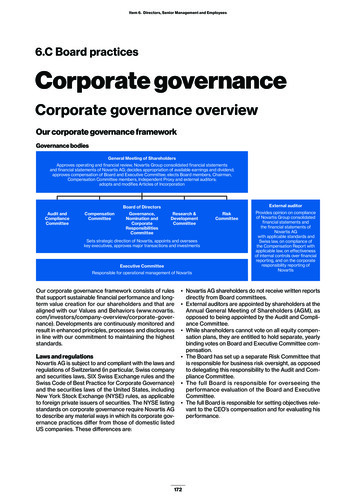

Transcription

Novartis Investor RelationsNovartis Strategyand Growth StoryVas Narasimhan, CEOJ.P. Morgan Healthcare ConferenceJanuary 10, 2022

Novartis presents an attractive profile for investors12345ClearstrategyAttractivegrowth profileStrong mid/latestage portfolioPlatformleadershipBalanced capitalallocationDeliveringon strategyas a focusedmedicinescompanyConfident in 4% sales CAGR (2020to 2026) and abovepeer medianbeyond 2026Breadth and depth,20 assets with USD 1bn potential, fuelfurther growth to2030 and beyondContinue todevelop leadershipacross technologyplatformsAims to combineinvesting in corebusiness and returningexcess capital toshareholders2J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS

Our strategyFocused medicines company powered by technology leadership in R&D,world-class commercialization, global access and data scienceWhere to play our focusHow to win our five prioritiesOur aspirationInnovationpowerStrengthen our coretherapeutic areasAdvance our leadingtechnology platformsEmbrace operationalexcellence every dayUnleash the powerof our peopleAccelerateour 4 prioritygeographiesTransformSandozDeliver transformativeinnovationGo big on dataand digitalBuild trustwith society1. Return on invested capital.3J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONSReturnsTop 3 innovatorHigh 30s IM margin,attractive ROIC1GrowthESGConsistent abovepeer medianaverage growthGlobal leaderin materialESG factors

We are delivering consistent top-line growth with margin expansionDiversifiedHealthcare GroupFocusedMedicines Company1996 - 20142015 - 2021Actions 2015 – 2020Actions 2021 Exit of Animal Health, Vaccines, Consumer Health Strategic Review of Sandoz to maximize shareholder value Alcon spin value creating, tax neutral, largest in EU market history Sale of Roche stake single bilateral transaction, USD 21bn, no tax leakage, IRR of 10.2% in USD Opportunistic bolt-on acquisitionsConsistent strong operating performance (Innovative Medicines)SalesCore OpIncInnovative MedicinesUSD bn, % CAGR ccUSD bn, % CAGR ccCore margin (%), growth bps cc 7%25.927.8 270bps 14%28.88.437.136.331.39.5 90bps10.411.6 220bps34.332.49M 2018 9M 2019 9M 2020 9M 202149M 2018 9M 2019 9M 2020 9M 2021J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS9M 20189M 20199M 20209M 2021

We remain disciplined and shareholder-focused in our capitalallocationInvesting in the businessReturn to shareholdersInvestments in organic businessDisciplined R&D investment into core therapeuticareas, investing 19%-20% of IM sales1 deliveringavg 2-3 NMEs p.a. between 2018 and 2021Value-creating bolt-ons20183 USD 30bn M&A bolt-ons since(10 deals, mean of USD 2bn)1. Core R&D as a % of 3rd party sales based on 2020 IM actuals.3. Until Q4 2021.5Growing annual dividend in CHFCapitalallocationprioritiesCommitted to maintain strong and growingdividend (in CHF), increased by CAGR 7.8%in CHF and 9.8% in USD between 1996-20202Share buybacksAnnounced share buybackof up to USD 15bn2. Reflecting dividend payments up to and including the business year 2020 (paid out in March 2021), converted at historic exchange rates at the respective dividend payment dates as per Bloomberg.J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS

We have strong positions in five therapeutic areas and newtechnology platforms, with a diversified geographic presence5CRM, IHD, NS, ONC,14HEM1Strong positions intechnology platformsTPDAdvance our broadportfolio of NMEsIn-marketblockbuster assets2CELLTHERAPYLead in next generationof CAR-Ts20 Potential bn USD pipelineassets with approval by 2026GENETHERAPYAdvance next waveof assets8%Limited binary risk ona single product2Opportunistic in others:Ophthalmology & RespiratoryGeographically diversified3Company 15Company 14Company 13Company 12Company 11Company 10Company 9Company 8Company 7Company 6Company 5Company 4Company 3Company 2Company 1Other companiesIn-market and pipelinedepth in 5 therapeutic areasNovartisRLTExpand acrossadditional solid tumorsUS Low exposure to US pricing reforms4EU Maintain sales leadership53%Key growth drivers andlaunches as % of IM sales,growing 26% in Q3 2021xRNAFully build upsiRNA capabilitiesChina Sales on track to double by 2024USAsia, Africa, AustralasiaEUCanada & Latin Americaex-US1. Cardio-Renal, Immunology, Neuroscience, Oncology, Hematology. 2. Based on 2020 Group sales actuals.3. Source IQVIA Analytics Link (MIDAS database), sales numbers are estimated bottom up based on average wholesaler price and volume, and thereforedeviates from net sales reported by companies in their annual reports. Includes branded and generics drugs as well as vaccine s but no OTC.4. Relative to peers.TPD: Targeted Protein Degradation, RLT: Radioligand Therapy.6J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS

Off this strong base, we are committed to driving consistent growthto 2030 and beyondIM sales evolutionIllustrative, USD billion, % CAGR cc12020-2026 4%Focused resources on key growthbrands and launches, upscaling nextgeneration engagement models353839212Double-down on internal pipelineassets to unlock their full potentialand add complementary BD&L3320182019202020262030 20301. 6% in USD7J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS2026-2030 peer median 2030 peer medianFocused investments in technologyplatforms while staying at the forefront ofinnovation in small and large molecules

1Novartis Growth Story2020 - 2026

Confident in delivering 4% sales CAGR 2020 - 2026 5% CAGR ccif Entresto LoEbeyond 20262Illustrative Group salesUSD billion, cc 4% CAGR ccWithout any pipeline contribution 1.5% CAGR rEntresto2020Future Gx impactup to n-market growthdrivers / Base businessLeqvioLu-PSMA-617ScemblixOther pipelineIM Division pipelineprobabilizedIM Core Margin35%Excludes potential impact from US healthcare reform. Compared to R&D Day 2021, removed Ligelizumab in CSU.1. Estimated based on relevant patents; further extensions possible. Additional products include Promacta, Q-Family and Votrient. 2. For internal forecasting purposes we do not expect Gx in US at least until 2025.9J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS2026IM Core MarginHigh 30s

Six in market growth drivers with multi-billion USD sales potentialUSD bnUSD bnUSD bnUSD bnUSD bnUSD bnQ3 salesannualized15.03.71.50.90.4nmQ3 Growth 22% 44% 28% 27%nmnmUSD bnUSD bnUSD bnUSD bnUSD bnUSD bn 7.0 onCAGR2020-2026Lowdouble-digitDoubledigit until LoELow tomid teensLow 30s4nmnmUS LoE22029 2025-20362031 2031 2031 2036 Peak salesUSD, all growth rates in constant currencies (cc). Excludes potential impact from US HC reform.1. Reported Q3 net sales annualized.2. Estimated based on relevant patents; further extensions possible.10J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS3. Including Zolgensma IT.4. Including Kisqali adjuvant.

Leqvio : US launch underwayEffective and sustained LDL-Creduction1 with twice a year maintenancedose administered by HCPBroad label covering 16m US ASCVDpatients not at LDL-C goalGo-to-market model designed toovercome clinical barriers and addressaccess, adherence and affordabilitySales, reimbursement and medical teamswith deep experience in the UScardiovascular marketLDL-C – Low Density Lipoprotein Cholesterol11ASCVD – Atherosclerotic Cardiovascular DiseaseAIC – Alternative Injection CenterJ.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONSFDA approvedRobust network of AICs to provideacquisition and administration flexibilityValue-based price per dose(USD 3,250)Comprehensive patient and HCP supportprograms available at launch to ensuretimely accessProduct available from specialtydistributors in early JanuaryHCP – Healthcare Professional1. Across the 6-month dosing interval.

Additional key 2022 launches include Scemblix and 177Lu-PSMA-617177Lu-PSMA-6172First STAMP inhibitor in 3L CMLPrognosis remains poor for patients with mCRPC3FDA approval received in 3L CML and CML patients with T315I mutation2nd most diagnosed cancer in men 25% of all CML patients addressable with current label 80% of patients metastatic at the time of CRPC diagnosis 10 months median OS on available treatment optionsPotential to provide best benefit-risk profile in 1L CML 50% of patients treated front line with imatinib30-40% treated with 2nd generation TKIsdevelop resistanceor intoleranceInitiated 1L pivotal study of asciminib vs. investigator-selectedTKI (FPFV1 achieved in Q4 2021)1. First patient first visit.122. Product and brand name are currently under FDA review.3. Metastatic castration-resistant prostate cancer.J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONSWith FDA Priority Review, PDUFA4 expected H1 2022Submitted 68Ga-PSMA-11 kit for PET imaging to FDAScaling community centers on RLTEMA submission completed and approval expected in H1 20224. Prescription Drug User Fee Act.

2Novartis Growth StoryBeyond 20263

Our innovative pipeline addresses unmet medical needs with arenewed focus to deliver high value 0FDA breakthroughtherapy designationsin the past 6 yearsNME US FDA approvals3Focus on assets withsignificant potentialNMEs65 85%Phase 3 / RegistrationPipeline2 potentially100Phase 1/214 1.5xeNPV growth per asset since 20174Rapid transitions to pivotal studiesespecially for high value assets(e.g. JDQ/TNO, NIS, YTB)first-in-class / first-in indication 80%Target areas of highunmet need21. As per IR Q3 2021 pipeline.Early expansion into multipleindications (e.g., Iptacopan,Remibrutinib)2. Confirmatory development pipeline.2017Early out licensure ofnon-strategic internal assetsConfirmatory Development Pipeline eNPV3. Source: Evaluate Pharma, US NME FDA Approvals 2018 -2020.J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS20214. Confirmatory development pipeline, IMB portfolio review May 2017 vs May 2021

20 potential billion USD pipeline assets with approval by 2026Most are supported by high strength of evidenceSelected assetsStrength of evidenceStrength of evidenceModerateHighUnprobabilizedpeak salesSabatolimabIptacopanKisqaliLeqvioMDS; AMLPNH; C3G; IgAN; aHUSAdj. BC ( endocrine th.)HypercholesterolemiaUSD bn / multi-bnNIS793RemibrutinibYTB3232CosentyxPDAC; Colorectal CancerCSU; MS2L DLBCLPelacarsenCVRRCanakinumabAdj. NSCLCOciperlimab1ZolgensmaSMA ITIanalumabSjogren’s; SLE; AIH;Lupus NephritisLu-PSMA-617mCRPC post & pre-taxane;mHSPCScemblixFA; CINDU3L CML; 1L CMLTislelizumabMultiple indicationsUNR844PiqrayPresbyopiaPROS; HER2 adv BC;TNBC; Ovarian cancerLibvatrep (SAF312)Most advanced andkey indication(s)approved by 2026Multiple indications177LigelizumabNSCLC SubmissionPhase IIIPhase IILCM ApprovedChronic Ocular Surface PainTNO155, JDQ4432NSCLC; Colorectal Cancer;CombosUnprobabilizedpeak salesLutatheraKymriahBeovu1L G2/G3 NETr/r Follicular LymphomaDMETafinlar/MekinistJakaviSolid Tumor AgnosticSR GvHDup to USD 1bn1. BeiGene option deal.2. Ph3 to start in 2022.Assets are shown in the phase of the most advanced indication (listed first).indication.15Value based on the total of the listed indication(s).J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONSStrength of evidence based on the most advanced indication: High if in Ph3 or when Ph2 results available for the same MoA in the lead

Recent data releases support progression of our mid-stage pipelineCosentyx HSIptacopanJDQ443IanalumabPrimary efficacy endpoint wasmet in both Ph3 studiesSUNSHINE and SUNRISEC3G: 45% proteinuria reduction;EMA PRIMEEntering Ph3 2L KRAS G12Cmutant NSCLC in H1 2022,based on ongoing Ph1 studySjögren’s Ph2b primaryendpoint met, confirmingefficacy and good tolerabilityPNH: Ph2 substantial reductionin intra- & extravascularhemolysis; FDA BTDAutoimmune hepatitis, SLEand CLL studies ongoingRemibrutinibYTB323 / PHE885BranaplamOciperlimab (TIGIT)Rapid and effective CSUdisease activity control, withfavorable safety in Ph2bT-Charge assets presentedat ASH:Potential FIC1 for Huntington’sPh2b initiated based ondemonstrated PoC in preclinical, Ph1 (healthyvolunteers) and SMA studiesCurrently in Ph3 trials forNSCLC in combination withtislelizumab2Additional studies ongoing in awide range of solid tumorsAnti-CD19 YTB to Ph3Anti-BCMA PHE to Ph21. First-in-class.162. Active trials conducted by BeiGene.J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS

Recent business development activities strengthening our pipelineand platformsAdding a one-time subretinal gene therapy that couldtransform care for geographic atrophy (GA), a leading causeof blindness1Option, collaboration and license agreement for TIGITinhibitor ociperlimab with the potential to treat a wide rangeof solid tumorsPotential 1st therapy with sustained efficacy for broad GApopulationEarly research suggests TIGIT inhibitors activity against broadrange of tumorsAAV-2 gene therapy inducing expression of CFI2 for treatmentOciperlimab adds innovative and complementary late-stageTIGIT inhibitor and potentially synergistic combinations withtislelizumab and other Novartis Oncology assetsCompelling early preclinical & clinical data of GT005 with welltolerated safety profile3FDA Fast Track designation for GT005Two Phase III trials underway in NSCLC 4 and additional studiesongoing in a wide range of solid tumorsUpcoming milestones (readouts)Phase 1/2: FOCUS Oct 2022Phase 2: HORIZON Oct 2022 and EXPLORE Feb 20231. Completion of the transaction is subject to customary closing conditions. Novartis and Gyroscope will continue to operate as separate and independent companies until closing.3. Publicly presented data J Heier, Retina World Congress, November 2021.4. Non-small cell lung cancer.17J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS2. Complement negative regulator complement factor.

Novartis and Molecular Partners report positive results on Phase 2EMPATHY clinical trial of ensovibep on COVID-19 patientsEnsovibep binding to spike protein (3D)Value proposition of ensovibepKey clinical dataDrug descriptionHSA bindingDARPin Three individual DARPin domains bindto three RBDs on spike protein offeringhigh potency against all variants Single IV infusion to be administeredwithin 7 days of symptom onset Manufacturing based on bacterialfermentation that is more easily scalableDARPin 1, 2, 3 Reduced hospitalizations, ER visits anddeaths vs. placebo (RR1 78%) Faster recovery in patients No unexpected safety findings Lowest dose of 75mg was effective inviral load reductionPan-variant-neutralization of all VOCs, in vitroSpike aP.1DeltaB.1.617.2OmicronB.1.1.529EnsovibepIC50*1 / 1.11.7 / 0.95 / 1.21.2 / 0.72.4 / -2.2 / 2.1* IC50 values in ng/mL in two different assays: VSV (Vesicular Stomatitis Virus) / Lentivirus Pseudo type Neutralization Assay1. Relative risk reduction.18J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS

Novartis is investing to lead as the Biopharmaceutical industry shifts tonew platformsNovartis portfolio shift towardsbiologics & advanced platformsGlobal pipeline composition,directional technology outlookProportion % of IM sales by platformOutlook illustrativeExpand platforms: Cell therapy Gene therapy Radioligand therapy xRNA therapy5%22%Scale biologicstherapies2Conventional(small molecules, non-recombinantvaccines, natural extracts)73%Focus on new approaches toaddress previously intractabletargets with small molecules,(e.g., TPD3)202020002010NowFuture1. e.g. Microbiome, Nanotechnologies, Bioelectronics, Bioengineered vaccines, Protein extracts.19Advanced Platforms2. Currently 60% of global clinical pipeline.J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS2030Biologics3. Targeted Protein Degradation.Small MoleculesSource: McKinsey analysis, EvaluatePharma

We take a principled approach to selecting platforms and deployingthem in our core therapeutic areasPrinciples forplatform investmentsMajor NovartisplatformsApplying our technologyacross other TAsBioChemistry therapeuticsChemistry & Chemical Biology TPD1Broad applicabilityCellGeneRLTxRNAOncologyClear differentiationBiotherapeutics xRNA2Advances disease area strategyCardio-RenalImmunologyStem-Progenitor Cell TherapyNeuroscienceScalabilityIntegration of diverse expertiseViral Gene TherapyOphthalmologyRespiratorySustained competitive advantageRadioligand TherapyCurrently marketed products1. Targeted Protein Degradation.202. xRNA includes RNA targeting LMWs, ASOs, siRNA, mRNA cancer vaccines.J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONSPotential to expand

Continue innovating on small molecules while building a strongposition in new technology tsKey focus# of projects2Expectednext filingUnlock previouslyundruggabletargetsExplore novelcargos, targeting,and switchableexpressionExpand theindicationlandscapeExplore newapproaches inRNA therapeutics1215221292026 2024202520232026 1 xRNA includes RNA targeting LMWs, ASOs, siRNA, mRNA cancer vaccines.21Enhance potency,durability andmanufacturingefficiency2. Exploratory to Ph1/2J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS

Novartis path to leadership in technology platformsBuilding on the integrated technology platform strengths across our organizationDepth and breadth across platforms 70 projects¹TechnologyplatformsDevelopment andregulatory experienceExperience in commercializationGlobalfootprint1 Exploratory to Ph1/222J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONSManufacturing scale and expertise

Novartis presents an attractive profile for investors12345ClearstrategyAttractivegrowth profileStrong mid/latestage portfolioPlatformleadershipBalanced capitalallocationDeliveringon strategyas a focusedmedicinescompanyConfident in 4% sales CAGR (2020to 2026) and abovepeer medianbeyond 2026Breadth and depth,20 assets with USD 1bn potential, fuelfurther growth to2030 and beyondContinue todevelop leadershipacross technologyplatformsAims to combineinvesting in corebusiness and returningexcess capital toshareholders23J.P. MORGAN HEALTHCARE CONFERENCE JANUARY 2022 NOVARTIS INVESTOR RELATIONS

8% Limited binary risk on a single product2 53% Key growth drivers and launches as % of IM sales, growing 26% in Q3 2021 Geographically diversified3 Company 8 Novartis Company 10 Company 12 Company 15 Company 14 Company 9 Company 13 Company 11 Company 7 Company 6 Company 5 Company 4 Company 3 Company 2 Company 1 US Asia, Africa, Australasia EU .