Transcription

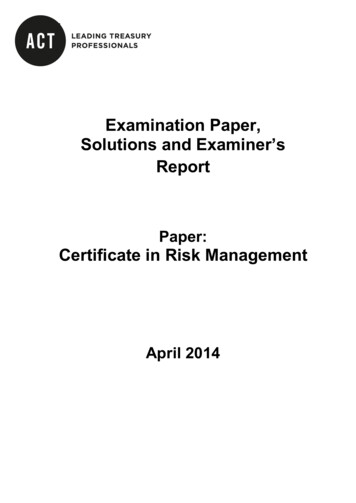

2022 Market OutlookHedge Fundsin 2022:Changing WithChanging RiskIn 2022, we believe the most notabletrends will be the continuationof ones that gathered strengthin 2021: Higher volatility levels inboth the equity and fixed incomemarkets leading to wider dispersionin performance of stocks, bondsand off-the-run investmentopportunities. The main volatilitydrivers were—and continue to be—the triumvirate of headlines thatbecame all-too-familiar: Tightening ofmonetary policy by the U.S. FederalReserve, increasing inflation, andthe uncontrolled growing spread ofCOVID-19. Hedge funds performedwell through this volatility(Display 1).MARK VAN DER ZWAN, CFACIO and Head of AIP HedgeFund SolutionsAIP HEDGE FUND SOLUTIONSPlease see important disclaimers at the end of this article.

2022 MARKET OUTLOOKRisk management seen as key tohedge fund success in 2022In contrast, risk markets in prior yearswere mostly driven by accommodativeFed policy and fiscal stimulus, creatingan ideal environment that lifted all boatsand beta returns. Hedge funds, whichlimit market risks and seek to generatealpha, underperformed.But rising volatility and performancedispersion create a fertile field for hedgefund managers, who found their footingagain in 2021, as shown by alphaproduction in Display 2. The rollingtwo-year average annualized alpha hasbeen positive all year and is the highest ithas been since January 2018. One needsto go back to August 2011 to find priorperiods of such strong and consistentalpha production.DISPLAY 1Hedge funds had solid performance in 2021.Last 12M (Ended November 0.0%8.0%6.0%4.0%2.0%0.0%HFRI Equity Hedge HFRI Event-Driven HFRI Fund Weighted(Total) Index(Total) IndexComposite IndexHFRI Macro(Total) IndexHFRI Relative Value(Total) IndexSource: HFR, Inc., as of November 30, 2021.DISPLAY 2The changing nature of riskWe believe that the biggest challenge tohedge funds in 2022 will be the changingnature of market risk. Hedging unwantedmarket exposure has always been keyto protecting alpha, but doing so hasbecome more complicated and nuanced.Hedge fund managers have generated alpha consistently for the pasttwo years.For example, the impact of “risk on/risk off” episodes has typically beeneffectively hedged with the S&P 500Index, largely because factors likegrowth, momentum and value have hadreasonably consistent—and predictable—performance during such periods.1.50%But the same has not held for “COVIDon/COVID off” episodes. Investorshave had to rapidly switch betweenthe prospects of the economy openingup and shutting down, and the relatedimpacts on stocks from labor shortages,supply chain dynamics and so forth.Performance factors underwent large2Annualized Alpha (Rolling 2Y) of HFRI Fund Weighted Composite to the S&P 500 Source: HFR, Inc., as of November 30, 2021.MORGAN STANLEY INVESTMENT MANAGEMENTJunJulAugSepOctNov

HEDGE FUNDS IN 2022: CHANGING WITH CHANGING RISKDISPLAY 3In “COVID on/COVID off” episodes, factor exposures behaved very differently than the S&P 500.Normalized S&P 500 Index and Barra Factor Returns1From November 26 to November 30, 2021Normalized Return(Z-Score 22 Day Lookback)3210-1-2-3-4S&P 500USLiquidityUS DividendYieldUSGrowthUS Long-Term US MidUSReversal Capitalization Momentum Nov 26 Nov 29US ShortInterestUS SizeUS Value Nov 30Past returns are not indicative of future results. Source: Barra (US Barra Medium Term Model)shifts in direction and magnitude, and asa result, the S&P 500 became too blunta tool for hedging in that environment.Factor exposures associated with hedgefunds have been behaving very differentlythan the market, as can be seen in the lastfew days of November 2021 (Display 3).The Omicron scareWe saw the impact of this in the wake ofthe Omicron scare of November 2021,when managers with good securityselection lagged the quick rebound in theS&P 500. For effective risk management,managers have to know how a basketof principal factor risks maps onto theirportfolios. Many clearly didn’t have arefined understanding of this “map” inthe evolving COVID on/COVID offworld, which likely led to overhedging orother uneven factor exposures.Another clue comes from the relativeperformance of classic long/shortmanagers in comparison with multi-portfolio manager platforms. We believethat the multi-PM platforms generallycan have a structural advantage for riskmanagement.and no one—including the Fed—reallyknows the optimal rate level for slowinginflation without harming the recovery.The economy has been shaped bysuper-easy money for a long time. Evenan increase of 75 basis points in 2022,as contemplated by the Fed, is a bigadjustment, and it is a big leap of faith toassume it will be a smooth one.Assuming the platforms devote sufficientresources and expertise to that function,they potentially can manage risk acrossmore dimensions and continuallydevelop the map connecting factors topositions. Even after accounting for theirhigher-cost pass-through structure, theafter-fee results of the Platform PeerGroup (Display 4) and their respectiveinvestment profile compare favorably.COVID is hardly the only likely sourceof volatility in 2022. The Fed’s taperingis potentially a major source, given theconflicting currents the central bank mayhave to navigate, with inflation printscoming in over 6% and the 10-year U.S.Treasury around 1.5% as of December2021. An accelerated tightening policycould slow growth, especially if there is aparallel drag from COVID developments,Implications for 2022Our outlook for more volatility anddispersion in performance for 2022 has anumber of implications:is likely to playa larger role in alpha generation, giventhe expected start/stop nature of themarkets and related choppiness thatis likely to disrupt sector trends andbroader thematic investing. By thesame logic, the intrasector opportunityset looks promising as a source ofidiosyncratic return independent of SECURITY SELECTIONNormalized returns is the statistical process of standardized returns by using the prior 22 trading day returns to calculate the average and standarddeviation and applying the Z-Score (x-average)/standard deviation methodology.1MORGAN STANLEY INVESTMENT MANAGEMENT3

2022 MARKET OUTLOOKCOVID on/COVID off, inflationor other macro influences. As notedearlier, long/short strategies that aresupported tightly by risk management,tend to preserve alpha better(Display 4). DIVERSIFICATION OF ALPHA SOURCESbecomes especially important becausedispersion is a double-edged swordthat increases both the number ofopportunities and the chance ofbad calls. Controlling intermanagercorrelations is critical—it ensures risksdo not overlap and helps minimizelosses from bad calls.for us includeglobal macro, with managers agileenough to capture the value of thecross currents in today’s environment,with a short-term, tacticallyoriented approach.DISPLAY 4Multi-PM platforms have outperformed classic long/short hedge funds.Last 5 Years (ended November 2021)PLATFORM PEER( 10B AVERAGE)HFRI EQUITY HEDGE(TOTAL) 59Annualized Alpha9.1%-1.1%Beta0.060.56Sources: HFR, Inc., Morgan Stanley. From December 31, 2016 to November 30, 2021. PROMISING STRATEGIESSelect commodity strategies fall in thiscategory, such as taking advantageof quick-shifting currents in supplyand demand in metals, livestock andagricultural markets, or even relativevalue trading in the oil marketsbetween West Texas Intermediate andBrent Crude. However, pure pricemoves are only part of the story, asspecialists can also maximize calendarspreads, contract rolls and physicaldelivery features.Less appealing strategies include longbias credit risk, where spreads are athistorically tight levels, and mortgagearbitrage—a sector hindered by alimited upside and the fact that durationtypically lengthens as rates rise.4 USING HEDGE FUNDS AS DIVERSIFIERSin classic 60/40 stock/bond portfolioscan help address a fundamentalproblem with bonds in 2022: Mostfixed-income sectors are long duration.For example, with a duration of 6.6years, the Bloomberg Aggregate Indexwould lose over 6% of its value witheach 1% increase in rates, and wouldbe unlikely to provide much of ahedge for equities in that scenario.As absolute-return vehicles, hedgefunds typically have a low beta toequities and rates, and thus may bean attractive hedge complement forbonds in 2022. CRISIS RISK OFFSET STRATEGIESMORGAN STANLEY INVESTMENT MANAGEMENTdeserve consideration by investorsseeking protection from tail riskevents. Such hedging strategies seekto deliver positive returns during lossscenarios while reducing outright costsin normal markets. They can alsoprovide the requisite diversificationneeded to allow for continued exposureto desired risks. Some risk offsetprograms are designed to even provideliquidity during times of significantmarket crisis.Changing with changing riskThe volatility and dispersion of returnswe expect in 2022 suggest that securityselection will be a key driver of returns.But this environment will demand morefrom managers. We believe successwill also require sophisticated portfolioconstruction, supported by a nuancedunderstanding of hedging as factorexposures change in the COVID on/COVID off world. In our view, investorswould benefit from considering hedgefunds constructed with diversifiedalpha sources and a strong riskmanagement process.

HEDGE FUNDS IN 2022: CHANGING WITH CHANGING RISKDEFINITIONSHFRI Equity Hedge (Total) Index: Investment Managers who maintain positionsboth long and short in primarily equity and equity derivative securities. A widevariety of investment processes can be employed to arrive at an investmentdecision, including both quantitative and fundamental techniques; strategiescan be broadly diversified or narrowly focused on specific sectors and canrange broadly in terms of levels of net exposure, leverage employed, holdingperiod, concentrations of market capitalizations and valuation ranges of typicalportfolios. EH managers would typically maintain at least 50% exposure to,and may in some cases be entirely invested in, equities, both long and short.HFRI Event-Driven (Total) Index: Investment Managers who maintainpositions in companies currently or prospectively involved in corporatetransactions of a wide variety including but not limited to mergers,restructurings, financial distress, tender offers, shareholder buybacks, debtexchanges, security issuance or other capital structure adjustments. Securitytypes can range from most senior in the capital structure to most junior orsubordinated, and frequently involve additional derivative securities. EventDriven exposure includes a combination of sensitivities to equity markets,credit markets and idiosyncratic, company specific developments. Investmenttheses are typically predicated on fundamental characteristics (as opposedto quantitative), with the realization of the thesis predicated on a specificdevelopment exogenous to the existing capital structure.HFRI Fund Weighted Composite Index (“HFRI Fund Weighted”): The HFRIFund Weighted Index is a global, equal-weighted index of single-manager fundsthat report to HFR Database. Constituent funds report monthly net of all feesperformance in USD and have a minimum of 50 million under managementor 10 Million under management and a twelve-month track record.HFRI Macro (Total) Index: Refers to the HFRI Macro (Total) Index, sponsoredby Hedge Fund Research, Inc. Macro funds trade a broad range of strategiesin which the investment process is predicated on movements in underlyingeconomic variables and the impact these have on equity, fixed income, hardcurrency and commodity markets.HFRI Relative Value (Total) Index: Investment Managers who maintainpositions in which the investment thesis is predicated on realization ofa valuation discrepancy in the relationship between multiple securities.Managers employ a variety of fundamental and quantitative techniques toestablish investment theses, and security types range broadly across equity,fixed income, derivative or other security types. Fixed income strategies aretypically quantitatively driven to measure the existing relationship betweeninstruments and, in some cases, identify attractive positions in which therisk adjusted spread between these instruments represents an attractiveopportunity for the investment manager. RV position may be involved incorporate transactions also, but as opposed to ED exposures, the investmentthesis is predicated on realization of a pricing discrepancy between relatedsecurities, as opposed to the outcome of the corporate transaction.Sharpe Ratio: a risk-adjusted measure developed by William F. Sharpe,calculated by dividing the Fund’s excess return relative to the risk-free rate(defined as the rate of return of the Citi Three-Month U.S. Treasury BillIndex) by the standard deviation of the Fund’s return.Volatility: A statistical measure of the tendency of a market or security to riseor fall sharply within a period of time – usually measured by standard deviation.Alpha: The excess return of an asset not explained by systemic (market) risk.Beta: Represents the Fund’s volatility relative to the market. A statisticalmeasure of the tendency of a market or security to rise or fall sharply withina period of time, usually measured by standard deviation. Higher levels ofvolatility correspond with higher levels of risk. See also Standard Deviation.RISK CONSIDERATIONSInvesting entails risks and there can be no assurance that any strategy willachieve profits or avoid incurring losses.Persons considering an alternative investment should refer to the specificfund’s offering documentation, which will fully describe the specific risksand considerations associated with a specific alternative investment.Morgan Stanley AIP GP LP, its affiliates and their respective directors,officers, employees, members, general and limited partners, sponsors,trustees, managers, agents, advisors, representatives, heirs, successors andexecutors shall have no liability whatsoever in connection with any person’sor entity’s receipt, use of or reliance upon any information in this piece orin connection with any such information’s actual or purported accuracy,completeness, fairness, reliability or suitability.Alternative investments are speculative and include a high degree of risk.Investors could lose all, or a substantial amount of, their investment.Alternative investments are suitable only for long-term investors willingto forgo liquidity and put capital at risk for an indefinite period of time.Alternative investments are typically highly illiquid—there is no secondarymarket for private funds, and there may be restrictions on redemptions orthe assignment or other transfer of investments in private funds. Alternativeinvestments often engage in leverage and other speculative practices thatmay increase volatility and risk of loss. Alternative investments typicallyhave higher fees and expenses than other investment vehicles, and suchfees and expenses will lower returns achieved by investors.IMPORTANT INFORMATIONThere is no guarantee that any investment strategy will work under allmarket conditions, and each investor should evaluate their ability to investfor the long-term, especially during periods of downturn in the market.A separately managed account may not be appropriate for all investors.Separate accounts managed according to the particular Strategy mayinclude securities that may not necessarily track the performance of aparticular index. A minimum asset level is required.For important information about the investment managers, please referto Form ADV Part 2.The views and opinions and/or analysis expressed are those of the authoror the investment team as of the date of preparation of this material andare subject to change at any time without notice due to market or economicconditions and may not necessarily come to pass. Furthermore, the views willnot be updated or otherwise revised to reflect information that subsequentlybecomes available or circumstances existing, or changes occurring, afterthe date of publication. The views expressed do not reflect the opinionsof all investment personnel at Morgan Stanley Investment Management(MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and maynot be reflected in all the strategies and products that the Firm offers.Forecasts and/or estimates provided herein are subject to change and maynot actually come to pass. Information regarding expected market returnsand market outlooks is based on the research, analysis and opinions ofthe authors or the investment team. These conclusions are speculative innature, may not come to pass and are not intended to predict the futureperformance of any specific strategy or product the Firm offers. Futureresults may differ significantly depending on factors such as changes insecurities or financial markets or general economic conditions.This material has been prepared on the basis of publicly available information,internally developed data and other third-party sources believed to bereliable. However, no assurances are provided regarding the reliabilityof such information and the Firm has not sought to independently verifyinformation taken from public and third-party sources.This material is a general communication, which is not impartial and allinformation provided has been prepared solely for informational andeducational purposes and does not constitute an offer or a recommendationto buy or sell any particular security or to adopt any specific investmentstrategy. The information herein has not been based on a consideration of anyindividual investor circumstances and is not investment advice, nor should itbe construed in any way as tax, accounting, legal or regulatory advice. To thatend, investors should seek independent legal and financial advice, includingadvice as to tax consequences, before making any investment decision.Charts and graphs provided herein are for illustrative purposes only. Pastperformance is no guarantee of future results.The indexes are unmanaged and do not include any expenses, fees or salescharges. It is not possible to invest directly in an index. Any index referred toherein is the intellectual property (including registered trademarks) of theapplicable licensor. Any product based on an index is in no way sponsored,endorsed, sold or promoted by the applicable licensor and it shall not haveany liability with respect thereto.This material is not a product of Morgan Stanley’s Research Departmentand should not be regarded as a research material or a recommendation.The Firm has not authorised financial intermediaries to use and to distributethis material, unless such use and distribution is made in accordance withapplicable law and regulation. Additionally, financial intermediaries arerequired to satisfy themselves that the information in this material isappropriate for any person to whom they provide this material in view ofthat person’s circumstances and purpose. The Firm shall not be liable for,MORGAN STANLEY INVESTMENT MANAGEMENT5

2022 MARKET OUTLOOKand accepts no liability for, the use or misuse of this material by any suchfinancial intermediary.This material may be translated into other languages. Where such a translationis made this English version remains definitive. If there are any discrepanciesbetween the English version and any version of this material in anotherlanguage, the English version shall prevail.The whole or any part of this material may not be directly or indirectlyreproduced, copied, modified, used to create a derivative work, performed,displayed, published, posted, licensed, framed, distributed or transmittedor any of its contents disclosed to third parties without the Firm’s expresswritten consent. This material may not be linked to unless such hyperlinkis for personal and non-commercial use. All information contained hereinis proprietary and is protected under copyright and other applicable law.Eaton Vance is par t of Morgan Stanley Investment Management.Morgan Stanley Investment Management is the asset management divisionof Morgan Stanley.DISTRIBUTIONThis material is only intended for and will only be distributed to personsresident in jurisdictions where such distribution or availability would notbe contrary to local laws or regulations.MSIM, the asset management division of Morgan Stanley (NYSE: MS), andits affiliates have arrangements in place to market each other’s productsand services. Each MSIM affiliate is regulated as appropriate in thejurisdiction it operates. MSIM’s affiliates are: Eaton Vance Management(International) Limited, Eaton Vance Advisers International Ltd, CalvertResearch and Management, Eaton Vance Management, ParametricPortfolio Associates LLC, Atlanta Capital Management LLC, Eaton VanceManagement International (Asia) Pte. Ltd.This material has been issued by any one or more of the following entities:EMEA:This material is for Professional Clients/Accredited Investors only.In the EU, MSIM and Eaton Vance materials are issued by MSIM FundManagement (Ireland) Limited (“FMIL”). FMIL is regulated by the CentralBank of Ireland and is incorporated in Ireland as a private company limitedby shares with company registration number 616661 and has its registeredaddress at The Observatory, 7-11 Sir John Rogerson’s Quay, Dublin 2, D02VC42, Ireland.Outside the EU, MSIM materials are issued by Morgan Stanley InvestmentManagement Limited (MSIM Ltd) is authorised and regulated by the FinancialConduct Authority. Registered in England. Registered No. 1981121. RegisteredOffice: 25 Cabot Square, Canary Wharf, London E14 4QA.In Switzerland, MSIM materials are issued by Morgan Stanley & Co.International plc, London (Zurich Branch) Authorised and regulated bythe Eidgenössische Finanzmarktaufsicht (“FINMA”). Registered Office:Beethovenstrasse 33, 8002 Zurich, Switzerland.Outside the US and EU, Eaton Vance materials are issued by Eaton VanceManagement (International) Limited (“EVMI”) 125 Old Broad Street, London,EC2N 1AR, UK, which is authorised and regulated in the United Kingdom bythe Financial Conduct Authority.Italy: MSIM FMIL (Milan Branch), (Sede Secondaria di Milano) PalazzoSerbelloni Corso Venezia, 16 20121 Milano, Italy. The Netherlands: MSIMFMIL (Amsterdam Branch), Rembrandt Tower, 11th Floor Amstelplein 11096HA, Netherlands. France: MSIM FMIL (Paris Branch), 61 rue de Monceau75008 Paris, France. Spain: MSIM FMIL (Madrid Branch), Calle Serrano 55,28006, Madrid, Spain.MIDDLE EASTDubai: MSIM Ltd (Representative Office, Unit Precinct 3-7th Floor-Unit701 and 702, Level 7, Gate Precinct Building 3, Dubai International FinancialCentre, Dubai, 506501, United Arab Emirates. Telephone: 97 (0)14 709 7158).EVMI utilises a third-party organisation in the Middle East, Wise Capital(Middle East) Limited (“Wise Capital”), to promote the investment capabilitiesof Eaton Vance to institutional investors. For these services, Wise Capitalis paid a fee based upon the assets that Eaton Vance provides investmentadvice to following these introductions.U.S.A separately managed account may not be appropriate for all investors.Separate accounts managed according to the Strategy include a numberof securities and will not necessarily track the performance of any index.6MORGAN STANLEY INVESTMENT MANAGEMENTPlease consider the investment objectives, risks and fees of the Strategycarefully before investing. A minimum asset level is required. For importantinformation about the investment managers, please refer to Form ADV Part 2.Please consider the investment objectives, risks, charges andexpenses of the funds carefully before investing. The prospectusescontain this and other information about the funds. To obtain aprospectus for the Morgan Stanley funds please download oneat morganstanley.com/im or call 1-800-548-7786 for the EatonVance and Calvert Funds please download one at documents.php or contactyour financial professional. Please read the prospectus carefullybefore investing.Morgan Stanley Distribution, Inc. ser ves as the distributor forMorgan Stanley Funds.Eaton Vance Distributors, Inc. (“EVD”), serves as the distributor for EatonVance and Calvert Funds.NOT FDIC INSURED OFFER NO BANK GUARANTEE MAY LOSE VALUE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY NOT A DEPOSITHong Kong: This material has been issued by Morgan Stanley Asia Limited foruse in Hong Kong and shall only be made available to “professional investors”as defined under the Securities and Futures Ordinance of Hong Kong (Cap571). The contents of this material have not been reviewed nor approved byany regulatory authority including the Securities and Futures Commissionin Hong Kong. Accordingly, save where an exemption is available underthe relevant law, this material shall not be issued, circulated, distributed,directed at, or made available to, the public in Hong Kong. Singapore: Thismaterial should not be considered to be the subject of an invitation forsubscription or purchase, whether directly or indirectly, to the public orany member of the public in Singapore other than (i) to an institutionalinvestor under section 304 of the Securities and Futures Act, Chapter 289of Singapore (“SFA”); (ii) to a “relevant person” (which includes an accreditedinvestor) pursuant to section 305 of the SFA, and such distribution is inaccordance with the conditions specified in section 305 of the SFA; or (iii)otherwise pursuant to, and in accordance with the conditions of, any otherapplicable provision of the SFA. This publication has not been reviewed bythe Monetary Authority of Singapore. Eaton Vance Management International(Asia) Pte. Ltd. (“EVMIA”) holds a Capital Markets Licence under theSecurities and Futures Act of Singapore (“SFA”) to conduct, among others,fund management, is an exempt Financial Adviser pursuant to the FinancialAdviser Act Section 23(1)(d) and is regulated by the Monetary Authority ofSingapore (“MAS”). Eaton Vance Management, Eaton Vance Management(International) Limited and Parametric Portfolio Associates LLC holds anexemption under Paragraph 9, 3rd Schedule to the SFA in Singapore toconduct fund management activities under an arrangement with EVMIAand subject to certain conditions. None of the other Eaton Vance groupentities or affiliates holds any licences, approvals or authorisations inSingapore to conduct any regulated or licensable activities and nothing inthis material shall constitute or be construed as these entities or affiliatesholding themselves out to be licensed, approved, authorised or regulatedin Singapore, or offering or marketing their services or products. Australia:This publication is disseminated in Australia by Morgan Stanley InvestmentManagement (Australia) Pty Limited ACN: 122040037, AFSL No. 314182,which accept responsibility for its contents. This publication, and any accessto it, is intended only for “wholesale clients” within the meaning of theAustralian Corporations Act. EVMI is exempt from the requirement to holdan Australian financial services license under the Corporations Act in respectof the provision of financial services to wholesale clients as defined in theCorporations Act 2001 (Cth) and as per the ASIC Corporations (Repeal andTransitional) Instrument 2016/396. Calvert Research and Management, ARBN635 157 434 is regulated by the U.S. Securities and Exchange Commissionunder U.S. laws which differ from Australian laws. Calvert Research andManagement is exempt from the requirement to hold an Australian financialservices licence in accordance with class order 03/1100 in respect of theprovision of financial services to wholesale clients in Australia.Japan:For professional investors, this material is circulated or distributed forinformational purposes only. For those who are not professional investors, thismaterial is provided in relation to Morgan Stanley Investment Management(Japan) Co., Ltd. (“MSIMJ”)’s business with respect to discretionary investmentmanagement agreements (“IMA”) and investment advisory agreements

(“IAA”). This is not for the purpose of a recommendation or solicitation oftransactions or offers any particular financial instruments. Under an IMA,with respect to management of assets of a client, the client prescribesbasic management policies in advance and commissions MSIMJ to make allinvestment decisions based on an analysis of the value, etc. of the securities,and MSIMJ accepts such commission. The client shall delegate to MSIMJ theauthorities necessary for making investment. MSIMJ exercises the delegatedauthorities based on investment decisions of MSIMJ, and the client shallnot make individual instructions. All investment profits and losses belongto the clients; principal is not guaranteed. Please consider the investmentobjectives and nature of risks before investing. As an investment advisory feefor an IAA or an IMA, the amount of assets subject to the contract multipliedby a certain rate (the upper limit is 2.20% per annum (including tax)) shallbe incurred in proportion to the contract period. For some strategies, acontingency fee may be incurred in addition to the fee mentioned above.Indirect charges also may be incurred, such as brokerage commissions forincorporated securities. Since these charges and expenses are differentdepending on a contract and other factors, MSIMJ cannot present therates, upper limits, etc. in advance. All clients should read the DocumentsProvided Prior to the Conclusion of a Contract carefully before executing anagreement. This material is disseminated in Japan by MSIMJ, Registered No.410 (Director of Kanto Local Finance Bureau (Financial Instruments Firms)),Membership: the Japan Securities Dealers Association, The InvestmentTrusts Assoc

Changing Risk In 2022, we believe the most notable trends will be the continuation . Normalized S&P 500 Index and Barra Factor Returns1 From November 26 to November 30, 2021 3-3-4 US Size . Source: Barra (US Barra Medium Term Model) 4 2022 MARKET OUTLOOK MORGAN STANLEY INVESTMENT MANAGEMENT COVID on/COVID off, inflation or other macro .