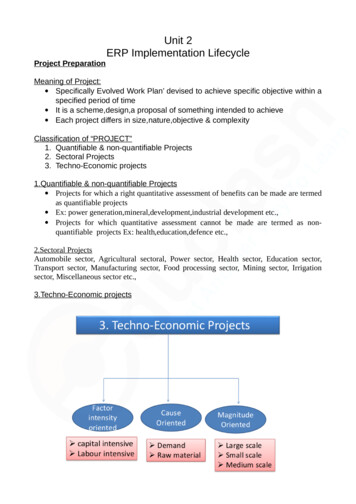

Transcription

ERP for defense auditcompliance

Any business performing work for a ministry ordepartment of defense will need to comply withaudits from their government customer. For theUnited States, these audits are performed bythe Defense Contract Audit Agency (DCAA),part of the Department of Defense (DoD).In other countries, different agencies areresponsible for auditing defense contracts, butthe steps necessary for audit preparation aresimilar. I n Norway, the Contract Audit Branch reportsaudit results to the HQ Defense CommandNorway M any countries operate collaborativeprojects or have reciprocal agreements withthe United States DoD, and in these casesDCAA audits may also affect these overseasdefense organizations and contractors I n the United Kingdom, audits may comefrom the Review Board for GovernmentContracts, Defense Equipment and Supportand the Directorate of Pricing t In France, audits are completed by theService for the Investigation of ArmamentCosts (SECAR) I n Spain, the Costs Evaluation Group, part ofthe Directorate General for Economic Affairsin the Spanish Ministry of Defense (MINISDEF)is responsible for auditsERP for defense audit compliance02

My experience is primarily with DCAA—in fact,my mother worked for DCAA in humanresources, and I have a more favorable feelingfor the organization than many of thosesubmitting to an audit. With the followingguidance, I hope to leave you feeling morepositive about the prospect of being auditedand more prepared. Some of that preparationwill require you to make the most of thecapabilities of enterprise resource planning(ERP) software optimized for defensemanufacturing and contracting. But a lot of thepreparation has to do with your mindset.Remember that this audit likely means that thegovernment is qualifying you to take on morework for your defense agency customers. This isa vote of confidence, and excellentperformance can put your company on the fasttrack towards increasing revenues fromdefense contracts.A rigorous approach to wrongdoing anddelivery improvementDefense audits have multiple goals, includingthe prevention of malfeasance, pricingirregularities and graft. The DCAA works closelywith the U.S. Department of Justice (DoJ) toprosecute infractions of contract law that riseto the standard of criminal behavior. DoJ forinstance has launched a Procurement CollusionStrike Force, focused on "deterring, detecting,investigating and prosecuting antitrust crimes,such as bid-rigging conspiracies and relatedfraudulent schemes . . ."AllocabilityA cost is allocable if it is assignable orchargeable to one or more cost objectives onthe basis of relative benefits received or otherequitable relationship—if it is incurredspecifically for one contract, benefits both thecontract and other work, or is necessary to theoverall operation of the business.ReasonablenessA cost is reasonable if, in its nature and amount,it does not exceed that which would be incurredby a prudent person in the conduct ofcompetitive business.“Audits can identifyopportunities to improveperformance againstcontract requirements."But not every audit is aimed at uncoveringmalfeasance. Audits can also identifyopportunities to improve performance againstcontract requirements. According to theDCAA’s strategic plan, one of its keyaccomplishments between 2011 and 2015 was a30 percent improvement in meeting agreed-todates. That is in addition to the 19.7 billionsavings and a doubling in the number ofexpended dollars examined for things likecompliance with Defense Federal AcquisitionRegulation Supplement (DFARS).At a high level, the DCAA audit of a contract orexpenditure will focus on three variables:AllowabilityThe cost is allowable when it is reasonable,allocable and complies with Federal AcquisitionRegulation (FAR) 31.205, CAS (Cost AccountingStandards), laws and regulations, and the termsof the specific contract.ERP for defense audit compliance03

The information to determine compliance withthese requirements comes largely from within anERP application or other accounting system ofrecord. This accounting system must also beapproved, pre-contract. According to a DCAAchecklist, an approved accounting system must bein full operation and provide for: P roper segregation of direct costs from indirectcosts. I dentification and accumulation of direct costsby contract. A logical and consistent method for the allocationof indirect costs to intermediate, and final costobjectives. (A contract is a final cost objective.) A ccumulation of costs under general ledgercontrol. A timekeeping system that identifies employees’labor by intermediate or final cost objectives. A labor distribution system that charges directand indirect labor to the appropriate costobjectives.Getting ERP rightAs the system of record, ERP is the central toolused to support an audit, and to ensure throughcentralization of business processes that thebusiness is auditable and compliant withcontract requirements and governmentregulations. But exactly how does ERP softwaresupport these auditability requirements? Arecertain ERP packages “approved” or compliantout of the box? What features in ERP arenecessary for DCAA compliance? How should amanufacturer or contractor go about selectingand implementing ERP for DCAA compliance?One thing that anyone involved in the defensecontracting or manufacturing space will seefrom time to time is marketing materials thatsuggest that a given enterprise softwarepackage is DCAA compliant. But this may be agross oversimplification that borders onmisrepresentation.An enterprise application like ERP can usuallybe configured to conform to DCAA auditrequirements. It may be configured so onlyallowed costs accrue against a given contract,for instance. It could just as easily beconfigured to allow inappropriate costs toaccrue against a contract. What this means isthat no ERP product is, by itself, DCAAcompliant. A great deal rests onimplementation, the knowledge and skills of theimplementation team and a rigorous anddisciplined approach to government projectaccounting.ERP for defense audit compliance I nterim (at least monthly) determination of costscharged to a contract through routine posting ofbooks of account. E xclusion from costs charged to governmentcontracts of amounts which are not allowable interms of FAR 31, Contract Cost Principles andProcedures, or other contract provisions. I dentification of costs by contract line item and byunits (as if each unit or line item were a separatecontract) if required by the proposed contract. S egregation of preproduction costs fromproduction costs. F inancial information required by contract clausesconcerning limitation of cost (FAR 52.232-20 and21) or limitation on payments (FAR 52.216-16). Support for requests for progress payments. R ecords maintained in such a manner thatadequate, reliable data are developed for use inpricing follow-on acquisitions.04

Do the due diligenceSelecting and then implementing ERP for DCAA,therefore, requires a high degree of duediligence during the selection cycle and asound methodology for implementation.The right integrated application will makecompliance easier. The governmentappreciates full access to information in anefficient and effective way. Features that canhelp deliver this include:Actual costing. In many implementations,actual costing is desirable as it is the DCAA’spreferred method for most programs andcontractors. Other methods like standardcosting may be workable, but it is hard to arguethat the DoD’s preferred method should not bethe goal contractors strive for.Fully integrated functionality. Data to supporta thorough DCAA audit can come from anynumber of places. A fully integrated suite ofsoftware will make it easier to collect data fromvarious sources including customer orders,purchase orders, shop orders and governmentproperty records.Broad project accounting functionality. It is notuncommon for DCAA to audit overall financesof a project. And when they do, they will want todrill down to associated objects, such aspurchase orders, that confirm the costs in thegeneral ledger. This means transactional datashould be organized by project or program, soduring an audit you can drill down and supplyDCAA with information specific to that projectfrom any number of data points.“The right integratedapplication will makecompliance easier."ERP for defense audit compliance05

Perhaps you are building a test setup for aproject, and you need to purchase somelaptops. Normally, those would be consideredan indirect cost or overhead, and depreciatedas a capital expense. But if these laptops aregoing to be consumed exclusively on behalf ofthis government program, they would be anallowable cost. The ability to tie expenditureslike this firmly back to a project is of particularimportance in the cost-plus environment,where extraneous expenses that cannot becharged can easily put a contract in the red.An ERP system properly configured forgovernment audit compliance will include bidsolicitation functionality. The system will thendocument the bidding process, the criteria forselection and the ultimate supplier selection.So, in proving reasonableness, you can sourcedata from what bids were received. It is notnecessary to prove that you selected thelowest bid, but rather document reasons formaking the selection decision that you did.Reasonableness of labor costs must also bedocumented. This can be done by reviewingthe history of labor cost on similar projects.ERP for defense audit complianceA project with a similar scope and level of effortcan be identified and used to establish ahistorically reasonable cost for labor.Apart from tracking cost, ERP for DCAA mustaccount for borrow-payback. This means ERPmust be organized around specific contracts,accounting for the degree to which inventoryfrom the project can be borrowed by otherprojects and to what extent they can borrowfrom other projects. Some contracts forbidborrow-payback. And those that allow it carryrequirements regarding the cost at whichborrowed inventory is replaced. Must theborrowing contract pay the price at which thematerial or inventory was originally purchasedby the contractor, or at the price thegovernment pays for the material or inventory?The government is naturally concerned withsuch things as they do not want to loan materialto another project only to find they have to paya higher price to replace it. ERP for DCAAcompliance must facilitate initial approval bythe government customer of the borrowing ofmaterial as well as the ensuing cost transferand payback.06

8 advanced tips for selection andimplementation1. L ook for a well-integrated ERP system versusa collection of best-of-breed solutions. Theamount of time and effort required to bring acollection of best-of-breed solutions togetherin a way that will channel and track costs in areliable and auditable fashion isconsiderable.2. No ERP software is certified out of the box forDCAA compliance. But you need to ask yourERP vendor if they have customers runningthe software in a DCAA compliantenvironment.3. Watch for industry-specific process modelsthat can streamline implementation forDCAA compliance. The existence of theseprocess models will indicate that a vendorhas long experience in a DCAA compliantenvironment, which reduces risk.4. As early as the initial screening of vendors,start thinking about how you need to presentdata to a government auditor, how youdistribute cost and how you define cost,traceability of information. Build theseconsiderations into a demo script vendorsmust take you through.6. Remember that actual cost can be hard topin down. In order to deliver reliable actualcosting, an ERP application just goes beyondcost at receipt. The invoice often reflects aslightly different cost than what wasunderstood when materials are delivered.So, ERP must be able to re-cascade costsbased on any changes that come to light inaccounts payable.7. A sk a lot of questions about borrow-paybacklogic. In order to comply with DCAA audits,some companies find they must also adhereto traceability of material transfer for borrowpayback logic. Optimal enterprise softwaremust include a process for netting groupsthat define how different groups of contractscan interact.8. Realize that in a cost-plus environment, asmuch indirect cost as possible must beallocated to projects or contracts. A lot ofcost would traditionally be consideredoverhead, but in a cost-plus environment, asmuch cost as is feasible needs to beallocated to projects.5. Consider all of the elements that go intoactual costing. In today’s environment,auditors are more likely to conduct afull-blown audit of a given project orcontract, and take deep dives into relateddocumentation. So, you will need to considerhow easy it is to drill down from a project orthe general record into the supportingdocumentation for each expense.ConclusionDefense agency audits of their contractors maybe something that must be done to avoid costand negative repercussions of failure to comply.But you can also see them as a way todemonstrate the value you are delivering toyour defense agency customer and win morework. The right ERP software will help youcreate solid, auditable business processes,preferably with predefined, template processflows. It will allow you the flexibility todocument, in great detail, the validity of yourinvoices. And it will automate a lot of theextremely complex requirements that inspireconfidence in your business.Matthew Medley, IFS Industry Director, DefenseERP for defense audit compliance07

About IFSIFS develops and delivers enterprise software for companies around theworld who manufacture and distribute goods, build and maintain assets,and manage service-focused operations. Within our single platform, ourindustry specific products are innately connected to a single data modeland use embedded digital innovation so that our customers can be theirbest when it really matters to their customers—at the Moment of Service.The industry expertise of our people and of our growing ecosystem,together with a commitment to deliver value at every single step, hasmade IFS a recognized leader and the most recommended supplier inour sector. Our team of 4,000 employees every day live our values ofagility, trustworthiness and collaboration in how we support our 10,000 customers. Learn more about how our enterprise software solutions canhelp your business today at ifs.com.Americas 1 888 437 4968Asia Pacific 65 63 33 33 00Europe east 48 22 577 45 00Europe Central 49 9131 77 340France, Benelux and Iberica 33 3 89 50 72 72Middle East and Africa 971 4390 0888Nordics 46 13 460 4000Copyright 2021 industrial and financial systems, IFS AB. IFS and all IFS products and services names are trademarks of IFS. All rights reserved. This document maycontain statements of possible future functionality for ifs’s products and technology. Such statements are for information purposes only and should not be interpreted asany commitment or representation. The names of actual companies and products mentioned herein may be the trademarks of their respective owners.Production: EDC Design, May 2021Uk & Ireland 44 178 42 78 222

the software in a DCAA compliant environment. 3. Watch for industry-specific process models that can streamline implementation for DCAA compliance. The existence of these process models will indicate that a vendor has long experience in a DCAA compliant environment, which reduces risk. 4. As early as the initial screening of vendors,