Transcription

Starting Thoughts2010 FPA Board of DirectorsChairRichard C. Salmen, CFP ,CFA, CTFA, EAGTrust Financial PartnersOverland Park, KSPresidentTom L. Potts, Ph.D., CFP Baylor UniversityWaco, TXPresident-ElectMartin Kurtz, CFP , AIFA The Planning Center Inc.Moline, ILDirectors Paul H. Auslander, CFP American FinancialAdvisors Inc.Orlando, FL Paula H. Hogan, CFP , CFAHogan FinancialManagement LLCMilwaukee, WI David C. Huxford Jr.Huxford & AssociatesOakland, MD Stephen D. Johnson, CFP Johnson LymanWealth AdvisorsHalf Moon Bay, CA Christopher Rand,CFP , CLU, AEPMetLife-FinancialPlanning DivisionSan Diego, CA Michael J. Smith, CFP RTD Financial Advisors Inc.Atlanta, GA Lee A. Baker, CFP Apex Financial ServicesTucker, GA Janet A. Stanzak, CFP Financial EmpowermentLLCBloomington, MN Michael A. Branham, CFP Cornerstone WealthAdvisors Inc.Edina, MN Karin Maloney Stifler, CFP True Wealth Advisors LLCHudson, OH Diana DeCharles, CFP Pinnacle AssetManagement Group LLCShreveport, LA Kenneth Ziesenheim,CFP , J.D., LL.M., AIFA Raymond JamesFinancial ServicesSebring, FL Edward W. Gjersten II,CFP Mack InvestmentSecurities Inc.Glenview, ILExecutive Director/CEOMarvin W. Tuttle Jr., CAEFinancial Planning AssociationDenver, CO Vern C. Hayden, CFP Hayden WealthManagementWestport, CTwww.FPAjournal.orgwwwwwww.FPAjournal.org 2010 Advisory Board Lance Alston, CFP Dallas, TX C. Carter Boucher,CFP , CRPC Boucher CapitalManagement Inc.Anderson, SC Jim BoxmaAbernathy FinancialServicesSouthlake, TX Patrick Dougherty, CFP Dougherty WealthManagement LLCDallas, TX Steve Holdsworth,CFP , CLULegacy WealthManagement Inc.Memphis, TN Jeff Johnson, CFP Executive WealthManagementLincoln, NE Alice Lowenstein, CFP Litman/Gregory AssetManagement LLCOrinda, CA John McDermott, Ph.D.Fairfield University/Symmetry PartnersFairfield, CT Lee McGowan, CFP TFC FinancialManagementBoston, MA Shikha Mittra, CFP ,CMFC, CRPSASNA RetiresmartConsulting LLCPrinceton, NJ Mark L. Prendergast,CPA, CFP Inspired FinancialHuntington Beach, CA Clark D. Randall,CFP , CLU, AEPLincoln Financial AdvisorsDallas, TX Sandeep Singh, Ph.D.,CFA, CCMSUNY BrockportBrockport, NY William J. Supper, CFP Merrill Lynch & CompanyNew York, NYMoving the NeedleAt the Journal of Financial Planning, we’re always keenly interested in contributed articlesthat “move the needle on the dial”—in other words, advance the profession in somesignificant way. It’s not always easy to determine which contributions will do that. Ultimately, it is up to you to decide which articles excite you and have a positive effect on the wayyou practice.This issue of the Journal features a contribution we feel has the potential to be very influential. It’s called “Finding the Planning in Financial Planning,” and it was written by David Yeske,a former FPA chair. Yeske has contributed a great deal of thoughtful work to the body of knowledge of the financial planning profession, some of it in partnership with his wife, Elissa Buie.And having been a big part of that profession for many years, he knows his history.His paper is seasoned with references to well-known contributions to the profession—worksby other thought leaders who have “moved the dial,” such as Dick Wagner, Lynn Hopewell, JonGuyton, George Kinder, Rick Kahler, Roy Diliberto, Deanna Sharpe, Carol Anderson, BillAnthes, Gobind Daryanani, and others.One of the works Yeske cites is a popular article written by Guy Cumbie, himself a formerFPA chair. In 2002, Cumbie wrote in Accounting Today of an “embarrassingly gaping hole in thepersonal financial planning profession’s body of knowledge in the area of planning.” I was working for CFP Board in Denver when Cumbie’s article came out, and I remember very well what astir is caused. Cumbie’s article was applauded as a wake-up call in some quarters, criticized byothers who believed that successful client outcomes provided all the evidence needed that planning was being done and done well.We all use terms that we take for granted. For example, we talk about “art,” but are usually ata loss to describe what a person can do to become artistic. Oh, we can talk about outcomes—painting, sculpting, writing, designing—but it’s much harder to describe the steps a person musttake to turn his or her work into true art. Often, we throw our hands in the air and quip that wedon’t know what art is, but we know it when we see it.Not content to take “financial planning” for granted, Yeske has written a paper thatattempts to break down planning into five, specific strategy-making modes. He suggests thatthese modes can be studied empirically, measured in terms of their effect on client trust andrelationship commitment, and used to assess whether planners possess the competenciesneeded to be successful.I can’t tell you with certainty that this article will change the way you do financial planning.All I can say with confidence is that this is an article worthy of your attention and careful consideration. It’s an article that merits discussion when you meet with colleagues at work, at FPADenver 2010, and on the FPA LinkedIn site.Lance RitchlinEditor Jimmy J. Williams,CPA/PFSCompass CapitalManagementMcAlester, OK Walt Woerheide,Ph.D., CFP The American CollegeBryn Mawr, PAwww.FPAjournal.orgSEPTEMBER 2010Electronic copy available at: http://ssrn.com/abstract 1612507 Journal of Financial Planning11

ContributionsYESKEFinding the Planning in FinancialPlanningby David B. Yeske, D.B.A., CFP David B. Yeske, D.B.A., CFP , holds an appointment asDistinguished Adjunct Professor in Golden GateExecutive SummaryUniversity’s Ageno School of Business and is a managingdirector of Yeske Buie, a wealth management firm withoffices in Vienna, Virginia, and San Francisco, California.The research reported in this article is basedon Yeske’s doctoral dissertation, the full text of which canbe found at http://ssrn.com/author 646759.After four decades of growth anddevelopment, the financial planning profession is still without anoverarching framework for organizing andtesting the strategy-making activities of itspractitioners. The profession lacks, inother words, a theory for where planningcomes from. This observation is not newand has been shared by a growing numberof academics and practitioners over thepast decade. In 2002, Guy Cumbie, thenchair of the Financial Planning Association(FPA), bemoaned the “embarrassinglygaping hole in the personal financial planning profession’s body of knowledge in thearea of planning” (Accounting Today, 2002).Warschauer, meanwhile, has observed that“we have poor theory to guide the practiceof financial planning” (2002), while BlackJr. et al point out that “the PFP field hasevolved largely devoid of a theoreticalfoundation” (2002). This research is meantto begin to address this gap by developingan integrating framework for the strategymaking activities of financial planners andthen empirically testing that model againstappropriate measures of success.But how can we measure success?40Journal of Financial Planning After four decades, the financial planningprofession still lacks an overarchingframework for organizing and testingthe strategy-making (that is, “planning”)activities of its practitioners. An integrating framework is proposedthat consists of five modes of strategymaking: planner-driven, data-driven,policy-driven, relationship-driven, andclient-driven. Each of these five modes represents adifferent relative role for the plannerand client in the planning process. Themodes also fall along a parallel dimension of planning versus emergence. The proposed model is tested againstA long-standing marketing message of theFinancial Planning Association declares that“Planning pays off.” But how do we knowthat’s true, and how might we measure it?Like many other professional services, afterall, financial planning possesses high credence properties (Sharma and Patterson,1999), which means that the quality of theservice is difficult to judge, even after it hasbeen delivered. This is easy to see when youconsider that financial planners are routinely asked to develop strategies for attaining goals that are many years or evendecades into the future. So, if we cannotwait decades to see whether a particularmeasures of client trust and relationship commitment, and the policydriven mode is found to be the mostpowerful predictor of both. Client complexity is also analyzed as apredictor of client trust and commitment, and it is found that trust and commitment are inversely related to thecomplexity of a client’s circumstances. Finally, a factor analysis of plannerstrategy-making activities shows thatplanners in independent firms tend tofavor data- and policy-driven approachesand those practicing at large financialservices firms tend to be more dominant in the planner-driven mode.approach to planning has “paid off,” whatcan we observe in the present that mightprovide us with a more immediate measure?The answer that has emerged over the lastdozen years through a series of research initiatives within the financial planning profession is centered on measures of client trustand relationship commitment.Client trust and commitment are attractive variables on which to focus, as anything that maximizes a client’s trust in thefinancial planner and commitment to thefinancial planning relationship can leaddirectly to positive outcomes. These includehigh acquiescence, a low propensity toSEPTEMBER 2010Electronic copy available at: http://ssrn.com/abstract 1612507www.FPAjournal.org

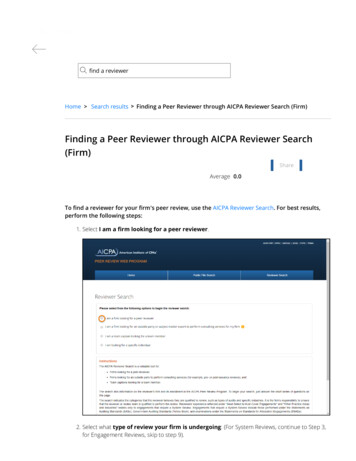

ContributionsYESKEleave, a high degree of cooperation, andfunctional conflict (that is, the ability tomaintain a highly functional relationshipeven when conflicts arise) (Hunt andMorgan, 1994). These qualities tend to leadto long-lasting relationships and are associated with greater client openness in disclosing personal and financial information,greater cooperation in implementing planning recommendations, and a greaterpropensity to make referrals (Sharpe andAnderson, 2008).The concept of client trust and commitment as key mediating variables first arosein the relationship marketing literature,notably in the work of Morgan and Hunt(1994), who attempted to identify theantecedents of trust and commitment.Among their proposed predictors wererelationship termination costs (that is,switching costs), relationship benefits,shared values, communication, and opportunistic behavior.Christiansen and DeVaney (1998) subsequently applied this same model to financial planners and found that relationshiptermination costs, relationship benefits,and shared values were all strong predictors of commitment. Shared values, communication, and opportunistic behavior,meanwhile, were strongly predictive oftrust, which itself was a strong predictor ofcommitment. Communication was thesingle most powerful antecedent to trustand commitment, acting directly on trustand through trust on commitment.Sharma and Patterson (1999) alsoaddressed the question of whichantecedents most influenced client trustand commitment within the financial planning relationship. As noted, these authorsobserved that financial planning is a “highcredence” service that unfolds over time,leaving clients hard pressed to judge thequality of the advice in the presentmoment. They go on to explain:After all, if clients have trouble evaluating outcomes, then it seems reasonable that interactions (“how” the service is delivered) and all forms ofwww.FPAjournal.orgFigureFigure 11::AntecedentsAntecedents toto TTrustrust sen & DDeVaneyeVaneynd CChristiansen & DeVaney (1998)Relationship Switching CostsRelationship BenefitsCommitmentShared ValuesCommunicationTrustOpportunistic Behavior2:FigureFigure 2:TechnicalTeechnical Quality,Quality, FunctionalFunctional Quality,Quality, and ssSharma & Patterson (1999)Relationship CommitmentCommunication EffectivenessFunctional QualityTrustTechnical Qualitycommunication will take on added significance as clients seek to minimizedissonance and uncertainty about theadviser they have chosen.The authors explored the links betweenperceptions of technical quality (what wasbeing delivered), functional quality (how itwas being delivered), and communicationeffectiveness on the one hand, and relationship commitment on the other. Theyfound that a client’s perception of the technical and functional quality of the planner’sadvice was positively correlated with theclient’s level of trust in the planner. Higherlevels of trust, in turn, were associatedwith higher levels of commitment to therelationship. Communication effectiveness,meanwhile, acted directly on trust andcommitment and also indirectly throughits effect on perceived technical qualityand functional quality.Sharma and Patterson (2000) laterreturned to the examination of theantecedents of relationship commitment,examining the role of trust and a new variable: satisfaction. They tested the effect oftrust and satisfaction on commitment inlight of three contingencies: switchingcosts, the availability of attractive alternatives, and prior experience. They foundthat trust had the greatest effect on commitment when switching costs were high,perceived alternatives were low, and/orprior experience was low. In situations inwhich switching costs were low, perceivedalternatives were high and/or prior experience was high, satisfaction was the dominant antecedent to commitment. Thiswork proved illuminating when unexpected results turned up in the presentresearch, as will be described later.Sharpe, Anderson, White, Galvan, andSiesta (2007) extended the work ofSEPTEMBER 2010 Journal of Financial Planning41

ContributionsYESKEChristiansen and DeVaney (1998) andSharma and Patterson (1999, 2000) byfocusing solely on the communicationdimension. They derived the communication elements to be examined from thelife planning literature and organized itinto three dimensions: communicationtasks, communication skills, and communication topics. They found that the following were most highly valued by financial planning clients:Communication tasks Systematic process to clarify goals andvalues Explaining how advice reflects goalsand valuesCommunication skills Eye contact, body language, verbalpacing Facilitating difficult conversationsabout moneyCommunication topics Client values and quality of life Initiating conversations about lifechangesIn discussing the virtues of the life planning approach to client interactions, theauthors state: “Using a life planninglargest of these is the “quantitative tools”cluster. To a significant degree, this clusterrepresents the adaptation of traditional toolsof financial and economic analysis to individuals and families. These offerings includesuch things as Warschauer’s (1981) uniformrisk-liquidity balance sheet and Hopewell’s(1997) introduction of stochastic modeling,especially Monte Carlo analysis. FollowingHopewell, stochastic modeling became aregular topic in the literature, including further forays by Kautt and Hopewell (2000)and Kautt and Wieland (2001). Other examples of this cluster are scenario planning(Ellis, Feinstein, and Stearns, 2000), discreteevent simulation (Houle, 2004), and sensitivity simulations (Daryanani, 2002).A second thread running through thefinancial planning literature involvesprocess-oriented techniques. These generally take the form of decision rules and aremeant to provide a framework for rapiddecision-making in the face of changingexternal circumstances. As elsewhere, thisarea has seen the direct adoption by financial planners of tools and techniques developed in other fields, including, for example, the use of investment policies (Booneand Lubitz, 1992, 2004).Another example is policybased financial planning, anIt is important for clients to seeidea first proposed by Hallmanand Rosenbloom (1987) andtheir own values, beliefs, and goalslater developed by Yeske andreflected in the policies if they are to Buie (2006). Policy-basedfinancial planning involves thefully embrace them.development of statements(policies) that capture whatclients intend to do and howthey intend to do it in termsnotlimitedtothe present circumstances.perspective, the planner’s role shifts frommaximizing a client’s investment returns to Policies are meant to be enduring touchstones that keep clients anchored to anhelping the client utilize financialappropriate course of action, especially inresources to construct a meaningful life.”turbulent environments. As such, it isimportant for clients to see their ownDeveloping the Model: Themes from thevalues, beliefs, and goals reflected in theFinancial Planning Literaturepolicies if they are to fully embrace them.Also found within this process-orientedAs one surveys the financial planning literature of the past 40 years, three major themes cluster are concepts such as opportunisticrebalancing (Daryanani, 2008) and safeor clusters naturally emerge. The oldest and“”42Journal of Financial Planning SEPTEMBER 2010withdrawal rates, especially thoseapproaches that incorporate active decisionrules or policies (Guyton, 2004; Guytonand Klinger, 2006). As with policy-basedfinancial planning, and unlike approachesinvolving static withdrawal rates, the decision rules developed by Guyton andKlinger are most efficacious with the activeunderstanding and participation of clients.The third major theme within the financial planning literature directly addressesthis need for a deeper understanding ofclients’ beliefs, values, and motivations.This area has been variously called interiorfinance, financial life planning, and lifeplanning. Examples include the work ofWagner (2002) in the area of interiorfinance (a term he coined), Kinder’s(2000) Seven Stages of Money Maturity,Kinder and Galvan’s (2005) EVOKEsystem, and Kahler’s (2005) financial integration framework. Carol Anderson andMitch Anthony, meanwhile, coined theterm “financial life planning,” and muchwork has been done under that label(Diliberto and Anthony, 2003; Anthony,2005; Diliberto, 2006).One notable aspect of the work beingdone on the interior dimension is that it isnot limited to offering new perspectivesbut has generated many specific tools andtechniques for improving the discoveryprocess. On this point, it’s worth recallingthat one of the key findings of the Sharpe,Anderson, White, Galvan, and Siesta(2007) research was that clients place ahigh value on a “systematic process forclarifying goals and values.”When viewed as a whole then, much ofthe financial planning literature seems tonaturally fall into the following categories: Quantitative tools Process-orientation Interior dimensionDeveloping the Model: Perspectives fromStrategic ManagementNo overarching framework has been proposed for how the three major themes foundwithin the financial planning literaturewww.FPAjournal.org

YESKEmight be meaningfully incorporated into acomplete theory of strategy-making byfinancial planners. A review of the strategic planning literature, however, offereduseful perspectives for organizing thesethree lines of development.Two themes that emerge explicitly fromthe strategic management literature andimplicitly from the financial planning literature involve the concepts of rationalityand involvement. Rationality refers to thedegree to which planning can be formalized, quantified, and controlled, whileinvolvement refers to the relative rolesplayed by the participants in the planningprocess. In the case of strategic management, the two groups that define thedegree of involvement or the roles dimension are top managers and all other organizational participants (Hart and Banbury,1994). In the financial planning context,relative involvement or roles are dividedbetween the financial planner and theclient. The rationality dimension can alsobe thought of as the role of planning versusemergence in the development of strategies. This refers to the dynamic tensionbetween classi

RTD Financial Advisors Inc. Atlanta, GA Janet A. Stanzak, CFP Financial Empowerment LLC Bloomington, MN Karin Maloney Stifler, CFP True Weal