Transcription

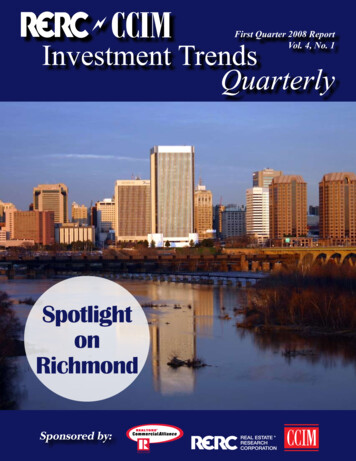

First Quarter 2008 ReportVol. 4, No. 1Investment TrendsQuarterlySpotlightonRichmondSponsored by:

InThisVolumeNow Available!National OverviewEconomic SummaryEffect on Real EstateProperty Sector Highlights“Richmond/Hampton Roads: Bright Outlookfor Virginia’s Top Markets”ContributorsScope & MethodologyRegional and Metro-LevelAnalyses Coming Soon!East RegionBaltimore, Boston, Charlotte, Hartford, Norfolk,Northern New Jersey, New York City, Pittsburgh,Philadelphia, Raleigh, Richmond, Washington, D.C.South RegionAtlanta, Austin, Dallas/Ft. Worth, Houston, Memphis,Miami, Nashville, New Orleans/Baton Rouge,Oklahoma City, Orlando, San Antonio, TampaMidwest RegionChicago, Cincinnati, Cleveland, Columbus, Detroit,Indianapolis, Kansas City, Milwaukee, Minneapolis,Omaha, St. Louis, ToledoWest RegionDenver, Honolulu, Las Vegas, Los Angeles, Phoenix,Portland, Sacramento, Salt Lake City, San Diego,San Francisco, Seattle, TucsonInvestment TrendsQuarterlyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

ForewordFebruary 2008Dear Readers,As the year 2008 gets underway, many investors expect significant changes in the U.S. economy, and as a result,in the commercial real estate market. The recent reductions in the federal funds rate and the anticipated stimuluspackage designed to ignite both business and consumer spending are strengthening our economic outlook, butthere is still a sense of unease that the subprime mortgage crisis, which has greatly affected the residential realestate market, may spill over into the commercial markets. Commercial real estate fundamentals remain strong, butthere remains risk as we peel back the layers and examine more closely the difficulties ahead.Such risk is why continued research about pricing and other investment issues in the various markets and with thedifferent property types is so critical. And that is why we are pleased to present to you this new issue of the RERC/CCIM Investment Trends Quarterly. Regularly priced at 395/year, the RERC/CCIM Investment Trends Quarterly is free to all CCIM designees and candidates, and serves as one of the no-cost benefits provided with yourmembership to the CCIM Institute. In addition to the economic and real estate overviews, there is property sectorpricing and capitalization rate analysis for the national and regional markets and for 48 metropolitan regions. Eachissue of the report also includes a feature article about commercial real estate in one of the 48 markets, with thefocus in this issue on the Richmond, Va., area.To make this research report even more valuable to CCIM members, we encourage you to share your transactioninformation. Here’s how to add a completed transaction: At www.ccim.com, go to the Member Services category,Click on the CCIM Transactions link (you’ll be prompted to enter your regular username & password),Under the Professional Profile section, click the Manage Completed Transactions link, andEnter the transaction.Thanks to all of you who contributed raw research through surveys, conversations, transactions, and shared reports.We appreciate your insights and your willingness to share your information with us, as we continue to provide thiskey research to the real estate industry.Best wishes for good health, good fortune, and a happy and prosperous 2008.Sincerely,Kenneth P. Riggs, Jr., CCIM, CRE, MAIPresident & CEOReal Estate Research Corporation (RERC)Investment TrendsQuarterlyTimothy S. Hatlestad, CCIM2008 CCIM Institute PresidentPresident, RE/MAX Commercial InvestmentCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

PeelingAwaytheLayersAlthough there is a strong sense that the recent aggressiveactions by the Federal Reserve to reduce the federal fundsrate, along with the anticipated economic stimulus package,will help to prevent a recession, wary investors remainconcerned about the risks that remain as we continue topeel away the layers of uncertainty associated with investingin the commercial real estate market.It is important to keep in mind that real estate fundamentalsare holding on, and with high construction costs, overbuildingis generally not a problem. However, with slower employmentgrowth and a reduced demand for space, we expect vacancyrates to increase slightly. Although some investors aredialing back on earning expectations, private commercialreal estate is holding its own reasonably well. Commercialreal estate pricing did not get too far ahead of the spacemarket fundamentals; therefore there is ample equity anddebt capital from unsecuritized sources that is saving thecommercial real estate industry from following the fate of thesubprime market. As a result, commercial real estate remainsrelatively attractive, with solid, stable returns expected(although possibly lower than during the last few years) andwithout the volatility characterized by the stock market.Even with the various market disruptions, however,commercial real estate looks more stable than stocks orbonds. RERC expects prices and returns to continue tostabilize during the coming year, which will bode well forthose investors that are discriminating and selective aboutthe property types and markets in which they invest. As it is,successful investors will have to face the market realities of2008, and let go of unrealistic return expectations from thepast.EconomicSummary Gross domestic product (GDP) growth slowed in fourthquarter 2007, ending the year at a seasonally-adjusted advance rate of 0.6 percent for the quarter. The expected decline was due in large part to decreasing inventories anda slowdown in federal and consumer spending. GDP grewat a revised seasonally-adjusted rate of 4.9 percent in thirdquarter, 3.8 percent in second quarter, and 0.6 percent infirst quarter. For all of 2007, GDP grew at 2.2 percent, following 2.9 percent growth in 2006, according to the Bureau of Economic Analysis (BEA).Investment TrendsQuarterly The Federal Open Market Committee (FOMC) continuedto aggressively reduce rates in an effort to fend off recession by slashing the federal funds rate to 3.0 percent. The50-basis-point cut came at their Jan. 30, 2008 meeting, following a 75-basis-point reduction at a special intermeetingon Jan. 22, 2008. The nation’s trade deficit narrowed to 63.12 billion in November 2007, but was still well above the level expectedfor that reporting period, reported the Commerce Department. Exports rose to a seasonally-adjusted 142.3 billion,while imports rose slightly to 205.4 billion. The Federal Reserve Board noted in its Jan. 16, 2008Beige Book that the national economy continued to growfrom mid-November through December, but at slower ratedue to sluggish retail and automotive sales. The seasonally-adjusted national unemployment rate increased to 5.0 percent in December 2007 from 4.7 percentin November, according to the Bureau of Labor Statistics(BLS). CCIM member respondents to RERC’s fourth quarter 2007survey rated the U.S. economy at 4.0 on a 10-point scale,with a score of 10 representing a very strong economy anda 1 representing a very weak economy. This is quite a bitlower than the third-quarter rating of 5.4, indicating increasing fears about the strength of the national economy. According to the Jan. 16, 2008 Beige Book, business lending was down from the previous reporting period. Levels ofconsumer lending and residential mortgage lending continued to decline in most areas. Non-farm business productivity increased 6.3 percent inthird quarter 2007, compensation per hour increased 4.2percent, and unit labor costs decreased 2.0 percent. Manufacturing productivity grew 5.0 percent, as compensationper hour increased 1.5 percent and unit labor costs fell3.3 percent. Although productivity numbers were revisedsharply upward from previous estimates, they are not expected to remain as strong in 2008. According to the Institute for Supply Management, themanufacturing index decreased to 47.7 in December following a reading of 50.8 in November. (A reading above50 indicates that the manufacturing economy is generallyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

EconomicSummaryexpanding; a reading below 50 indicates that the manufacturing economy is generally contracting.)percent in October. Personal consumption increased 0.2percent in December, following increases of 1.0 percent inNovember and 0.3 percent in October. New orders for manufactured goods decreased 6.9 percent in December 2007, and production decreased 4.6percent. Exports decreased 6.0 percent, while imports increased 0.5 percent. The consumer confidence index declined to 87.9 in December 2007 from 88.6 in November, according to theConference Board. The present situation index increasedto 115.3 in December from 112.9 in November. The expectations index declined to 69.6 in December from 75.8in November. According to the BLS, the producer price index for finishedgoods decreased 0.1 percent in December 2007, following a 3.2-percent increase in November and a 0.1-percentincrease in October. The finished goods index increased0.2 percent in December and 0.4 percent in November,and remained unchanged in October. The BLS reported that the consumer price index for all urban consumers increased 0.3 percent in December 2007(after seasonal adjustment), 4.1 percent higher than yearago averages. Although year-ago averages increasedduring December, overall inflation continued to remain lowduring the quarter. According to the BEA, personal income increased 0.5 percent in December 2007, 0.4 percent in November, and 0.2NAR U.S. Economic Outlook: January 20082007 Quarterly2008 Quarterly2009 9Real arm Payroll .6Consumer al Disposable Consumer yment4.54.54.74.85.15.25.35.35.35.24.64.65.35.1Fed Funds nth T-Bill e orate Aaa Bond Year Government ear Government al Growth RateInterest Rates, PercentSource: Forecast produced using Macroeconomic Advisers quarterly model of the U.S. economy.Quarterly figures are seasonally-adjusted annual rates.Assumptions and simulations by NAR's Dr. Lawrence Yun.Investment TrendsQuarterlyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

TheEffectonRealEstate According to the Jan. 16, 2008 Beige Book, the residentialreal estate market continued to weaken in most districts,due in large part to historically high inventories and muchslower sales. However, it is reported that many areas areseeing strong declines in new home construction, helpingto reduce the inventory of unsold homes. The market as awhole is expected to remain weak in 2008. According to the National Association of REALTORS (NAR), existing home sales fell to 4.89 million in December 2007 from 5.00 million in November. Total home salescontinue to be at the lowest level seen since tracking began in 1999. The median home price for existing homes in December2007 was 208,400, nearly 6 percent lower than the median price reported a year ago, according to NAR. The Commerce Department reported that single-familyhousing starts in December 2007 decreased to a seasonally-adjusted annual rate of slightly more than 790,000, a2.9-percent decrease from November. Approximately 1.0million single-family housing completions occurred in December, 12.0 percent below those for November. In addition, approximately 690,000 single-family building permitswere issued in December, 10.1 percent below Novemberpermits. Total new construction remained relatively unchangedfrom November to December 2007, at a seasonally-adjusted annual rate of 518.4 billion, according to McGraw-HillConstruction. For the year, total construction starts weredown for the first time since 1991. Nonresidential buildingdecreased about 1 percent in December to an annual rateof nearly 188 billion, and residential building increasedabout 3 percent in December to an annual rate of nearly 222 billion. Fundamentals for commercial properties were mixed,according to the Federal Reserve’s Jan. 16, 2008 BeigeBook, but most districts saw steady rental and vacancyrates. Most districts reported a slowdown in commercialconstruction, a trend that is expected to continue throughout 2008. CCIM designees and candidates continued to rate commercial real estate as the top investment alternative (overstocks, bonds, and cash). Commercial real estate earneda 6.0 rating, while cash was rated at 5.9, bonds at 4.7, andstocks at 3.9, on a scale of 1 to 10, with 10 being high. Survey respondents rated the overall “return versus risk”for the commercial real estate market during fourth quarter2007 at 5.3 on a scale of 1 to 10, with 10 being high, indicating that respondents perceive a slightly higher return isbeing received on commercial properties versus the risktaken. At 7.0 on a scale of 1 to 10, with 10 being high, the apartment market received the highest “return versus risk” rating during fourth quarter 2007. CCIM respondents rated the “return versus risk” of the retail and office sectors below 5.0 on a scale of 1 to 10, with10 being high, demonstrating their view that the risk of investing in these property types is higher than the amountof returns received.Average Rating* by Survey Respondents - 4Q urn vs. Risk4.65.44.77.05.55.3Value vs. Price4.34.64.46.05.14.5*Ratings are based on a scale of 1 to 10, where 1 is poor and 10 is excellent.Source: RERC.Investment TrendsQuarterlyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

TheEffectonRealEstate Fourth quarter 2007 survey respondents rated the overall“value versus price” of commercial real estate at 4.5 on ascale of 1 to 10, with 10 being high, a half-point lower thanthe previous quarter’s rating of 5.0. This rating indicatesthat respondents feel commercial real estate has less value than the price paid. Many fourth quarter 2007 survey respondents stated thatthe industrial sector offers the greatest opportunity for investment during the next year due to increased warehousespace for the exporting of goods and the sector’s lack ofactivity during the last few quarters. The majority of fourth quarter 2007 survey respondentsstated that the retail sector offered the lowest investmentopportunities for the next year due to slowdowns in consumer spending, less demand, higher vacancy, and overdevelopment.In Summary: During fourth quarter 2007, a variety of economic indicators began to show signs of the predicted slowdown,with job growth down and consumers spending slowing,to name a few. However, with the expected reduction ininterest rates and the economic stimulus, RERC continuesto expect the economy to grow during 2008, but at a muchslower rate than we have seen in the recent past. Commercial real estate is still in slightly higher favor thanalternative investments, according to RERC’s survey results, although cash is gaining ground. RERC believesthat the commercial real estate market remains a stronginvestment vehicle. However, continued compression ofcapitalization rates in some property types will help to address overpricing issues. Overall, investors will have to face new market realitiesduring 2008, and let go of what may be considered unrealistic return expectations from the past. Prices and returnswill continue to stabilize during the coming year, and willhelp commercial investment remain a preferred investment alternative.What Do the Financial Markets Tell Us?Compounded Annual Rates of Return as of 12/31/2007Market Indices1-Year3-Year5-Year10-Year15-YearConsumer Price Index4.08%3.34%3.03%2.68%2.65%10-Year Treasury Bond*4.63%4.57%4.40%4.86%5.38%Dow Jones Industrial Average6.43%7.15%9.72%5.31%9.72%NASDAQ Composite9.44%7.38%13.92%5.44%9.73%NYSE Composite6.58%10.34%14.27%6.07%9.37%S&P 5003.53%6.61%10.79%4.23%8.44%NCREIF Index15.85%17.50%15.20%12.99%11.29%NAREIT Index-16.61%6.62%16.96%9.78%12.43%*Based on Average End of Month T-Bond RatesSources: Economy.com, Federal Reserve Board, BLS, NYSE, NCREIF, NAREIT, compiled by RERCInvestment TrendsQuarterlyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Real Estate Indicators - 4Q 2007Performance IndicatorRecent DataImpact on Commercial Real EstateConsumer ConfidenceJanuary 2008 - 87.9December 2007 - 88.6November 2007 - 87.8October 2007 - 95.6September 2007 - 99.5Consumer confidence continued to decline during the majority of fourth quarter 2007and into 2008. With fears of a weakening economy continuing, the retail and hotel sectors could suffer, as discretionary spending may slow.Consumer Spending(percent change fromprevious month)November 2007 - 1.1%October 2007 - 0.4%September 2007 - 0.5%August 2007 - 0.4%July 2007 - 0.4%Although consumer confidence increased during November 2007, consumer spendingincreases have been slight. With recession fears continuing, consumer spending mayslow, affecting retail and hotel properties more than the other commercial real estatesectors.Real GDP(seasonally adjustedannual rates in billions)4th Quarter 2007 - 14,080.8 (advanced)3rd Quarter 2007 - 13,970.52nd Quarter 2007 - 13,768.81st Quarter 2007 - 13,551.94th Quarter 2006 - 13,392.3Evidence of slowing appeared in fourth quarter 2007 when GDP growth declined to lessthan 1 percent due to a slowdown in consumer and federal spending. The slowdownlikely will affect all commercial sectors as investment slows.Unemployment Rate(seasonally adjusted)December 2007 - 5.0%November 2007 - 4.7%October 2007 - 4.8%September 2007 - 4.7%The unemployment rate increased in December 2007 as job growth fell. Retail, construction, and manufacturing jobs decreased sharply in December. Investment in commercialreal estate may suffer, as less space will be needed for fewer jobs and less demand forgoods.Federal Funds RateJanuary 30, 2008 - 3.0%January 22, 2008 - 3.5%December 11, 2007 - 4.25%October 31, 2007 - 4.5%September 18, 2007 - 4.75%The Federal Reserve further reduced the target rate in December, with even larger decreases coming on Jan. 22, 2008 and Jan. 30, 2008. The rate deductions were triggeredby increased unemployment and fiancial market fears. This may help the commercialreal estate market, as borrowing rates will continue to fall.10-YearTreasury RatesJanuary 24, 2008 - 3.68%December 31, 2007 - 4.04%November 30, 2007 - 3.97%October 31, 2007 - 4.48%September 28, 2007- 4.59%Long-term rates were down in fourth quarter 2007, spurred on by the reduction in thefederal funds rate. Low treasury rates should increase investment in the commericalmarket, but growth may not be as strong as expected due to slower demand and lowerrental growth.S & P 500 IndexJanuary 24, 2008 - (7.92%) YTD ReturnDecember 31, 2007 - 3.53% YTD ReturnNovember 30, 2007 - 4.43% YTD ReturnOctober 31, 2007 - 9.245% YTD ReturnSeptember 28, 2007 - 7.65% YTD ReturnThe stock market continued its roller coaster ride during fourth quarter 2007 and early2008. With interest rates dropping and returns and prices on properties stabilizing, thecommercial real estate market likely will regain some of the investment dollars lost to thestock market’s earlier strong performance.Existing Home Sales(seasonally adjusted,in millions)December 2007 - 4.89November 2007 - 5.00October 2007 - 4.98September 2007 - 5.03Existing home sales continued to decline during fourth quarter 2007. This should positively affect apartment fundamentals, but at a much slower pace than at the beginning ofthe residential market crisis.Vacancy RatesOffice (TWR) 12.5% unchanged from 12.5% in 3Q06Industrial (TWR) 9.4% up from 9.2% 3Q06Retail (TWR) 8.7% down from 8.9% in 2Q06Apartment (Reis) 5.4% down from 5.6% 3Q06Overall, vacancy rates for commercial real estate remained positive during fourth quarter2007. Although vacancy rates reflect increased strength in the market as a whole, theyare very market-specific.Rental Rates(RERC’s surveyed rentgrowth expectations)Office - 2.7% to 3.0%Industrial - 2.5% to 2.6%Retail - 2.4% to 2.6%Apartment - 2.9%Hotel - 2.7%Although RERC’s fourth quarter 2007 rental growth expectations remain positive, theyare lower than those for third quarter. This puts returns at risk, as capitalization ratecompression is drastically lower, and returns will need to be found elsewhere.Real Estate ReturnsRERC’s Required Returns:Office - 7.8% to 8.3%Industrial - 8.0% to 8.5%Retail - 7.9% to 8.1%Apartment - 8.0%Hotel - 9.3%NCREIF Realized Returns:Office - 18.0% to 24.3%Industrial - 14.5% to 18.4%Retail - 9.3% to 16.8%Apartment - 11.4%Hotel -18.1%Although still high, total commercial real estate returns decreased in fourth quarter 2007.Expect continued stabilization of returns in 2008, as rates are expected to continue todecline to more normal levels.Capitalization RatesRERC’s Realized Cap Rates:Office - 5.6%Industrial - 6.7%Retail - 6.4%Apartment - 5.8%Hotel - 7.7%NCREIF Implied Cap Rates:Office - 5.1% to 5.8%Industrial - 6.0% to 6.3%Retail - 5.8% to 6.0%Apartment - 4.7%Hotel - 7.6%RERC’s fourth quarter 2007 required capitalization rates increased slightly while NCREIFimplied capitalization rates decreased slightly. As noted last quarter, captialization rateshave bottomed out in most markets, and asset management will become absolutelycritical to income generation and value creation. Rates will continue to stabilize in 2008,further calming fears of asset overpricing.Investment TrendsQuarterlyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

NAR Commercial Forecast (December cy Rate (%)12.712.412.512.913.113.213.212.612.913.2Net Absorption (’000 sq. 55,40342,975Office Employment 14316,70716,99617,207Completions (’000 sq. 671,88461,707Inventory (millions sq. ,4604.30.31.71.71.1.5.25.28.02.0Rent Growth (%)INDUSTRIAL9.39.39.29.49.69.59.59.49.49.5Net Absorption (’000 sq. 365127,424143,975Industrial Employment 28610,23510,28110,288Completions (’000 sq. 979140,822171,240Inventory (millions sq. y Rate (%)Rent Growth (%)RETAIL8.38.78.68.98.88.68.68.08.98.6Net Absorption (’000 sq. 424,744Completions (’000 sq. 2620,750Inventory (millions sq. 35.14.85.95.45.1Net Absorption 229,452234,399245,786Completions 24,170230,932216,880Inventory (Units in ent Growth (%)0.70.70.80.91.01.31.44.13.13.8Vacancy Rate (%)Rent Growth (%)MULTIFAMILYVacancy Rate (%)Sources: NAR, CBRE/Torto Wheaton Research.Investment TrendsQuarterlyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

Commercial RealEstate Index Levels Outin Third QuarterCommercial real estate market activity is expected to level out, suggesting stablebusiness opportunities for commercial practitioners in the months ahead, according to a forward-looking index for the commercial real estate sectors published bythe National Association of Realtors (NAR).The Commercial Leading Indicator for Brokerage Activity slipped 0.1 percent toan index of 120.6 in third quarter 2007 from a record reading of 120.7 in secondquarter, but remains 0.6 percent higher than third quarter 2006 when it stood at120.0. NAR’s track of the index dates back to 1990.Lawrence Yun, NAR chief economist, said momentum in the commercial marketappears to be leveling at a high plateau. “Commercial real estate has been performing quite well over the past few years, and the flattening index means net absorption of space in the industrial and office sectors is likely to contract modestlyor hold over the next six to nine months,” he said. “This trend is consistent withanticipated slower economic expansion in upcoming quarters.”There should be no measurable change in net absorption in the office and industrial sectors in the first quarter of 2008, and no measurable change in newlycompleted commercial construction activity.The level of the commercial leading indicator also implies that commercial realestate practitioners could expect leasing and sales activity in the first quarter ofnext year to be about 0.7 percent higher than the first quarter of 2007.The commercial leading indicator is a tool to assess market behavior in the majorcommercial real estate sectors. The index incorporates 13 variables that reflectfuture commercial real estate activity, weighted appropriately to produce a singleindicator of future market performance, and is designed to provide early signalsof turning points between expansions and slowdowns in commercial real estate.The 13 series in the index are industrial production, the NAREIT (National Association of Real Estate Investment Trust) price index, NCREIF (National Council ofReal Estate Investment Fiduciaries) total return, personal income minus transferpayments, jobs in financial activities, jobs in professional business service, jobsin temporary help, jobs in retail trade, jobs in wholesale trade, initial claims forunemployment insurance, manufacturers’ durable goods shipment, wholesalemerchant sales, and retail sales and food service.Nearly 140,000 NAR members offer commercial services, and 73,000 of thoseare currently members of the Realtors Commercial Alliance, NAR’s commercialdivision.This information is reproduced in part from the December 2007 “Commercial Real EstateOutlook,” a newsletter published by the REALTORS Commercial Alliance and with theirpermission.NAR Commercial Forecast (July 2007)CommercialLeading% Change from % Change fromIndicator1 Quarter Ago1 Year 12Q111.90.5-2.120062005200420032002Source: NAR.125Commercial Leading ource: NAR.Investment TrendsQuarterlyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.

NationalMarketAnalysisNational Transaction Breakdown (1/1/07 - 12/31/07)OfficeIndustrialRetailApartmentHotel 3,075 5,090 5,446 6,084 342Size Weighted Avg. 89 52 85 74,326 33,335Price Weighted Avg. 129 88 131 112,736 58,202Median 93 59 84 83,333 35,938 5,777 8,790 9,657 7,646 1,696Size Weighted Avg. 121 61 137 70,828 40,723Price Weighted Avg. 192 104 244 136,505 60,940Median 167 85 212 99,874 44,295 236,480 46,109 64,063 95,549 58,522Size Weighted Avg. 264 78 176 106,825 192,735Price Weighted Avg. 452 129 279 178,605 520,218Median 196 91 188 101,014 112,500 245,332 59,989 79,166 109,278 60,560Size Weighted Avg. 251 72 159 100,788 170,330Price Weighted Avg. 442 122 265 171,992 504,748Median 150 72 132 91,667 96,3783.2 - 11.03.7 - 10.83.3 - 10.53.0 - 10.44.0 - 12.0Weighted Avg.5.66.76.45.87.7Median6.77.06.66.08.9 2 MillionVolume (Mil) 2 - 5 MillionVolume (Mil) 5 MillionVolume (Mil)All TransactionsVolume (Mil)Capitalization Rates (All Transactions)RangeSource: RERC.Investment Conditions Ratings* - 4Q el6.4*Ratings are averages based on responses to surveys from CCIM designees andcandidates for fourth quarter 2007.Investment TrendsQuarterlyCopyright 2008 by Real Estate Research Corporation (RERC) and the CCIM Institute.10

NationalOfficePropertySector CCIM designees and candidates who responded toRERC’s survey rated investment conditions for the office market during fourth quarter 2007 at 5.6 on a scaleof 1 to 10, with 10 being high, lower than the previousquarter’s rating of 6.1. According to RERC’s analysis of fourth quarter 2007sales, the average prices of office properties increasedslightly from third quarter, while average capitalizationrates for office property sales decreased. At 4.6 and 4.3, respectively, the office sector earnedthe lowest “return versus risk” and “value versus price”ratings among the major property types, indicating thatsurvey respondents feel the returns on office properties are less than the amount of investment risk, andthat the value of office properties overall is less than theprice paid for the investment.RERC Weighted Average Capitalization Rate7.5%EastSouthMidwestWestNationalCCIM survey respondents noted that in most regions, officedemand has slowed and vacancy rates in some areas – LosAngeles, Chicago, Las Vegas, Memphis, to name a few – areincreasing. One investor sees this as a good opportunity becauseof “less buyer competition due to the slowing economy,” andanother pointed out that “if an investor can hold on until thecredit crunch turns around, some money could be ma

quarter, 3.8 percent in second quarter, and 0.6 percent in first quarter. For all of 2007, GDP grew at 2.2 percent, fol- . Man-ufacturing productivity grew 5.0 percent, as compensation per hour increased 1.5 percent and unit labor costs fell 3.3 percent. Although productivity numbers were revised sharply upward from previous estimates, they .