Transcription

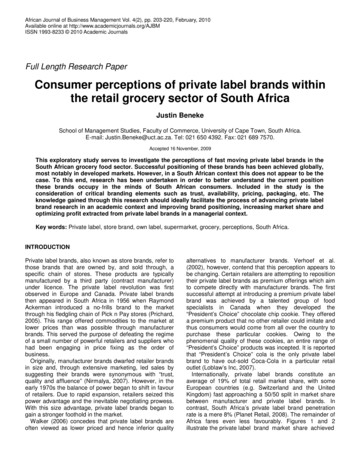

African Journal of Business Management Vol. 4(2), pp. 203-220, February, 2010Available online at http://www.academicjournals.org/AJBMISSN 1993-8233 2010 Academic JournalsFull Length Research PaperConsumer perceptions of private label brands withinthe retail grocery sector of South AfricaJustin BenekeSchool of Management Studies, Faculty of Commerce, University of Cape Town, South Africa.E-mail: Justin.Beneke@uct.ac.za. Tel: 021 650 4392. Fax: 021 689 7570.Accepted 16 November, 2009This exploratory study serves to investigate the perceptions of fast moving private label brands in theSouth African grocery food sector. Successful positioning of these brands has been achieved globally,most notably in developed markets. However, in a South African context this does not appear to be thecase. To this end, research has been undertaken in order to better understand the current positionthese brands occupy in the minds of South African consumers. Included in the study is theconsideration of critical branding elements such as trust, availability, pricing, packaging, etc. Theknowledge gained through this research should ideally facilitate the process of advancing private labelbrand research in an academic context and improving brand positioning, increasing market share andoptimizing profit extracted from private label brands in a managerial context.Key words: Private label, store brand, own label, supermarket, grocery, perceptions, South Africa.INTRODUCTIONPrivate label brands, also known as store brands, refer tothose brands that are owned by, and sold through, aspecific chain of stores. These products are typicallymanufactured by a third party (contract manufacturer)under licence. The private label revolution was firstobserved in Europe and Canada. Private label brandsthen appeared in South Africa in 1956 when RaymondAckerman introduced a no-frills brand to the marketthrough his fledgling chain of Pick n Pay stores (Prichard,2005). This range offered commodities to the market atlower prices than was possible through manufacturerbrands. This served the purpose of defeating the regimeof a small number of powerful retailers and suppliers whohad been engaging in price fixing as the order ofbusiness.Originally, manufacturer brands dwarfed retailer brandsin size and, through extensive marketing, led sales bysuggesting their brands were synonymous with “trust,quality and affluence” (Nirmalya, 2007). However, in theearly 1970s the balance of power began to shift in favourof retailers. Due to rapid expansion, retailers seized thispower advantage and the inevitable negotiating prowess.With this size advantage, private label brands began togain a stronger foothold in the market.Walker (2006) concedes that private label brands areoften viewed as lower priced and hence inferior qualityalternatives to manufacturer brands. Verhoef et al.(2002), however, contend that this perception appears tobe changing. Certain retailers are attempting to repositiontheir private label brands as premium offerings which aimto compete directly with manufacturer brands. The firstsuccessful attempt at introducing a premium private labelbrand was achieved by a talented group of foodspecialists in Canada when they developed the“President’s Choice” chocolate chip cookie. They offereda premium product that no other retailer could imitate andthus consumers would come from all over the country topurchase these particular cookies. Owing to thephenomenal quality of these cookies, an entire range of“President’s Choice” products was incepted. It is reportedthat “President’s Choice” cola is the only private labelbrand to have out-sold Coca-Cola in a particular retailoutlet (Loblaw’s Inc, 2007).Internationally, private label brands constitute anaverage of 19% of total retail market share, with someEuropean countries (e.g. Switzerland and the UnitedKingdom) fast approaching a 50/50 split in market sharebetween manufacturer and private label brands. Incontrast, South Africa’s private label brand penetrationrate is a mere 8% (Planet Retail, 2008). The remainder ofAfrica fares even less favourably. Figures 1 and 2illustrate the private label brand market share achieved

204Afr. J. Bus. Manage.Figure 1. Private label share of market, by value in percentage terms – 2007e (dark) versus 2012e (light).Source: Planet Retail, 2008.Figure 2. Share and volume of private label brand sales, as indicated by leading global retailers. Source: PlanetRetail, 2008.

Benekeby a host of countries and the share of volume enjoyedby leading global retailers. It is clearly evident thatEuropean and North American retailers excel in thisrespect. Emerging markets such as South Africa, Brazil,China and Russia experience penetration rates below theinternational average and are therefore playing ‘catch up’.Two anomalies present themselves in terms ofpenetration of private label brands in South Africa(Nielson, 2006). Firstly, it has been concluded that retailconcentration (essentially an oligopoly scenario in theretail sector) is highly correlated with success of privatelabel brands. Yet, in South Africa, despite high retailconcentration enjoyed by the major supermarket chains,private label brands have not achieved the successes oftheir global counterparts. Secondly, lower income groupstend to be the most common purchasers of private labelbrands due to higher levels of affordability. In SouthAfrica, despite a much larger population of lower incomeconsumers, it is the higher Living Standards Measures(LSM) categories, particularly LSM 6-10, which appear topurchase these brands (ibid). Research suggests that asconsumers become increasingly affluent, they are morewilling to try various alternatives to trusted brands(Mawers, 2006). In general, consumers with limitedfinancial resources are likely to purchase trusted (that ismanufacturer) brands in which quality is well establishedand thus confidence is high (Rusch, 2002). Another factorcontributing to this phenomenon has been identified asaccessibility. In South Africa, lower income groupsfrequently do not have direct access to the large retailstores where private label brands are available. Thisleads these consumers to shop at local ‘spaza’ outletswhich are similar to convenience stores, albeit present inthe informal sector (that is township) areas. These storestend to charge higher prices due to their location, as wellas not being able to benefit from larger economies ofscale (Klemz et al., 2006). It is estimated that betweenten and twenty percent of fast moving consumer goods,sales are estimated to occur through the informal sector(Blottnitz, 2007), therefore representing a lost opportunityfor private label brands.RESEARCH STATEMENTThis paper aims to uncover current consumerperceptions of, and attitudes towards, private labelbrands in the South African grocery sector. In doing so,the research will ascertain the impact of variousdemographic factors (with particular reference toethnicity, gender and income) on consumption of privatelabel brands. Furthermore, it aims to shed lights on theeffect that pricing, accessibility, packaging, omotions have on shopping behaviour with reference topurchasing food-based private label brands.205LITERATURE REVIEWBrand building fundamentalsAccording to Dick et al. (1997), consumers basejudgement of brand quality on direct and indirect factors.Direct attributes include ingredients, taste and texture,whilst indirect factors are represented by price and brandname. Direct factors are usually difficult for consumers totest without consuming the product, or completing varioustests. Hence, reliance on indirect quality indicators suchas brand name and price are more heavily relied upon.The authors thus suggest that a thorough understandingof how these indirect cues impact different consumergroups in their purchasing decisions may help retailers toimprove success of private label brands. Through furtherinvestigation, they identified brand, package andadvertising as indirect factors which impact consumerperceptions and hence influence purchasing decisions.The success of a brand in the long term is not based onthe number of consumers that buy it once-off, but on thenumber of consumers who become regular buyers of thebrand. Thus, repeat purchases and customer loyalty areprioritised by retailers (Odin et al., 1999). Chaudhuri andHolbrook (2001) suggest that consumers become brandloyal when they perceive some unique value in the brandthat no alterative can satisfy. This uniqueness may bederived from a greater trust in the reliability of a brand orfrom a more favourable experience when a customeruses the brand. Schoenbachler et al. (2004) take thisfurther, stating that not only does the brand loyalcustomer buy the brand but (s)he also refuses to switch,even when presented with a better offer. Bayus (1992)proposes that maintaining brand loyalty is becoming acritical component in the development of competitivestrategy, thus highlighting the importance of developingmethods to measure and evaluate brand loyalty.Davis (2002) identified further positive repercussionsresulting from a strong brand other than simply increasedsales. Effective brands have been correlated withincreasing market share; lending credibility to newproduct developments; giving a clear, valued andsustainable point of difference as well as commanding apremium. Most importantly, consumers appear less pricesensitive and more trusting towards these brands.Private label brandingPrivate label brands are available in a multitude offormats. There are, essentially, three varieties of privatelabel brands. The first being a representative brand,which is a private label brand that through its name andpackaging announces that it is produced and solelyowned by the retailer. The second being an exclusiveprivate label brand, which is owned and produced by theretailer, yet this fact is not explicitly conveyed to the

206Afr. J. Bus. Manage.consumer through brand name and packaging. The lasttype is confined labels. These are brands that are notowned by the retailer but are found exclusively in theirstores. This type of private label brand has not beenincorporated in this research study. Manufacturer brandson the other hand are controlled and produced bymanufacturers and sold through a plethora of retailers. Interms of branding, the general consensus appears to bethat private label brands are considered “every bit asmuch a brand as manufacturer’s” (Murphy, 1987).Ailawadi and Keller (2004) identify at least four tiers ofprivate label brands. These include low quality generics;medium quality private labels; somewhat less expensivebut comparable quality products; and premium qualityprivate labels that are priced in excess of competitormanufacturer brands. Whilst the nature of a store’sprivate label brand(s) should be guided, first andforemost, by its target market, the authors suggest thatsuccessful retailers will adopt more than one tier ofprivate label brand if they are to achieve wide scalemarket coverage.According to Kumar and Steenkamp (2007), half ofprivate label brands are copycat brands. These brandsessentially attempt to imitate the packaging and contentof first tier manufacturer brands. Retailers analyse thecontents of leading brands, and then re-create theproduct, through a process known as reverse engineering(ibid). Thus, since there are minimal research anddevelopment costs, and the retailers have alreadyrecognised that there is a potentially lucrative marketavailable, these products are more often than notsuccessful. The retailers use in-store promotions toaggressively promote the brands, using a “me-too at acheaper price” strategy (Kumar and Steenkamp, 2007).This type of strategy involves producing an almostidentical product and offering it at a reduced price relativeto competitors. As the examples in Figures 3 and 4reveal, packaging is nearly indistinguishable fromcompetitor brands.The copycat strategy is not without complications –pursuing this approach may well result in legal tussles.Actions of trademark infringement and “passing off”because of consumer confusion, unfair misappropriationof brand owners’ intellectual property can have legalimplications (Mitchell and Kearney, 2002).Benefits and drawbacks of selling private labelbrandsFernie et al. (2003) have identified various advantages toretailers for the development of a private label brand: (1)increased profitability through cost saving and increasedmargins; (2) increased store loyalty and creation of adistinct corporate identity; (3) opportunities to seize newmarket ventures; and (4) increased bargaining leveragewith suppliers.The first relates to potential increases in profitability,which stems from the higher average price margins thesebrands generate for retailers. These price margins couldbe higher due to the fact that private label brands requireminimal advertising expenditure; lower research anddevelopment costs; reduced costs of testing productsprior to launching nationally; and, usually, reducedpackaging costs. Furthermore, according to Herstein andGamliel (2006), private label brands can assist indeveloping loyalty to a retailer and in the creation of adistinct corporate identity for a business. Veloutsou et al.(2004) support this view, yet emphasise that as a result,careful managerial practices for these brands should beimplemented in order to maintain retailer brand equity.Consumers tend to associate the retailer with itsrespective private label brand. Therefore negativeperceptions of the retailer may impact negatively on itsfascia (that is store) brand and vice versa (Ailawadi andKeller, 2004).Labeaga et al. (2007) contend that private labels assistbuilding loyalty by differentiating the retailer. Thesebrands are available at one retailer exclusively whilstmanufacturer brands are available at many competingoutlets. Regular consumers of private label brands areconfronted with psychological costs when switchingretailers as their preferred private label choice is nolonger available. As a result, consumers who changeretailers undergo demanding cognitive processes byevaluating other brands, including unfamiliar storebrands, in choosing a new product. Thus, researchindicates that consumers who purchase private labelbrands regularly do not only become loyal to thatparticular brand but also to the retailer through which it issold (Collins and Burt, 2003).Raju et al. (1995) assert that retailers have becomemore proficient at managing their private label brands.Kumar and Steenkamp (2007) add that over the lastdecade, private labels have become omnipresent andhave achieved enormous success, thus providing a basefor the improvement in branding activities. The authorscontend that private labels have changed from inferiorgenerics to brands in their own right with value beyondfunctional attributes. Figure 5 demonstrates examples ofpremium quality private label tea brands that areavailable at Woolworths. The attractively packaged itemsare, arguably, addressing consumer needs of esteemand status. According to the retailer, it aims to make itsbrand synonymous with innovation, excellence and valuefor money, pitching it as being of the highest quality,equivalent to (if not better than) the category leaders.Retailers should also acknowledge potential pitfalls inoffering private label brands. Firstly, such brands in manyproduct categories may expose the retailer to unduebusiness risk. This essentially arises from the retailerextending its reach into unfamiliar markets with established competitors (Fernie et al., 2003). Secondly, theprivate label brand’s reputation may tarnish consumer’’s

BenekeFigure 3. Manufacturer ‘copycat’ brands. Captured: Pick n Pay,Pinelands, Cape Town.207perceptions of the retailer if it fails (Veloutsou et al.,2004). Thirdly, the profitability per square metregenerated by private label brands may not be on a parwith that of manufacturer brands. This may beattributable to the fact that most private label brands arepriced below their manufacturer brand counterparts(Kumar and Steenkamp, 2007). Consumers who areheavy purchasers of private label brands may not proveto be more profitable in the long run (ibid). This could beaccredited to the fact that these consumers may besubstituting a more expensive manufacturer brand withthe less expensive private label option. The authorsargue that this is sometimes considered an outdatedtheory as pricing differentials between private label andmanufacturer brands have been reduced. In the past,private label products tended to be lower priced generics.However, more recently, sophisticated private labelproducts have become available and relative prices haveincreased accordingly. A local example of this is the Pickn Pay Choice brand which, according to Prichard (2005),is usually priced only marginally below mostmanufacturer brands.Consumer perceptions and private label brandpronenessFigure 4. Private label ‘copycat’ brand. Captured: SPAR,Rondebosch, Cape Town.Figure 5. Premium tea brandsWoolworths, Pinelands, Cape Town.at Woolworths.Captured:Jin and Yong (2005) note that the success of private labelbrands is dependent on factors such as the country’sretail structure, the level of retailer concentration, theadvertising rate of manufacturer brands, economies ofscale, management, and even imagination. Baltas (1997)notes that whilst past behaviour, demographic variables,socio-economic factors as well as personality traits havebeen found to influence private label brand purchasingbehaviour; perceptions, attitudes and behaviouralvariables are more effective in this regard. Richardson etal. (1996), as cited by Baltas (1997), identified familiarity,extrinsic cues, perceived quality, perceived risk,perceived value for money and income level as theprimarily influencing factors of private label proneness.Interestingly, younger consumers appear to have a morefavourable view towards private label brands than oldergenerations (Veloutsou et al., 2004). Moschis (2003)echoes this sentiment, suggesting that older consumersare more brand loyal and are likely to prefer brands withwhich they are more familiar. Younger consumers, on theother hand, are more willing to try new or unfamiliarbrands and products.Walker (2006) suggests that due to relatively lowerprices, consumer quality perceptions are negativelyimpacted. Private label brands are thus frequently seenas inferior quality alternatives. This is reiterated by DeWulf et al. (2005) who suggest that consumers perceivemanufacturer brands to be superior to private labelbrands. Yet, Verhoef et al. (2002) present a contrastingopinion on consumer quality perceptions of private labelbrands, contending that consumers do indeed foster a

208Afr. J. Bus. Manage.positive attitude towards these brands. Smith and Sparks(1993) appear to view the situation in a similar light,proposing that the perceptual gap between private labeland manufacturer brands is narrowing. Whilst debate iscertainly present in the literature with regards to trends inconsumer perceptions of private label brands, thesebrands do seem to represent value to hard pressedconsumers. According to Quelch and Harding (1996),private label share is inversely related to economicstrength. Therefore, when the economy is thriving, asmaller proportion of private label brand products arepurchased. Additionally, Nandan and Dickinson (1994)inferred that during economic recessions, popularity ofprivate label products increases. Lamey et al. (2007)note, however, that the effects of economic fluctuationsare non-symmetrical in terms of growth versuscontractions. By way of explanation, the authorscomment that the rate at which consumers adopt privatelabel brands during a recession is faster than the reverseprocess which occurs after the economic downturn hasceased. Thus, once the economy has stabilised,consumers do not rapidly change consumption habitsthat were created during the recession. The authorshighlight that levels of private label consumption do notreturn to the levels that existed before the advent of therecession.Pricing and in-store promotion of private labelmerchandisePrice represents an extrinsic cue and provides one of themost important forms of information available toconsumers when making a purchasing decision (Jin andSternquist, 2002).According to the authors, priceconstitutes 40% of the average consumer’s informationsearch. Avlonitis and Indounas (2005) underline theimportance of pricing decisions in terms of a company’slong term profitability. The authors emphasise theflexibility of pricing – pricing strategies can be adaptedmore quickly than other marketing facets. As alluded topreviously, this is particularly applicable with regard toprivate label brands as they are under full control of theretailer, and are free from the manufacturer’s pricingstrategies and considerations (Uusitalo and Rokman,2007).Manufacturer and private label brand prices tend tovary among different retailers and certain products types.Davies and Brito (2004) suggest that although priceelasticities have a large effect on pricing decisions,generally the price advantage of private label brands isinclined to have approximately 20 to 44% higher grossprofit margins. A variety of reasons are suggested as towhy private label brands tend to be more cost effective.Firstly, as previously mentioned, this can be attributed toprivate label brands often being imitations of manufacturer brands. Thus the limited associated researchand development costs result in the retailers’ ability tocharge a reduced price (ibid). Furthermore, the authorsargue that new private label brand products can be at alower cost by test marketing in a few of their own retailstores. This again contributes to lower research anddevelopment costs. In addition, packaging of private labelbrands tends to be marginally less expensive, as the rawmaterials used are often of a slightly lower quality.However, the factor that has the greatest impact onoverall variable costs is the reduction in advertisingexpenses. Field (2006) concur that the majority ofretailers have little or no advertising expenditure withrespect to their private label brands.Kumar and Steenkamp (2007) note that over use ofpromotions by manufacturer brands may conditionconsumers to become price sensitive and this may,eventually, result in a “trade down” to a private label item.Therefore deal seekers become regular purchasers ofprivate label brands over time. Putsis and Dhar (2001)contrastingly note that promotions of manufacturerbrands based on price are more likely to attract salesaway from lower quality private label competitors, whilstthe price promotion of private label brands does not seemto have an equal level of success in this regard.Advertising of private label brandsIn the case of supermarket retailers, communications arebecoming an increasingly important tool for productdifferentiation (Uusitalo, 2001). These retailers operate ina slow-growth market and products are becomingincreasingly homogenous, hence the importance ofcommunications as a means of distinguishing one retailbrand from another.According to Kim and Parker (1999), it is difficult tomeasure the success of private label brand advertising.This is attributed to the manner in which advertising costsare internalised within the retailing organisation. Berry(2000) adds that brands, such as private labels, which fallunder the “umbrella image” of a company, are essentiallypromoted in conjunction with all company promotions.For example, based on Berry’s argument, it would appearthat Pick n Pay No Name brand is promoted through allPick n Pay advertising and promotions due to the mannerin which these brands are associated with one another byconsumers.Figure 6 illustrates an advertisement for “Pick n Pay’s”foremost private label - No Name brand. The blue andwhite colour theme clearly brings to mind associations forboth fascia and private label brands.Abe (1995) queries whether high quality producersshould advertise more than low quality producers or if lowquality producers should advertise more in order tocompensate for their relative product disadvantage.Private label brands are generally assumed to be of aninferior quality to manufacturer brands and thus represent

Beneke209Figure 6. Pick n Pay branding advertisement. Source: Pick n Pay website.these two quality alternatives for the purposes of thisargument (De Wulf et al., 2005). Advertising accentuatespredilections for a brand, thus differentiating it fromcompetitors. It would appear that increased advertisingdoes not increase sales at a rate that would make thisexpenditure more lucrative for private label brands.Therefore, Abe (1995) asserts that private label brands’potentially inferior quality does not necessitate a largeradvertising budget than manufacturer brands in order tocompete. Baltas (2003), on the other hand, suggests thatmanufacturer brands cannot often compete with privatelabel brands in terms of pricing and thus advertising playsa vital role in product differentiation for manufacturerbrands. Retailers are therefore challenged to promotetheir range of private label brands without large scaleadvertising. This is often achieved through placement ofone or two private label products – alongside theirmanufacturer-branded counterparts – in a newspaperinsert or the co-branding of both fascia and private labelbrands in a television advert. Nonetheless, retailers aremindful that private label brands need to be self promotedto some degree and that excessive advertising thereof isalmost certainly unwarranted.The effect of packagingUnderwood et al. (2001) state that there has been anemerging trend to use packaging as a brandcommunications vehicle. The authors describe theprimary role of product packaging as a means tocaptivate consumer attention by breaking through thecompetitive clutter. According to Ampuero and Villa(2006), packaging plays a crucial role, especially from theconsumer’s perspective. This is due to the fact that aproduct’s packaging is what first attracts a consumer. Theauthor asserts that as self-service sales environmentshave increased, the role of packaging has gainedmomentum. Thus, packaging has become the “salientsalesman” as it informs consumers of the qualities andbenefits of a product. This substantiates Fielding’s (2006)argument that packaging plays the lead role in building aprivate label brand. The author takes this one stepfurther, suggesting that packaging has a long-lastingeffect in the minds of consumers and is thus a manner inwhich to blur manufacturer brands’ distinctiveness.Building upon this, Ampuero and Vila (2006) considerpackaging to be the most important communicationsmedium for the following reasons: (1) it reaches almostall buyers in the category; (2) it is present at the crucialmoment when the decision to buy is made; and (3)buyers are actively involved with packaging as theyexamine it to obtain the information they need. It isinteresting to note that, according to one particular study,nine out of ten purchasers occasionally buy on impulse,and these unplanned purchases are generally as a resultof striking packages or in-store promotions (Nancarrow etal., 1998).Meyer and Gertsman (2005) argue that differences inpackaging between private label and manufacturerbrands have been reduced over time. Qualityimprovements and decreases in price differentialsbetween private label and manufacturer brands have ledto an increase in the importance placed on packaging –the authors identify this form of communication as a keysource of product and brand differentiation. According toNogales and Gomez (2005), packaging by private labelbrands is specifically selected in order to facilitate productcomparison. “Pick n Pays” No Name brand is immediatelyidentifiable by its blue and white packaging, and likewisefor Checkers’ Housebrand through its teal, white andmagenta packaging.Halstead and Ward (1995) highlight the fact thatretailers have re-evaluated the importance of packagingfor their private label brands. Thus retailers are placingmore emphasis on adding colour or modifying packagingto appear more like competing manufacturer brands.Furthermore, in some instances, packaging quality is ofan excellent standard (Suarez, 2005), making itsomewhat difficult to distinguish between private labeland manufacturer brands on shelf. Copy-cat brandingoften involves utilizing the colour of the brand leader inthe category. For example, private label cola brands areoften featured in red to associate themselves with CocaCola.Apportioning shelf spaceAmrouche and Zaccour (2006) describe shelf space as“one of the retailer’s most important assets”. This vitalresource is limited and therefore allocations can play a

210Afr. J. Bus. Manage.key strategic role. Retailers ultimately hold this trumpcard with respect to negotiations. Allocations to privatelabel have been known to be as sizable as twice thatapportioned to manufacturer brands (Nogales andGomez, 2005). In addition, Suarez (2005) notes thatretailers purposefully allocate their private label brands tomore advantageous positions on the shelves, such asplacing their own brands directly to the right of themanufacturer brands they are competing against. Thisbeing due to the fact that 90% of the population are righthanded and are thus theoretically more likely to reach forthe private label alternatives (ibid).According to Hwang et al. (2004) the level on which theproduct is displayed has a significant effect on sales. Forinstance, a product which is located at eye-level fallswithin the average consumer’s line of vision, attractinghis/her attention, and hence increasing the likelihood ofthe product being chosen. De Wulf et al. (2005) concurswith this premise and emphasises the influential role thatshelf positioning of a private label brand can play withregard t

Internationally, private label brands constitute an average of 19% of total retail market share, with some European countries (e.g. Switzerland and the United Kingdom) fast approaching a 50/50 split in market share between manufacturer and private label brands. In contrast, South Africa's private label brand penetration