Transcription

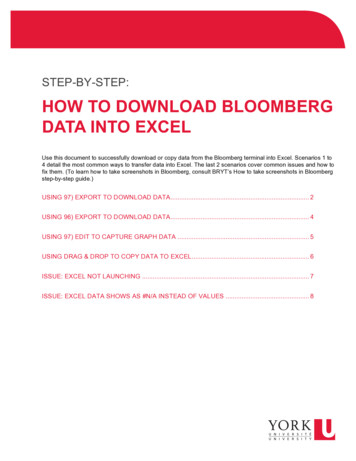

TuesdayJune 14, 2016www.bloombergbriefs.comMay Retail Sales, Import Prices; MSCI ClassificationQUOTE OF THE DAYBEN BARIS AND JAMES BATTY, BLOOMBERG BRIEF EDITORS"The issue is not whether or notthere is a bubble — it’s whetheror not the Fed actually movesand we move toward a flat topotentially inverted yield curve.It's not the level of interest rates,it's the level of the yield curve. Ifit starts to get inverted or getreally flat, that’s trouble."WHAT TO WATCH: Germany’s 10-year government bond yields tumbled below zerofor the first time on record, while four polls in the U.K. put the “Leave” campaign aheadof “Remain.” U.S. retail sales are expected to advance 0.3 percent in May following a1.3 percent gain in April, 8:30 a.m. Ex-autos sales are forecast to rise 0.4 percent. Alsoprinted at 8:30 a.m., import prices are expected to gain 0.8 percent last month after a0.3 percent gain in April. Business inventories for April are expected to rise 0.2percent following a 0.4 percent gain the month before, 10 a.m.ECONOMICS: The Federal Reserve begins its two-day policy meeting. The NFIB'sSmall Business Optimism Index rose to a level of 93.8 in May from a print of 93.6 themonth before.— Peter Borish, chief strategist at Quad CapitalGOVERNMENT: The District of Columbia holds its Democratic primary, the finalcontest in the U.S. presidential race.COMMENTARY IN THIS ISSUEMARKETS: MSCI Inc. will announce the results of its 2016 Annual MarketClassification Review shortly after 5 p.m., including whether Peru remains as anemerging market. Reclassification as a frontier market could trigger billions of dollars ofoutflows. The MSCI China A and MSCI Pakistan Indexes are also on the list for apotential reclassification to emerging markets.Never before have bond traders paid somuch to own trillions of dollars in debt andgotten so little in return: Susanne WalkerBarton and Liz Capo McCormick.(All times local for New York.)Retail Sales Green-Light Fed's 2016 Growth TargetU.S. consumers have long had animpressive propensity to get into debt —lately, though, the government has beenplaying a much bigger role in enablingthem: Mark Whitehouse.UBS Investment Bank's Drew Matusdiscusses corporate debt, globalmonetary policy and market distortion:Michael McKee and Tom Keene.DATA MONITORWhile the fate of the June FOMC meeting was sealed by the weak May jobs report, retailsales data could adjust the lens through which policy makers view current economic trends.Weak results could influence how the FOMC characterizes consumer activity, and in turn, howit views overall growth momentum, which is now tightly linked to consumers. The April retailsales report provided important confirmation that consumers were up to the task of boostingeconomic activity after a frail first quarter. Rising gas prices will lift the overall May results.BI Economics estimates total sales for the second quarter need to rise roughly 3.5-4 percentfor growth to be on track to hit the Fed's target for 2016. This appears to be within reach.— Carl Riccadonna, Bloomberg Intelligence EconomistClick here to view a live version of this chart on the Bloomberg terminal.Source: BloombergRisk aversion prevailed in markets, spurringslides in Asian and European stocks onBrexit anxiety. The pound fell with oil, whilesovereign bonds rallied.

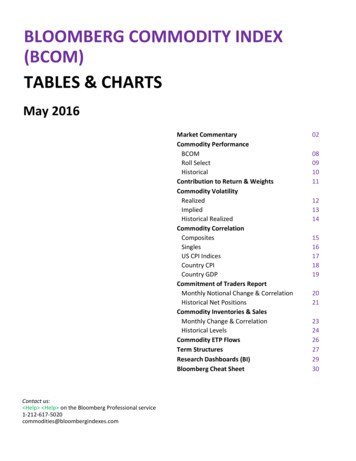

Bloomberg BriefJune 14, 2016CREDITEconomics2SUSANNE WALKER BARTON AND LIZ CAPO MCCORMICK, BLOOMBERG NEWSMost Expensive Bond Market in History Has Come Unhinged. Or Not.Today’s bond market is defying justabout every comparison known to man.Never before have traders paid somuch to own trillions of dollars in debtand gotten so little in return. JackMalvey, one of the most-respectedfigures in the bond market, went back asfar as 1871 and couldn’t find a time whenglobal yields were even close to today’slows. Bill Gross went even further,tweeting that they’re now the lowest in“500 years of recorded history.”Lackluster global growth, negativeinterest rates and extraordinary buyingfrom central banks have all keptgovernment debt in demand, even asyields on more than 8 trillion of thebonds dip below zero. But as investorsforgo any margin of safety to bid upprices higher and higher, the big worry isthat the insatiable demand has blindedthem to potential dangers that may resultin painful losses — especially as theFederal Reserve considers raising rates.“This absolutely leaves the markets alot more vulnerable,” said Torsten Slok,the chief international economist atDeutsche Bank AG.Beyond the bubble of the bond market,history offers some clues. Ten-year U.S.government notes now yield less thanstocks pay in dividends — just the thirdtime that’s happened in the past halfcentury. The last two times, Treasuriessuffered their biggest annual losses onrecord.The stakes couldn’t be higher. Averageyields for 10-year notes in the U.S.,Japan, Germany and the U.K., whichhave issued more than 25 trillion ingovernment debt, fell to 0.69 percent lastweek, data compiled by Bank of NewYork Mellon Corp. showed. That’s thelowest on record and well below the 5percent average over the course of 145years.With yields so low, bond buyers areleaving themselves no room for error. Inthe U.S., a metric known as the termpremium now stands at minus 0.47percentage point for 10-year notes. Themeasure, which the Fed uses as a tool inguiding monetary policy, reflects theextra compensation investors demand tohold longer-maturity debt instead ofsuccessive short-term securities.Global Benchmark Yields PlungeRead the full story with a live version of this chart on the Bloomberg terminal here.As its name suggests, the termpremium should normally be positive andhas been for almost all of the past 50years. But since the start of the year, thepremium has turned into a discount,suggesting that bond investors can’t seeany risks on the horizon that would pushyields higher. The same is true in Japan,Germany and the U.K., where the termpremium has gone negative asbenchmark yields in all three markets hitall-time lows last week.The “term premium should almostnever be negative, but we’re in a newnormal,” said Stanley Sun, a New Yorkbased strategist at Nomura Holdings Inc.,one of 23 dealers that trade directly withthe Fed.For the pessimists, there are plenty ofreasons to keep paying up for the safetyof government debt — even at sky-highprices.The odds of the U.S. entering arecession over the next year is now thehighest since the current expansionbegan seven years ago, according toJPMorgan Chase & Co. TheOrganisation for Economic Cooperationand Development also warned thismonth the global economy is slipping intoa self-fulfilling “low-growth trap.” What’smore, Britain’s vote on whether to leavethe European Union this month has beena major source of market jitters.“Markets are becoming increasinglyconvinced that developed nations maybe less able to create inflation even ifthey want to,” said Neela Gollapudi, thehead of portfolio management andresearch at Gentrust WealthManagement, which oversees 1 billion.Last year, inflation in developedeconomies slowed to 0.4 percent and isforecast to reach just 1 percent in 2016— half the 2 percent rate most majorcentral banks target, data compiled byBloomberg show.Yet some say that quantitative easing,or the aggressive bond-buying stimulusthat central banks in Europe and Japanare currently pursuing, is causing manydebt markets to become unmoored fromtheir fundamental value.That may help to explain the recorddemand at U.S. government debtauctions this year. With almost all thenegative-yield debt concentrated in theeuro area and Japan, investors arepouring into Treasuries, which offer someof the highest yields in the industrializedworld. Demand at sales of two-, five- andseven-year notes last month soared to alltime highs, according to data compiledby Bloomberg. Foreigners also boughtthe most Treasuries at the May auctionssince 2011, data compiled by TDSecurities showed.

June 14, 2016Bloomberg BriefEconomics3

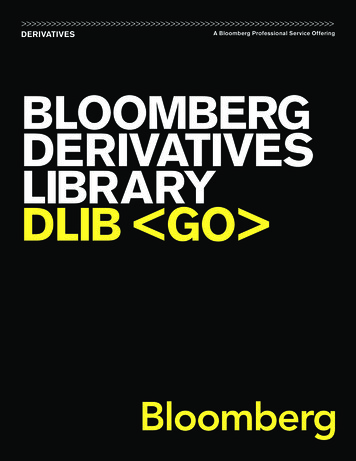

Bloomberg BriefJune 14, 2016COMMENTARYEconomics4MARK WHITEHOUSE, BLOOMBERG VIEW COLUMNISTWhat American Consumers Owe to Uncle SamU.S. consumers have long had animpressive propensity to get into debt.Lately, though, one lender has beenplaying a much bigger role in enablingthem: Uncle Sam.Total U.S. consumer credit — whichincludes credit cards, auto loans andstudent debt, but not mortgages — stoodat 3.54 trillion at the end of March,according to the latest data from theFederal Reserve. That's the most onrecord, both in dollar terms and as ashare of gross domestic product.What's really unusual, though, is thesource of the money: The federalgovernment accounted for almost 28percent of the total. That's up from lessthan 5 percent before the 2007-2009recession, thanks in large part to thegovernment's efforts to promoteeducation by making hundreds of billionsof dollars in student loans directly, ratherthan going through banks. Here's howthat looks (top chart).To some extent, the government'sgrowing role makes sense. Amid a deepeconomic slump and slow recovery, itwas best equipped to satisfy the demandfor credit among Americans looking toimprove their job prospects througheducation. Without the government'sinvolvement, consumer credit as a shareof gross domestic product would still bewell below the pre-recession level (allelse equal). Here's how that looks(bottom chart).That said, the government assist hashelped push total student debt to a record 1.3 trillion, much of which has beenspent on rising tuition costs or on coursesthat didn't do much to improve people'searning potential. Because student debtis extremely difficult to discharge throughbankruptcy, it will weigh on the borrowers— and on the U.S. economy — for manyyears to come.The Barack Obama administration hassought to ease the burden, for exampleFederal Government Share of Consumer CreditConsumer Credit as a Share of GDPwith a plan that limits payments to 10percent of a borrower's income.Ultimately, though, the government mayhave to write off a lot of the debt — attaxpayer expense.This column does not necessarily reflect theopinion of the editorial board or Bloomberg LPand its owners.

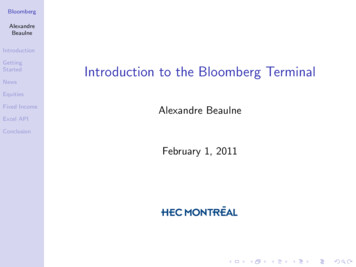

Bloomberg BriefJune 14, 2016Economics5DATA & EVENTSConsumer Inflation Expectations Little Changed: NY FedOVERNIGHTEuropeU.K. inflation unexpectedly held at 0.3percent in May as rising transport costswere offset by falls in the price of clothingand food. The rate, reported by theOffice for National Statistics today,was lower than the 0.4 percent medianestimate in a Bloomberg survey ofeconomists. Core inflation, whichexcludes volatile food and energy prices,remained at 1.2 percent.U.S. households’ expectations for inflation were little changed last month, according to aFederal Reserve Bank of New York survey. Results of the consumer survey for Mayshowed the median respondent expected inflation to be 2.7 percent three years from now.That number fell to 2.5 percent in January — marking the lowest in the survey’s three-yearhistory — before bouncing to 2.8 percent in April. The release follows preliminary results ofthe University of Michigan’s monthly consumer survey, announced Friday, which showedexpected inflation between five and 10 years ahead plunged to the lowest level on record indata to 1979.— Matthew Boesler, Bloomberg Intelligence EconomistClick here for the full story and here to view a live version of this chart on the Bloomberg azil8:00BrazilRetail Sales MoM0.50%-0.90%Retail Sales YoY-6.60%-5.70%8:00BrazilRetail Sales Broad MoM-0.90%-1.10%8:00BrazilRetail Sales Broad YoY-8.60%-7.90%8:30U.S.Import Price Index MoM0.70%0.30%8:30U.S.Import Price Index YoY-5.90%-5.70%8:30U.S.Retail Sales Advance MoM0.30%1.30%8:30CanadaTeranet/National Bank HPI MoM—1.20%8:30U.S.Retail Sales Ex Auto MoM0.40%0.80%8:30U.S.Retail Sales Ex Auto and Gas0.30%0.60%8:30CanadaTeranet/National Bank HPI YoY—8.10%8:30U.S.Retail Sales Control Group0.30%0.90%10:00U.S.Business Inventories0.20%0.40%Source: Bloomberg. Surveys updated at 5:35 a.m. New York time.Click on the highlighted releases to see the full range of economists' forecasts on the terminal.Swedish inflation slowed more thanestimated in May, adding pressure on thecentral bank to expand its unprecedentedstimulus measures at its meeting nextmonth. Consumer prices rose an annual0.6 percent in May, compared with 0.8percent the prior month, StatisticsSweden said in a statement today. TheRiksbank and analysts surveyed byBloomberg estimated a 0.7 percent gain.Adjusted for mortgage costs, inflationslowed to an annual 1.1 percent, belowthe 1.2 percent estimate.AsiaThe yuan drew closer to a five-yearlow as concern over China’s economicslowdown and Britain’s vote on EuropeanUnion membership spurred selling inriskier assets. The Chinese currencytraded within 0.1 percent of its low set inJanuary after slumping the most in amonth yesterday. The exchange rate fell0.11 percent to 6.5917 a dollar as of 4:53p.m. today in Hong Kong, and dropped toits lowest level since 2014 versus tradingpeers including the yen and the euro.

June 14, 2016Bloomberg BriefEconomics6MARKET INDICATORSSource: Bloomberg. Updated 5:35 a.m. New York time.

June 14, 2016Bloomberg BriefEconomics7

Bloomberg BriefJune 14, 2016Economics8SURVEILLANCE WITH KEENE & MCKEEUBS Investment Bank Senior U.S. EconomistDrew Matus, speaks with Bloomberg's MichaelMcKee and Tom Keene about corporate debt,global monetary policy and market distortion.Q: Do we get back to an okay nominalGDP with the pressures a bit off M&A?A: I think you do get back to a betternominal GDP. I mean this year isprobably going to be a somewhat softyear because inflation hasn't started tobuild up yet and real growth is somewhattepid. Next year though real growth kindof hangs in and inflation begins to pickup. And it's part of the reason why eventhough our real numbers move up verymodestly, we still have the Fedcontinuing a rate hike cycle into 2017because the nominal numbers startlooking so much better because theinflation figures are moving higher.Q: Do we see companies start to beable to make more money at the topline? Do sales improve enough do youthink coming up over the comingyear? I saw a note that said, yes, thatcould happen. But at the same time,what you're seeing now is companiesare going to have to pay up for laborso nobody really gains.A: If companies are paying up for labor,that's fine as long as they're getting someproductivity out of it. And if you ask mewhat the number one question in the U.S. economy is, which will tell you wheremarkets are going and where everythingis going to head, if you told me what wasgoing to happen to productivity, I'd havea much more informed view of the worldin terms of how everything else will playout.And unfortunately the productivitynumbers are a completely open questionand no matter how you try to look atthem, you can pretty much come up witha model that gives you any answer youwant. So that's really not helpful from aneconomist's standpoint. And so as I said,that is the focus. If I needed just onenumber, that would be the number that Iwould need.Q: It seems like companies can usedebt whether or not it's a good idea. Isthis a sign that markets are distorted?A: Low rates have a lot of interestingeffects on people's perceptions. The flipside of it is are low rates and theperception of low rates going forwardwould mean that companies never haveto make a decision, right? You canalways make the decision next week ornext month because the cost of waitingfor more information is zero. So it can cutboth ways. And I think that's one of thethings the Fed maybe missed when ittook rates to zero was that lowering ratesdoesn't always result in the positive kindof outcomes that the Fed would hopethat they would.Q: This is a week where we're going tosee something like five central banksmeet and nothing happening?A: The problem with central banks —and I think this is globally — is thatthey've all become so fixated on financialmarkets. Financial markets are supposedto respond to central banks, not the otherway around. And when you have the cartleading the horse instead of the otherway around, you typically can't steer verywell. And I think that's the danger of theFed moving into where every time theequity market has had the hiccups, theFed pulls back. Every time there's asingle data point that doesn't go theirway, they pull back. You cannot be datapoint dependent. You can be datadependent.Q: How much does the extraordinarypolicy that we're in now continue todistort markets and pricing?A: I think it makes a significantdifference. I think it corrupts consumerbehavior. I think what you see is there isa much higher savings rate than thereshould be. The logical reason for that isbecause a lot of the workforce isapproaching retirement age and lookingout into a low rate environment inperpetuity. And that means that if theythought they had enough money savedfor retirement, they were wrong. Andnow, they're trying to play catchup in thelast few working years of their life.This interview has been edited and condensed.Bloomberg Brief: EconomicsBloomberg Brief Managing EditorJennifer Rossajrossa@bloomberg.netChief U.S. EconomistCarl Riccadonnacriccadonna3@bloomberg.netEconomics EditorsBen Barisbbaris1@bloomberg.netU.S. EconomistsRichard Yamaroneryamarone@bloomberg.netJames Crombiejcrombie8@bloomberg.netYelena Shulyatyevayshulyatyev2@bloomberg.netGlobal Director EconomicResearch & Chief EconomistMichael McDonoughmmcdonough10@bloomberg.netReprints & PermissionsLori Hustedlori.husted@theygsgroup.com 1-717-505-9701 x2204Marketing & Partnership DirectorJohnna Ayresjayres1@bloomberg.net 1-212-617-1833AdvertisingChristopher Konowitzckonowitz@bloomberg.net 1-212-617-4694Economics Terminal SalesMatthew Traummtraum@bloomberg.net 1-212-617-4671Interested in learning more aboutthe Bloomberg terminal? Request afree demo here. 2016 Bloomberg LP.All rights reserved. This newsletterand its contents may not beforwarded or redistributed withoutthe prior consent of Bloomberg.Please contact our reprints grouplisted left for more information.

head of portfolio management and research at Gentrust Wealth Management, which oversees 1 billion. Last year, inflation in developed economies slowed to 0.4 percent and is forecast to reach just 1 percent in 2016 — half the 2 percent rate most major central banks target, data compiled