other services also being provided.AtosAtos is positioned in the Niche Players quadrant due to being a European-centric provider. AtosCustomer Experience (ACE) is one of Atos' key digital focus areas, where it works on the connectedCX primarily for consumer-centric industries. Atos approaches CX from a digital technologyperspective, leveraging an integrated approach to digital, cloud, mobility, analytics and CRMtechnology integration, especially related to commerce using Worldline. Atos is a good fit forEuropean enterprises that are looking to increase revenue and customer interaction throughtechnology. Atos is the 10th-largest CX and CRM service provider worldwide, with 2015implementation revenue of about 600 million representing 5% of its total service revenue and 18%of its consulting and implementation revenue. The top five industries for its CRM and CX servicesare retail, public sector, transportation, financial services and utilities/energy.Strengths Addressing business objectives — Customer references repeatedly stated that Atos was verygood at listening to their objectives, understanding their business models and processes, andthen being able to adapt CRM and CX technologies to support the customers' processes. Atosutilizes its UX Lab and Business Transformation Innovation Center network to help clientsenvision these solutions. This enables IT organizations to support business objectives in apragmatic and effective manner and is particularly true within its focus industries. Technical and committed execution — Atos has a wide range of deep technologycompetencies, particularly those needed for CRM and CX projects, including informationarchitecture and commerce. References scored Atos well on technical skills, customerinformation architecture, system integration and project management. References commentedon technical skills and ability to mobilize quickly. Comments from references cited a culture ofreliable execution and commitment to the client's success as strengths. Commerce and mobility — Atos has aligned its CX strategy to the "connected customer" withthe attitude that everything is digital and mobile. The investments into Canopy, Worldline andthe CX practice enable Atos to bring together commerce, mobility and analytics in end-to-endsolutions. Atos has the highest percentage of revenue from commerce enablement of allproviders, and mobility enablement is part of virtually all services.Gartner, Inc. G00299019Page 5 of 37

Cautions Project management and execution — Atos references score it lower than most competitorsin project management, project methodology and meeting expectations. Some referencesdescribed issues with cost control and coordination of project resources and said Atos was notproactive in directing some projects. Geographical coverage — Non-European buyers may find a lower base of skills in CRM andCX implementation in their regions. Atos generates over 85% of its CRM and CX revenue inEurope. Atos provides support to customers globally and is building more CRM and CXcapabilities in North America and Asia/Pacific. CX thought leadership and business consulting — References scored Atos relatively low onkey criteria related to business transformation and change. These included business acumen,business process functional skills and CX thought leadership. The ability to work with clients onbusiness issues is strong when Atos serves as the technical and commerce partner.BearingPointBearingPoint with its global network partners is positioned in the Visionaries quadrant because itutilizes an effective consultative and innovative approach to CX transformations but with limitedscale. BearingPoint, West Monroe Partners, gA and ABeam are all regional consulting and strategyfirms that support clients globally through a strategic partnership. BearingPoint in Europe and WestMonroe in North America lead CX initiatives and are a good fit for enterprises seeking businessdriven CRM strategy and/or complex CX solutions. Gartner estimates that BearingPoint, combinedwith its partners, makes up the 14th-largest CX and CRM service provider worldwide, with 2015revenue of about 350 million. BearingPoint is a good choice for European enterprises looking forCX strategy and consulting, along with analytics, as part of their solution. West Monroe is a goodchoice for North American enterprises looking for CX strategy and transformation with limited scaleof implementation. ABeam is a good choice for Asian clients looking for CRM softwareimplementation. gA is a good choice for Latin American clients looking for CX consulting and CRMimplementation. The top five industries for CRM and CX services are banking, insurance,automotive/manufacturing, public sector and telecom/media.Strengths Business-driven CX approach — BearingPoint and West Monroe lead projects with businessand industry orientation and a consultative approach. The collaborative and consultativeapproach enables them to understand the objectives and nuances of the client situation andthen bring CX best practices, analytics and business frameworks to address the clientobjectives. References cited the ability to understand their issues and the collaborativeapproach as strengths. Project management and execution — BearingPoint and West Monroe both received strongratings for project management and execution by the team. References referred to effectiveproject management and change management competencies from both business and technicalperspectives.Page 6 of 37Gartner, Inc. G00299019

Transforming CX vision into reality — References gave BearingPoint and West Monroe strongscores and comments related to the ability to address business objectives. Comments alludedto the ability to understand the client's business model and project needs, and then developbusiness and technology solutions and support business change in a rapid yet pragmaticmanner. West Monroe was recognized as having great CX vision and thought leadership toguide clients.Cautions Limited scale and varied focus by geography — The partners operate in each region andsupport each other's clients for global coverage, but there is scale only with BearingPoint inEurope (58% of revenue) and ABeam in Asia (32% of revenue). BearingPoint's efforts in Europeare very CX-oriented with an emphasis on sales and commerce leveraging analytics.BearingPoint and ABeam's combined activities in Asia/Pacific now represent 32% of revenue,mostly in Japan for technology-oriented CRM sales and service initiatives. North America, ledby West Monroe, contributes only 9% of revenue from CX initiatives, mostly in mutichannelcommerce and marketing leveraging analytics. While still small, gA CRM and CX services grewin 2015 to 2% of revenue focusing on automotive. Proactive innovation — Although BearingPoint understood the client's situation andobjectives, references expressed a desire for BearingPoint to provide more proactive guidance,innovation and insight and a desire to be pushed by BearingPoint further than it provided. Price — BearingPoint and partners were viewed as having high cost, and some clients citedreduced value for these high costs. These firms are optimized for on-site and nearshore deliveryand execution, and the consultative approach leverages senior talent. BearingPoint is not agood choice when cost-efficiencies are a driving factor.Business & DecisionBusiness & Decision (B&D) is positioned in the Niche Players quadrant due to its specialty focus onEuropean enterprises seeking revenue generation from sales and marketing with a heavy focus oncustomer analytics. Gartner estimates that B&D is the 20th-largest CRM service provider worldwide,with 2015 revenue of about 200 million. B&D has its largest practices on Microsoft Dynamics CRMand Adobe, as well as practices in Salesforce, Siebel, Oracle Cloud and Coheris. The top fiveindustries for its CRM and CX services are banking, insurance, life sciences, manufacturing andconsumer goods.Strengths Business marketing solutions — B&D focuses its CRM efforts and skills on marketing andsales organizations. The percentage of revenue from marketing solutions was the highest of allproviders, and the company also generates significant revenue from sales enablement. Thisorientation has a technology focus on Adobe and analytics, which are applied to consumercentric industries of banking, insurance, hospitality, retail and telecommunications/media.Gartner, Inc. G00299019Page 7 of 37

Customer analytics and information architecture — B&D approaches the CX market from aninformation and analytics perspective, integrating and leveraging internal and external data togenerate value and business impact for clients. Business intelligence and CX are the primaryfocus of B&D, and the two disciplines generate more than 80% of revenue. This strongcustomer analytics competency is utilized in marketing areas such as lead management, loyaltyprograms, segmentation and campaign automation. There have been targeted investments todevelop frameworks that deliver incremental value creation through return on information. Flexibility — References praised B&D for flexibility, professionalism and understanding of theirbusiness operations. With this approach, B&D delivers increased sales and marketingeffectiveness through the use of analytics to make better decisions and increase productivity.Cautions Project management — B&D executes projects that are unique and highly adapted to eachclient to achieve value. However, multiple clients gave B&D relatively low ratings in projectmanagement, implementation methodologies and change management skills. B&D is investingin client success programs to assure quality project execution. Resource management and scale — B&D is the smallest of the service providers in thisassessment and specializes in analytics, sales and marketing solutions. References stated thatthe breadth of skills was limited, and that at times, there was less expertise than needed.References also noted there was turnover on projects, and at times, there were delays in fillingkey roles. Geographic reach — Non-European companies may not be as well-supported by B&D, whichhas a strong presence in France, Belgium and Switzerland. There is a growing presence inNorth Africa (15% of revenue); but 83% of its revenue comes from Europe and more than 50%of that from France. B&D has only a small presence in Latin America (Peru) and India and haslimited presence in other parts of Europe (the Nordics, Italy and Central Europe) and otherregions of the world compared with market leaders.CapgeminiCapgemini is positioned in the Leaders quadrant due to market presence, growing market shareand a focus on solutions for large or complex projects that require a combination of businessinnovation and CRM technical advisory and implementation skills. Capgemini's Digital CustomerExperience brings a wide range of competencies that integrate industry, consulting, CRMtechnology and analytics capabilities. Gartner estimates that Capgemini is the fourth-largest CX andCRM implementation provider worldwide, with 2015 CX and CRM revenue estimated to be around 2 billion (accounting for about 25% of its global consulting and technology service revenue) andabove-average market growth. Capgemini has very large practices in SAP CRM, Siebel, OracleCloud and Salesforce, with additional competencies in Microsoft Dynamics CRM, Pegasystems andAdobe.Page 8 of 37Gartner, Inc. G00299019

Strengths CX vision and thought leadership — Capgemini has invested heavily in CX and digitalmarketing initiatives. The Digital Customer Experience team brings together a wide range ofbusiness and technology competencies. Capgemini

Dec 01, 2016 · Magic Quadrant Figure 1. Magic Quadrant for CRM and Customer Experience Implementation Services, Worldwide Source: Gartner (December 2016) Gartner, Inc. G00299019 Page 3 of 37. Vendor Strengths and Cautions Accenture Accenture is positioned in the Leaders quadrant due to market presence, vision and digital