Transcription

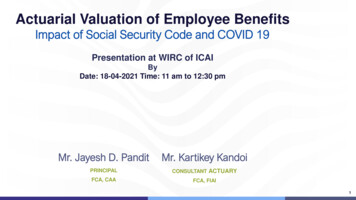

Actuarial Valuation of Employee BenefitsImpact of Social Security Code and COVID 19Presentation at WIRC of ICAIByDate: 18-04-2021 Time: 11 am to 12:30 pmMr. Jayesh D. PanditMr. Kartikey KandoiPRINCIPALCONSULTANT ACTUARYFCA, CAAFCA, FIAI1

AgendaIntroduction to Actuarial ValuationKAP Insights - COVID-19 & the ImpactThe Code on Social Security, 2020Actuarial Valuation Assumptions - Analysis and ImpactActuarial Valuation - Calculation ExamplePractical points in Actuarial ValuationQ&A and Open Forum Discussion2

Introduction toActuarial Valuation

IntroductionEmployee BenefitsShort TermDefined Benefit (DB) Fixed Formulaebased BenefitsDefined Contribution (DC) Other Long TermPost EmploymentTermination Unknown cost foremployerMajority financialrisk borne by theemployer FixedcontributionsNo benefitguaranteeKnown cost foremployerMajority financialrisk borne by theemployee4

Actuarial Valuation of Employee BenefitsGratuity Eligibility as per 10 EmployeesCommunicationLeave Provisions as per Shops Establishment ActPara 70 of AS 15/ Para 72 of Ind AS 19 – Gratuity Provision even serviceless than 5 yearsAS 15 & Ind AS 19 - Provision as per Projected Unit Credit MethodDetailed Disclosure to Notes to Accounts5

KAP INSIGHTSCOVID-19 & THE IMPACT

Impact of COVID-19 on Employee BenefitsEffect onthe count ofemployeesThe analysis conducted:01 FY 2019 v/s FY 2020 - Q1Effect onPatterns ofleaveaccumulationEffect onsalaryKAP FY 2019 v/s FY 2020 - H1 FY 2019 v/s FY 2020 - 9M0203Between 550,000 and 650,000 employees7

Pattern of Leavers and New JoineesAttrition Rate as percentage of opening members30%24%25%20%15%13%KAP12%10%5%7%7%4%0%March to JuneMarch to September2019KAPMarch to December2020Reduction in attrition over the first 2 quarters, 3rd quarter slightly higher attrition.8

Pattern of Leavers and New JoineesNew Joinees as percentage of opening members30%28%25%20%17%15%10%KAP12%8%5%5%2%0%March to JuneMarch to September2019March to DecemberKAP2020Fewer New Joinees in the current year compared with 2019, slightly improved in Q3.9

Pattern on Salary Movement% of Members getting Increase in 0%22%10%0%March to JuneMarch to September20192020KAPMarch to DecemberSignificantly few members received any salary increment till H1. This gap has reduced by Q3 end.10

Pattern on Accumulated Leave DaysIncrease in Leave 20%10%0%March to JuneMarch to September2019KAPMarch to December2020Over 80% of employees having an increase in accumulated leave balances in 2020,up from 70% in 201911

What’s Next Post Unlock?KAPShould we realignassumptions tolong term averagerate?Outlook ofmanagement forfuture mediumterm growth rate?Impact on Leaveprovisions ifspecific measurestaken in this leaveKAPpolicy year.12

THE CODE ONSOCIAL SECURITY, 2020

The Code on Social Security, 2020The Employees' Compensation Act, 1923The Employees' State Insurance Act, 1948The Employees' Provident Funds and Miscellaneous Provisions Act, 1952The Employment Exchanges (Compulsory Notification of Vacancies) Act, 1959KAPThe Maternity Benefit Act, 1961The Payment of Gratuity Act, 1972The Cine-Workers Welfare Fund Act, 1981The Codeon SocialSecurity,2020KAPThe Building and Other Construction Workers’ Welfare Cess Act, 1996The Unorganised Workers Social Security Act, 200814

Key Changes - Chapter V “Gratuity”Minimum Vestingcriteria relaxed from 5years to 3 years forGratuity EligibilityApplicableSalaryWorkingJournalistFixed Term KAPEmploymentKAPDefinition updatedfrom Basic DA to‘Wages’No Minimum vestingcriteria15

“Wages” definition0102“ this includes”TotalRemunerationLessExclusionsBasic DA RetainingKAPplusExcessExclusionsSocial SecurityCode, Section 2(88)The specified exclusions, however may not exceed 50 percent of all remuneration, and in the event ofexceeding, such excess amount will be added in "wages"16

“Wages” definition - ScenariosPay ComponentBasic Pay (35% CTC)HRALTAConveyancePF Employer ContributionsGratuityNPS ContributionsSpecial allowanceVariable BonusCTC incl. BonusCTC No BonusSSC 000262,3981,500,0001,200,00057% ofCTCWages for Gratuity (p.a.)Wages for Gratuity (p.m.)420,00035,000682,39856,867600,00050,000If Bonus considered Wages for Gratuity (p.a.)Wages for Gratuity (p.m.)420,00035,000982,39881,867750,00062,50065% ofCTC17

About the study1,000 companies in 202031 Marchdata2016-202018

Basic to Gross Ratios – Year on YearYearLess than 25% From 26% to 35%From 36% to 49%From 50% to 174%18%48%30%20162%17%49%32%Percentage of companies with the following Basic to Gross RatiosCompanies may face an increase in the deemed “wages” for benefit calculations. For e.g.if current ratio is 40% the deemed wages would increase by 25%.UnderInterpretation#219

Basic to Gross Ratios – Industry griculture3%InformationTechnologyLess than 25%9%Infrastructure2%1%ManufacturingFrom 26% to 35%From 36% to 49%OthersKAP11%14%2%PharmaceuticalFrom 50% to 65%2%Services1000 Companiesin 202020

Impact of Social Security Code on GratuityProvisions – Macro levelSectorGratuity DefinedBenefit Obligation at31.03.2020 (INR Cr)Approx. PercentageincreaseAgriculture14835%Information %Grand Total3,35536%1000 Companiesin 2020While calculating the above increase in Gratuity liability, we have considered change only in applicable wages and have kept othervariable such as data, actuarial assumptions, and scheme constant as per each company’s previous valuation as on 31-03-202021

Impact of Social Security Code on GratuityProvisions – Salary DefinitionExample Monthly Basic DA: INR 200,000 Monthly Wages (SSC): INR 250,000Valuation Assumptions Financial Assumptionso Discount Rate : 8.00% p.a.o Salary Escalation : 6.00% p.a.KAP Age: 42 years Service: 15 years Demographic Assumptionso Mortality Rate – IALM (2006-08)o Attrition Rate – 10.00% p.a.KAP22

Impact of Social Security Code on GratuityProvisions – Salary DefinitionSalary and Liability with maximum ceilingSalary and Liability without maximum 001,730,7691,211,429 1,256,9221,000,000500,000AMOUNT IN INRAMOUNT IN 500,000KAP1,000,000500,000-Discontinuance LiabilityMonthly Salary: INR 200,000Projected Benefit ObligationMonthly Salary: INR 250,000KAPDiscontinuance LiabilityMonthly Salary: INR 200,000Projected Benefit ObligationMonthly Salary: INR 250,000Impact – Past service cost / Actuarial Loss?23

Impacts of Wages Definition onOther BenefitsLeave encashment impact depends onThe Shops and Establishment Act in respective statesImpact on PF and ESIC contributions may be limitedWill be pertinent to see if NPS contributiontax allowances and salary definition may change24

Actuarial Valuation AssumptionsAnalysis and Impact

Discount RateBased on Expected Working Term of Obligation/ Expected Future ServiceCommunicationSource – FBIL (mostly used by RBI regulated entities)‘Fixed Income Securities’ tab under ‘GSEC’Select required date in from and to, download G-sec excel fileGo to sheet Par-Yield. We need to select annualized rates.26

Discount Rate TrendAnnualised Par Yields on G. Secs(www.fimmda.org with prices/yields published by FBIL)7.50%7.00%Annualised Par 45631-03-20207891011121314 15 16 17Tenure 02127

Salary Escalation & Attrition RateCan be based on past trend and allow for future outlookCommunicationAssumption analysis at regular intervalsCategory wise?Short term/ long termService Specific/ Age Specific28

Attrition Rate – Analysis ResultsService Specific-Attrition Rate p.a.Age Specific-Attrition Rate %10%5%5%0%0%0246810 12 14 16 18 20 22 24 26 28 30 32 34Service Cohort2022242628303234363840424446485052Age CohortAttrition rate lower for employees with lower service,Attrition rate high at the younger ages.29

While in Service Leave Availment RateThe availment is expected leave taken in the future years out of thecurrent accumulated balance.CommunicationShould be valued on CTCCan be based on past trend and allow for future outlook(Leave Availed - Leave Credited)/Opening Leave Balance(Applicable only when availed days are greater than the current leave credited, else availment rate is 0%)Alternative method - (Closing Leave Balance – Opening Leaves Balance)/Opening Leaves Balance30

Mortality Rate : Pre-RetirementComparison of Mortality Rates over IALM 2006-08 and 2012-14over ages 18-65Communication1.800%Indian AssuredLives Mortality2006-08 Ultimate1.600%Mortality Rate (%)1.400%1.200%1.000%Indian AssuredLives Mortality2012-14 Ultimate0.800%0.600%0.400%0.200%0.000%010203040Age (Years)IALM 2006-08506070Male Insured LivesMedically underwrittenIALM 2012-1431

Mortality Rate : Post-RetirementComparison of Mortality Rates over IALM 2006-08 andIAMT 2012-15 over ages 60 and aboveCommunication100%Indian AssuredLives Mortality2006-08 UltimateMortality Rate (%)80%60%Indian IndividualAnnuitant’sMortality Table(2012-15)40%20%0%60708090AgeIALM 2006-08IAMT 2012-15100110 All Genders Effective From 1st April, 2021 Longevity increase by 2.61years at age 60 years32

Mortality Rate : Post-RetirementComparison of Longevity (Life Expectancy)IALM 2006-08 and IAMT 2012-15 over ages 60 and aboveCommunication25.00Indian AssuredLives Mortality2006-08 UltimateLongevity Years20.0015.00Indian IndividualAnnuitant’sMortality Table(2012-15)10.005.0060708090AgeIALM 2006-08IAMT 2012-15100110 All Genders Effective From 1st April, 2021 Longevity increase by 2.61years at age 60 years33

Actuarial ValuationCalculation Example

Actuarial Valuation MethodCalculated for each: Type of benefit payment Projected KAPyear till retirement age EmployeeKAPObligation Projected Benefit x Probability x Discounting35

Actuarial Valuation Calculation ExampleExample Monthly Eligible Salary: INR 85,000 Age: 32 years Service: 2 yearsValuation Assumptions Financial Assumptionso Discount Rate : 8.00% p.a.o Salary Escalation : 6.00% p.a.KAP Demographic Assumptionso Mortality Rate – IALM (2006-08)o Attrition Rate – 10.00% p.a.KAPAccrued Amount 15/26*2*85,000 capped at INR 20 Lakhs INR 98,07736

Projected Accrued Amount 450,000 400,000 350,000 300,000 250,000 200,000 150,000 100,000 65758AGE 10,000 5,000 50,000 0 8,591 8,190 7,809 7,445 7,099 6,769 6,454 6,155 5,870 5,598 5,340 5,094 4,860 4,636 4,423 4,219 4,023 3,835 3,655 3,481 3,313 3,152 2,997AMOUNT IN INR 98,077 103,962 110,199 116,811 123,820 131,249 139,124 147,471 156,320 165,699 175,641 186,179 197,350 209,191 221,743 235,047 249,150 264,099 279,945 296,741 314,546 333,419 353,424 374,629 397,107 420,933 446,189 500,000 110 109 108AMOUNT IN INR 30,000 25,911Actuarial Valuation Calculation ExampleExpected Payout 25,000 20,000Projected BenefitObligationINR 58,727 15,00032 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58AGE37

Impact of Change in Vesting Criteria 30,000 25,000 20,000 20,000 0 10,000 5,000 65758AGE 9,454 9,012 8,591 8,190 7,809 7,445 7,099 6,769 6,454 6,155 5,870 5,598 5,340 5,094 4,860 4,636 4,423 4,219 4,023 3,835 3,655 3,481 3,313 3,152 2,997 5,000 15,000 110 10,000 8,591 8,190 7,809 7,445 7,099 6,769 6,454 6,155 5,870 5,598 5,340 5,094 4,860 4,636 4,423 4,219 4,023 3,835 3,655 3,481 3,313 3,152 2,997 15,000AMOUNT IN INR 25,000 110 109 108AMOUNT IN INR 30,000Expected Payout with vesting criteria as 3 years 25,911Expected Payout with vesting criteria as 5 years 25,911Projected Benefit Obligation INR 75,013Projected Benefit Obligation INR 5455565758AGEExpected cashflow for – Fixed term contract employees - ?38

Practical aspects inActuarial Valuation

Practical aspects in Actuarial ValuationLimit of LeaveAvailment andEncashmentDirectors Included?Ind AS 24 Disclosure?Benefit Scheme as perpolicy and ActuaryReportContribution toGratuity Fund, TaxRule 103KAP.EmployeeKAP Transferwithin GroupPension Valuation forKAPRegional Rural Banks40

Common Errors Found by FRRB inImplementation of AS 15 Employees BenefitsNon-provisioning of Gratuity (Matching Principle)Inadequate disclosure in policy pertaining to liability forsuperannuation fund (Para 45)No disclosure or inadequate disclosures pertaining to para 120KAPDefined Benefit Plan wrongly treated as Defined Contribution PlanNon-Disclosure of para 47 (expense for Defined Contribution Plan)KAPInadequate disclosure pertaining to para 65 (Use of PUCM Method)Source: The Chartered Accountant Journal April 201941

OPEN FORUM DISCUSSION

Food for thought - Open DiscussionWages definition - Statutory Bonus v/s Variable Bonus ?PF Interest – On Opening Accumulated Balanceor Current year contribution interest only ?Impact of change in Gratuity Wage definition under Social Securitycode (Past Service Cost/ Other Comprehensive Income) ?Companies likely to restructure CTC?Discount Rate as Single G-Sec or Term Structure of G-Sec?43

ANY QUESTIONS?

Our Solutions for Employee BenefitsCommunicationGovernance andAdministrationFinancialDesign andInsightsStructure Actuarial valuations underIndian and Global AccountingStandards Financial projections formanagement and fundingpurposes Cashflow projections forasset-liability assessments Trend and experience Advise on Retirement Trustsset up and ongoing operations Regulatory advice Trust Documentation draftingand approvals Trust accounting and Design new employeebenefits Review existing designs to Draft handbooks / rules Presentation toemployeesoptimize Assess cost implications ofproposed changessecretarial support Project management of Trustoperationsanalyses for appropriateness Funding vendor selectionof assumptions Trustee Training workshops45

We work for you, wherever your business takes you!Thank You!46

DisclaimerThis material and the information contained herein prepared by M/S. K. A. Pandit Consultants & Actuaries (KAP) is intended to provide generalinformation on a particular subject or subjects and is not an exhaustive treatment of such subject(s). This material contains information sourced from thirdparty sites (external sites). KAP is not responsible for any loss whatsoever caused due to reliance placed on information sourced from such external sites.By means of this material, KAP is not rendering professional advice or services. This information is not intended to be relied upon as the sole basis forany decision which may affect you or your business. Before making any decision or taking any action that might affect your personal finances orbusiness, you should consult a qualified professional adviser. No entity in the KAP Network shall be responsible for any loss whatsoever sustained by anyperson who relies on this material. 2020 K. A. PANDIT ISO 9001:2015 CERTIFIED ISO 27001:2013 CERTIFIED.47

Patterns of leave accumulation Effect on salary. 8 KAP KAP Pattern of Leavers and New Joinees . Special allowance 262,398 262,398 Variable Bonus ? 300,000 CTC incl. Bonus 1,500,000 CTC No Bonus 1,200,000 Wages for Gratuity (p.a.) 420,000 682,398 600,000