Transcription

The Global AerospaceIndustrySize & Country Rankings16 July 2018

Aerospace is one of the world’s most important industries, yet thereis no consensus on its size and compositionThe best industry data is kept by national industry associations.yettheir definition of “aerospace” variesSome associations include non-aerospace, defense and security. It isunclear that out-of-country activities are excluded from estimates. It isalso unclear that civil and military operator MRO data is included.This joint assessment from Aerodynamic Advisory and Teal Groupincludes sub-tier supply chain activities and MRO2

AeroDynamic Advisory and Teal Group created an independentglobal aerospace industry size estimate based on a clear definition Aerospace Industry DefinitionThe aerospace industry includes all in-country activitiespertaining to the development, production, maintenance andsupport of aircraft and spacecraftIncluded in DefinitionAircraft manufacturing*Space manufacturing*Missile & UAV manufacturing*Airborne defense electronicsSimulator & ground support equip.MRO - transport aircraftMRO - military aircraftMRO - BGA aircraftResearch & developmentExcluded from DefinitionAirline operationsSatellite broadcasting servicesDefense - ground, maritime, C4ISRNon-aerospace defense electronicsTraining servicesInduced economic activity in other sectors* includes engines, systems, aerostructures & subtier suppliers3

and followed a four-step process to standardize nationalaerospace industry estimates12Collect national industryassociation baseline dataSubtract non-aerospaceand out-country activities3Add activity not includedin industry associationdata4Add estimated activity forcountries lacking anindustry associationand/or verifiable data4

The assessment includes sub-tier supply chain activities and a fullaccounting of maintenance, repair and overhaul (MRO) activityAerospace Manufacturing Supply Chain StructureOEMsAircraftOEMsAeroengineOEMsTier 1Systems &Major StructuresModules & MajorComponentsTier 2Parts & AssembliesParts & AssembliesTier 3Tier 4Make to print parts & componentsRaw materials, forgings, castings, extrusions &hardwareSource: AeroDynamic Advisory & Teal GroupMaintenance, Repair & Overhaul UpgradesThird-party MROsOEMs, OperatorsService Parts &MaterialSpecialist Repairs “Wrench-turning” MRO activities and upgradesconducted by MROs, OEMs and operators areworth 160-170 billion in civil and military sectors There is another 60 billion in service (spare)parts, material and specialty repairs consumed inMRO “wrench turning”5

The global aerospace industry is worth 838 billion; OEMs and subtier manufacturers comprise 54% of all activity2017 Global Aerospace IndustryOther7%Missiles & UAVs5%Aircraft & EngineOEMs28%Satellites & Space7% Civil and military aircraft and engineOEMs and their extended supply chainsaccount for nearly half of the globalaerospace economic activity Maintenance, repair, overhaul, andupgrades generated 27% (just over 200B) in economic activity Other activity, including simulatormanufacturing, defense electronics nototherwise captured, and researchperformed by government or non-profitassociations accounts for just over 7%of activityTotal: 838 BCivil & Military MRO &Upgrades27%Aircraft Systems & ComponentManufacturing26%Source: AeroDynamic Advisory & Teal Group6

The US accounts for 49% of the global aerospace industry2017 Global Aerospace Industry - 838 Billion The US boasts deep and broad civil and militaryaerospace clusters, and accounts for half of allaerospace activity France has the second largest industry, followed byChina, the UK and Germany The Americas is the largest region (54%), followedby Europe, Middle East, & Africa (31%) and AsiaPacific (15%)Source: AeroDynamic Advisory & Teal Group7

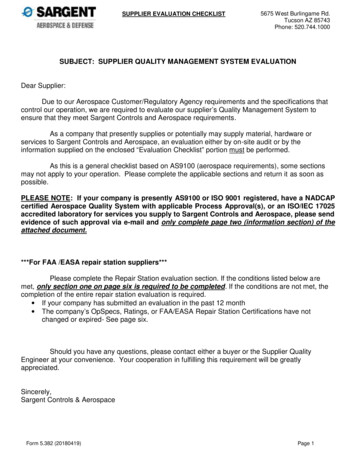

The Top Ten countries comprise 87% of the global industry2017 Global Aerospace Industry – Top 10 CountriesRankingCountryIndustry Size ( B)1United States 408.42France 69.03China 61.24United Kingdom 48.85Germany 46.26Russia 27.17Canada 24.08Japan 21.09Spain 14.410India 11.0 The aerospace industries of the top ten countriesare worth 731 billion – 87% of the global industry The United States comprises almost 49% of theworld aerospace total, more than the next 25countries combinedTOTAL 731BSource: AeroDynamic Advisory & Teal Group8

The US and France alone make up 57% of the global aerospaceindustry total#1: United States - 408.4 B High and rising defense procurement budgetsensure military segment growth into next decade#2: France - 69.0 B Share of total world aircraft output value at 50%with upward direction with F-35, 787 Second only to US as airframer; remarkable trackrecord as aeronautical leader; very high ratio ofexports. Second only to US as components,avionics, and other subsystems provider, too Extremely strong trade position reflects exportmarket dominance in most key segments(exceptions: second place in single aisle jets, andno regional aircraft market position) Last country in Europe with true combat aircraftself-sufficiency; Rafale success helping withbroader military standing, and futuredevelopment prospects Biggest civil airframer (Boeing), biggest militaryairframer (Lockheed Martin), biggest engine OEM(GE), and biggest systems OEM(UTAS/RC). Very high level of space systemsinnovation and development. Extremely diverse exposure to Jetliner, combat,business aircraft, rotorcraft, space, and missilesmarkets World leader in UAVs, by any measure: dollarvolume, variety of systems, technology Big weakness: Airbus twin aisle marketuncertainty, A380 uncertaintySource: AeroDynamic Advisory & Teal Group High level of government support for new productdevelopment and export sales9

China now boasts the third largest national aerospace industry andcontinues to grow#3: China - 61.2 B Continued focus on copying Western jetliner designs andbuilding existing Western jetliners in-country. Lowest percentage of export sales of any top tenaerospace producer; minimal presence on Westernplatforms. Efforts to replicate Western vertical supplier bases forindigenous development programs represent a veryexpensive and risky approach to industry development. Historical focus on building, replicating, modifying, andsustaining Russian fighters; now shifting towardsexperimental stealth fighters (J-20, J-31) and newindigenous military aircraft (Y-20). Overall, very high levels of expenditure and employment;very low levels of productivity, output, and profit. Third largest aerospace industry but largest aerospacetrade deficit in the world Despite these problems, China on par to be largest jetlinermarket in the world, with very high resources andtremendous talent.Source: AeroDynamic Advisory & Teal Group#4: UK - 48.8 B Very high ratio of exports to domesticconsumption; heavy presence on US andEuropean platforms. Special Relationship with USstill key. Exiting role as military prime (civil prime statusabandoned over a decade ago); world leading roleas risk-sharing partner. Increasing defense procurement without domesticcontent a concern. Big questions: trade relations with Europe (andthe world) post-Brexit; access to Europe-wideprograms and development funding Very high ratio of aftermarket and sustainmentwork relative to new-build. Extensive global holdings and work by UKcompanies not in our numbers.10

Germany and Russia together account for 73 billion of the 838billion total#5: Germany - 46.2 B#6: Russia - 27.1 B Growing Airbus single aisle facility in Hamburg;A320 added to portfolio this year Very high ratio of military to civil work; attemptinga civil comeback with MS-21 and CR929 Very high ratio of exports High ratio of exports to domestic use Low defense spending damagingcompetitiveness and sustainment work Two key export markets at risk; China movingtowards indigenous developments, India movingtowards Western aircraft Highly innovative subsystems and manufacturingtechnology development aided by strong R&Dfunding High level of international partnerships;considerable work performed elsewhere and notin our Germany total Tornado replacement, next-generation combataircraft will play large roles in determiningindustry’s future direction; cooperation withFrance (rather than UK) may be problematicSource: AeroDynamic Advisory & Teal Group Other export markets highly problematic (Libya,Algeria, Syria) or Former Soviet Union Risky model of using intellectual property ascontribution towards Joint Ventures. FGFA withIndia seems to have gone wrong; CR929 withChina at risk too11

Canada and Japan have similar sized aerospace industries#7: Canada - 24.0 B High level of vertical domestic content onBombardier platforms; this has created deepernational risk Transition from failed Bombardier C Series topotentially successful Airbus A200 may threatennational aero output if Airbus moves work Positive: Bombardier now able to prioritize andrestore strong business jet market position Negative: Highly uncertain future for Bombardierregional platforms Pratt & Whitney Canada remains second mostimportant company, with strong growth prospects,followed by Bell Helicopter; many successfulsmaller providers#8: Japan - 21.0 B Historic willingness to pay much higher prices fordefense platform domestic assembly and content F-35 acquisition represents a return to off-theshelf fighter acquisition if that’s the future,domestic design work is at risk, and F-3 won’thappen However, C-2 and P-1 represent very ambitiousnew platforms; export markets highly uncertain Commercial supplier business very important;biggest source of US aerostructures imports Periodic efforts to create civil platforms generallyfail; MRJ hanging in balance Low defense budget a concern; limited defensemarket exposure. F-35 work at risk with RCAFfighter decisionSource: AeroDynamic Advisory & Teal Group12

While both in the Top Ten, Spain and India only account for 1% eachof the global total#9: Spain - 14.4 B#10: India - 11.0 B Large number of small and mid-sized suppliercompanies with emphasis on composites,subsystems, and space systems Difficult and uncertain transition from autarky andstate-owned companies to private sector firmsaiming at global partnerships Relatively low percentage of work performed outof country; strong levels of foreign investment Difficult and uncertain transition from indigenousplatforms to Western systems Last Spanish-designed and built productionaircraft, Airbus’s C-295, still selling in modestnumbers High level of failure, risk, and uncertainty withindigenous platforms Future direction uncertain with dependence ondwindling A400M output, national Eurofighter line Gradual, tentative move away from Russianplatforms; FGFA abandonment may be awatershed moment Very high potential due to large commercialmarket, very high defense spending, and stronglocal talentSource: AeroDynamic Advisory & Teal Group13

The next ten countries are headlined by Israel, Mexico and Italy2017 Global Aerospace Industry – Countries 11-20RankingCountryIndustry Size ( B)11Israel 10.312Mexico 9.513Italy 9.214Brazil 7.215Singapore 7.216South Korea 6.917Netherlands 4.618Australia 4.519Turkey 4.220Malaysia 3.7 Israel’s aerospace industry is dominated by IsraelAerospace Industries (IAI) a government ownedcompany involved in everything from commercial andmilitary aircraft to missiles, drones and avionics Fast-rising Mexico boasts hundreds of low costfabrication facilities Embraer and its local supply chain comprises most ofBrazil’s total While the aerospace industries of most countries inWestern Europe are focused on fixed wing airtransport aircraft, a large portion of Italy’s aerospaceindustry is dedicated to rotary wing aircraftTOTAL 67.3BSource: AeroDynamic Advisory & Teal Group14

The next ten largest countries have industries worth 26 billion2017 Global Aerospace Industry – Countries 21-30RankingCountryIndustry Size ( B)21Belgium 3.622Taiwan 3.223Sweden 3.124UAE 2.925Switzerland 2.526Indonesia 2.327Thailand 2.228Austria 2.129Norway 2.030Ireland 2.0 Belgium has both aerospace manufacturing and someMRO, although most of the former Sabena Technics,which was affiliated with the Belgian airline Sabena, isbased in Bordeaux, France Thailand’s aerospace industry is primarily focused onsub-tier component manufacturing, raw materialproduction, and MRO activity Although Ireland is one of the world’s largest aircraftleasing hubs, this activity is considered aviationrather than aerospace and is not included in the total Indonesia has ambitions to grow an indigenousaircraft OEM industryTOTAL 25.9BSource: AeroDynamic Advisory & Teal Group15

Saudi Arabia, Portugal and South Africa headline the next tencountries which total 12 billion2017 Global Aerospace Industry – Countries 31-40RankingCountryIndustry Size ( B)31Saudi Arabia 1.932Portugal 1.933South Africa 1.834Philippines 1.635Poland 1.336Morocco 1.137Czechia 0.9038Finland 0.8039Greece 0.6240Denmark 0.47 Countries 31-40 are primarily focused on MRO andlow-cost manufacturing Eastern European countries like Poland and Czechiaare hubs for airframe MRO and low-cost sources forthe engine supply chain Morocco has more than 100 aerospace facilitiesfocused on aerostructures, components and wireharnessesTOTAL 12.4BSource: AeroDynamic Advisory & Teal Group16

The aerospace industries of #41 – #45 countries are worth 1.5 billion2017 Global Aerospace Industry – Countries 41-45RankingCountryIndustry Size ( B)41Tunisia 0.4342Romania 0.3943Hungary 0.3344New Zealand 0.2245Chile 0.15 Tunisia is a growing low-cost source for EuropeanOEMs Hungary has a growing aerospace cluster with over130 companiesTOTAL 1.5BSource: AeroDynamic Advisory & Teal Group17

Thank you for your attention!www.aerodynamicadvisory.comSource: AeroDynamic Advisory & Teal Groupwww.tealgroup.com18

Presenter BiographiesRichard AboulafiaVice President – ResearchThe Teal

The Top Ten countries comprise 87% of the global industry Source: AeroDynamic Advisory & Teal Group Ranking Country Industry Size ( B) 1 United States 408.4 2 France 69.0 3 China 61.2 4 United Kingdom 48.8 5 Germany 46.2 6 Russia 27.1 7 Canada 24.0 8 Japan 21.0 9 Spain 14.4 10 India 11.0 The aerospace industries of the top ten countriesFile Size: 2MBPage Count: 19