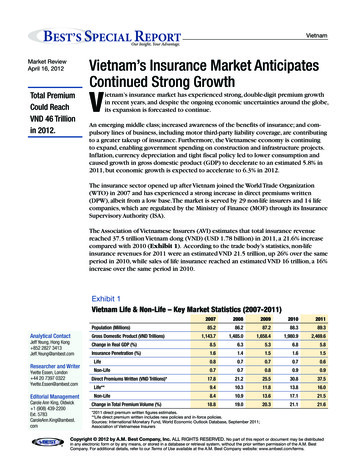

Transcription

Savings InSight Your Automated Retirement Builder

Savings InSight ,Your Automated Retirement BuilderWe live in a high-tech, multi-media culture designed for automation andinstant gratification. So how does that affect employees planning for retirement?Simple: many no longer do. They’re too busy to focus on the long term, they don’thave the comfort level or insight to make investment decisions, and they struggleto stay on track to reach their financial goals. If you offer a program that educatesthem, helps them save for retirement, and manages their income after retirement,you’d be giving them a powerful retirement readiness tool they won’t want togive up. What’s more, you’ll improve employee engagement levels and boost yourunderstanding of employee behaviors and outcomes.

OPTIONALIMAGE FPOSavings InSight, part of our retirementplan services, is our innovative newsavings program, with periodic monitoringfunctions and both pre- and postretirement features. Savings InSighthelps your employees better prepare forretirement. It aligns with your currentplan offerings and can automatically:enroll individuals in their 401(k) plan,set a reasonable retirement target,determine a contribution scheduledesigned to deliver on the target, investthe assets in default Target, Lifestyle,or Managed Accounts, review actualresults versus targeted results and makeany needed adjustments, and set up apayout schedule for retirement to helpthe savings last. Plus, Savings InSightautomatically projects Social Securitybenefits and allows your participants toenter in any additional savings and priorretirement plan balances.Advantages for employees: Simplifies the puzzle sothey can finally make wellinformed decisions for acomfortable retirement Saves time/reduces anxiety Provides a calculator/modeling tool to bettercustomize results Spurs individualinvolvement in retirementplanningKey Features Full automation is available – Thedaunting task of planning for a secureretirement is now made easy. Forperhaps the first time ever, employeeswill have a retirement program theycan understand, know where theyare against the target they helpeddetermine, and visualize how they willget there. Note: They can always opt outfor the “traditional” 401(k) approach,making all of their own decisions. Monitoring – Every year the programwill compare actual savings balancesagainst the targeted balances, and makeadjustments, if and when needed. Thisfeature keeps them on the right course. Post-retirement management –The program can pay a “monthlypaycheck” to retirees to help makethe savings last over the designatedretirement period. The amount ofthe payment is also monitored andautomatically adjusted, as needed. Flexibility – We realize that “onesize doesn’t fit all” when it comesto retirement plans. Not only doesSavings InSight allow the plan sponsorto customize investment return andsavings assumptions, it also has theability to identify different targets,assumptions, and participation modelsfor different employee groups (e.g.union populations) or demographicgroupings. Savings InSight can alsoincorporate your other retirementprograms (pension, non-qualifiedplans) to provide employees with afull retirement picture. The level ofautomation is also up to the sponsor– Savings InSight can be implementedwith an “opt-in” or “opt-out” approach. An actuarial perspective – We’vebeen a leading actuarial firm foralmost 100 years, and we’ve put thatexperience to use here with SavingsInSight. Our actuarial team will reviewall assumptions to ensure the modelingis appropriate for your plan. What’smore, the annual report that displaysthe impact Savings InSight is having onyour participants’ retirement readinessis reviewed and evaluated by a memberof our actuarial team.Savings InSight works with any definedcontribution plan design, providing avaluable benefit in a post-defined benefitworld. Our program simplifies the retirementmystique, leading to higher participationand savings, better investment results,and more transparent fees.Advantages for employers: Works for any type/designof DC plan Influences retirementpatterns to align withbusiness objectives Supports every stage withfull communications Provides information onworkforce retirementbehaviors in annual reports2

Savings InSight , Your Automated Retirement BuilderSavings Insight makes saving for retirement as easy as 1-2-3!StepWhat’s in it for you?Why is it different?1. We get you started. Automatic enrollment in your 401(k) planwhen you become eligible. Automatic contribution at the percentage ofpay that is “right” for you. Automatic investment of your contributionsunless you select your own investment fund.We automatically calculate the contributionpercentage that is right for you based on yoursalary, age and existing savings. You receive a personalized annual report ofwhere you are, where you need to be, andwhat it will take to get you there. If needed, an automatic adjustment is madeto your contribution percentage, based onyour goal.We provide you with a snapshot of yourprogress vs. your goal and automaticallyincrease your contribution if you fall short. Youcan also look at what happens to your savingsif you earn higher or lower returns on yourinvestments.2. We keep you on track.You don’t have to spend hours usingcomplicated assumptions to make uncertainprojections about your future income and howmuch you’ll need to save to maintain yourstandard of living.You don’t have to agonize about monitoringyour investment returns and rely solely on yourinvestment strategy to reach your goal.3. We pay you back.3 Retirement income payments work just likedirect deposits of your paycheck did. Each year, your retirement income amountwill be analyzed acocrding to your specificsituation and adjusted if needed. We’ll even set some of your savings aside inreserve, to help keep your payments steadythroughout your retirement. You can alsouse the reserve as a cushion for unexpectedexpenses.We send you a monthly “paycheck”, based onyour life expectancy. We adjust it automaticallyevery year, if needed, depending on how muchyou’ve earned on your savings, the paymentsyou’ve received and your year-end balance.You don’t have to continually worry aboutwithdrawing too much from your savings. And,you don’t have to worry about paying hiddenexpenses found in many annuities, which caneat into your hard-earned savings.

How does it compare?Here’s how Savings InSight compares to the retirement readiness capabilities offered by a composite of other solutions in themarketplace.FeatureSavings InSightCompetitor SolutionsParticipant EngagementProactively compels all employees to participateat appropriate levels and changes savings levelautomatically, as needed. Annual retirementreadiness report distributed to all employees.Caters primarily to participants who like todo their own research, especially the moresavvy investors or those closer to retirement,and typically requires the participant to takeaction. Annual reports are distributed to allemployees.Ease Of UseTakes the next step of making the “smart”deferral that sets the employee on the correctpath to having a financially secure retirement;and requires the employee to opt out.Provides useful information, but employeestypically must make decisions to achievetarget outcomes.CostFees not tied to assets, low flat dollar amounts;fees do not increase as account balances grow.Many are tied to fees based on assets whichcan lead to high costs as balances grow.FlexibilityEmployer can set targets and provide inputon a myriad of assumptions. The result is aprogram that matches the characteristics andexpectations of your plan.Little flexibility in setting replacement ratios,inflation, and Social Security assumptions.Periodic AdjustmentsAnnual true-up with automatic adjustmentskeeps employees on track.Quarterly updates and recommendations tohelp participants keep on track, assets can bemoved automatically for those in managedaccount programs.PersonalizationAbility to take into account all existingretirement assets and personalize goals to refinea participant’s results.Access to personal support, robust tools for thesophisticated saver and investor.Retirement AdequacyKey focus is on helping employees save enoughfor retirement; employees always know wherethey are, where they are going, and how to getthere.Key focus is typically on investmentmanagement, but provides information onhow much is needed for retirement and actionsrequired to achieve goals.InvestmentsAssumes the use of Target Funds, BalancedFunds, Life Cycle Funds, or Managed Accountsas default investment options; offers theparticipant and the plan sponsor maximumflexibility and leverages the work done by thesponsor to select and monitor a QDIA.Sophisticated investment advice features,automatic rebalancing, adjustments to reflectrisk levels.Investment AdviceNot intended to be provided, but works inconjunction with existing funds and investmentadvice collateral.Typically available both online and viarepresentative. Managed accounts can beavailable at additional asset based fees to theparticipant.Retirement PayoutsSets up monthly payments, much like apaycheck, and adjusts them annually dependingon the actual account balance. Includes asmoothing mechanism. Lifetime income optionsare available as well.Few providers offer an income stream inretirement, and asset-based fees apply tothose who choose to use the draw-downfeature. Annuities may be an option.4

Savings InSight , Your Automated Retirement BuilderCommonly Asked QuestionsQ. How does Savings InSight interactwith your defined contribution (DC)recordkeeper?A. Savings InSight complements your DCrecordkeeper. That is, the recordkeeperwill continue to be responsible forall tasks it has currently. SavingsInSight requires a small number ofdata elements on an annual basisfor current actives, and throughoutthe year for any new or changedparticipants. The implementation teamwill work with HR and payroll to setup the process to transmit this datasecurely on a standard/automatedbasis. If it is deemed that the DCrecordkeeper is the best and mostefficient resource for this transmission,we will accommodate that method.For retirees, the DC recordkeeper willneed to be able to accommodate thedistribution of the monthly retireepaychecks, using standard installmentpayment functionality supported bythe vast majority of recordkeepers.The Savings InSight Web experience isan additional way for participants tomake contribution deferral elections,but will not eliminate any of the currentrecordkeeper capabilities.Q. How are investments handled in theSavings InSight approach?A. Savings InSight takes a differentapproach than most other solutionswith respect to retirement readiness. Itfocuses primarily on helping participantssave and defer appropriate amounts.For investments, the Savings InSightapproach works best with plans that offera qualified default investment alternative(QDIA) with automatic investmentallocation and rebalancing features.Target Date Funds, Life Cycle Funds,or Managed Accounts are examplesof investment options that work best.Plan Sponsors spend a great deal oftime and effort to ensure their QDIA isan appropriate investment vehicle; weleverage that work with Savings InSight.5Why Savings InSight?It can completely automatethe steps needed totransform your savings planto a true retirement program: Automatic enrollment inthe plan Automatic retirementtarget and contributionschedule Automatic ongoingadjustments Automatic payoutschedule at retirementThe participant always maintainsflexibility to select the default option ortake complete control of the investments.Q. What if we already offer otherretirement readiness tools or education,including investment advice andmanaged account programs? Is SavingsInSight still a viable alternative?A. Absolutely. The answer dependson how effective these tools are withrespect to helping your employeesprepare for a secure retirement. Whatpercentage of your population isaccessing the tools/materials? Howmany are actually saving enough toprepare adequately for retirement?If you’ve had these tools in place fora while, but you are not seeing thedesired outcomes, then Savings InSightis an ideal option. It can be offered inaddition to existing materials and tools.Savings InSight provides a goodalternative for those employees whoare not capitalizing on the educationand tools that are currently available.Compared to the other alternatives, itis low cost and takes minimal time andeffort to get good results.Q. Why are updates done annually?What information will employees seemore frequently?A. Saving for retirement is a career-longeffort. Reviewing results and makingadjustments annually allows for anappropriate time period to make changesand keep participants on the right tracktoward a secure retirement. For thoserecordkeepers that support single-signon with Savings InSight, participants willsee data dynamically updated with eachlogin. Employees will continue to haveaccess to account balance informationand investment performance, as well ashave the ability to make contributionor allocation changes or apply for loansthrough the existing recordkeeper andconsistent with existing plan provisions.These services are not impacted by theaddition of the Savings InSight application.Q. Can the Savings InSight solutionwork for all employees?A. One of the key positives of SavingsInSight is the simplicity of the conceptand the approach. The goal of SavingsInSight is to increase the number ofpeople who will reach their retirementgoals. For those with more complexsituations, the Savings InSight solutionincludes access to a state-of-the-artretirement modeling tool, which offerspowerful and educational savingsguidance, provides easy “one click”action elections, and allows participantsto further personalize their data andgoals. The Web experience also helpsguide those participants with complexpersonal situations in using themodeling tool. It’s important to notethat a key objective of Savings InSightis to lead people to a place where theycan be more comfortable during theirretirement years. It is not a guaranteeof lifetime retirement income securitybased on an exact calculation. It’san effective option that will appealto many. It also complements otherretirement readiness solutions thatmay already be available, utilized, andeffective for some employees.

“For many people, being askedto solve their own retirementsaving problems is like beingasked to build their own cars.”Richard H. Thaler, “Shifting OurRetirement Savings Into Automatic,”New York Times, April 6, 2013.Q. How does Savings InSight affect thefiduciary responsibilities of the plansponsor?A. Savings InSight, does not— and isnot meant to — provide investmentadvice, and therefore does not take onany fiduciary responsibility from the plansponsor. It does, however, strengthenthe plan sponsor’s role as a fiduciary byproviding additional information andsupport to help participants prepare fora secure retirement.Q. I already offer planning toolsthrough my recordkeeper; won’t SavingsInSight conflict with those offerings?A. While many recordkeepers and plansponsors offer account balance andprojection tools, Savings InSight takesinto account Social Security and otherretirement income sources to provideyour employees with a clear path toretirement security. The combination ofrobust on-line tools and an annual, easyto-understand retirement update goesabove and beyond the services offeredby recordkeepers. Savings InSightincludes a complete communicationprogram that will clearly outline how touse the tools and how they coordinatewith existing recordkeeper resources. 2016 Xerox Corporation. All rights reserved. Xerox and Xerox and Design are trademarks of Xerox Corporation in the United Statesand/or other countries. Savings InSight is a trademark of Buck Consultants, LLC in the United States and/or other countries. BR13722Learn MoreTo speak to one of our Wealth Practiceconsultants, contact us at1.866.355.6647 orhrconsulting@xerox.comXerox HR Consulting is delivered throughBuck Consultants at Xerox.www.xerox.com/hrconsulting6

The Savings InSight Web experience is an additional way for participants to make contribution deferr