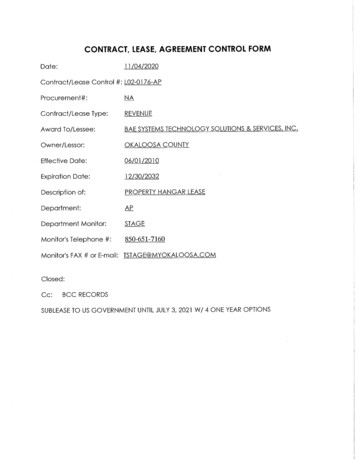

Transcription

Allowance for loanand lease lossesThe road ahead with thecurrent expected creditlosses (CECL) approach

We are pleased to present the third in a series1 of publications that highlights Deloitte Advisory’s point of viewabout the significance of the Financial Accounting Standards Board’s (FASB) Proposed Accounting StandardsUpdate (ASU), Financial Instruments—Credit Losses, and its impact on allowance for loan and lease losses(ALLL). Papers describing our perspective and the potential implications of the current expected credit loss(CECL) model will continue to be published at www.deloitte.com/us/cecl.BackgroundIn recent years, financial institutions have received additional scrutiny from regulators and external auditors on the ALLL.One of the main reasons for the heightened scrutiny from regulators and auditors around the allowance is the delayedrecognition of credit losses (“too little, too late”) as witnessed by the downturn.Industry challenges include a need for more robust ALLL quantitative and qualitative processes that are well-documentedand also demonstrate how the financial institution’s management has critically challenged the underlying assumptions andconsistently applied ALLL policies and procedures. Supporting policies and procedures, data, models, and appropriate riskrating systems are also challenges financial institutions are encountering. Ongoing monitoring of model performance, aswell as independent model validations, are integral to managing model risk around the ALLL process.The financial downturn experienced in 2008 and afterward appeared to expose the weaknesses of the incurred lossapproach. In response, the FASB has proposed a new ASU, Financial Instruments—Credit Losses (Subtopic 825-15),commonly referred to as the current expected credit loss (CECL) model. Under CECL, entities are required to account forexpected losses over the estimated life of the loan. This is a significant change to the current requirement of recordingonly incurred losses (probable losses) that can be reasonably estimated. Although outcomes of this calculation will beinstitution- and portfolio-specific, an increase in ALLL levels is expected under CECL. The distinction between using the“life of the loan” for the loss forecast horizon compared to the existing loss emergence period concept is perhaps thegreatest impact of CECL. In addition, financial institutions will be required to incorporate “reasonable and supportableforecasts” that impact the reserve estimate as well as corresponding ALLL processes.The CECL guidance represents a substantial departure from current ALLL practices. However, many of the modelingapproaches that financial institutions currently use for Basel regulatory capital calculations, economic capital calculations,and for stress testing purposes can be leveraged and adapted for CECL. The introduction of the CECL model has broadimplications, and adoption of the CECL model will require a well-thought-out tactical plan.ModelingThe recession challenged many of the existing models and methodologies used by banks to estimate the ALLL. Key industryconsiderations related to the ALLL process include: Increased regulatory oversight of banking risk management practices, including the ALLL process and modeling capabilities. Clean, accurate, loan-level data for both modeling and reporting purposes.–– Data silos that cannot be linked/aggregated–– Lack of internal loss history to support ALLL model Portfolio combinations or changing/inconsistent definitions Assumed relationships to external data (is the relationship real?)–– Lack of granular data–– Stale credit ratings/score data1The first publication, Staying ahead: Allowance for loan losses can be found at www.deloitte.com/us/all. The second publication, Putting currentexpected credit losses in perspective: Fundamentals of implementation success, can be found at tml.Allowance for loan and lease losses: The road ahead with the current expected credit losses (CECL) approach2

Development of robust, well-documented, data quality processes that provide details for extract, transform, and load (ETL)procedures as well as data quality scorecards or reports. Separation of loan-level characteristics to be used in modeling probability of default (PD) and loss given default (LGD)parameters, to align ALLL practices with Basel requirements. Challenges to banks to support their loss emergence period (LEP). Model variance tolerance policies that often do not exist. Overly simplistic or overly complex models. Lack of sensitivity analysis and stress testing around the ALLL. Models development using spreadsheet-based formulas rather than programming languages. Business and modeling assumptions are many times not adequately documented and rationalized. Regulatory requirements that banks better discern among different risk profiles and identify appropriate homogenouspools of loans. Over-reliance on qualitative adjustments given the inaccuracies of the current quantitative methodology.Consideration and planning for CECL is crucial as banks enhance their ALLL programs to withstand increased regulatory scrutiny.CECL modeling considerationsTransitioning from the current accounting guidance’s incurred loss approach to CECL will require a significant amount ofthought and discussion with key stakeholders. A brief discussion of key changes that may impact credit modeling—thelife-of-loan estimate, and use of reasonable and supportable forecasts—is provided below.Life-of-loan estimatesOne of the most talked about aspects of CECL is the use of a life-of-loan concept. In practice, the life-of-loan concept iswidely viewed as replacing the LEP that is currently used, thus creating the potential that estimates need to cover a longerloss horizon. Exhibit 1 depicts a typical situation where a loan’s average life is longer than its LEP.Exhibit 1. LEP vs. Life-of-loanLife-of-loanOriginationApplication approved,loan agreement signed, and loan fundedLoss eventUnobserved event causing the borrowerto become delinquent (e.g. healthcare issues,job loss, divorce)The average time from the loss event to thediscovery date can be estimated using thecombination of business assumptions,post mortem analysis of charged-off loans,or a survey of relationship managers.Obtaining their expert judgment viewscan provide multiple points to triangulatethe reasonableness of loss confirmationperiod assumptions.Loss emergence periodEnd of loan's lifePaid off, settlement, restructured, etc.Discovery dateWhen the borrower’s inability to paybecomes evident to the financial institution(e.g. borrower begins missing payments)Loss confirmation date(charge-off)The average time from the discovery date toloss confirmation date can be estimatedusing historical data.Allowance for loan and lease losses: The road ahead with the current expected credit losses (CECL) approach3

It is widely expected that many loan portfolio segments will have longer average lives than LEPs. To better understand thedifferences between these two loss horizon estimates, institutions should consider the following methods as possible startingpoints in the process: To determine the life of the loan time horizon, an institution could take the weighted average life of the loan (by portfolio)to estimate the time horizon over which to forecast losses. Banks can then begin developing life-of-loan loss estimates and justify adjustments from the historic average lossesestimated using LEPs.Performing comparisons between these estimates with the current loss forecast, using the LEP concept, would provide ageneral estimate of the potential impact. Where PD models are used, PD term structures, much like term structures usedfor managing interest rate risk, will need to be developed to align with the average life of the loan for each portfolio.Reasonable and supportable forecastsThe estimate produced by the CECL model would be founded on management’s assessment of current conditions andforecasts about future conditions. Some considerations in developing forecasts include: Significant reliance on judgment where detailed long-term forecasts are not available. Regulatory stressed scenarios not intended to be used directly for accounting purposes. Development and documentation of processes to demonstrate appropriate macroeconomic scenarios used in ALLLestimation under CECL (i.e., scenario generation). Consistent application of macroeconomic forecasts and other relevant information where credit risk drivers of theportfolios are affected by forecasts/assumptions in a similar manner.Allowance for loan and lease losses: The road ahead with the current expected credit losses (CECL) approach4

Points of convergenceWhile CECL represents a significant change in accounting for the allowance, current credit risk measurement approachesused for Basel regulatory capital calculations, economic capital, and stress testing (CCAR/DFAST) provide some elements thatcan be potentially leveraged for CECL. The underlying transition matrix, loss curve, and expected loss (EL) framework lossestimation methodologies, among others, have several points of convergence that can be leveraged through an integratedapproach. Some key examples include: Balance sheet mapping/exposure identification. Common definitions and classifications of both on and off balancesheet exposures allow for a holistic balance sheet mapping and ongoing exposure identification activities. Data sourcing. Given the significant overlap of data requirements (e.g., balance amounts, obligor data), upfront activities toalign efforts can reduce redundant data. Infrastructure. Common components including enterprise level data warehouses and related activities such as commondata quality protocols can simplify infrastructure design, reduce cost, and enhance operational efficiencies. Processes and controls. Common processes and control points can be identified and leveraged to reduce theimplementation and operational burden. Risk models and valuation engines. Quantitative tools can be aligned and calibrated for use across the capitalmanagement framework to ensure consistency.Exhibit 2 lays out some common factors used in calculating regulatory capital, stress testing. It also describes how theyare—or should be—used for each estimation exercise.Exhibit 2. Points of convergenceBaselProbability of default (PD)Loss given default (LGD)Other factors(macroeconomic, etc.)Stress testing(CCAR, DFAST)CECLOne-yearthrough-the-cycle PDStressed PD alignedwith forecast horizonLife-of-loan,point-in-time PDDownturn LGDLife of the loanLife of the loanNot prescribed, but effectiveoversight should includemacroeconomic factors inassessing reasonableness ofregulatory capital estimatesForecasts are 13quarters in lengthMacroeconomic forecasts needto align with the same timehorizons used in assessingPD and LGD; assumptionsneed to be documented andrelationships to the portfolioand the allowance need to bedemonstratedAllowance for loan and lease losses: The road ahead with the current expected credit losses (CECL) approach5

Practical solutionsPD models have widespread use in the financial services industry on a range of portfolios and exposure types. Under the incurred loss model, the number of months used in the PD forecast horizon corresponds to the LEP overwhich inherent losses are estimated (e.g., one-year PD estimates correspond to a twelve-month LEP). Under CECL, this would change to using a life-of-loan concept as the starting point for estimating expected credit losses.In order to estimate PDs under CECL, a bank must calculate its loan portfolio’s average life, which should then betranslated into a term structure for PD. The following steps illustrate a potential approach for performing such an exercise.Step 1. Calculate the average life of the loan for each portfolio segmentThe following are some common methods to calculate the life of a loan: Weighted average life, which is the average time until a dollar of principal is repaid. The principal amount is not discounted. Duration, which is the weighted-average time to receive the discounted present values of all the cash flows(including both principal and interest). Weighted average maturity, which is the average of the maturities of the loans in a pool.Step 2. Estimate new PDs for each segment of the portfolio using that segment’s average lifeThis concept can be seen as being analogous to tenor/maturity matched funds transfer pricing used in balance sheetmanagement, where costs of funds are aligned to the assets based on the interest rates in effect at the time, based on theasset’s time to maturity. Under the CECL paradigm, in essence, the ALLL should help bring an asset’s credit and market risksinto closer alignment, which will assist companies with developing a more fulsome picture of the risks their assets contain.Step 3. Analyze the impact Re-estimate ALLL model with life-of-loan PDs instead of PDs tied to loss emergence periods. As applicable, develop LGD analyses that relate macroeconomic data to loss severities and collateral recovery rates,to assess and document any relevant relationships between changes in the economy with changes in the portfolio’sloss history. Re-estimate credit conversion factors or loan equivalents used in the estimation of exposure at default (EAD). Layer in additional CECL components, such as reasonable and supportable forecasts into qualitative factors. Develop an analysis showing the incurred loss model result, expected life-of-loan model estimate, and other CECLcomponents to explain prospective changes in the allowance under the CECL framework vis-à-vis the current incurredloss approach. Socialize with key stakeholders, including the entity’s internal audit department and external auditors.Allowance for loan and lease losses: The road ahead with the current expected credit losses (CECL) approach6

Next stepsTo prepare for CECL, develop an implementation framework that aligns with the company’s strategy. Board members shouldpush risk management to be prepared for the transition so that the change in the reserve estimate under CECL is transparentto regulators and external auditors from modeling and process standpoints. Exhibit 3 illustrates a high-level implementationframework that can be used to guide the institution’s adoption of the CECL standard.Exhibit 3. Illustrative implementation frameworkFASB issues new credit impairment standardUnderstandcurrent plementation2Develop roadmapto future stateExhibit 4. Recommended next steps1Identify CECL changes Evaluate CECL and identify process and operational impacts Define a target future state with management, incorporating CECL and leading banking practices2Gap assessment Evaluate current state (data, processes, models, governance, operating model, etc.) Identify gaps, enhancement opportunities, and develop high-level roadmaps Develop an overall strategy/prioritization related to key cross-functional initiatives thatimpact the ALLLTarget futurestate of theALLL program(adopting CECL)3Operationalize changes Develop CECL implementation playbook Develop a detailed implementation plan, leveraging the playbook (timing/sequencing,resources, plan to close gaps, infrastructure needed to support CECL, etc.) Identify/remediate implementation issues (iterative) Implement changes in a parallel process and analyze ALLL impact (iterative)Allowance for loan and lease losses: The road ahead with the current expected credit losses (CECL) approach7

Successful implementation of the CECL standard will also require a well-thought-out tactical plan to meet the implementationframework’s objectives. One way to operationalize the CECL implementation is to develop a CECL playbook that includesdetailed roadmaps describing how initiatives will be implemented. Exhibit 4 provides some recommended next steps inassessing and planning for CECL adoption, above and beyond the development of a CECL playbook.An effective CECL implementation requires the development of a unified strategy, operationalized with a CECLplaybook, a detailed execution plan, and proper governance to oversee implementation.ContactsJH CaldwellPartner Deloitte AdvisoryDeloitte & Touche LLP 1 704 227 1444jacaldwell@deloitte.comJonathan PrejeanDirector Deloitte AdvisoryDeloitte & Touche LLP 1 703 885 6266jprejean@deloitte.comCorey GoldblumPrincipal Deloitte AdvisoryDeloitte Transactions andBusiness Analytics LLP 1 404 220 1432cgoldblum@deloitte.comBrian FlanaganManager Deloitte AdvisoryDeloitte & Touche LLP 1 312 486 4709brianflanagan@deloitte.comTony FrameManager Deloitte AdvisoryDeloitte & Touche LLP 1 704 887 1747aframe@deloitte.comEric MurphySenior Manager Deloitte AdvisoryDeloitte & Touche LLP 1 704 887 1880ericmurphy@deloitte.comJames O’NeillManager Deloitte AdvisoryDeloitte Transactions and BusinessAnalytics LLP 1 404 631 3572jaoneill@deloitte.comPublished by theThis document contains general information only and Deloitte is not, by means of this document, rendering accounting, business, financial, investment,legal, tax, or other professional advice or services. This document is not a substitute for such professional advice or services, nor should it be used as abasis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you shouldconsult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this document.About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of memberfirms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “DeloitteGlobal”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please seewww.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be availableto attest clients under the rules and regulations of public accounting.Copyright 2016 Deloitte Development LLC. All rights reserved.

consistently applied ALLL policies and procedures. Supporting policies and procedures, data, models, and appropriate risk rating systems are also challenges financial institutions are encountering. Ongoing monitoring of model performance, as well as independent model validations, are integral to mana