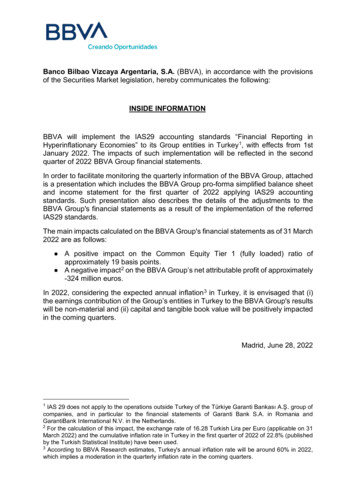

Transcription

1Q22 Results 29 April 2022

DisclaimerThe purpose of this presentation is purely informative and should not be considered as a service or offer of anyfinancial product, service or advice, nor should it be interpreted as, an offer to sell or exchange or acquire, or aninvitation for offers to buy securities issued by CaixaBank, S.A. (“CaixaBank”) or any of the companies mentionedherein. The information contained herein is subject to, and must be read in conjunction with, all other publiclyavailable information. Any person at any time acquiring securities must do so only on the basis of such person’sown judgment as to the merits or the suitability of the securities for its purpose and only on such information as iscontained in such public information set out in the relevant documentation filed by the issuer in the context of suchspecific offer or issue and after taking any professional or any other advice as it deems necessary or appropriateunder the relevant circumstances and not in reliance on the information contained in this presentation.CaixaBank cautions that this presentation might contain forward-looking statements concerning the development ofour business and economic performance. Particularly, the financial information from CaixaBank Group (“Group”)related to results from investments has been prepared mainly based on estimates. While these statements are basedon our current projections, judgments and future expectations concerning the development of our business, anumber of risks, uncertainties and other important factors could cause actual developments and results to differmaterially from our expectations. Such factors include, but are not limited to, the market general situation,macroeconomic factors, regulatory, political or government guidelines and trends, movements in domestic andinternational securities markets, currency exchange rates and interest rates, changes in the financial position,creditworthiness or solvency of our customers, debtors or counterparts, etc. These risk factors, together with anyother ones mentioned in past or future reports, could adversely affect our business and the levels of performanceand results described. Other unknown or unforeseeable factors, and those whose evolution and potential impactremain uncertain, could also make the results or outcome differ significantly from those described in our projectionsand estimates.Statements as to historical performance, historical share price or financial accretion are not intended to mean thatfuture performance, future share price or future earnings for any period will necessarily match or exceed those ofany prior year. Nothing in this presentation should be construed as a profit forecast. In addition, it should be notedthat although this presentation has been prepared based on accounting registers kept by CaixaBank and by the restof the Group companies it may contain certain adjustments and reclassifications in order to harmonise theaccounting principles and criteria followed by such companies with those followed by CaixaBank, as in the specificcase of Banco Português de Investimento (“BPI”), so that, the relevant data included in this presentation may differfrom those included in the relevant financial information as published by BPI. Likewise, in relation to the historicalinformation on Bankia and that referring to the evolution of Bankia and/or the rest of the Group contained in thispresentation, it must be taken into account that it has undergone certain adjustments and reclassifications in orderto adapt it to CaixaBank Group's presentation criteria.results in the first quarter of 2021. Likewise, extraordinary impacts associated with the integration of Bankia havebeen excluded from the result.In particular, regarding the data provided by third parties, neither CaixaBank, nor any of its administrators, directorsor employees, either explicitly or implicitly, guarantees that these contents are exact, accurate, comprehensive orcomplete, nor are they obliged to keep them updated, nor to correct them in the case that any deficiency, error oromission were to be detected. Moreover, in reproducing these contents in by any means, CaixaBank may introduceany changes it deems suitable, may omit partially or completely any of the elements of this presentation, and incase of any deviation between such a version and this one, CaixaBank assumes no liability for any discrepancy. Thisstatement must be taken into account by all those persons or entities that may have to make decisions or prepareor disseminate opinions regarding securities issued by CaixaBank and, in particular, by analysts and investors whohandle this document. All of them are encouraged to consult the documentation and public informationcommunicated or registered by CaixaBank with the National Securities Market Commission (Comisión Nacional delMercado de Valores, “CNMV”). In particular, it should be noted that this document contains unaudited financialinformation.In relation to Alternative Performance Measures (APMs) as defined in the guidelines on Alternative PerformanceMeasures issued by the European Securities and Markets Authority on 30 June 2015 (ESMA/2015/1057), thispresentation uses certain APMs, which have not been audited, for a better understanding of the company's financialperformance. These measures are considered additional disclosures and in no case replace the financial informationprepared under the International Financial Reporting Standards (IFRS). Moreover, the way the Group defines andcalculates these measures may differ to the way similar measures are calculated by other companies. Accordingly,they may not be comparable. Please refer to the Glossary section of the relevant CaixaBank’s Business Activity andResults Report for a list of the APMs used along with the relevant reconciliation between certain indicators.This presentation has not been submitted to the CNMV or to any other authority in any other jurisdiction for reviewor for approval. Its content is regulated by the Spanish law applicable at the date hereto, and it is not addressed toany person or any legal entity located in any other jurisdiction and therefore it may not be compliant with therelevant regulations or legal requirements as applicable in any such other jurisdiction.Notwithstanding any legal requirements, or any limitations imposed by CaixaBank which may be applicable,permission is hereby expressly refused for any type of use or exploitation of the content of this presentation, and forany use of the signs, trademarks and logotypes contained herein. This prohibition extends to any kind ofreproduction, distribution, transmission to third parties, public communication or conversion by any other mean, forcommercial purposes, without the previous express consent of CaixaBank and/or other respective proprietary titleholders. Any failure to observe this restriction may constitute as sanctionable offense under the current legislation.In the same way, and in order to show the recurring evolution of the results of the new entity resulting from themerger, a proforma income statement has been prepared by adding, to the CaixaBank Group’s results, Bankia’sPresentation prepared with Group data at closing of 31 March 2022, unless otherwise noted.From an accounting point of view, BKIA consolidates from 31 March 2021, incorporating assets and liabilities from BKIA at fair value on that date. The results from BKIA are included from 2Q21; in 1Q21 do not contribute to consolidated net income inthe quarter. BKIA P&L figures are presented based on CaixaBank reporting criteria.2

CONTENTSI.HighlightsII.1Q22 P&L and Balance Sheet3

1Q22 HIGHLIGHTSSolid operating performance in a volatile environmentStable volumes underpinned by improving loan production andresilient AuM inflowsHigher core operating leverage supported by non-NII corerevenues and cost-savings from personnel restructuring%NPL ratio down and coverage up with CoR trailing downdespite prudent provisioning to incorporate new macro scenarioStrong capital and MREL further reinforced–with ample buffers over requirements 4.6BnCONSUMER MORTGAGELOAN PRODUCTION(1)L/T SAVING EXMARKETS (2), QOQ 10.6% qoq 1.2Bn 0.5% qoq 1.9% yoyCORE OPERATING INCOME(3)NON-NII CORE REVEN.(3)ǀ REC. COSTS(3) 3.6% -4.3% yoy% NPL ǀ % NPLCOVERAGE-0.1 pp ytd% CoR ttm3.5%65% 2 pp ytd0.23% -42 bps yoy(3)% CET1 ex IFRS9 TA13.2% 36 bps ytd% MREL PF(4)26.5% 77 bps ytd1Q22 Net Income of 707M ( 21.9% yoy)(5)(1) Consumer and residential mortgage production in Spain. (2) Mutual funds, pension plans and saving insurance funds. Net inflows excluding market valuation impact. (3) yoy vs. 1Q21 PF including BKIA. (4) PF including 500M and 1Bn SNPbonds issued in April. The % MREL without considering April issues would be 25.8%. (5) % yoy vs. 1Q21 PF including 1Q21 of BKIA and excluding M&A one-offs.4

HIGHLIGHTSBulk of network restructuring completedwhile commercial programmes and model are fully integratedIntegration calendarBULK OF NET WORK RESTRUCTURING ALREADY COMPLETEDMAR2Q21 80% 90%APRMAYof total departures(1)completed by 1 AprilJUNof planned branch integrations(1)completed by 1 April(2)JUL3Q21SUCCESSFULLY EXECUTED WITH LIMITED COMMERCIAL DISRUPTIONAUG% Relational client base(3)SEP67.9%OCT4Q21NOV65.9%DEC68.6%66.8%March NPSat N-21SEP-21DEC-21MAR-22Setting the foundations for effective delivery of synergies(1) Total departures expected at 6,452; total branch integration involving c.1,500 branches. (2) 90% completed by end of April. (3) Individual clients in Spain. Until October 2021, excludingformer BKIA clients. From November (post IT integration) including all individual clients. (4) In Spain.5

HIGHLIGHTSStable loan-book due to rebound in new lendingunderpinned by continued commercial focus and new initiativesNEW MORTGAGE ANDCONSUMER LENDINGPERFORMING LOAN BOOK,31 MARCH 2022New lending inSpain (1) ,NEW LENDING TO SMEsNEW MORTGAGES ATPOST MERGER MAXIMUM BnNew lending inSpain (1) ,New lending in Spain (1) , Bn Bn2.1 341 Bn1.9 16% 0.2% ytd1.91.54.64.00.51.6J3Q214Q214.00.63.24.21Q21 PF 2Q21 22%1.0F3.1M1Q221Q21 PF4Q21 27%1Q22 11%1Q21 PF4Q211Q22CasaFácilByCaixaBankA solid performance in a quarter with seasonally low production To be further fuelled by NGEU initiatives(1) 1Q21 PF includes 1Q21 of BKIA.6

HIGHLIGHTSContinued success in roll-out of MyBox insurance offeringMYBOX PRODUCTION IS GROWING STRONGLYNew MyBox premia: life-risk, MNew MyBox premia: non-life, M 12%94.785.055.6 163M55.5 22%1Q22 (3)AUTOPROTECTIONINSURANCEREVENUES(2) 71%67.860.71Q22 new MyBox premia, by type of %BURIAL12%AUTO9%OTHER3%1Q22 343M 5% yoy(3)1Q22MyBox over total 1Q22 protection LEMENTING SERVICES 15 pp yoy.Includes revenues from insurance distribution fees, premia for life-risk insurance, and equity accounted income from insurance JVs. BKIA Vida consolidates from 1 January 2022, contributing to life-risk insurancerevenues and detracting from insurance distribution fees and equity accounted income from insurance JVs.% yoy vs. 1Q21 PF including BKIA.7

HIGHLIGHTSCustomer funds also stable with net inflows of long-term savingsresilient to market volatilityCUSTOMER FUNDS,31 MARCH 2022CONTINUED MARKET SHARE GAINS .Market share in long-term(Spain), % WITH POSITIVE NET INFLOWS ANDMAINTAINING HIGH LEVEL OF AUMs 29.4%NET INFLOWSINTO LONG-TERMSAVINGS(1) (1Q22) 1.2 Bn29.6%Market volatility: Vstoxx index80706050( 1% ytdex markets )40LONG-TERMSAVING AUM ON31 MARCH 2022 VS.FY21 PF(3) AVG. 2%LONG TERM SAVINGS(1) 0.5% ytd DESPITE HEIGHTENED MARKET VOLATILITY 13 bps 620 BnStable ytdsavings(2)YE21Mar-22302010D-19 M-20 J-20 S-20 D-20 M-21 J-21 S-21 D-21 M-22ex marketsA ROBUST BUSINESS UNDERPINNED BY A UNIQUE ADVISORY MODELUNIQUE MODELBASED ONADVISORY ANDSPECIALISATIONTAILOR-MADESOLUTIONS &EXTENSIVEOFFERINGSUSTAINABLEINVESTMENTAND SOLUTIONSOFFERINGCAPTIVE PRODUCTFACTORIES – ABILITYTO BROADENPRODUCT OFFERING(1) Mutual funds, pension plans and savings insurance funds. (2) Combined market share in mutual funds, pension plans and savings insurance. Sector data are internal estimates based on INVERCO and ICEA data. (3) Mutual funds (includingmanaged portfolios and SICAVs), pension plans and unit linked. 2021 PF including BKIA in 1Q21.8

HIGHLIGHTSEconomic recovery to continue despite geopolitics and inflationWhile facing a more constructive interest rate environmentGDP GROWTH PROJECTIONS REVISEDDOWNWARDS POST UKRAINEPOSITIVE DYNAMICS IN CONSUMERSPENDING CONTINUEDomestic credit/debit card spending in Spain(2), % change vs. sameperiod in 2019Spain Real GDP(1) – Central scenario, rebased to 100 FY19104IMPROVED INTEREST RATE OUTLOOK FOLLOWINGFEBRUARY ECB MEETINGPrevious projection15%Current projection10%3.0%2.5%2.0%5%100Euribor 12M, annual 0192018-25%882017-0.5%2016April 22: 13%-20%0.0%2015-15%92(1)(2) 10%20141Q22:2013-10%201296FEB MAR APRImplicit at YE212022CaixaBank Research as of March 2022. Refer to the appendix for additional information on macroeconomic scenarios.Transactions (including e-commerce) and cash withdrawals with credit/debit cards issued by CABK. Clients from Bankia or shared with Bankia are excluded.Current implicitHistorical(3)2022e, 20223e and 2024e based on implicit market rates as of27 April 2022 and 31 December 2021.9

HIGHLIGHTSFacing future scenarios from a position of strengthSOUND CREDIT METRICS WITH STRONG COVERAGENET INCOME GROWTHNetincome(1),NPLs, Bn eop M-5% 22%707 22% yoy5804Q21 PF13.6SUPPORTED BYOPERATING LEVERAGEAND LOWERIMPAIRMENTS3371Q21 PF14.11Q2213.4-2%0.23% CoR ttm , -42 bps yoy(2)65% NPL COVERAGE1Q214Q211Q22( 2 pp ytd)FURTHER REINFORCED SOLVENCY POSITIONSTRONG MREL AND COMFORTABLE LIQUIDITY% CET1 ex IFRS9 TA (eop) vs. requirement% MREL including IFRS9 TA (eop) vs. requirement12.8%13.2%13.4% CET1 INCLUDING 36 bps8.3%25.7%IFRS9 TA26.5%22.2% 77 bps17.9% TOTAL CAPITALINCLUDING IFRS9 TA4Q21(1)(2)(3)3.5% NPL RATIO (-0.1 pp ytd)1Q22SREP511 bps MDA BUFFER4Q211Q21 PF including BKIA and excluding M&A one-offs. 4Q21 PF excluding M&A one-offs.yoy vs. 1Q21 PF including BKIA.PF including 500M and 1Bn SNP bonds issued in April. The % MREL without considering April issuances would be 25.8%.1Q22 PF(3)2022 Req.CONTINUED MARKETACCESS 1BN SOCIALSP ISSUED IN JAN 500M SNP AND 1BNSNP IN APRIL154% NSFR10

HIGHLIGHTSStrengthening our commitment to support clients and societySWIFT RESPONSE TO SUPPORT THOSEAFFECTED BY THE WARWHILE SUPPORTING OUR MOST VULNERABLE CLIENTS AND THE ECONOMIC RECOVERYMicroBank in 2021 figuresTransfers and use of ATMs free of charge for refugees Free current accounts for refugees Platform to collect funds to donate to NGOs Buses to transport 400 refugees to Spain Corporate volunteering programme 5,000 ACTIVEVOLUNTEERS (2021)(1)According to “Microfinance in Europe: Survey Report 2020 edition”. 1.2 MillionMicro-loans with socialimpact granted sinceMicroBank was createdin 2007 953M6,672Granted inmicro-loansNew businesses createdwith micro-loan support17,00786,859Jobs createdwith microloan supportFamily microloans grantedW I T H S U PPO R T F R O ME U R O PE A N I N S T I T U TI O NSLARGEST PRIVATE MICROFINANCE INSTITUTION IN EUROPE(1)11

CONTENTSI.1Q22 HighlightsII.1Q22 P&L and Balance Sheet12

1Q22 P&L AND BALANCE SHEETStable loan-book in a quarter with usual adverse seasonalityLOAN BOOKP E R F O R MI N G L O AN S31 March 2022 Bn% ytdI. Loans to individuals182.9-1.0%Residential mortgages138.7-0.8%Other loans to individuals44.3-1.6%o/w consumer loans18.80.6%o/w other25.4-3.1%II. Loans to businesses148.60.8%Loans to individuals & businesses331.5-0.2%21.95.4%Total loans353.40.1%Performing loans340.70.2%(1)III. Public sector(1)(2)Waterfall ytd, BnDec-21MortgagesStructural deleveraging inmortgages continues, althoughproduction trends are rapidlyimproving Gradual recovery in consumerlending underpinned by macrorecovery, post pandemic spendingand new commercial initiatives Solid growth in business lendingdespite adverse seasonality,supported by growth in SMEproduction340.0(1.0) 0.1Consumer 1.2Businesses 0.2% 0.4Other(2)Mar-22 340.7Unsecured loans to individuals, excluding those for home purchases. Includes personal loans as well as revolving credit card balances excluding float.Includes public sector and “Other loans to individuals” other than consumer lending.NGEU tailwind yet to come13

1Q22 P&L AND BALANCE SHEETHigher ALCO book and yieldsTOTAL ALCO (1)WHOLESALE FUNDING COSTS Bn, eopFV-OCIAC (2)62.340.260.341.844.570.362.456.420.5Mar-21 PFEx )2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 REI GN EXPOSURE0.30.30.30.30.53.83.94.34.9AVERAGE LIFE, YRS3.5DURATION, YRS2.78.614.914.6YIELD, %3.07.84.715.8VolumeGroup as of 31 March 2022, Bn9.447.941.124.40.6Group ex BPI wholesale funding back-book volumes(5) in Bn and spread over 6M Euribor in bpsMATURI TY PROFI L E3.0Breakdown by main exposures(4), 31 March 2022OTHER83%3.43.44.14.57%5%5%Mar-21 PFEx BKIA(1) Banking book fixed-income securities portfolio, excluding trading book assets. It includes 3.5Bn of callable bonds for which yield, average life and duration are calculated based on current market levels. (2) Securities at amortised cost.(3) Additionally, there are SAREB bonds not included in the Group’s ALCO portfolio (c. 19Bn by end of 1Q). (4) Sovereign exposures account for 91% of total ALCO book. (5) It includes securitisations placed with investors. It does not include AT1issues. Wholesale funding figures in the Quarterly Financial Report reflect the Group’s funding needs and as such do not include ABS securities and self-retained multi-issuer bonds but include AT1 issuances.14

1Q22 P&L AND BALANCE SHEETCustomer funds stable despite market impactsWith resilient inflows into long-term savings productsCUSTOMER FUNDS31 March 2022I. On-balance-sheet fundsDeposits% ytd457.70.6%385.80.4%Evolution ytd, Bn620.0AUM (6) AVG. BALANCESGroup, rebased to 100 FY21 avg. AuM(7) 1.0%(6.1) 4.92021 Average(7) 100619.91031051021021Q221Q22 -3.3%Mutual funds(2)106.2-3.5%Pension plans46.6-2.8%9.333.9%1.2-4.1%619.90.0% Off-balance sheet funds AuM reflect market correction in Jan-Feb partly offset by positive net inflows in the quarter andMarch market recovery221.8-2.2% Q1 end of period AuM 2% vs. 2021 avg.(7) expected to provide support in 2QDemand depositsTime deposits(1)Insuranceo/w unit linkedOther fundsII. Off-balance-sheet AuMIII. Other managed resourceso/w insurance fundsTotalLong-term savings(1)(2)(3) BnCUSTOMER FUNDS WATERFALL(3)613.8Marketeffects(4)Dec-21 1.2L/t savingnet inflows(ex market)98Deposits& other(5)94Mar-221Q21 PF2Q213Q214Q21 Stable customer funds despite adverse market impact. Excluding such impact, customer funds grow by 1% ytd On-balance sheet funds remain flat with support from demand deposits and continued growth in unit linkedIncludes retail debt securities amounting to 1.4Bn on 31 March 2022.Includes SICAVs and managed portfolios.Savings insurance (on-balance-sheet and other managed resources), pensionplans and mutual funds (including SICAVs and managed portfolios).(4)(5)(6)(7)Includes impact from markets on off-balance-sheet AuMs and unit linked.Includes deposits, other funds and other managed resources (excluding insurance funds).Mutual funds (including managed portfolios and SICAVs), pension plans and unit linked.PF including BKIA in 1Q21.15

1Q22 P&L AND BALANCE SHEETNet income growth underpinned by lower costs and provisions1Q22 P&L HIGHLIGHTS(3)CONSOLIDATED INCOME STATEMENT (1)(3)% qoq adj. (3)1Q21 PF (2) % yoy adj. M1Q22Net interest income1,5501,639-5.4%-0.6%Net fees and commissions9699412.9%-12.0%Income and expense 26.1%LLPs(228)(297)-23.2%-33.7%Other provisions(45)(72)-37.7%-75.2%Gains/losses on disposals and 70758021.9%DividendsEquity accountedOther operating income/expensesGross incomeRecurring operating expensesExtraordinary operating expensesPre-impairment incomePre-tax incomeTax, minority & other(2)Net incomeo NII starts to stabilise qoq; affected by lower day-countREVENUESCore revenues2,7612,808-1.7%-4.4%Core operating income(5)1,2381,2151.9%-5.7%o Fees 2.9% yoy with qoq impacted by adverse seasonality and marketvolatilityo Insurance grows strongly with both organic growth and 100%consolidation of BV Non-core revenues reflect higher trading offsetting lower equity accountedincome and higher charges in “other operating income/expenses”; qoqimpacted by seasonal items(8)Pro memoria(4) Core revenues(4) -1.7% yoy on lower NII, partly offset by growth in fees andpremiaCOSTS Lower costs in line with guidance (-4.3% yoy) reflecting personnelcost-savings Core operating income(5) 1.9% yoyPROVISIONS LLPs remain at low levels despite incorporating UKR-related macro risks Other provisions and gains/losses fall significantly(1) BKIA consolidated from 1 April 2021. 1Q22 affected by consolidation of BKIA Vida from 1 January 2022. (2) 1Q21 PF including BKIA and excluding M&A one-offs. (3) % yoy vs. 1Q21 PF including BKIA and excluding M&A one-offs; % qoq vs.4Q21 PF excluding M&A one-offs. (4) NII Fees other insurance revenues (including life-risk revenues and equity accounted income from SCA and other bancassurance stakes). Both yoy/qoq across all core revenue lines affected byconsolidation of BKIA Vida. (5) Core revenues minus recurrent expenses.16

1Q22 P&L AND BALANCE SHEETBPI segment:Growth of core revenues yoy driven by solid commercial trendsBPI SEGMENT P&L (1) M1Q22% yoy% .5%9.6%64-1.2%340-70.1%9823.8%(29)39.9%6918.1%Core revenues1894.2%-7.5%Core operating income (2)748.7%-25.4%Net interest incomeNet fees and commissionsOther revenuesGross incomeRecurring operating expensesHIGHER OPERATING LEVERAGECONTINUED LOAN -BOOK GROWTHB PI - se g m e n t c o re o p e ra t i n g i n c o m e ( 2) , MPe rf o rm i n g l o a n - b o o k ( e o p ) wa t e rf a l l , i n B n a n d % y t d 8.7% 0.4Impairment losses & other provisionsGains/losses on disposals and otherPre-tax incomeIncome tax, minority interest & othersNet attributable profit1Q211Q22 0.3Businesses 0.0Public sector& other(3)27.6MortgagesYE21Loan production – 1Q22Including the results of BPI's domestic banking activity, carried out essentially in Portugal.Core revenues minus recurrent expenses.Credit to public sector and other credit to individuals excluding residential mortgages and consumer lending.Production of consumer loans and car financing. 0.0Consumer26.9-39.0%Pro memoria(1)(2)(3)(4)7468Extraordinary operating expensesPre-impairment income 2.7%1Q22% NPL, 31 March 2022 48% yoy 35% yoy2.3%MortgagesConsumer lending(4)Stable ytd17

1Q22 P&L AND BALANCE SHEETNII (ex TLTRO) and margins start to stabilise in Q11Q22 QOQ EVOLUTIONNII EVOLUTION (1) M1,6391,636NII BRIDGE QOQ (1)-5.4%1,5891,559NII affected by lower day-count in Q1 M1,5591,550-15Day-count448 8-2Client NII(2)1,1911,550ALCO &other(3)ALCO: positive contribution fromhigher volumes and yields-0.6%1Q21 PF2Q213Q214Q21YIELDS (1)171Client funds167163161costs(4)1611000-21Q21 PF2Q213Q214Q211Q221Q22MARGINS (1)167163Customer spread and NIM broadlystableLoan BB yields start to stabiliseCus tom e r s pre ad, bps170FB LOAN-0.6%4Q211Q22Net loan yieldsI n bpsClient NII impacted by both lower loanaverage volumes and lower index resets161FB yields increase in Q1 driven by lowerweight of CIB163Y I E L D ( 5)NIM 2 bps191 bps89 bpsS t a b le v s . 4 Q 2 1 27 bps vs.4Q211Q21 PF2Q213Q214Q21FACING A MORE FAVOURABLEINTEREST RATE OUTLOOK1Q22(1) 1Q21 PF with BKIA. 1Q22 affected by consolidation of 100% of BKIA Vida from 1 January 2022. (2) Excluding day-count and including NII from life-savings insurance with contribution from consolidation of 100% of BKIA Vida from 1January 2022. (3) Including assets, liabilities and other. (4) Evolution in 1Q22 qoq reflects impact from swap derivatives concerning a small subset of retail funds. (5) Group ex BPI. Excluding public sector. Front-book yields are compiled fromlong-term lending production data (loans and revolving credit facilities, including those that are syndicated) of CaixaBank,S.A. and MicroBank.18

1Q22 P&L AND BALANCE SHEETFees grow c.3% yoy with AM and wholesale banking fees showingresilience to markets QoQ affected by adverse seasonalityFEE EVOLUTION (1) M941FEE BREAKDOWN BY MAIN CATEGORY (1) 2.9%9811,1019649692821Q226591Q21 PFRECURRENTBANKING-12.0%2Q213Q214Q211Q22FEE BRIDGE YOY (1) 32 M941-16Recurrentbanking 9Wholesale969(1)(2)(3)471% yoy adj.(2)-3.3%% qoq-10.6%ASSETMANAGEMENT(3)345 10.3%-14.2%INSURANCEDISTRIBUTION100 2.3%-13.9%WHOLESALEBANKING52 22.0%-6.0%TOTAL969 2.9%-12.0% 2InsurancedistributionAM 2.9%1Q21 PFNet fee evolution qoq affected by lowerday-count and other adverse seasonalityacross different lines1Q22, M and %1Q221Q21 PF with BKIA. 1Q22 affected by consolidation of 100% of BKIA Vida from 1 January 2022.% yoy vs. 1Q21 PF including BKIA.Including mutual funds, managed portfolios, SICAVs, pension plans and unit linked.Recurrent banking: affected by loyaltyprogrammes; qoq also reflecting adverseseasonalityAM: growth yoy supported by higheraverage volumes; with qoq mostly reflectingpositive seasonality in Q4, lower day-countand impact from market correction, partlyoffset by positive net inflowsInsurance distribution: continued growthyoy; qoq mostly reflecting positiveseasonality in Q4Wholesale banking: strong growth yoywith qoq affected by market correction andseasonally low production19

1Q22 P&L AND BALANCE SHEETContinued growth in other insurance revenuesboosted by BV revenue synergiesOTHER INSURANCE REVENUES (1) MLife-risk insurance revenues, MLife-riskEquity accounted 6.4%202164243228138Strong growth in life-riskinsurance revenues ( 22.9% yoy/ 17.6% qoq) supported bycontinued organic growth andrecovered revenues from BV150130110164 22.9%202Evolution in equity accountedincome affected by consolidationof 100% of BV and by lower equityaccounted income from SCAreflecting impact from extensionof commercial agreement644532641Q21 PF411Q221Q141Q151Q161Q171Q181Q191Q201Q211Q22(1) Including life-risk revenues and equity accounted income from SCA and other bancassurance stakes.1Q21 PF including BKIA’s other insurance revenues. 1Q22 affected by consolidation of 100% of BKIA Vida from 1 January 2022(positive contribution to life risk insurance revenues and negative contribution to equity accounted revenues).20

1Q22 P&L AND BALANCE SHEETSignificant cost reduction as personnel cost savings feed inRECURRENT COSTS (1)Lower recurrent costs (-4.3% yoy / -3.4%qoq) as cost-savings from restructuring feed in M-4.3%1,5931,5981,6061,5771Q22, 2%DEPRECIATION195 7.1%-0.5%1,523-4.3%-3.4%TOTAL1Q21 PF(1)(2)2Q213Q214Q21% qoqPERSONNEL1,523444% yoy adj.(2)1Q22 90% of employee departures alreadycompleted by 1 April 2022; bulk of departuresexpected to be completed by July 2022 80% of cumulative cost-synergies expectedto be booked by 20221Q expenses impacted by consolidation of BVand by seasonal items (property taxes)Recurrent Core C/I ratio (ttm): 55.8%(-38 bps qoq)1Q21 PF including BKIA. 1Q22 affected by consolidation of 100% of BKIA Vida from 1 January 2022% yoy vs. 1Q21 PF including BKIA.21

1Q22 P&L AND BALANCE SHEETAmple coverage allows for LLCs in line with guidanceCOR TTMLOAN LOSS CHARGES MGroup LLPsBKIA LLPs-23.2%%1Q22 LLCs include impactfrom new macro scenario1Q22 CORA N N U A L I S ED %0.23%3Q214Q211Q22CoR (ttm and annualised)in line with guidance-33.7%1Q21(1)(2)(3)0.25%0.30%1651741Q21 PFMaintaining an ampleCOVID reserve buffer of 1.2 Bn(3)2Q213Q214Q211Q22CoR in 1Q21 TTM reported excluding impact from BKIA in the denominator for consistency with the numerator.1Q21-4Q21 PF including 12 months of BKIA.COVID reserve recalculated in Q1.(1)2Q21CoR TTMCoR TTM PF W/BKIA(2)Reiterate FY22E CoR: c.25 bps22

1Q22 P&L AND BALANCE SHEET%NPL ratio down and coverage reinforced further% NPL (-0.1 pp qoq) AT HISTORICALLY LOW LEVELSGroup NPL stock and % NPL(1), eop in Bn and %% NPLNPL .5%-5.1%-9 bps .48.7Mar-21 PFEx BKIANPLs fall yoy and qoq with % NPL (-0.1 ppqoq) broadly stable at March 2021 levelsNPL RATI O BY SEGMENT, 1Q22 % EOPB KI .4%-2 bps qoqNET OREO EXPOSURE1 Q 2 2 , % e op% NPL COVERAGE (3)31 MARCH 2022-13 bps qoqOther(2)3.5% 2.2Bn-16 bps qoq-2.5% qoq65% 2 pp qoqStrong NPL coverage at 65% ( 8.6Bnprovision funds including 1.2Bn unusedCOVID reserve by end of Q1)7% of total ICO loans(4) granted werealready amortised; of the remainder, 40%are already repaying principal by end ofQ1 and 91% will do so by end of 2Q 97% of ICOs are performing(5)Non-material exposure to RUS(6);strong coverage and prudent riskmanagement provide comfort for thefuture(1) Includes non-performing contingent liabilities ( 657M by end of March 2022). (2) Includes other credit to individuals (ex consumer lending), credit to the public sector and contingent liability NPLs. (3) Ratio between total impairment allowanceson loans to customers and contingent liabilities over non-performing loans and advances to customers and contingent liabilities. (4) L

1Q22 Net Income of 707M ( 21.9% yoy)(5) (1) Consumer and residential mortgage production in Spain. (2) Mutual funds, pension plans and saving insurance funds. Net inflows excluding market valuation impact. (3) yoy vs. 1Q21 PF including BKIA. (4) PF including 500M and 1Bn SNP bonds issued in April.