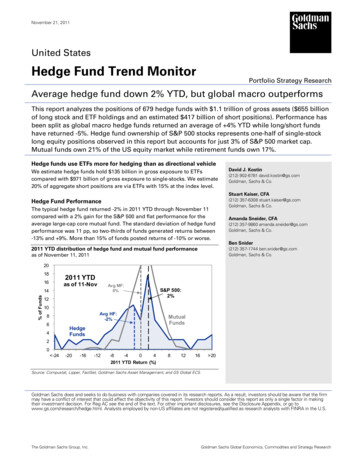

Transcription

THE LIFE CYCLE OF HEDGE FUNDSfunds, underscoring the importance of understandingthe history and lineage of hedge fund managers.INTRODUCTIONHarder, Better, Faster, Stronger.-Daft Punk/Kanye WestWhile every business is different, all typically gothrough a five phase life cycle: Start-up, to Growth,then Expansion, Maturity, and then finally,Decline.Few investors spend time thinking about applyingthat same framework to hedge funds. The life cycleof hedge funds is very similar, as no hedge fund canFrom our viewpoint, the life cycle of hedge funds canbe divided into four phases: Start-up; WealthCreation; Wealth Preservation; and ultimately,Decline, as shown in Figure 1 below.We discuss each of these distinct phases in detailbelow and flesh out our team’s constant quest for thenext undiscovered star hedge fund manager – andidentifying them before they become well-knownhousehold names.Figure 1exist into perpetuity. Hedge funds do have expirationdates. However, as we have seen time and timeagain, the death of one hedge fund often results in thebirth of “spin-offs” - a variety of new firms, with thecycle beginning yet again. This occurs when younginvestment talent leaves their predecessor firms, andhave entrepreneurial aspirations to launch their ownCONFIDENTIALPHASE I: START-UPYou don’t get another chance. Life is no Nintendogame.-EminemNascent and hungry, newly minted hedge fundmanagers hanging their own shingle for the first timePage 1

Windrose Advisors – The Life Cycle of Hedge Fundshave fire in their bellies and something to prove.Many of these emerging managers are compellingbecause they often include a star analyst from amature hedge fund that is looking to replicate pastsuccess – but without the constraints of a large assetbase. In addition, recent data confirms that thesehedge funds early in their life cycle are delivering thehighest returns and beating more established fundsevery year. A recent study of nearly 1600 hedgefunds conducted by alternative assets data providerPreqin found that recently launched hedge funds(defined as hedge funds that are less than three yearsold) have consistently outperformed moreestablished funds by almost 4% annually since2012.1 This analysis confirms that the argument foridentifying and investing with emerging managers isvery compelling.Figure 2 fleshes this out further, showing thatannualized returns of emerging managersoutperformed established managers by 3.7% and4.6% on a three- and five-year annualized basis,respectively. This outperformance is achieved withmodestly higher risk – the volatility is a mere 1.2%and 0.5% higher than for established managersduring that same time period.In addition, the annual returns shown in Figure 3through the January 2012 to June 2019 time periodalso demonstrates consistent outperformance byemerging managers, outperforming establishedFigure 2 Statistical Performance of Early Lifecycle vs. Established Hedge Funds, 2012 – 2019Source: Preqin. Data from January 2012 to June 2019.Figure 3 Annual Performance of Early Lifecycle vs. Established Hedge Funds, 2012 – 2019Source: Preqin. Data from January 2012 to June 2019.“Opportunities Investing with Early Lifecycle HedgeFunds: A Preqin & 50 South Capital Study”. Preqin.October 2019. PDF file.1CONFIDENTIALPage 2

Windrose Advisors – The Life Cycle of Hedge Fundsmanagers every single year. Not only did emergingmanagers outperform but they also protected capitalbetter in 2018, when markets experienced extensivelosses. These observations are not intended todiminish the returns that can be realized frominvesting in established funds. Rather, it is tohighlight that the results suggest that investors canbenefit from identifying and investing in emergingmanagers as part of a dynamic, blended hedge fundprogram alongside established managers.While an important cornerstone of any investment, itis often not just about the manager’s pedigree or theiredge (in other words, what they like to identify astheir “secret sauce”). It is, however, in those earlyyears, a struggle. London-based financial servicesconsultancy Capco’s often-cited research shows thatover 50% of hedge fund failures are due tooperational risk alone as opposed to investment risk.2This was based on Capco’s study of 100 hedge fundfailures over the past 20 years. Most investors focuson management, strategy, and the track record whenchoosing hedge funds, paying less attention to theoperational side of the business.When launching a hedge fund, few realize howdifficult it will be to raise assets in a highlycompetitive landscape, as they need to be not only agood investor (to manage the fund), a good businessmanager (to manage the business), but also a goodmarketer (to raise assets). It requires a significantcommitment from a core team of highly experiencedindividuals in terms of time, capital, and patience,and requires them to be well versed - not only froman investment perspective, but also from anoperational perspective.However, emerging managers often don’t have thelevel of assets that would afford them the ability tobuild a world-class, institutional-grade, operationalinfrastructure. Investing too early in an institutionalquality infrastructure before assets materialize canreassure prospective investors but create afundamental weakness by raising the breakevenpoint. On the opposite end of the spectrum, somefunds rush to launch, without taking intoconsideration what careful steps are needed to scaletheir businesses accordingly as they grow.Somewhere in the middle, we have seen fundssuccessfully grow their operations prudentlyalongside asset growth. It is a fine and tricky balance,and we recognize that the cost of not getting thestructure right in the first place can lead toconsiderable pain later. As a result, in the start-upphase we often see hedge funds outsource their backoffice. The growth in outsourcing these functionsand delegating those responsibilities to dedicatedprofessionals in their respective fields is mainlydriven by the need for money managers to focus ontheir core strength, which is leveraging theirinvestment expertise.In attracting initial capital, during the start-up phasethere are often three types of investors who show upat the door. This typically includes Seeders, Fund ofHedge Funds, and Family Offices, but all fordifferent reasons. Many hedge funds cannot launchwith a large enough asset base to coverorganizational expenses and be considered credibleby investors. As a result, there exists an ecosystemof strategic investors who often get involved at thisstage. However, there is no free lunch.Seeders: Hedge Fund Seeders are exactly what theysound like – they provide early-stage capital and areinstrumental in the development of emerging hedgefunds. However, different from other investors aseeder’s return potential is greater than that of otherinvestors because in exchange for its willingness totake start-up risk and make an early commitment, itreceives a portion of the hedge fund’s revenue stream(a percentage of the manager’s management andperformance fees). It also may establish otheradvantages, such as rights to future capacity, fulltransparency, etc. There are many groups thatspecialize only in hedge fund seeding activities.Seeding hedge funds is a fully mature industry.However, it is important to note that large seeders arenot usually considered quality capital. This isGiraud, Jean-Rene. “Mitigating Hedge Funds’Operational Risks.” EDHEC Business School. June2005. PDF file.2CONFIDENTIALPage 3

Windrose Advisors – The Life Cycle of Hedge Fundsbecause seeders can abruptly redeem their capital ifa fund is not quickly successful, introducing astructural weakness. In addition, managers end uptrading away economics in their business to facilitateasset gathering, which could imply a lack ofconfidence in their own odds of success.Fund of Hedge Funds (“FoHF”): Fund of HedgeFunds investors create a pooled fund that will investin a variety of hedge funds. They may participate inthe seeding business (as discussed above) or mayassemble collections of managers focused on aparticular strategy or goal. The FoHF industry hasbeen declared dead many times, as players failed toevolve. Fund of Hedge Funds have often assembledcollections of managers that are too large and dilutethe successful strategies. They have also favoredlower risk strategies to deliver a high Sharpe ratio,but at the expense of higher returns. Nevertheless, aFoHF structure allows nimble allocators to takesome risk with emerging managers. At present, thereare a select few successful FoHFs that remain, butthe industry not surprisingly has contracted in the lastdecade.Family Offices (“FO”): Family Offices are privatewealth management firms that serve ultra-high-networth investors. It is an often-overlooked source offunding. As many of the underlying families are farout on the wealth distribution curve, they can employprofessionals whose sole focus is to manage andpreserve wealth. While some wealth is generational,others are entrepreneurs who have achieved outsizedbusiness success. As a result, Family Offices can bemore innovative and forward thinking, willing toinvest in early-stage managers. More importantly,Family Offices contend with taxes and therefore aimfor higher returns than institutional investors. Sincemost of the best strategies are capacity constrained,FO recognize that you need to partner early with highpotential managers in order to secure access.At Windrose Advisors (WA), we uniquely sharetraits of both the Fund of Hedge Fund structure andthe Family Office structure – we seek higher returnsfor our taxable investors, while our structureuniquely allows us to integrate emerging managersinto the mix alongside established managers.CONFIDENTIALWhere do we typically prefer to nail our stake intothe ground? While we constantly conduct researchacross strategies, geographies, asset sizes andmaturity levels, not surprisingly there are certainpoints in the cycle that we gravitate towards.Somewhere between Phase I and Phase II tends to bethe optimal entry point. This is typically when amanager is not yet fully discovered by the broaderinvestor community. The fund may still be rampingup its operational infrastructure at this point.However, after a few years in business, managershave tackled some of their start-up issues, raisedassets and built their back office to a higher standardthan on day one. They are often looking to closetheir fund to new investors in a relatively short timeframe and to embark on a wealth creation phase thatis often the most rewarding for their investor, andthemselves.Given our team’s experience, we often provideconsultative advice to assist managers as they get upto speed and become more institutionally friendly.As can be expected, we end up turning over a lot ofrocks before we find something worth pursuing. Wejoke that it is a lot like dating, and you have to go ona lot of dates before you finally find “the One”.PHASE II: WEALTH CREATIONGet rich or die tryin’.-50 CentAfter some initial growing pains, by focusing onperformance and achieving a three-year track record,emerging managers are no longer considered startups. At this juncture, after posting three or moreyears of what are considered “good” returns, theysurvived what most institutional investors, especiallyconsultants, consider a critical period. In our view,three years of returns is still not statisticallysignificant, and we prefer to focus on ourfundamental understanding of a strategy. Manyallocators underestimate the role of luck andfavorable market conditions in the early years. Forexample, with value investing so out of favor atpresent, it is highly unlikely that a new valueoriented manager built a stunning track record andattracted much interest in recent years.Page 4

Windrose Advisors – The Life Cycle of Hedge FundsOverall, however, managers who have successfullynavigated this period have likely reached criticalmass in terms of assets under management. Theinvestment team generally remains focused andsmall. And, having achieved breakeven (in terms ofbeing able to pay all operating expenses), they arenow able to fine tune operations and invest further indeveloping their back-office controls. This is amission critical element. In addition to performance,institutional quality operational infrastructure is akey component to garner interest from consultants.Consultants are employed by institutional allocatorsto navigate the “opaque” world of hedge fundinvesting and are often dubbed “The Gatekeepers.”They advise some of the world’s most powerfulallocators on where to invest their money and, as aresult, for many hedge fund managers, it is arelentless quest to curry favor with consultants inorder to access these valuable clients. Getting on theexclusive short lists of recommended managers is arigorous, extensive process that is long, tedious, andchallenging. It is a highly coveted prize, however, tomake it past the evaluation stage onto the approvedlist, and into client portfolios. For the lucky few, this“stamp of approval” spurs growth in assets undermanagement.However, it is a double-edged sword. More oftenthan not, recognition by consultants can trigger somuch interest that it can also lead a manager to allowits asset base to grow beyond what the strategy canreasonably handle – in turn resulting in a potentialdegradation in performance. Large consultants(growing larger through industry consolidation) havean incentive to prioritize high capacity strategies thatcan be deployed across many client accounts. This“agency bias” may result in niche strategiesreceiving less attention, despite their attractive returnpotential.As an independent advisor with a significant butmanageable asset base in the context of these largeallocators, WA is uniquely suited to allocate to anymanager or strategy without bias to size or capacity.Even smaller allocations in absolute terms canmeaningfully enhance performance for our clients.CONFIDENTIALPHASE III: WEALTH PRESERVATIONSuccess is my idol and being broke is my rival.-Big SeanSeveral years have gone by, and the hedge fundmanager is now firmly established in the market.There are no longer any operational kinks, it now hasan institutional quality back office where significanttime and money has been invested to pass the test ofeven the most discerning operational due diligenceteam. The investment team has expanded from notjust a portfolio manager and two analysts, to a morehierarchical organizational structure, with senioranalysts, junior analysts and research associates.This allows more portfolio breadth but results in thefund manager becoming more of a manager ofpeople and less in touch with the underlyingportfolio. More importantly, as managers strive tomaintain their investor base, there is an increasingfocus on limiting downside, mitigating volatility,and as a result, maintaining a high Sharpe Ratio.These underlying factors typically attractendorsement by Endowments & Foundations(“E&Fs”), Pensions, and Insurance Funds who tendto favor stability and predictability because of thenature of their underlying assets and the constituentsthey serve. In addition, these groups do not contendwith tax friction and as a result can afford to take lessrisk and accept a lower risk/lower return proposition.It is fair to say, that on a general basis, the group ofinvestors that tends to dominate during the “WealthPreservation stage” typically constitutes what wewould describe as the quintessential “institutionalinvestor sector.”As hedge fund managers continue to grow and attractthe types of institutional investors that can write verylarge checks, it is likely that asset size becomes aconstraint and begins to level off. There is often lessmonth to month volatility in performance as themanager endeavors to satisfy the desires of its largerinvestors. The larger asset base also results in heftymanagement fees, and performance fees matter lessto the manager’s wealth, reducing the incentive totake risks and generate outsized returns.Page 5

Windrose Advisors – The Life Cycle of Hedge FundsThe manager at this juncture has now amassed apersonal fortune. The hunger that existed when themanager first hung his or her shingle has nowevolved into a “stay rich” mentality. With growingwealth, the manager’s lifestyle can changedramatically, whether it is though the consumptionof material goods or a new interest in philanthropiccauses. We are constantly assessing if the managers’time enjoying the fruits of their success will distractthem from investment management.During this phase managers may also hire young,talented apprentices and aim to groom them andtransfer years of knowledge and expertise with theintention of passing on the torch. This is all inattempt to maintain continuity of the firm. This oftenis not a successful exercise as a manager may havedifficulty retaining younger talent as they may haveaspirations of their own – with a focus on higherreturns or the desire to be entrepreneurial. Or, theseapprentices may not possess the same talent level.PHASE IV: DECLINEThe future is born, put the past in a casket.-Lil WayneAfter a while, the hedge fund manager is considereda large, well-known brand name across the investorcommunity; it has amassed assets undermanagement on a multi-billion dollar basis; it hasestablished several offices globally; it has alsoexpanded the investment and operational teammeaningfully. Performance begins to disappoint as alarge asset base makes deploying assets into ment begins to waver as the manager begins tofocus instead on retaining assets to maintain thecontinuity of the firm. The fund may evolve from asimple single strategy into new areas with significantproduct proliferation. It may experience teamdepartures, as younger talent who desire to beentrepreneurial or have different aspirations begin toleave and create spin-offs.After being able to successfully preserve wealth, butunable to continue the pace of work to sustain anCONFIDENTIAL“edge,” the manager at this point is facing a majorissue: as younger talent departs, he or she recognizesthe need to create a succession plan. It is verydifficult in our view to “transfer” the originalmanager’s edge to the next generation within thesame firm. In our collective experience, there havebeen very few hedge fund firms that have been ableto do this successfully. This creates meaningfulinstability in the firm that ultimately contributes tothe hedge fund firm’s eventual, and slow, decline,but spurs the evolution and innovation of new talentwhere the cycle starts again.AND THE CYCLE BEGINS AGAINLife is a wheel of fortune and it’s my turn to spin it.-TupacAll hedge fund investors should maintain a keen eyeon where a hedge fund manager is in its life cycleand integrate this critical element into theconsideration, due diligence, and allocation of hedgefund assets. It can be a lonely road for investors whofocus on the earlier parts of the life cycle, as fewinvestors are well equipped to conduct investmentand operational due diligence at this stage andintegrate the risks into an investment program. Thisis where opportunities lie. The constant life cyclethat exists amongst managers across a variety ofstrategies makes for a very robust pool (with fewercompetitors) for our investment team to fish anduncover new investment talent for inclusion into ourportfolios.RESEARCH/COMMENTARY DISCLAIMERPAST PERFORMANCE IS NO GUARANTEE OF FUTURERESULTS. This material has been prepared by Windrose Advisors, LLC on the basis ofpublicly available information, internally developed data and other sources believed to bereliable. The information provided herein is for general informational purposes only and doesnot constitute an offer to sell or a solicitation of an offer to buy any securities or commodities,or investment advice relating to securities or commodities, or a representation that any securityor commodity is a suitable or appropriate investment for any person. All information hereinis written and prepared for large and experienced institutional investors with the highest degreeof financial sophistication and knowledge and the capacity to withstand and assess anyfinancial losses. Opinions expressed herein are current opinions as of the date appearing inthis material only and are subject to change without notice. In the event any of the assumptionsused herein do not prove to be true, results could vary substantially. All investments entailrisks. There is no guarantee that investment strategies will achieve the desired results under allmarket conditions. No representation is being made that any account, product, or strategy willor is likely to achieve profits, losses, or results similar to those discussed, if any. No part ofthis document may be reproduced in any manner, in whole or in part, without the prior writtenpermission of Windrose Advisors, LLC. You may not rely on the statements contained herein.Windrose Advisors, LLC shall not have any liability for any damages of any kind whatsoeverrelating to this material. You should consult your advisors with respect to these areas. Byaccepting this material, you acknowledge, understand and accept the foregoing.Page 6

over 50% of hedge fund failures are due to operational risk alone as opposed to investment risk.2 This was based on Capco's study of 100 hedge fund failures over the past 20 years. Most investors focus on management, strategy, and the track record when choosing hedge funds, paying less attention to the operational side of the business.