Transcription

Corporate Alternative Minimum Tax,1987-1990Data Releasehe corporate alternative minimum tax (ANMwas designed to ensure that all corporations withT substantial amounts of "economic income" wouldpay a minimal amount of tax, regardless of their allowableuse of exclusions, deductions and credits. The AMTprovides a formula for tax computation which, in effect,ignores certain preferential tax treatments that are allowedin figuring the regular income tax. By eliminating thesepreferential deductions and credits, a tax liability iscreated for a corporation that would otherwise pay little orno tax.The total AMT reported by corporations for Tax Years1987 through 1990 was 17.2 billion [1]. The amount ofAMT increased each year over this 4-year period. TaxYear 1990 accounted for the largest amount of AMT, 8.1billion, or 47 percent of the total [2]. The AW for 1990represented a large increase over the 3.5 billion reportedfor 1989. In contrast, the amounts reported for 1987 and1988 were 2.2 billion and 3.4 billion, respectively.The number of corporation income tax returns thatreported AMT increased each year over the 4 years, from17,370 for 1987 to 32,462 for 1990. Although "giant"companies, i.e., those with total assets of 250 million ormore, tended to report most of the tax, "non-giants"fueled the rise in the number of payers, from 16,427 for1987 to 31,138 for 1990. The rate of increase in thenumber of giant companies which reported AMT wasslower, from 943 for 1987 to 1,324 for 1990.Although giant companies accounted for only 4 percent of the number of returns with AW between 1987and 1990, they reported 83 percent of the AMT for these4 years. For 1990, these companies reported 7.1 billionof AMT, approximately 87 percent of the total ANIT forthat year. This was the largest percentage of the totalreported by giant companies over the 4 years. Amonggiant companies with AMT, the 372 companies with totalassets of 2 billion or more accounted for 73 percent ofthe AMT reported by all companies for 1990.Indusby CharacteristicsLooking at AMT reported by corporations on an industrialbasis, the following three industrial divisions are ofprimary importance: manufacturing; finance, insuranceand real estate; and transportation and public utilities.This data release is based on a paper presented at the 1992National Tax Association meetings by Amy Gill, an economistwith the Corporation Special Projects Section, and PatriceTreubert, an economist with the Corporation Returns AnalysisSection, both under the direction of Karen Cys, Chief, Corporation Statistics BranckTables 1-4 present statistics on AW and related items for1987-1990 by industrial divisions.Manufacturers comprised the largest amount of AMTover the 1987-1990 period, with 6.8 billion, or 40 percent of the total. For 1990, corporations whose majorsource of receipts was from the manufacture of motorvehicles and equipment reported the largest amount ofAW in this industrial division [3]. Previously, petroleum and coal products companies (for 1988 and 1989)and nonelectrical machinery companies (for 1987) reported the largest AMT for manufacturers.Finance, insurance and real estate accounted for 23percent of the total AMT reported over the 1987-1990period. During this time, banks and insurance companiesswitched places as the predominant major industry basedon AMT. For 1990, insurance companies reported almosttwice as much AMT as banks.Transportation companies and public utilities comprised 20 percent of the AMT reported by all companiesduring the 1987-1990 period. For each of the 4 years,companies classified in the electric, gas and sanitaryservices industry group accounted for the largest amountof AMT. However, over the 4-year period, communications companies steadily increased their share of the totalAMT. Thus, for 1990, of the 1.8 billion of AMT reported for the transportation and public utilities industrialdivision, 0.8 billion was from electric, gas and sanitaryservices and 0.6 billion was from communications.Computation of the Alternative Minimum TaxCorporations (other than S Corporations which are taxedthrough their shareholders) were liable for the AMT iftheir tax base for purposes of the regular income tax(before subtraction of the "net operating loss deduction,"or NOLD), when combined with certain adjustments and"tax preference" items, exceeded the lesser of 40,000 oran allowable exemption amount. Under the Tax ReformAct of 1986, to compute the AMT, adjustments weremade to the income subject to regular tax, i.e., "taxableincome," computed before NOLD. These adjustmentitems could either increase or decrease the income subjectto regular tax, as derived for the computation of AMT.They were designed to eliminate the acceleration ofdeductions allowed in figuring regular tax and reflectedthe difference in treatment of certain items under theregular tax system versus the treatment under the AMTsystem. In some cases, the differences resulted innegative amounts.Tax preference items, which typically express morepermanent differences between the regular tax system andthe AMT system, were also added to the income base of71

Corporate Alternative Minimum Tax, 1987-1990the AMT. In addition, for Tax Years 1987-1989, therewas a book income adjustment in deriving the incomebase of the AMT. For Tax Year 1990, the book incomeadjustment was replaced by an adjusted current earningsadjustment, the so-called ACE adjustment. The bookincome and ACE adjustments were designed to ensurethat corporations reporting large earnings to investors paysome tax. The sum of income subject to regular taxbefore NOLD, the other adjustment items and the preference items first was compared to either the net bookincome or adjusted current earnings computed for AMTpurposes, and the difference multiplied by 50 percent forthe net book income calculation and 75 percent for theACE calculation. The result was the net book income orACE adjustment. Thus, the income subject to regular taxbefore NOLD combined with the adjustment items,including the book incomeadJuitment or the adjustedcurrent earnings adjustment, and the tax preference items,equaled "alternative minimum taxable income," or AMTI,before alternative tax NOLD.--Taxable- income-before-NOLD-and-the-book-itfc onfeFciradjusted current earnings adjustment were consistently thelargest components of AMTI before alternative taxNOLD. Of the tax preference items and the remainingAdjustments, the defteciMion of tangible Property placed'in service after 1986 was noticeably larger than any otheradjustment or preference item.AMTI before alternative tax NOLD could be reducedby an alternative tax NOLD and an income exemptionamount. The exemption amount was 40,000 minus 25percent of AMTI in excess of 150,000; the exemptionwas phased out when AMTI exceeded 310,000. ("Controlled groups" of corporations were required to use asingle exemption for the group, even if they filed separatereturns for each member.) By applying a 20 percent taxrate to the resulting amount, the "tentative minimum. tax"was determined.The tentative minimum tax could be reduced by anAMT foreign tax credit. The amount by which the remaining tentative minimum tax exceeded the regular tax72after reduction by the foreign tax credit (under the regularsystem) and the U.S. possessions tax credit was thealternative minimum tax (AMT) for the year [4]. However, AMT could then be further reduced by the investment credit.Notes and References[1] Tax Year 1990 represents corporate accountingperiods ended July 1990 through June 199 1. TaxYears 1987 through 1989 are similarly defined. TheAMT, introduced by the Tax Reform Act of 1986,'was for the most part first effective with corporateaccounting periods ended December 1987. Therefore, for the purpose of these tables, for Tax Year1987, only returns with accounting periods endedDecember 1987 through June 1988 are included inthe data.[2] Data for Tax Years 1987 and 1990 are revised.Earlier versions of the 1987 data were published invarious Statistics of Income publications. Preliminary 1990 data were presented in a paper at the 1992National Tax Association meetings.[3] For the statistics, returns are classified in a particularindustry group based on-the principal businessactivity (i.e., the activity which accounted for thelargest portion of total receipts) of the corporationfiling the return. However, a given return may havebeen fora' company engaged in several businessactivities or may have been a consolidated return filedfor an affiliated group of corporations which conducted different business activities. To this extent,the data presented here are not entirely related to theindustrial activity under which they are shown.[4] For a more detailed explanation of the alternativeminimum tax, and descriptions of the sample onwhich the statistics were based and of the samplingvariability of the estimates, see Statistics of IncomeCorporation Income Tax Returns, for the appropriateyear.

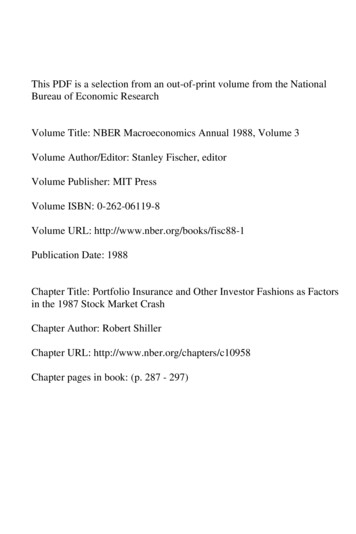

Table 1.-Returns with Alternative Minimum Tax: Selected Items by Industrial Division, Tax Year 1987[Ail figures are estimates based on samples--rrioney amounts are in millions of dollars]ftemNumber of returns.Total assets.Net income (less.deficio.--* ***'*'*'*"'**Taxable income (or loss) before not operatingloss deduction.Adjustment items:Total .Depreciation of property placed in serviceafter 1986 .Amortization of certified pollution controlfacilities placed in service after 19W.Amortization of mining exploration anddevelopment costs paid or incurredafter 1986 .Circulation expenses .Basis adjustment .Long-term contracts entered intoafter February 28, 1986 .Installment sales of certain property .Merchant marine capital construction funds .Section 833(b) deduction.'.Tax shelter farm activity loss .Passive activity loss .Certain loss limitations .Tax preference items:Total .Depletion .Tax-exempt interest from private activitybonds issued after August 7, 1986 .Appreciated property charitable deduction.Intangible drilling costs.Reserves for losses on bad debts offinancial institutions .Accelerated depreciation of real propertyplaced in service before 1987 .Accelerated depreciation of leased personalproperty placed in service before 1987 .Amortization of certified pollution controlfacilities placed in service before 1987.AJI industrialdivisionsAgriculture,forestry andfishingMiningConstructionIndustrial divisionTransportationManufacturingand publicutilitiesWholesaleand retailtrade02,667127,4962,767Finance,insurance andreal 1,17352224109118Adjusted net book income (less deficiQ .69,9531791.867Alternative tax not operating loss deduction.24,231771,121Alternative minimum tax foreign tax credit .2,5541137Tentative minimum tax .4,88416153Alternative minimum tax.2,228791'Includes "Nature of business not allocable."2Less than 500,000.'Deduction allowed certain health insurance organizations voas disregarded for alternative minimum tax purposes.NOTE: Detail may not add to totals because of rounding.

74a,'6 gaC.FIR4v19'q]yizJ:0cotWiC)111 K11" Vo lk" iisPig1I HjR!all; 1'qcO 11 A1g2 1U0U.-sc1. ataNiK "sit:I 'iUo F6C4IsmRRAV9 ism0 C4iI-Elm"A'soI9j i E2:dENJI11 IEE132t 0MY U zE-ARMS, win v 1 pill9 9 E:owT 1 E 1 , - E E A -: "Corporate Alternative Minimum Tax, 1987-1990.E8eilIE

0)In gNNN(do-VNN:aocL- :o'woaz ItII ovs-9c 11-0)49f,c !9Ogglpa)9J- :ELxleCorporate Alternative Minimum Tax, 1987-1990csgn-4(4 cd (dtQ :'6SLDi:o:vr c42 r IQ(Dc48z 1-9c1l(qNjv51c"-1-4aa G TIIL I .0cqN'iMc4F 9 § ol coo g-cn9w c4cq(qE"ie'6lea v.-"i i RJ1EchNce75

Table 4.- Returns with Alternative Minimum Tax: Selected Items by Industrial bivision, Tax Year 1990(All figures are estimates based on samples - money amounts are in millions of dollars)ItemNumber of returns. I.Total assets. .Net income (less deficlo.Taxable income (or loss) before net operatingloss deduction . .Selected adjustment items:Total . .Depreciation of property placed in serviceafter 1 986 . :.Amortization of mining exploration anddevelopment costs paid or incurredafter 1 986 . .Selected tax preference Items:Total .Depletion .Tax-exempt interest from private activitybonds issued after August 7,1986 .Appreciated property charitable deduction. ;Intangible drilling costs .Accelerated depreciation of real propertyplaced in service before 1987.Accelerated depreciation of leased personalproperty placed in service before 1987.Pre-adjustment alternative minimum taxable income.Adjusted current earnings .Alternative minimum taxable income before alternativetax not operating loss deduction.Alternative tax not operating loss deduction.Alternative minimum taxable income.Exemption.Alternative minimum tax foreign tax credit .Tentative minimum tax. .Alternative minimum tax.1 Includes "Nature of business'not allocable."2 Less than 500,000.NOTE.: Detail may not add to Iotals because of rounding.Al industrialdivisionsAgriculture,forestry andfishingMiningConstruction(4)1Industrial divisionTransportationManufacturingand publicutilifies(5)R6,4942,7581.650 116783 3,07973056,89715,94326,087811Wholesaleand retailtrade05,012297,8634.103Finance,insurance andreal ,6531 ,5363,996292954923301,53538288,3597,586 3103

AMTI before alternative tax NOLD could be reduced by an alternative tax NOLD and an income exemption amount. The exemption amount was 40,000 minus 25 percent ofAMTI in excess of 150,000; the exemption was phased out when AMTI exceeded 310,000. ("Con-trolled groups" ofcorporations were required to use a