Transcription

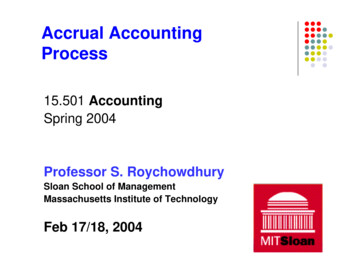

Accrual AccountingProcess15.501 AccountingSpring 2004Professor S. RoychowdhurySloan School of ManagementMassachusetts Institute of TechnologyFeb 17/18, 20041

An accountant’s functions include Classifying and summarizing, made easier by therepetitive nature of business transactionsAll repetitive transactions of the same nature arerecorded and summarized in one account An account is a storage unit used to classify andsummarize money measurements of businessactivity of a similar nature Each account has a title2

T-Account Has two sides Debit means Left Credit means Right Created for each type of AssetLiabilityStockholders’ equity3

Recording changes in Assets andLiabilities Increases in assets are recorded on the left side of the TaccountDecreases are recorded on the right side of the T-account Reverse for liabilities and stockholders’ equity Assets Liabilities Stockholders’ equity Assets are on the left side of the Balance Sheet Equation Liabilities and owners’ equity are on the right side4

How does a T-account look like? Like a Capital “T”5

Summary of T-account RulesAssets (cash, receivables, equipment)IncreasesDecreasesLiabilities (loans payable)DecreasesIncreasesOwners’ equity (contributed capital, retained earnings)DecreasesIncreases6

About T-Accounts What is one major objective of financial statements? To provide information to “users” regarding the financialperformance of a businessWhich T-account(s) includes the accountant’s estimate offinancial performance over a given accounting period? Retained earnings (includes current period income)Which financial statement provides the details of the financialperformance over a given accounting period? Income statementHow do we construct an income statement from the T-accountfor retained earnings? Not very easily! But we will try.7

Components of stockholders’ equityCommon StockAdditionalCapitalRetained EarningsExpensesDividendsRevenue8

Why record expenses and revenuesseparately in various T-accounts?Retained EarningsRent exp.800 1,000Salaries650 1,100Interest exp. 450 3,000Salaries1,000 200Rent exp.400 4,500Dividends 2,000Interest exp. 350Sales revenueInterest IncomeSales RevenueInterest IncomeSales RevenueSales Revenue (1,000 3,000 4,500)Interest Income (1,100 200)Rent expense (800 400)Salaries expense (650 1,000)Interest expense (450 350)Net Income8,5001,300(1,200)(1,650)(800)6,1509

Why record expenses and revenuesseparately in various T-accounts?Retained EarningsRent exp.800Salaries650Interest exp. 450Salaries1,000Rent exp.400Dividends 2,000Interest exp. 3501,0001,1003,0002004,500Interest Expense450350Dividends2,000Sales revenueInterest IncomeSales RevenueInterest IncomeSales RevenueSales Revenue1,0003,0004,500Interest Revenue1,100200Rent Expense800400Salaries Expense6501,00010

Why record expenses and revenuesseparately in various T-accounts?Sales RevenueInterest Revenue1,0003,0004,5008,5001,1002001,300Interest Expense450350800Rent Expense8004001,200Dividends2,000Salaries Expense6501,0001,65011

Why record expenses and revenuesseparately in various T-accounts?Sales Revenue1,0008,5003,0004,5008,500Retained EarningsRent Exp.1,200 8,500 Sales RevenueSalaries Exp. 1,650 1,300 Interest RevenueInterest Exp. 800Dividends2,0004,150Interest Revenue1,1001,3002001,300Rent ExpenseInterest ,200Salaries Expense6501,0001,6501,65012

Why record expenses and revenuesseparately? A Summary Revenues, expenses and dividends are temporary TaccountsInformation on changes in retained earnings pertaining to asingle accounting period is collected in these temporaryaccountsAt the end of the accounting period, balances in these Taccounts are transferred to Retained EarningsThe temporary accounts are set to zero at the end of anaccounting period in order to start collecting information forthe next periodRevenues, expenses and dividend accounts are flowaccountsRetained earnings is a stock accountIn fact, all balance sheet accounts are stock accounts13

Recording expenses: A Summary Expenses decrease retained earnings. Decreases in retained earnings are recordedon the left side Expenses are recorded on the left side14

Recording Revenues: A Summary Revenues increase retained earnings. Increases in retained earnings are recordedon the right side (Increase in) revenues are recorded on theright side Decrease in revenues are recorded on the leftside15

Recording Dividends: A Summary Dividends decrease retained earnings Therefore, treated similarly to expenses, butdividends is not an expense Dividends are recorded on the left side16

Expenses and Revenues: Debitsand Credits Retained earnings (in general) has a credit balance. Revenues have credit balance (before they are closedout) because they increase retained earnings Expenses and dividends have debit balance (beforethey are closed out) because they decrease retained earnings Yes, when cumulative earnings are less than cumulativedividends Can retained earnings have a debit balance?17

The Ledger Accounts are collectively referred to as the ledger Types of accounts Balance Sheet accounts or real accounts orpermanent accountsIncome statement accounts or nominalaccounts or temporary accounts, i.e., revenue, expenses, and dividends - all theseare subdivisions of retained earnings18

The Recording Process Journal entries Adjusting entries Posting to T-accounts Trial Balance Financial statement preparation19

The Journal Journal contains a chronological record of thetransactions of a business20

1. Joe’s Landscaping ServiceJoe contributes 10,000 in cash Assets Cash 10,000 Liabilities Owners’ EquityContributed Capital 10,000Journal EntryDrCashCrContributed capital10,00010,00021

2. The company borrows 3,000 fromthe bank Assets CashLoans Payable 3,000 3,000 Liabilities Owners’ EquityJournal EntryDrCashCrLoans payable3,0003,00022

3. Company purchases equipment for 5,000 cash Assets Cash - 5,000Dr L OEEquipment 5,000Journal EntryEquipmentCrCash5,0005,00023

4. Company performs service for 12,000. Thecustomer pays 8,000 in cash and promises topay the balance at a later date. Assets Cash L Owners’ EquityReceivables 8,000Retained Earnings 4,000 12,000Journal EntryDrDrCashAccounts receivableCrRetained earnings (Revenue)8,0004,00012,00024

5. Company pays 9,000 for expenses (wages,interest, and maintenance) Assets Cash - 9,000 Liabilities Owners’ EquityRetained EarningsJournal EntryDr Retained Earnings (Expenses)CrCash- 9,0009,0009,00025

6. Company pays a dividend of 1,000 Assets Cash - 1,000Dr Liabilities Owners’ EquityRetained Earnings- 1,000Journal EntryRetained Earnings (Dividends)CrCash1,0001,00026

Posting to T-accountsCASHDr10,000 (1)03,000 (2)08,000 (4)06,0005,000 (3)9,000 (5)1,000 (6)Cr27

Summary T-accounts Debit is LeftCredit is RightIncreases in Assets – DebitsIncreases in liabilities – CreditsIncreases in shareholders’ equity – CreditsExpenses are DebitsRevenues are CreditsUse balances from T-accounts to preparefinancial statements at the end of a fiscal period28

sAdjusting entries: Recall four waysthat recognition and cash do notcoincidePay CashRecognize ExpenseTimeBalance Sheet DateRecognize ExpensePay CashTimeBalance Sheet Date29

sAdjusting entries: Recall four waysthat recognition and cash do notcoincideReceive CashRecognize RevenueTimeBalance Sheet DateRecognize RevenueReceive CashTimeBalance Sheet Date30

Accruals (Accrue Today, CashTomorrow) Accrued Wages Employees of Taylor Motor are paid at the end of eachweek.Payroll per day: 2,000Weekly payroll: 10,000 (five working days)Taylor’s year ends on December 31.Assume December 31, 2003 falls on a Tuesday On December 31, 2003 Taylor Motor has incurred wage expense for two daysBut will not pay it in cash until Friday, January 3, 2004.31

Accruals (Accrue Today, CashTomorrow) Periodic adjustment on December 31 Assets Liabilities Owners’ Equity Wages Payable Retained Earnings 4,000-4,000 Dr Wage Expense (-RE)4,000 Cr Wages Payable ( L)4,000 Effect of omitting this journal entry? Liabilities are understated by 4,000Retained earnings & Net income overstated by 4,00032

Accruals (Accrue Today, CashTomorrow) What would you see on the balance sheet as of12/31? Wages Payable 4,000 under Liabilities What would you see on the income statement forthe year ended 12/31? Wage Expense of 520,00052 Weeks x 10,000 per week Wage expense would have been 4,000 less.Expense would have been understatedNet income overstated Without the adjusting entry33

Accruals (Accrue Today, CashTomorrow) 10,000 paid on Jan. 3 of 2004. Assets Liabilities Owners’ Equity CashWages Payable Retained Earnings -10,000-4,000-6,000 Dr Wage Expense (-RE)6,000 Dr Wages Payable (-L)4,000 Cr Cash (-A)10,000 What would be the balance in the T-account forWage Expense on January 3rd? 6,00034

Accruals (Accrue Today, CashTomorrow) Consider the 10,000 paid to the employees. Where and How would it show up in thefinancial statements?Period 1Cash Flow StatementOperating cash flowIncome StatementWage expense (-RE)Period 2-10,000-4,000-6,00035

Cost Expirations (CashYesterday, Accrual Today) Supplies Inventory During 1994 Deere and Company purchases (for cash)supplies in the form of spare parts to support themanufacture of farm machinery at a total cost of 700.The company began the year with 500 in the suppliesaccount. Assets Cash -700 Liabilities OESupplies 70036

Cost Expirations (CashYesterday, Accrual Today) On December 31, a count reveals that supplies in the amount of 300 remain on hand.Supplies Used Beg. Inv. Purchases - Ending Inventory 500 700 - 300 900 Assets L Supplies -900 Dr Supplies Expense (-RE) Cr Supplies Inventory (-A)Owners’ EquityRetained Earnings-90090090037

Cost Expirations (CashYesterday, Accrual Today)Supplies AccountBeg balPurchasesEnding Inv 500900Supplies expense700300Supplies expense of 900 is the adjusting entry and thecorresponding debit is to Retained Earnings (i.e., expenseon the income statement that affects retained earnings).The Ending Inventory of 300 appears on the balancesheet (and it serves as the ending inventory for the currentfiscal period and beginning inventory for the following fiscalperiod).38

Cost Expirations (CashYesterday, Accrual Today) What shows up in the cash flow statement? The cash paid during the year for purchase of suppliesOperating outflow 700 The cost of supplies consumed during the yearSupplies expense 900 Ending balance in Supplies of 300 What shows up in the income statement? What shows up in the balance sheet?39

Cost Expirations (CashYesterday, Accrual Today) Pre-received revenues Unearned revenueFees received in advanceCustomer advancesSubscription received in advance, etc. Time Warner receives 5,000 during 1994 formagazine subscriptions to be fulfilled during 1994and 1995. Assume that as of the end of 1994 Timehad fulfilled 60% of the subscriptions.40

Cost Expirations (CashYesterday, Accrual Today) 5,000 received during 1994 Assets Liabilities OE CashUnearned Revenue 5,000 5,000 Dr Cash ( A)5,000 Cr Unearned Revenue ( L)5,000 What happens to this liability at the end of 1994? Decreases by 60% because Time Warner deliversmagazines in 1994.41

Cost Expirations (CashYesterday, Accrual Today) Assets Liabilities Owners’ Equity Unearned Revenue Retained Earnings -3,000 3,000 Dr Unearned Revenue (-L)3,000 Cr Subscription Revenue ( RE)3,000 Effect of omitting this entry? Liabilities are overstated by 3,000Retained earnings (income) understated by 3,00042

Cost Expirations (CashYesterday, Accrual Today) Effect on financial statements? 19941995 Operating cash inflow ( ) 5,000 Subscription revenue ( RE) 3,000 2,000 What do you see in the balance sheet as of12/31/94? Liabilities: Unearned Revenue 2,000Represents the obligation for unfulfilled journalsubscriptions.43

Summary Accrual accounting can be confusing! Understand the logic behind it and it will beclear.44

Accrual Accounting Process 15.501 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management . Supplies expense of 900 is the adjusting entry and the corresponding debit is to Retained Earnings (i.e., expense