Transcription

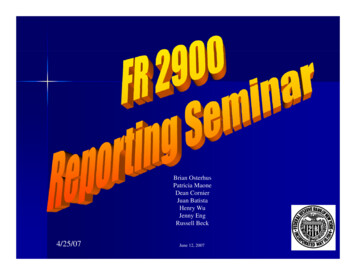

Brian OsterhusPatricia MaoneDean CornierJuan BatistaHenry WuJenny EngRussell Beck4/25/07June 12, 20071

Purpose andGeneral InstructionsB i OsterhusBrianOt h2

A dAgenda Purpose and General Instructions Annual FR 2900 Items Deposits vs. Borrowings TTransactionti AccountsAt Nontransaction Accounts and Vault Cash Schedules AA, BB and CC Other FR 2900 Reportingpg Issues ReserveCalc3

What is the FR 2900? The FR 2900 is a weekly/quarterly reportreflectingfl ti dailyd il datad t (Tuesday(T d throughthhMonday) where Depository Institutions (DIs)reportt “sources“off funds”f d” Amounts reported on the FR 2900 include:––Deposits held by the DIOther fundsf nds (borrowings(borro ings obtained fromnon--exempt entities)non4

The Purpose of the FR 2900 The FR 2900 has two pprimaryy ppurposes:pa)The calculation of money stockb)The calculation of reserve requirements5

What is Moneyy Stock(or Money Supply)? Money supply is the total amount ofmoney in the economy Two basic measures of moneypublishedbli h d byb theh FederalF d l ReserveR6

What is Moneyy Stock(or Money Supply)?M1 - 1.4 trillionNarrowest and most liquid measure of money,comprised of:– Currency– Travelers checks– Demand deposits– Other transaction accounts (ATS, NOW accounts)7

What is Moneyy Stock(or Money Supply)?M2 - 7.1 trillionA bbroaderd measure. IIncludes,l din addition to M1:– Small denomination time deposits(less than 100,000)– Savings deposits, including MMDAs and nonnon-institutionalmoney market mutual funds (MMMFs)8

What is Moneyy Stock(or Money Supply)? Th FR 2900 isThei theh primaryisource off thishiinformation, and is used to construct moneystock weekly The aggregate data are released each Thursdayafternoon to the public in the Board’s H.6 release9

What are Reserve Requirements? Reserve requirements are a percentage of adepository institution’s (DI’s) deposits (or fractionalreserves) that must be held either as cash in the“vault” of the DI, on deposit at the Federal ReserveBank, or at a correspondent bank RReserverequirementsit are one off theth toolst l usedd bybthe Federal Reserve as a means to conductmonetary policy10

What are Reserve Requirements? Reserves can be added to or removed fromthe banking system by changing the reserveratio applied to reservable liabilities Other Monetary Policy tools––System Open Market OperationsDiscount Window Lending11

Who Must Report? U. S. branches and agencies of foreign banks,and banking Edge and Agreement corporations,regardless of sizesize, must report the FR 2900weekly12

Who Must Report? U. S. branches and agencies of a foreign bankllocatedd ini theh same state andd withini hi theh sameFederal Reserve District are required to submita consolidatedlid d report off depositsdi to theh FederalF d lReserve Bank in the District in which theyoperate (excluding( l di any balancesb loff theh IBF)13

Reportingg of Edgegand Agreement Corporations When preparing the FR 2900, deposits of offices of ab ki Edgebankingd or Agreement corporationi shouldh ld notbe aggregated with related U.S. branches andagencies of foreign banks or commercial banks Banking Edge and Agreement corporations arerequired to file separate FR 2900 reports, regardlessof size14

September 2007 DepositReporting Requirements Applies to all institutions except for U.S. branches andagencies of foreign banks and Edge or AgreementcorporationsExemptN transactionNeti accounts 8.5 millionNon-reportersTotal deposits 8.5 millionAnnualReportersTotal deposits 8.5 millionNon-exemptN transactionNeti accounts 8.5 million, OR M2 deposits 1.163 billion reduced reportingli itlimitQuarterlyWeeklyReportersReportersM2 deposits M2 deposits 207.7 million 207.7 million15

Who Must Report?M2 Deposits Sum of transaction accounts, savingsdeposits and small time deposits16

Who Must Report? The Federal Reserve will continue to screeninstitutions, and inform each institutioneligible for reduced reporting17

Who Must Report? FR 2900 weekly: commercial banks, savingsbanks, savings and loan associations and creditunions– M2 deposits above the “nonexempt deposit cutoff” and “nettransaction accounts” above the indexed level, or– M2 deposits above the “reduced reporting limit”, regardlessof the level of “net transaction accounts”18

Who Must Report? FR 2900 quarterly: commercial banks,savings banks, savings and loanassociations and credit unions– M2 deposits below the “nonexempt depositcutoff”, and “net transaction accounts” above theindexed level19

Who Must Report? FR 2910a: commercial banks, savingsb k savingsbanks,iandd loanlassociationsi ianddcredit unions–M2 deposits between the “exemption amount” andbelow the “reduced reportingpg limit”, and “nettransaction accounts” below the indexed level20

FR 2900 vs. FFIEC 002Definitional Differences Consolidation of branches and agencies ofthe same foreign (direct) parent bankFR 2900––U.S. branches and agencies in the same Federal ReserveDistrict and state must submit a consolidated FR 2900 report21

FR 2900 vs. FFIEC 002Definitional Differences Consolidation of branches and agencies of thesame foreignf i (direct)(di ) parent bankb kFFIEC 002– U.S. branches and agencies in the same Federal Reserve District andstate are not required to consolidate, but may submit a consolidatedFFIEC 002 provided:4Theoffices are located in the same city and insured anduninsured branches are not combined22

FR 2900 vs. FFIEC 031/041Definitional Differences Consolidation of domestic branchesand subsidiariesFR 2900– Head office and all branches in the 50 states plus District ofColumbia– Subsidiaries– Branches on military facilities, wherever located23

FR 2900 vs. FFIEC 031/041Definitional Differences Consolidation of domestic branches andsubsidiariesFFIEC 031/041– Head office and all branches in the 50 states plusDistrict of Columbia– Majority owned, significant subsidiaries, including domesticcommerciali l banks,b k savingsibanks,b k savingsiandd loanlassociationsi i– Branches on military facilities, wherever located24

FR 2900 vs. FFIEC 002/031/041Definitional Differences “U.S.”FR 2900– 50states plus District of ColumbiaFFIEC 002/031/041–50 states plus District of Columbia–Puerto Rico and U.S. territories and possessions25

Where and When to Submit? The reportingpg week is a seven dayy pperiod that beginsgTuesday and ends the following Monday. Th reports are dueThed to theh FederalF d l ReserveRbyb thehWednesday following the Monday asas-of date viaelectronic submission,submission or signed hard copy sent bymessenger or fax. (Please do not submit the samereportp via more than one method).)26

WhereWh andd WhenWh tot Submit?S b it? Electronic submissions of these reports isavailable via the Internet using the IESUBapplication27

Close of Business The term “close of business” refers to the cutcut-off time for posting transactions to the GeneralLedger (G/L) for that day. The time should be reasonable and appliedconsistently.i t tl28

Close of Business SelectiveSe ect ve postingpost g iss prohibitedp o b ted–A debit or credit cannot be made without theoffsetting transaction being posted; and–All transactions occurring during the period oftime the books are open must be posted29

Back--valuing vs.Backvs Misposting The FR 2900 should reflect only the G/L balanceas off theth “close“ loff business”b i” eachh dayd Balances should be reflected on the FR 2900based on:– When an institution has received or sent funds and– The institution has a liability to make payment to a customer/thirdparty30

Back--valuing vs.Backvs Misposting Balances should be reported as of “closeclose ofbusiness”, regardless of when the transactionshould have occurred.31

Back--valuing vs.Backvs Misposting An institution is allowed to backback-value only inth case off a clericalthel i l bookkeepingb kk i error. The FR 2900 may be adjusted to moreaccurately reflect the transaction as it shouldhave been recorded.32

Back--valuing vs.Backvs Misposting For significant postpost-closing adjustmentsadjustments, DIsshould review their reports to determinewhether revisions are required for additionalas--of dates.as33

Back--valuingBackg vs. MispostingpgExamplesQuestion 1On day 1, Bank R receives a 10 million demanddeposit for the credit of Corporation A. However,due to a misposting error, Corporation A wascredited 1 million. On day 2, the error wasdiscovered.How should this be reported ?34

Back--valuingBackg vs. MispostinggExamplesAnswerWhen the error is discovered on day 2, Bank Rshould revise the 1 million misposted on day 1 toreflect the 10 million deposit from CorporationA received on day 1. Thus, 10 million shouldb reportedd inbei Linei A.1.c on bothb h days.d35

Back--valuingBackg vs. MispostinggExamplesQuestion 2On day 1, Bank R borrows 5 million fromBank S. However,, Bank S erroneouslyy sends 15 million.How should these funds be reported ?36

Back--valuing vs. MispostingBackExamplesAnswerOn day 1, Bank R does not report the 5g it receives, on the FR 2900.million borrowingThe 10 million Bank R receives in errorpin Line A.1.a as “Due toshould be reportedbanks”.37

Back--valuingBackg vs. MispostingpgExamplesAnswerBank R should exclude the 10 million sentin error from Line A.1.aA 1 a when those fundsare returned to Bank S.38

Reporting ofDeposits in Foreign Currencies Transactions denominated in nonnon-U.S.currencyy must be valued in U.S. dollarseach reporting week by using one of thefollowingg methods:–The exchange rate prevailing on the Tuesday thatbegins the 77-day reporting week; or–The exchange rate prevailing on each correspondingday of the reporting week39

Reportingg ofDeposits in Foreign Currencies Once a DI selects a method it must usethat method consistently over time for allFederal Reserve reports.reports40

Reportingg ofDeposits in Foreign Currencies If the DI chooses to change its valuationmethod, the change must be applied to allFederal Reserve reports and usedconsistently thereafter The Federal Reserve Bank of New Yorkshould be notified of anyy such changeg41

QuarterlyQy Reportp of Foreigng ((Non(NonU.S.) Currency Deposits (FR 2915) In addition, FR 2900 respondents holdingforeign currency denominated deposits mustfile the Report of Foreign (Non(Non-U.S.) CurrencyDeposits (FR 2915) This report is filed quarterly, and it includesweekly averages for selected items from theFR 290042

R l t d InstitutionsRelatedI tit ti For U.S. branches and agencies of foreignbanks, related institutions are defined as– The foreign (direct) parent bank– Offices of the same foreign (direct) parent bank For all other institutions– Foreign (non(non--U.S.) branches43

Reporting of Related Institutions Deposits due to or due from U.S. branches andagencies of the same (direct) parent bankshould be excluded from the FR 2900 Deposits due to or due from nonnon-U.S. branchesand agencies of the same foreign (direct)parent bank should be reported in Schedule CC44

Foreign Bank Organization ChartBankBk HoldingH ldiCompany unrelatedReportingInstitutionClemenza Corp.Ltd(Rome)Parent BankrelatedIBFClemenza BClBankk(Munich)Vario Bank(Rome)U.S. BranchrelatedVario Bank(N.Y. Branch)Affiliated BankunrelatedVario Bank(Madrid)Vario Bank(Paris)Foreign BranchrelatedForeign BranchrelatedVario Bank(L.A. Branch)IBF

Bank Holding Company OrganizationChChartBankBk HoldingH ldiCompany unrelatedMaiden Lane Co. USAReportingInstitutionMaiden LaneBank Int’lBanking EdgeCorporationunrelatedMaiden LaneBankForeign BranchrelatedWaterWt StreetSt tBankIBFIBFMaiden LaneBank (Madrid)Affiliated BankunrelatedMaiden LaneBank (Paris)Foreign Branchrelated

Affili t andd SubsidiariesAffiliatesS b idi i Affiliates and subsidiaries of the same (direct)parent bank should be treated as unrelated forpurposes of Regulation D Deposits from these entities should beclassified on the FR 2900 according to the typeof entity (e.g., banking or nonbanking) andmaturity47

FR 2900 vs. FFIEC 002Definitional DifferenceFR 2900Deposits of U.S.U S andnon--U.S. subsidiariesnonof the pparent areincluded on theFR 2900 (accordingto entity and maturity)FFIEC 002Deposits of U.S.U S and nonnonU.S. banking subsidiaries areexcluded from Schedule Eand included on Schedule MNon-banking (majorityNonowned) subsidiaries areincluded in both Schedules Eand M, Part III48

Subscription Service A subscription service was created to notify ofreportingti changeshandd seminariannouncementst as theythare added to the Federal Reserve website. To subscribe, please register at the link ribe.html?code USFRBNEWYORK 849

Summary Purpose of the FR 2900 FR 2900 Filing Requirements–– Who must file?ConsolidationReporting Issues––––Back valuing vs. mispostingForeign currency valuationRelated vs. nonnon-related institutionsReportingi differencesdiffbetweenbtheh FR 2900and Call Reports50

Deposits vs. BorrowingsPatricia Maone51

Objectives Primaryy obligationsgreportablepon the FR 2900 Exempt and nonnon-exempt entities Examples of primary obligations Cashh equivalentsi l Precious metals borrowings52

Deposits vs.vs Borrowings A deposit is defined by Regulation D as theunpaid balance of money or its equivalentreceived or held by a depository institution inthe usual course of business.business In economic terms, deposits and borrowingsare similar. However, they are differenttransactions from a legal and regulatoryperspective.53

DDepositsit vs. BorrowingsBi If a transaction is called a depositpit mustbe treated as a deposit, regardless of thecounterparty and the terms of the transactiontransaction.54

Deposits vs.s BorrowingsBorro ings Whether a transaction is considered abborrowingi dependsdd on theth termstoff thethtransaction. If the document does not specifically refer tothe transaction as a borrowing, it should berecorded as a deposit.55

Primary Obligations Primary obligations are borrowingsthat should be reported as either:–––Transaction accountsSavings depositsTime deposits56

PiPrimaryObliObligationsti There are two factors to consider whendetermining if a transaction orinstrument is a “primaryprimary obligationobligation”.– The type of entity with which the transactionis entered into; and– The nature of the transaction or instrument57

Primary ObligationsExempt and NonNon--Exempt Entities The concept of exempt and nonnon--exempt entityapplies only to primary obligations. A “deposit” is reservable regardless ofp ythe counterparty.58

Include as Exempt Entities The following are exempt entities:–U.S. commercial banks and trust depository companiesand their subsidiaries–U.S. branches or agencies of foreign banks organizedunder Foreign (non(non-U.S.) law–Banking Edge and Agreement corporations–Industrial banks–Savings and loan associations and credit unions59

Incl de as ExemptIncludeE empt Entities Exemptp entities also include:–Federal Reserve Banks–U.S. Government and its agencies–U.S. Treasury60

IncludeIncl de as NonNon-exempte empt Entities The following are nonnon-exempt entities:–––Individuals, partnerships, and corporations (whereverlocated)Securities brokers and dealers, wherever located (Exceptwhen the borrowing has a maturity of one day, is inimmediately available funds,funds and is in connection withsecurities clearance)State and local ggovernments in the U.S. and their ppoliticalsubdivisions61

IncludeIncl de as NonNon-exempte empt Entities The following are nonnon-exempt entities:–A bank’s holding company–A bank’s nonnon-bank subsidiaries–InternationalI tti l InstitutionsI tit ti(IBRD,(IBRD IMF,IMF etc.)t )–Non--U.S. banks (related or unrelated)Non62

Examplesp of PrimaryyObligations The following are examples of primaryobligations to be included on the FR 2900 ifentered into with a nonnon--exemptp entityy–Repurchase agreements collateralized with assets otherg y securitiesthan U.S. ggovernment or federal agency–Purchases of immediately available funds(federal funds)63

Examplesp of PrimaryyObligations The following are examples of primary obligationsreportable on the FR 2900 if entered into with anon--exemptnonp entity:entityy:–Promissory notes–CCommerciali l paper–Due bills64

RRepurchasehAgreementsAt A repurchase agreement is an arrangementiinvolvingl i theth salel off a securityit or otherth assettunder a prearranged agreement to buy back thatasset at a fixed price If repurchasepagreementsgwith nonnon-exemptpentities are not collateralized by U.S. governmentor federal agency securities, they are to be reportedon the FR 290065

FR 2900 vs. FFIEC 002/031/041Definitional DifferencesFR 2900FFIEC 002/031/041Repurchase agreementsagreements,Repurchase agreementsagreements,collateralized with assetsotherth thanth U.S.USGovernment or Federalcollateralized with assetsAgency securities, arereported as deposits onthe FR 2900other than securities andwith a maturity greaterthan one business day,are reported as borrowings66

Federal Funds Purchased Federal funds are unsecured borrowings ofiimmediatelydi t l availableil bl fundsf d Immediately available funds can be used ordisposed of on the same business day thefunds become available Federal funds purchased from a nonnon-exemptinstitutions are reportable on the FR 290067

Promissoryy Notes andCommercial Paper A ppromissoryy note is a negotiableginstrumentwhich is evidence of a liability of a depositoryinstitution for funds that have been received. If the promissory note is issued to anon--exempt entity it should be reportednonon the FR 290068

Promissory Notes andCommercial Paper Commercial paper is an unsecuredpromissory note and should be reportedon the FR 2900.69

D BillDueBills A due bill is an instrument evidencing theobligationbli ti off a sellerll tot deliverd lisecuritiesiti attsome future date. If the due bill is not collateralized within 3b ibusinessdays,dit becomesbreservablebl on thethfourth business day regardless of the purposeor cocounterparty.nterpart70

Reporting of PrimaryObligations Any primary obligation of the reporting institution dueto a nonnon--exemptp entityy must be reportedpunless all ofthe following conditions are met:–Is subordinated to the claims of the depositors–Has a weighted average maturity of five years ormore–Is issued by a DI with the approval of, or under therules and regulations of,of its primary federalsupervisor71

Guidelines for Reporting PrimaryObligationsYesIs it a deposit?NoYesI it dueIsd tto an exemptt entity?tit ?NoSecurities Broker?Individual, Partnership or Corporation?YesYesIs it a Repo fully backed by a U.S.USGovernment Security?NoInclude on FR 2900YesIs it overnight funds regardingsecurities clearance?NoYesExclude from FR 2900

BorrowingsBioff “Cash“C h Equivalents”E i l t” For purpose of Regulation D the term depositis defined as the unpaid balance of money ori “equivalent”.its“ i l ”73

Borrowings of “CashCash EquivalentsEquivalents” Borrowingsg of U.S. Government or Agencyg ysecurity from nonnon-exempt entities arereservable,, if uncollateralized–If securities borrowings are collateralized with cashcash,, thettransactionti isi treatedt t d as a resalel agreement,t nott a depositdit74

Borrowings of “CashCash EquivalentsEquivalents” Borrowingsg of pprecious metals or otherequivalents of money are to be reported on theFR 2900 in the same manner as other currencyy(e.g., U.S. dollars)–These are reported based on the counterparty and maturity75

Borrowings of “CashCash EquivalentsEquivalents” For example,example borrowings of gold are consideredreservable liabilities.–ThTheseare reportedd on theh FR 2900,2900 ddependingdi on thehlender and the maturity.76

ReviewTTrueor FalseF lTrueRepurchase agreements with non-exemptnon exemptentities collateralized by U.S. Treasurysecurities are not reportable on the FR 2900.290077

ReviewTrue or FalseTrueCommercial paper issued by a DI is reportableon the FR 2900.78

ReviewTrue or FalseFalseBorrowing of gold bullion from a U.S.corporation would not be reported on theFR 2900.79

ReviewFederal funds purchased from which ofth followingthef ll i institutionsi tit tiare reportedt d onthe FR 2900?a)b)c)d)U.S. branch of a foreign bankFinance Corp.CorpABC Bank, N.A.W ld BankWorldB k80

SummarySummary Deposit is defined as unpaid balance of money orits equivalent q Primary obligations are reportable on the FR 2900 Exempt vs. non-exempt entities Borrowings of precious metals are consideredcashh equivalentsi lreportablebl on theh FR 290081

Transaction AccountsDean Cornier82

TTransactionti AccountsAt In general, there are two types oftransaction accounts:– DemandDd ddepositsit– “Other”Other transaction accounts (ATS,(ATS NOW,NOWtelephone and prepre--authorized transferaccounts)83

Demand Deposits Demand depositspare defined as:–Deposits payable immediately on demand, or issuedwith an original maturity of less than seven days84

Demand Deposits– InI addition,dditiunderd theth requirementsit offRegulation Q, interest cannot be paid onddemandd depositsdit4Section217.34Section 217.2217 2 (d)85

DDemanddDDepositsit Demand deposits include:–Checking accounts–O t t di certified,Outstandingtifi d cashiers’,hi ’ tellers’t ll ’ anddofficial checks and drafts–Outstanding travelers’ checks and moneyorders (unremitted)–Suspense accounts86

Demand Deposits Demand deposits include:–Funds received in connection with letters of credit sold tocustomers, including cash collateral accounts–Escrow accounts that meet the definition of a demanddepositp–“Primary obligations” with original maturities of less than7 days entered into with nonnon-exempt entities87

Demand Deposits Due toDepository Institutions (Line A.1.a) Include deposits in the form of demand depositsdue to:–U.S. commercial banks–Non--U.S. depository institutions (including banking affiliates)Non–U.S. branches and agencies of other foreign (non(non-U.S.) banks,including branches and agencies of foreign official bankinginstitutions88

Demand Deposits Due toDepository Institutions (Line A.1.a)Include deposits in the form of demandddepositsi dued to: –U.S. and nonnon-U.S. offices of other U.S. banks andEdge and agreement corporations–Mutual savings banks–Savings and loan associations–Credit unions89

Demand Deposits Dueto U.S. Government (Line A.1.b) Include in this item deposit accounts in theform of demand deposits that are designated asfederal public funds,funds, including U.S. TreasuryTax and Loan accounts Include only deposits held for the credit of theU.S. Government90

TT&L TT&L depository institutions have twooptions:––Remittance optionNote optioni91

TT&L–R iRemittanceoptioniByy the end of next business day,y, TT&L4deposits must be remitted to the FRB92

TT&L Note option–By the end of next business day, TT&L depositsmustt beb convertedt d tot openopen--endedd d iinterestinteresttt-bearingb inotes– These note balances are primary obligations to theU.S. Government but not reported on the FR 290093

Other Demand Deposits (Line A.1.c)A 1 c) Include in this item all other deposits in theform of demand deposits,deposits including:–Demand deposits held for:4Individuals, partnerships, and corporationsState and local governments and their subdivisions44Foreign governments (including foreign officialbanking institutions) and international institutions4U.S. government agencies94

Cashiers’ and Certified ChecksCashiers Cashiers’ checks are those checks drawn by thereportingpg institution on itself Certified checks are anyy business or ppersonalchecks stamped with the paying bank’scertification that:–The customer’s signature is genuine; and–Th are sufficientThereffi i t fundsf d ini theth accountt tot coverthe check.95

T ll ’ ChecksTellers’Ch k Tellers’ checks are those checks drawn by theTellersreporting institution on, or payable at orthrough, another depository institution, aFederal Reserve Bank,, or a Federal Home LoanBank.96

Tellers’ ChecksTellers Those checks drawn on,on or payable at or through,throughanother depository institution, on a zerozero-balanceaccount or an account not routinely maintained withsufficient balances to cover checks or drafts drawnin the normal course of business should be reportedpin Line A.1.c.97

Tellers’ Checks However,, those checks drawn on an account inwhich the reporting institution routinelymaintains sufficient balances should be:–Excluded from Line A.1.c.–The amount of the check should be deducted from thebalances reported in Line B.1.98

Suspense Accounts Unidentified funds received and held insuspense are considered deposits and are to bereported on the FR 2900. ThTheseffundsd shouldh ld bbe reportedt d as “Other“Othdemand deposits” in Line A.1.c99

FR 2900 vs. FFIEC 002/031/041Definitional DifferencesSuspense accountsFR 2900FFIEC 002/031/041Items held in suspense arereported in other demand.Entries to the G/L in theperiod subsequent to the closeof business on the reportdate are reported as if they hadbeen posted to the G/Lat or before the cutcut-offoff time.100

Reporting of Overdrafts Overdrafts in depositp(due(to)) accounts:–When a deposit account is overdrawn, the balance shouldbe raised to zero and not included as an offset to otherdemand deposit accounts–Instead the overdrawn amount should be reportedpas aloan by the reporting institution and excluded from thisreport101

Reporting of Overdrafts Overdrafts in depositp(due(to)) accounts:–The amount of the overdraft should not be nettedagainst positive balances in the depositors’ otheraccounts unless a bona fide cash managementgfunctionis served102

Reporting of Overdrafts Overdrafts in an account maintained atanotherth depositoryditinstitutioni tit ti (due(d from):f)–When a due from account becomes overdrawn,the balance should also be raised to zero–If the account is routinely maintained withsufficient funds, the overdrawn amount isconsidered a borrowingg and excluded fromthis report103

Reporting of OOverdraftserdrafts Overdrafts in an account maintained atanotherth depositoryditinstitutioni tit ti (due(d from):f)–If the dduee from accoaccountnt is not routinelyro tinel maintainedwith sufficient funds (e.g., zero balance account)the overdrawn amount is considered a demanddeposit and must be reported in other demand inLine A.1.a104

ReviewBank ABC maintains the following demand deposits.DDA AccountCorp. ACorp. BCorp CCorp.Corp. DAmount 10,000 15,000( 5 000)( 5,000) 20,000What should be reported on line A.1.c? 45,000105

Guidelines for Bona FideCash Management Agreements A bona fide cash managementagreement exists when a depositoryinstitution:–Allows a depositor to use the balance in onedeposit account to offset overdrafts inanotherth depositdit accountt–Some genuine cash management purposeis served106

Guidelines for Bona FideCash Management Agreements A written agreement does not have to be inplacelto beb “bona“bfide”fid ” Th cashh management agreement must haveThehsome indication the institution intends to usetwo or more checkingh ki accounts to controllreceipts and disbursements107

Guidelines for Bona FideCash Management AgreementsExample 1Establishing one account for receipts andanother for disbursements would be consideredbona fide.Example 2Establishing one account for payroll andanother account for receipts and disbursementswould not be considered bona fide.108

Guidelines for Bona FideCash Management AgreementsPositive balances in one type of deposit accountcannot be used to offset balances in another typeof deposit account.Example 3An overdraft in a demand deposit account cannotbe covered by positive balances in an MMDAaccount.109

Escrow Accounts An escrow agreement is a written agreementauthorizingth i i fundsf d tot beb heldh ld byb a thirdthi d party.t The funds are placed with the depository institutionuntil the agreement has been met, at which time theescrow funds are sent to the proper party. Escrow accounts are reported on the FR 2900accordingg to the terms of the escrow agreement.g110

Escrow Accounts If the funds may be withdrawn on demand orare to be disbursed within 7 days, the escrowaccount is a transaction account.111

“Other” TransactionAccounts112

“Other”Other Transaction Accounts “Other” transaction accounts are:– Deposit accounts (other than savings) where theDI reserves the right to require 7 days written notice prior towithdrawal/transfer of funds in the account– Subject to unlimited withdrawal by check, draft, negotiableorder of withdrawal,withdrawal electronic transfer,transfer or other similar items– Provided the depositor is eligible to hold a NOW account113

NegotiablegOrder of Withdrawal(NOW) Accounts (Line A.2) NOW accounts are deposits:–Where the DI reserves the right to require 7 days writteny funds in thenotice pprior to withdrawal/transfer of anyaccount–That can be withdrawn/transferred to third parties by anegotiable or transferable instrument (more than 6 times permonth)114

NOW Account Eligibility Eligibility limited to accounts where theentire beneficial interest is held by:–Individuals or sole proprietorships–U.S. governmental units, including the federalgovernment and its agencies–Non-profit organizations, such as churches,Nonprofessional, and trade associations115

Difference Between DemandDeposits and Other TransactionAccounts Demand deposits differ from “other”transaction accounts in that:–The DI does not reserve the right to require 7 days writtennotice before an intended withdrawal–There are no eligibility restrictions on who can hold addemandd depositdi account–Interest may not be paid on a demand deposit account116

Retail Sweeps Legal–One account with two legally ub4 NonNon--transaction subsub--account–Disclosure11

FR 2900 vs. FFIEC 002 Definitional Differences Consolidation of branches and agencies of the same fi (di ) bkforeign (direct) parent bank FFIEC 002 - U.S. branches and agencies in the same Federal Reserve District and state are not required to consolidate, but may submit a consolidated