Transcription

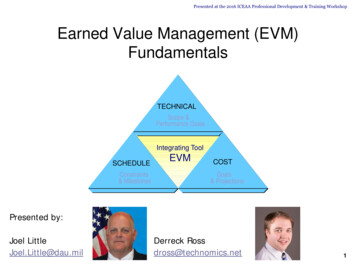

Presented at the 2017 ICEAA Professional Development & Training Workshopv1.2www.iceaaonline.com/portland2017Earned Value Management(EVM)Tracking cost and scheduleperformance on projects“What are my chances?” / “Not good.” / “You mean, not good like oneout of a hundred?” / “I’d say more like one out of a million.” / “Soyou’re telling me there’s a chance!”- Jim Carrey as Lloyd Christmas to Lauren Holly as Mary SwansonDumb and Dumber, http://www.imdb.com/title/tt0109686/.Unit V - Module 15 2002-2013 ICEAA. All rights reserved.1

Presented at the 2017 ICEAA Professional Development & Training ledgments ICEAA is indebted to TASC, Inc., for thedevelopment and maintenance of theCost Estimating Body of Knowledge (CEBoK )– ICEAA is also indebted to Technomics, Inc., for theindependent review and maintenance of CEBoK ICEAA is also indebted to the following individuals who have madesignificant contributions to the development, review, and maintenance ofCostPROF and CEBoK Module 15 Earned Value Management (EVM)– Lead authors: Jennifer M. Rose, Maureen L. Tedford– Senior reviewers: Richard L. Coleman, Brian L. Octeau, Fred K. Blackburn,Colleen M. Craig– Managing editor: Peter J. BraxtonUnit V - Module 15 2002-2013 ICEAA. All rights reserved.2

Presented at the 2017 ICEAA Professional Development & Training WorkshopUnit Indexv1.2www.iceaaonline.com/portland2017Unit I – Cost EstimatingUnit II – Cost Analysis TechniquesUnit III – Analytical MethodsUnit IV – Specialized CostingUnit V – Management Applications13. Economic Analysis14. Contract Pricing15. Earned Value Management (EVM)16. Cost ManagementUnit V - Module 15 2002-2013 ICEAA. All rights reserved.3

Presented at the 2017 ICEAA Professional Development & Training WorkshopEVM Overview Key Ideasv1.2www.iceaaonline.com/portland2017 Practical Applications– Integrated baseline Resource-loaded schedule– Earned value Objective progressing– EACs – risk-adjusted rollups– EACs – alternative formulae– Performance measurement Contract vs. technical– Extrapolation from Actuals– Cost and scheduleperformance Analytical Constructs Related Topics– AC (Actual Cost) actuals to– Risk Managementdate– Project Management– EV (Earned Value) value of– Schedule Analysis / Riskwork performed– PV (Planned Value) budget– EAC AC (BAC-EV)/PI Tip: This formula, while intuitive, may not be theBCWRbest predictor of EAC!Unit V - Module 15 2002-2013 ICEAA. All rights reserved.4

EVM within theCost Estimating FrameworkPresented at the 2017 ICEAA Professional Development & Training esentFutureUnderstanding yourhistorical dataDevelopingestimating toolsEstimating the newsystem3000.03000.0Management Reserve2500.0VACManagement Reserve2500.0PMBEAC or LRECBBCBBBACPMB2000.02000.0Schedule DelayCost Variance500.0Earned Valuedata elementsEstimate AtComplete (EAC)formulaeUnit V - Module 15 2002-2013 ICEAA. All rights reserved.EAC ost 1500.0AprScheduleVariance1500.0

Presented at the 2017 ICEAA Professional Development & Training Workshopv1.2www.iceaaonline.com/portland2017EVM and Cost Estimating How should Cost Estimators beinvolved in EVM? Verify Realistic Baselines20– Control Accounts that trace to BOEs– Cost Estimator participation in IBRs Develop Accurate EACs– Statistical and risk-based methods Gather Cost Data to Support Estimating– IPMR and other EV data serve as datasources for estimating analogous effortsUnit V - Module 15 2002-2013 ICEAA. All rights reserved.6

Presented at the 2017 ICEAA Professional Development & Training WorkshopEVM Outlinev1.2www.iceaaonline.com/portland2017 Core Knowledge– Introduction to Earned Value– Earned Value Management (EVM)Components– Earned Value Analysis Summary Resources Related and Advanced TopicsUnit V - Module 15 2002-2013 ICEAA. All rights reserved.7

Presented at the 2017 ICEAA Professional Development & Training uction to Earned Value EVM ObjectivesThe EVM Bottom Line and BenefitsEVM Not Universally RightEVM Guidance and ContractRequirementsUnit V - Module 15 2002-2013 ICEAA. All rights reserved.8

Presented at the 2017 ICEAA Professional Development & Training WorkshopWhat?EVM Objectivesv1.2www.iceaaonline.com/portland2017 Earned Value Management (EVM) integratesTechnical Scope, Schedule, and Cost fordefinitized contract work Earned Value Management System (EVMS)– Planning tool– Reporting tool– Analysis and Decision Making tool15 Provides for integrated management of programplanning and execution, which can enable – Accomplishment of Technical Scope within Cost andSchedule parameters– Reduced or Eliminated Schedule Delay– Reduced or Eliminated Cost OverrunUnit V - Module 15 2002-2013 ICEAA. All rights reserved.9

Presented at the 2017 ICEAA Professional Development & Training WorkshopWhy?www.iceaaonline.com/portland2017The EVM Bottom Linev1.2 Yeah, yeah “integrated management” isgreat, but costs . Why should I really do it?– The cost avoidance window of opportunity isBEFORE contract is 15% complete– According to a study of more than 700 major DoDprograms, percent overrun at completion will bewithin 10% of percent overrun at 20% complete“Cost Performance Index Stability,” David S. Christensen and Scott Heise, National Contract Management Journal, 1993– If you can’t plan the near-term work well, you won’tplan the far term work any better EVM requires all work on contract to beplanned before beginning– Can provide early insight into areas of concernand opportunityUnit V - Module 15 2002-2013 ICEAA. All rights reserved.10

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Key EVM Benefits1 Imposes discipline on resource planningprocess through the development ofwork and planning packages Provides disciplined, standardizedapproach to measurement andterminology Ties cost and schedule performance totechnical accomplishment of work Provides objective analysis ofperformanceUnit V - Module 15 2002-2013 ICEAA. All rights reserved.11v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Basic EVM Example Managing projects without earned valueprovides only part of the picture Traditional approach:– Budget work– Record Actual expenses Example:– Budgeted for 4 Aquaria to be built inNovember at 100 each– At end of November, spent 300– Great! I am 100 under budget or am I?Unit V - Module 15 2002-2013 ICEAA. All rights reserved.12v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Basic EVM Example Example (continued):– Did I accomplish 400 worth of work whilespending only 300?– Earned value adds a new dimension – whatis the VALUE of work accomplishedEarnedValueBudget 400vsActual 300Variance 100Unit V - Module 15 2002-2013 ICEAA. All rights reserved.13v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Basic EVM Example Example (continued):– At the end of November I spent 300 butonly completed 2 AquariaBudget 400EarnedValue 200Actual 300CostVariance- 100– So I am not only overrunning Cost, I amalso behind schedule!Unit V - Module 15 2002-2013 ICEAA. All rights reserved.14v1.2

Presented at the 2017 ICEAA Professional Development & Training WorkshopWhen?www.iceaaonline.com/portland2017EVM Not Universally Rightv1.2 EVM costs time and money to implement EVM is not the best management tool for all projects EVM is best suited/most beneficial for projects with:– Defined deliverables/products– Longer durations Guidance varies by organization Due to set up time required– Strict budget limits or Firm Fixed Price (FFP) contracts– A single contract encompassing all or most of the effort Few to no interfaces with or dependence on efforts contracted separately EVM less suited for projects with:– Difficult to define or open-ended objectives– Shorter durations– Level of Effort (LOE) support hours as the primary deliverableEVM is required on DoD andother government contractsabove a certain thresholdUnit V - Module 15 2002-2013 ICEAA. All rights reserved.15

EVM GuidancePresented at the 2017 ICEAA Professional Development & Training WorkshopHow?RiskBasedDecisionEVM DataRequirementsContract Value 0(EVM on FFP, LOE & T&M Contracts Discouraged)Dollar thresholds are the same for all budget appropriation categories.Color of money is no longer an EVM discriminator.Pre 7/1/2012EVM SystemRequirementsCost Reimbursement & Incentive ContractsPost7/1/2012AcquisitionFunding(Then Year M)v1.2Policy Updated June 2012No Mandatory RequirementsContract Typewww.iceaaonline.com/portland2017Conformance withANSI / EIA 748Conformance withANSI / EIA 748Formal EVMSvalidation not requiredFormal EVMSvalidation requiredContract Performance Report(DI-MGMT-81466) (5 formats)Contract Performance Report(DI-MGMT-81466) (Tailored)Integrated Master Schedule(DI-MGMT-81650) (Tailored)Integrated Master Schedule(DI-MGMT- 81650)Integrated Program Management Integrated Program ManagementReport (DI-MGMT-81861)Report (DI-MGMT-81861)5020Earned Value and the Acquisition Program, Prof Roberta Tomasini, DAU, 2008Unit V - Module 15 2002-2013 ICEAA. All rights reserved.16

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017EVM Contract Requirementsv1.2 Per DFARS 252.234 and the DoD IPMRImplementation Guide, EVMS is required for cost andincentive contracts and subcontracts as follows: 50MContracts 50MEVMS must be determined ANSI/EIA-748 compliantby Cognizant Federal AgencyAll formats mandatory 20MContracts 20M, but 50MEVMS must comply with guidelines in AmericanNational Standards Institute/Electronic IndustriesAlliance Standard 748, Earned Value ManagementSystems (ANSI/EIA-748).Formats 1, 5 – 7 mandatory, 2 – 4 optionalContracts 20MApplication of EVMS is optionalUnit V - Module 15 2002-2013 ICEAA. All rights reserved.Note: EVMS is lessfrequently used onFirm-Fixed Price, Levelof Effort, and Time &Material effortsregardless of cost, aswell as short durationcontracts (e.g., 1 yr)NEW!17

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017EVM within the Acquisition OURCE SELECTIONAWARD PROJECTDEVELOPProgram Execution& .2ESTABLISHPerf Meas.BASELINEMGT VOLUMEASSESS RISKTECH VOLUMEDEVELOP MRCOST VOLUMEASSIGN BUDGETSSTATUSREPORTSEarned Value and the Acquisition Program, Prof Roberta Tomasini, DAU, 2008Unit V - Module 15 2002-2013 ICEAA. All rights reserved.18

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Earned Value Management(EVM) Components Integrated Baseline OverviewWork Breakdown StructureAssignment of WorkEarned Value Data ElementsBaseline DevelopmentPerformance MeasurementUnit V - Module 15 2002-2013 ICEAA. All rights reserved.19v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Integrated Baseline Overview Key component of EVM is the ResourceLoaded Schedule– Elements of the Performance MeasurementBaseline (PMB) defined early in acquisitionprocess by Government and Contractor WBS Structure Schedule BOEs (justification for time phased costs and effort)– Time-Phased Budget / Resource LoadedSchedule initially defined for proposal andrefined/baselined post negotiations Government review of PMB occurs viaIntegrated Baseline Review (IBR)Unit V - Module 15 2002-2013 ICEAA. All rights reserved.1520v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017WBS Definition/Overview Work Breakdown Structure (WBS): Product1oriented division of material and work tasks Used to organize and define product/work tobe accomplished Different forms:– Program Summary WBS (Government), usuallyreferred to as WBS– Contractor WBS, usually referred to as CWBS– Cost Element Structure (CES) Level and scope may depend on the underlying data andmethodology used in developing the estimate– WBS typically several levels higher than CWBSOSD EVM Website: http://www.acq.osd.mil/evm/Unit V - Module 15 2002-2013 ICEAA. All rights reserved.21v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017WBS Importance to EVM WBS provides framework within which allEarned Value planning is accomplished WBS must be:– Comprehensive Matches program content– Hierarchical– “Sufficient” level of detail Sufficiency depends on size, complexity, risk, and otherfactors For EVM, level of detail for tracking costs usually lowerthan level for reporting costsUnit V - Module 15 2002-2013 ICEAA. All rights reserved.22v1.2

Presented at the 2017 ICEAA Professional Development & Training WorkshopWBS Examplewww.iceaaonline.com/portland2017v1.2 WBS Sample layout for the aquaria example1.0 Aquarium Development Program1.1 Program Management / Systems Engineering1.2 Design AquariumNOTE: Example1.3 Develop/Integrate AquariumWBS is not1.3.1 Material Acquisitioncomprehensive or1.3.2 Material Integrationextensively detailed.1.3.3 Development Documentation1.4 Test Aquarium1.5 Deploy Aquarium2.0 Aquarium Maintenance Program2.1 Maintain Environment2.2 Replace Material2.3 Maintain/replace Fish PopulationUnit V - Module 15This WBS does notadhere toMIL-STD-881C andtherefore needs acomprehensive WBSDictionary.4 2002-2013 ICEAA. All rights reserved.23

Organizational BreakdownStructure (OBS) DefinitionPresented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017v1.2 Functional breakdown of Organization16– Identifies the program’s organizational structure– Supports the identification of the functionresponsible for controlling overhead costs Typically aligns with Company’s Org Chart One piece of the framework used for planningresources One popular organization technique involvedIntegrated Product Teams (IPTs)– Multi-disciplined– Overarching IPT and Working-level IPT(s)Defense Acquisition w document&rf GuideBook\IG c10.3.asp.Unit V - Module 15 2002-2013 ICEAA. All rights reserved.24

Assignment of Work –Control AccountsPresented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017 WBS cross-walked to OBS Control Accounts– Identifies Responsibility– Result is Control Account (sometimes called a Cost Account) Control Account is the focal point for integration ofscope, cost, and schedule Control Account Manager (CAM) is personresponsible for:– Developing plan for Control Account (Technical Scope,Schedule Tasks, Budget/Resources) Work Authorization Document (WAD)– Managing Earned Value performance within Control Account Monitoring EVM metrics Analyzing control account performance status Reporting variances– Conducting risk management/mitigation as requiredUnit V - Module 15 2002-2013 ICEAA. All rights reserved.25v1.2

Assignment of Work –Work PackagesPresented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017 Work Packages are the lowest level at whichresources are allocated Within Control Accounts, work and planningpackages defined at lowest level of detail– Work packages for near-term workTip: Typically 4-6weeks long– Planning packages for far-term work– Planning packages become more detailed work packages astime progressesTip: Detail plantypically 6 months out Resources allocated to each work/planning package– Direct Labor– Material– Other Direct Charges (ODCs)Unit V - Module 15 2002-2013 ICEAA. All rights reserved.26v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Assignment of Work IllustrationAquariumDevelopmentProgramProgram WBSElementsProgramMgmt/SystemsEngineeringContract WBSReportingElementsMaterialAcquisitionContract tControlAccountPlanningPackagesGraphic adapted from EVMS Basics Concepts, Sean Alexander, MeridianetOBS DATA SUMMARIZATIONUnit V - Module 15 2002-2013 ICEAA. All rights reserved.27v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Earned Value Data Elementsv1.2 Earned Value has five basic data elements:ElementTitleCommon TerminologyBCWSBudgeted Cost of WorkScheduledPlanned Value (PV), PerformanceMeasurement Baseline (PMB), plan,baselineBCWPBudgeted Cost of WorkPerformedEarned Value (EV)ACWPActual Cost of Work PerformedActual Cost (AC), actualsBACBudget at CompletePlanned CostEAC / LREEstimate at Complete / LatestRevised EstimateForecasted CostTip: EAC generally refers to the Government’s independent assessment of theestimate at complete while LRE refers to the Contractor’s estimate at completeUnit V - Module 15 2002-2013 ICEAA. All rights reserved.28

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017BCWS (The Plan)v1.2 Budgeted Cost of Work Scheduled (BCWS): The sum ofthe budgets for all work packages, planning packagesscheduled to be accomplished within a given time period– The value of the work scheduled– The baseline used to measure all performance– The resource-loaded scheduleAKA PlannedValue (PV) Picture a Gantt chart17 BCWSBACTimeUnit V - Module 15 2002-2013 ICEAA. All rights reserved.29

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017v1.2BCWP (What Work Was Performed?) Budgeted Cost of Work Performed (BCWP): Thesum of all budgets for completed work packagesand completed portions of open work packagesAKA Earned– The value of the work performedValue (EV)– Dependent on BCWS – can only earnas much as is loaded in the completed BCWS tasksTime now BACBCWSBCWPTimeUnit V - Module 15 2002-2013 ICEAA. All rights reserved.30

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017ACWP (Cost Incurred)v1.2 Actual Cost of Work Performed (ACWP): The costsactually incurred to accomplish the work earnedwithin a specified time frameAKA Actuals (AC),Actual ValueLaborMaterialGeneral LedgerContractor’sAccounting SystemSubcontractInvoicesExport actualsto EVM databaseInvoicesTravelODCsACWP BCWSBACBCWPTimeUnit V - Module 15 2002-2013 ICEAA. All rights reserved.31

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017BAC and LRE (End of Work) Budget At Complete (BAC): Cumulative BCWS atthe end of the contract Latest Revised Estimate (LRE): The contractor’sbest guess at how much the effort will actually costat the end of the contractLREACWP BCWSBACBCWPTimeUnit V - Module 15 2002-2013 ICEAA. All rights reserved.32v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Baseline DevelopmentPriceContract BudgetBaseMR coversunanticipated,in scopechangesCost (CBB)ManagementReserve 10MControl Accounts arethe managementcontrol point for theintegration of scope,schedule & cost 110Mf 100M 40MFeePerformance MeasurementBaseline (PMB) 90MDistributed Budget(Control Accounts) 85MWorkPackagesv1.2UndistributedBudget 5M 10MEarned Value ismeasured againstthe PMBWork is tied toan activity, butis not detailplannedPlanningPackages 45MUnit V - Module 15 2002-2013 ICEAA. All rights reserved.33

Presented at the 2017 ICEAA Professional Development & Training ne Development – PMB18 Performance Measurement Baseline (PMB)developed– Sum of all Work/Planning Package Budgets UB– Undistributed Budget (UB) is: Work tied to an activity, but not detail-planned Used most often when new work added to contract Earned Value is Measured against the PMB Work packages and related budget (BCWS)are time phased using logic-driven schedule– e.g., PERT chart showing dependenciesTip: UB usually distributed within 60 daysUnit V - Module 15 2002-2013 ICEAA. All rights reserved.34

Presented at the 2017 ICEAA Professional Development & Training ne Development – MR Management Reserve (MR) set asidewhile developing PMB19– Covers unanticipated, in scope changes– MR % tied to level of risk and type ofcontract14 2-4% low risk and/or Cost Plus 15% high risk and/or Firm Fixed Price– More discussion on MR and its use iscovered under the Analysis of PastPerformance sectionTip: MR is most commonly 7-9% of CBBUnit V - Module 15 2002-2013 ICEAA. All rights reserved.35

Presented at the 2017 ICEAA Professional Development & Training ne Development – CBB PMB and MR together form the Contract3Budget Base (CBB) (“Cost”) CBB plus fee yields the Total Contract Value(“Price”) A time-phased graphic illustrating PMB andMR forming CBB is on the next slide EVM should be complemented by adisciplined Risk Management (RM) approachto identifying, quantifying, and addressingunknown future events“Integrating EVM and RM: A Statistical Analysis of Survey Results,” Alissa C. Kumley, Northrop Grumman Corporation,ISPA/SCEA Joint International Conference, 2005Unit V - Module 15 2002-2013 ICEAA. All rights reserved.36

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Baseline Developmentv1.2 Typical Phased Baseline (BCWS)3000.0CBBManagement nAprFebDecOctAugJunAprFeb0.0Tip: Cum PMB usually follows an S-curve.Unit V - Module 15 2002-2013 ICEAA. All rights reserved.37

Presented at the 2017 ICEAA Professional Development & Training e Measurement There are different ways to estimate progressof a project– Key issue is in-process work packages Value is earned (BCWP) when correspondingwork is accomplished When value will be earned is determinedbefore beginning work using commonperformance measurement methods Assignment of method should strive to reducesubjectivity Table on next slide outlines:– Most common methods– When methods are typically employedUnit V - Module 15 2002-2013 ICEAA. All rights reserved.38v1.2

PerformanceMeasurement – EV MethodsPresented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017v1.2EV MethodDescriptionType of Tasks that Use MethodMilestone(Weighted)Take performance as definedMilestones (MS) are accomplished.MSs can be weighted if one or moreare considered more importantTasks that can be planned usinginterim MilestonesPercentCompletePerformance is taken based onPercent of task completedWork that does not have anyreasonable interim measurable MSs0/100All performance is taken when task iscompleteShort duration tasks - one month orless50/50Or X%/Y%50% (X%) performance taken whentask starts; 50% (Y%) performancetaken when task is completeShort duration tasks - two months orlessLOEPlan based on resource expenditureplan – Performance always equalsPlanUsed for tasks that are more timeoriented vice task oriented, such asProgram ManagementBest Method for EVMUnit V - Module 15 2002-2013 ICEAA. All rights reserved.39

Example –Performance MeasurementPresented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017 Determine the best earned valuemeasurement technique:– Aquarium System Program Management– Aquarium Design– Aquarium Deployment to Site ATLANTIC4Unit V - Module 15 2002-2013 ICEAA. All rights reserved.40v1.2

Example –Performance MeasurementPresented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017v1.2 Valid earned value measurement techniques:– Aquarium System Program Management LOE – most common method Milestone– Aquarium Design Most likely Design will be divided into smaller workpackages and multiple methods will be employed Milestone / Weighted Milestone – most common method Percent Complete– Aquarium Deployment to Site ATLANTIC 0/100 X%/Y% MilestoneMultiple Answers are JustifiableUnit V - Module 15 2002-2013 ICEAA. All rights reserved.41

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Earned Value Analysis Elementary EV AnalysisAnalysis of Past PerformanceVariance ReportsProjection of Future PerformanceEarned Value Review ProcessUnit V - Module 15 2002-2013 ICEAA. All rights reserved.42v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Elementary EV Analysis Common calculated Data Elements:– Schedule Variance (SV) BCWP – BCWS– Cost Variance (CV) BCWP – ACWPAKAAccomplishmentVariance3000.0CBBManagement Cost VarianceBCWSACWP500.0BCWP 2002-2013 ICEAA. All rights reserved.AugJunAprFebDecOctAugJunAprFeb0.0Unit V - Module 15v1.243

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Elementary EV Analysis Common calculated Data Elements:– Variance at Complete (VAC) BAC – LRE– Estimate at Complete (EAC) Forecasting measure Various methods applicable Discussed in more detail later– Budgeted Cost of Work Remaining (BCWR) BAC – BCWP Analysis of data, including sampleproblems, in next sectionUnit V - Module 15 2002-2013 ICEAA. All rights reserved.44v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Elementary EV Analysis3000.0EAC or LRECBBVACManagement Reserve2500.0BACPMB2000.0Schedule DelayScheduleVariance1500.0BCWS500.0ACWPUnit V - Module 15 2002-2013 ICEAA. All rights .0Cost Variance45v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Analysis of Past Performance CV, SV, and VAC: Most common andsimplest derived earned value data Examine current and cumulative data pointsand trends– Cumulative data points good for determiningaverage performance– Current data points good for assessing currentperformance and for highlighting anomalies, errorsin data, and error corrections– Trend lines good for assessing performance overtime – Sudden trend changes should be examinedUnit V - Module 15 2002-2013 ICEAA. All rights reserved.46v1.2

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Analysis of Past Performancev1.2 Any variance over 10% is serious and shouldbe examined– CV % CV / BCWP 1 – 1/CPI– SV% SV / BCWS SPI - 1 Focus on CV and SV (vice VAC) Variances are natural– Explained and managed, but not eliminated Variances, and emerging or present trends,can erase with a rebaselineTip: Sudden “healing” spikes in cum CV/SVtypically mean a rebaseline has occurred“Understanding Program Resource Management through Earned Value Analysis.” Falls Church, Va.: Abba Consulting,June 2006.Unit V - Module 15 2002-2013 ICEAA. All rights reserved.47

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Analysis of Past ebaselineFeb7Variance Percentage CV, SV, and VAC:VACUnit V - Module 15 2002-2013 ICEAA. All rights reserved.48v1.2

Presented at the 2017 ICEAA Professional Development & Training e – Past Performance Sample problem:– Building 8 Aquaria Budgeted for 4 to be built in Nov and 4 to be built in Decat 100 each256– At the end of Nov, contractor spent 300 andcompleted 2– Contractor now expects the project to cost a totalof 1000– For Month-end (ME) Nov, what is cumulativeBCWS? BCWP? ACWP?– For ME Nov, what is cumulative CV? SV? VAC?– What are those variances telling us?Unit V - Module 15 2002-2013 ICEAA. All rights reserved.49

Presented at the 2017 ICEAA Professional Development & Training e – Past Performance Answers:–––BCWS 400 BCWP 200ACWP 300CV - 100 SV - 200VAC - 200What are those variances telling us?1. Overrunning now, accomplished less than planned, expectoverrun at complete, if task on critical path then expect a delayat complete – Facts based on data provided2. Do not expect to repeat overrun for Aquaria #3-8 becauseVAC 4 * CV. Ask: Is this realistic? Why do they thinkoverrun will not be repeated?3. Built 2 in one month, now expect to build 6 in next month –Unlikely – Ask: How do they plan to accomplish this and notspend more /system than budgeted–Begin to plan for how to cover current overrun andexpected future overrunUnit V - Module 15 2002-2013 ICEAA. All rights reserved.50

Presented at the 2017 ICEAA Professional Development & Training Workshopwww.iceaaonline.com/portland2017Past Performance – Indices Cost Performance In

2002-2013 ICEAA. All rights reserved. v1.2 Unit V - Module 15 1 Dumb and Dumber, http://www.imdb.com/title/tt0109686/. Earned Value Management (EVM)