Transcription

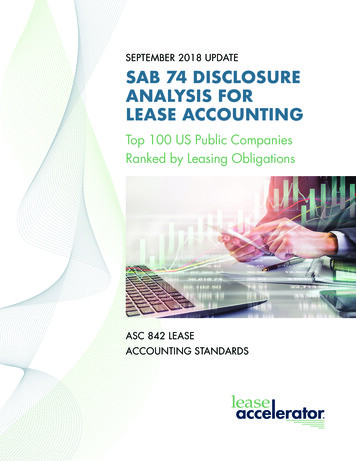

SEPTEMBER 2018 UPDATESAB 74 DISCLOSUREANALYSIS FORLEASE ACCOUNTINGTop 100 US Public CompaniesRanked by Leasing ObligationsASC 842 LEASEACCOUNTING STANDARDS

TABLE OF CONTENTSExecutive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3SAB 74 Disclosures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3Key Findings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Detailed Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Balance Sheet Impacts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Income Statement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Cash Flow Statement. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Early Adoption. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Transition Method. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7Practical Expedients. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9Implementation Progress. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10Project Team. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Software Evaluation And Selection. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13Policies & Controls. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Lease Accounting Change . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15SAB 74 Disclosures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Additional References . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Top 100 Us Companies Ranked By Leasing Obligations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 2010-2018 LeaseAccelerator, Inc. All rights reserved. This document is the copyrighted work of LeaseAccelerator, Inc.

EXECUTIVE SUMMARYSAB 74 DISCLOSURESAs the implementation deadlines for ASC 842 grow closer, public filers will be required to include a discussionof the potential future impacts to their financial statements from the new lease accounting standards. SEC StaffAccounting Bulletin Topic 11.M (SAB 74) requires SEC filers to disclose the effects of accounting standards thathave been announced but not yet adopted. The guidance from the bulletin encourages registrants to considerdisclosing: A brief description of the new standard, the date that adoption is required, and the date that the registrant plansto adopt, if earlier. A discussion of the methods of adoption allowed by the standard and the method expected to be utilized by theregistrant, if determined. A discussion of the impact that adoption of the standard is expected to have on the financial statements of theregistrant, unless not known or reasonably estimable. In that case, a statement to that effect may be made.Disclosure of the potential impact of other significant matters that the registrant believes might result from theadoption of the standard (such as technical violations of debt covenant agreements, planned or intended changesin business practices, etc.) is encouraged.In an effort to assist the industry with accelerated adoption of the new lease accounting standards, LeaseAcceleratorcompiled 100 examples of SAB 74 disclosures from SEC registrants over the past year. We focused on the top 100US public companies as ranked by the total leasing obligations tabularized in the footnotes of annual filings. Thesource of the data was 10-Q and 10-K filings submitted between October 1st, 2017 and September 7th, 2018TOP 100 US PUBLIC COMPANIES RANKED BY LEASING OBLIGATIONSSEPTEMBER 2018 UPDATE3

KEY FINDINGSEarly AdoptionWith the revenue recognition standard (ASC 606) a number of companies including Alphabet, Microsoft, GeneralDynamics, Ford, and Raytheon were early adopters. Only two of the 100 companies analyzed, Microsoft andTarget, adopted the standards early. No other companies stated their intention to early adopt.Transition ApproachA new optional transition method was approved in July 2018. Some companies who filed after that datereferenced the new transition method in their disclosures, either stating their intention to elect the new method orstating that they were still evaluating whether or not they chose to elect the new method. As of the time of this study,14% of the companies stated they would choose the new method, while 9% stated they were undecided.Material Impacts to Balance SheetsAs expected, the new right-of-use assets and liabilities being added to balance sheets is expected to be the mostmaterial impact to financial statements. 83% of the Top 100 reported that there will be a material impact resultingfrom the transfer of most right-of-use assets and liabilities on to corporate balance sheets. Another 14% are stillanalyzing the potential impacts of the new standard.Quantitative ImpactsCompanies are still in the process of estimating the definitive size of their leasing portfolios under ASC 842. Only19% provided quantitative estimates of the material impact to the balance sheet, which ranged from 1.3 billion topotentially 18 billion.Limited Impacts to Income Statement and Cash Flow Statements34% of the Top 100 reported that there would not be a material impact to their income statement from ASC 842.Another 61% are still analyzing the impacts. 28% of the Top 100 reported there would be no impact to their cashflow statements and 63% are still analyzing the impact.Implementation ProgressThe level of information disclosed about the progress of implementation efforts has increased since the firstpublication of this report, but is still relatively limited by most filers. Of the companies we analyzed, only 37% statedthey are evaluating, developing, or implementing new policies and controls to support the standard. Similarly,amongst the filers we reviewed, only 39% stated they are evaluating, have selected, are implementing, or havefinished implementing a lease accounting software application. Only 18% indicated that a project team had beenformed to address the new standard.4 SEPTEMBER 2018 UPDATESAB 74 DISCLOSURE ANALYSIS FOR LEASE ACCOUNTING (ASC 842)

SAB 74 DISCLOSURE ANALYSIS FOR LEASEACCOUNTING (ASC 842)BALANCE SHEET IMPACTSBalance Sheet Impacts will be MaterialAs expected, the most material impact to financial statements cited by most filers is the new right-of-use assets andliabilities being added to the balance sheets. 83% of the Top 100 reported that there will be a material impact resultingfrom the transfer of most right-of-use assets and lease liabilities onto corporate balance sheets. Another 14% are stillanalyzing the potential impacts of the new standard.Bank of America and UnitedHealth Group were the only two companies in our sample set that indicated that the impactwould not be material. While no other health care insurance companies were analyzed in this study, other financialinstitutions, such as JPMorgan ( 10B) and Citigroup ( 5B), did indicate that the balance sheet impact would bematerial, so there does not appear to be an industry-wide trend for commercial banks.Companies are still in the process of estimating the definitive size of their leasing portfolios under ASC 842. Only19% provided quantitative estimates of the material impact to the balance sheet, which ranged from 1.3 billion topotentially 18 billion.BALANCE SHEET IMPACTSBALANCE SHEET IMPACTSNot StatedNot Stated1% 1%Still EvaluatingStill Evaluating14%14%MaterialImpactMaterial Impact83%83%Not MaterialNot Material2% 2%TOP 100 US PUBLIC COMPANIES RANKED BY LEASING OBLIGATIONSSEPTEMBER 2018 UPDATE5

EXAMPLES OF DISCLOSURE COMMENTS RELATED TO BALANCE SHEETSSEC REGISTRANTEXCERPT OF DISCLOSUREAppleWhile the Company is currently evaluating the impact of adopting ASU 2016-02, based onthe lease portfolio as of June 30, 2018, the Company anticipates recording lease assets andliabilities of approximately 8.8 billion on its Condensed Consolidated Balance Sheets, withno material impact to its Condensed Consolidated Statements of Operations. However, theultimate impact of adopting ASU 2016-02 will depend on the Company’s lease portfolio asof the adoption date.JPMorgan Chase& Co.The Firm expects to recognize a lease liability and a corresponding right-of-use asset(at their present value) related to predominantly all of the 10 billion of future minimumpayments required under operating leases as disclosed in Note 28 of JPMorgan Chase’s2017 Annual Report. However, the population of contracts subject to balance sheetrecognition and their initial measurement remains under evaluation; final financial statementimpacts will depend on the lease portfolio at the time of adoption.Bank of AmericaCorp.The effect of the adoption will depend on the lease portfolio at the time of transition and thetransition options ultimately available; however, the Corporation does not expect the newaccounting standard to have a material impact on its consolidated financial position, results ofoperations or disclosures in the Notes to the Consolidated Financial Statements.Wal-Mart StoresAlthough management continues to evaluate the effect to the Company’s CondensedConsolidated Financial Statements and disclosures, management currently estimates totalassets and liabilities will increase approximately 14 billion to 18 billion upon adoption,before considering deferred taxes. This estimate could change as the Company continuesto progress with implementation and will also fluctuate based on the lease portfolio anddiscount rates as of the adoption date. Management does not expect a material impact tothe Company’s Condensed Consolidated Statements of Income or Cash Flows.INCOME STATEMENTUnder ASC 842, there is expected to be little impact to the income statement. Operating leases will be presentedon the same line-item on the income statement, the same as under the current standard, ASC 840. For financeleases, which replace capital leases under ASC 840, the interest and amortization will still be presented separately.As a result, we expect few of the remaining 61% still evaluating and the 4% that did not comment on the incomestatement impacts to find a material impact to the income statement.CASH FLOW STATEMENT63% of companies are still evaluating the impact to the cash flow statement and 28% have stated that there will beno impact to the cash flow statement.6 SEPTEMBER 2018 UPDATESAB 74 DISCLOSURE ANALYSIS FOR LEASE ACCOUNTING (ASC 842)

EARLY ADOPTIONWith the revenue recognition standard (ASC 606) a number of companies including Alphabet, Microsoft, GeneralDynamics, Ford, and Raytheon were early adopters. The lease accounting standard has very few early adoptersthus far. Only two of the 100 companies analyzed, Microsoft and Target, have early adopted.TRANSITION METHODWith other recent accounting changes, such as revenue recognition, much of the focus for SAB 74 disclosures wason the transition approach being adopted. However, until recently, only a modified retrospective approach wasallowed under ASC 842. The modified retrospective method would have required companies to not only transitionat the date of adoption, but also provide reports of their lease data under ASC 842 from the earliest comparativeperiod to the effective date. For example, companies who will adopt on January 1, 2019 would have beenrequired to report their lease data from January 1, 2017 to January 1, 2019 under both ASC 840 and ASC 842.However, in July 2018, FASB voted to approve a simpler transition method that eliminates the need for comparativereporting. 14% of companies stated their intention to elect this approach. 9% were still evaluating the approach.However, no companies stated that they would not select the alternate approach. We anticipate that as the nextround of disclosures are released, the number of companies selecting the modified transition method will increase,as the approach reduces the implementation burden for corporate accounting organizations.OPTIONAL TRANSITION METHOD90%80%70%60%50%40%30%20%10%0%Will SelectUndecidedTOP 100 US PUBLIC COMPANIES RANKED BY LEASING OBLIGATIONSNo CommentsSEPTEMBER 2018 UPDATE7

EXAMPLES OF DISCLOSURE COMMENTS RELATED TO THE NEW TRANSITION METHODSEC REGISTRANT EXCERPT OF DISCLOSUREHewlett PackardEnterpriseThe Company is required to adopt the guidance in the first quarter of fiscal 2020 and earlyadoption is permitted. In addition, the FASB provided a practical expedient transition methodto adopt the new lease requirements by allowing companies to recognize a cumulative-effectadjustment to the opening balance of retained earnings in the period of adoption that wouldenable the Company to not provide comparative period financial statements. Instead, theCompany would apply the transition provisions at its effective date. The Company is currentlyevaluating the timing and the impact of these amendments on its Condensed ConsolidatedFinancial Statements.Tractor SupplyThis guidance is required to be applied, at the Company’s election, either using a (1) modifiedretrospective approach for all leases existing at, or entered into after, the beginning of the earliestcomparative period presented, or (2) cumulative-effect approach for all leases existing at, orentered into, after the effective date. The Company expects to apply the guidance using thecumulative-effect approach, thereby applying the new guidance at the effective date, withoutadjusting the comparative periods and, if necessary, recognizing a cumulative-effect adjustmentto the opening balance of retained earnings in the period of adoption.AndeavorUnder this optional transition method, we would recognize a cumulative-effect adjustment tothe opening balance of retained earnings in the period of adoption. We expect to elect theoptional transition method.Michaels Cos.In July 2018, the FASB issued ASU 2018-11, “Leases (Topic 842): Targeted Improvements”which provided an additional transition option that allows companies to continue applyingthe guidance under the current lease standard in the comparative periods presented inthe consolidated financial statements. Companies that elect this option would record acumulative-effect adjustment to the opening balance of retained earnings on the date ofadoption. We are in the process of determining which transition method to apply.8 SEPTEMBER 2018 UPDATESAB 74 DISCLOSURE ANALYSIS FOR LEASE ACCOUNTING (ASC 842)

PRACTICAL EXPEDIENTSAmongst our sample set, 13% of companies indicated an intention to elect some or all of the practical expedientsavailable under ASC 842, while another 13% were still evaluating all of the available practical expedients.However, most did not provide any commentary.PRACTICAL EXPEDIENTS80%70%60%50%40%30%20%10%0%Evalua ngSelectedNo CommentsEXAMPLES OF DISCLOSURE COMMENTS RELATED TO PRACTICAL EXPEDIENTSSEC REGISTRANT EXCERPT OF DISCLOSURETargetThe modified retrospective approach provides a method for recording existing leases at adoptionand in comparative periods that approximates the results of a full retrospective approach. Inaddition, we elected the package of practical expedients permitted under the transition guidancewithin the new standard, which among other things, allowed us to carry forward the historicallease classification. We also elected the practical expedient related to land easements, allowingus to carry forward our accounting treatment for land easements on existing agreements. Inaddition, we elected the hindsight practical expedient to determine the lease term for existingleases. Our election of the hindsight practical expedient resulted in the shortening of lease termsfor certain existing leases and the useful lives of corresponding leasehold improvements. In ourapplication of hindsight, we evaluated the performance of the leased stores and the associatedmarkets in relation to our overall real estate strategies, which resulted in the determination thatmost renewal options would not be reasonably certain in determining the expected lease term.TOP 100 US PUBLIC COMPANIES RANKED BY LEASING OBLIGATIONSSEPTEMBER 2018 UPDATE9

CenturyLinkThe modified retrospective approach includes a number of optional practical expedients thatwe may elect to apply. On January 25, 2018, the FASB issued ASU 2018-01, “Leases: LandEasement Practical Expedient for Transition to ASU 2016-02” (“ASU 2018-01”). ASU 2018-01permits reporting companies to elect to forego reassessments of land easements that exist orexpire before the entity’s adoption of ASU 2016-02 and that were not previously accounted foras leases. We plan to adopt ASU 2018-01 at the same time we adopt ASU 2016-02. On July30, 2018, the FASB issued ASU 2018-11, “Leases: Targeted Improvements”. (“ASU 2018-11”)provides entities with an additional (and optional) transition method to adopt the new leasesstandard. Under this new transition method, an entity initially applies the new leases standardat the adoption date and recognizes a cumulative-effect adjustment to the opening balance ofretained earnings in the period of adoption. We have not yet determined whether we will usethe newly permitted adoption method.DaVitaThe Company expects to adopt this ASU on January 1, 2019 and is currently planningon electing the package of practical expedients to not reassess prior conclusions relatedto contracts containing leases, lease classification and initial direct costs. The Companycontinues to evaluate the transition options and other practical expedients available underthe guidance as well as the effect that the implementation of this guidance will have on itsconsolidated financial statements, related disclosures and controls, and ongoing businesspolicies and processes.IMPLEMENTATION PROGRESSThe level of information disclosed about the progress of implementation efforts is still relatively limited by most filers.A significant work effort will be required to comply with the new lease accounting standards by most companieswith portfolios in excess of 100M. Changes will be required for accounting systems, business processes, andfinancial controls. A cross-functional project team will need to be fo

6 SEPTEMBER 2018 UPDATE SAB 74 DISCLOSURE ANALYSIS FOR LEASE ACCOUNTING (ASC 842) EXAMPLES OF DISCLOSURE COMMENTS RELATED TO BALANCE SHEETS SEC REGISTRANT EXCERPT OF DISCLOSURE Apple While the Company is currently evaluating the impact of adopting ASU 2016-02, based on the lease