Transcription

Family officeThe roots of the family office extendback to the late 19th century when manyfamily offices were founded to managethe significant fortunes of successfultycoons. While the original familyoffices were in many cases establishedfor those individuals who had createdlarge manufacturing empires, today weobserve many hedge fund and privateequity founders, as well as technologyand real estate entrepreneurs, formingfamily offices following a significantliquidity event.

Download the third issueIntroductionEvaluating services tobe providedTransfer pricing in thefamily officeFraud in the family officeResourcesFamily officeIntroductionIn the last decade, several factors haveconverged to significantly drive interest infamily offices: A wave of new global wealth creation andaccumulation, including Baby Boomerswho are selling their businesses andreinvesting the resulting liquid assetsto sustain, enhance, and protect thefamily’s wealth Successful entrepreneurs selling theirbusinesses and pursuing their passion toinvest capital and sweat equity in philanthropic endeavors A growing number of families committedto “making an impact” in the world, nowand in the future Continued market volatility leadingwealthy families to take more “hands on”control over investment policy decisions Banking and business failures, investmentfraud, and cybercrime prompting familiesto take an institutional approach to familyrisk managementAlthough many top-tier private banks,investment firms, and consulting practicescan provide these services, a growingnumber of individuals and families havechosen to form a single family office thatis devoted to the personal needs anddesires of the family. And regardless of howlong a family office has been in existence,we consistently find that individuals andfamilies want to assess the services thefamily office provides to the individuals,trusts, and entities (“clients”) served bythe family office.deliver the services, the complexity of theservice to be delivered, and whether talentexists in the marketplace to provide theservices. In many instances, the cost toacquire technology necessary to deliver theservice is also a deciding factor. If the costto acquire, implement, and maintain thetechnology exceeds a certain threshold, itmay be more effective to hire a third partyto deliver the service.In this section of our guide, we will take alook at the services frequently provided bythe family office to its clients and discusshow the family office determines whether itwill insource or outsource the responsibilityfor such services. There are a variety offactors that will impact a family office’sdecision to hire talent to deliver the servicesinternally compared to paying a third partyto provide the services to the family office’sclients. Those factors include the cost toAlthough many top-tier private banks and investment firms canprovide these services, a growing number of individuals and familieschoose to form a single family office that is devoted to the personalneeds and desires of the family.2017 Essential Tax and Wealth Planning Guide Family office5

Download the third issueIntroductionEvaluating services tobe providedTransfer pricing in thefamily officeFraud in the family officeResourcesFamily officeIntroductionIn addition to evaluating whether toinsource or outsource services, many familyoffices are reassessing the fees chargedfor their services. Although a family officemay be created to serve one or multiplegenerations, the typical goal is to create abusiness organization that is appropriatelycompensated for the customized servicesit delivers to its clients. Furthermore, whererelated party transactions occur betweenthe family office and its clients, such aspayment for the services delivered, cautionmust be exercised to ensure that theamounts charged are reasonable and atmarket rates. We will evaluate in this sectionof the guide how transfer pricing guidelinescould apply to assist the family office withdetermining reasonable compensation forthe services it delivers.Finally, whether the family office ismanaging assets that the family desires topass to future generations or to achievefamily members’ philanthropic goals, thepreservation and security of these assetsis critical. No one wants to think thatfraud could impact their family’s wealth.Unfortunately, we are all susceptible to thepossibility of fraud. Whether it be throughidentity theft, an attack on the family officetechnology systems, or even an employee’sunanticipated fraudulent behavior, thefamily office should proactively implementstrategies to mitigate the likelihood that oneof these actions will occur.Whether the family office is managing assets that the family desires to pass to futuregenerations or to achieve family members’ philanthropic goals, the preservation andsecurity of these assets is critical.2017 Essential Tax and Wealth Planning Guide Family office6

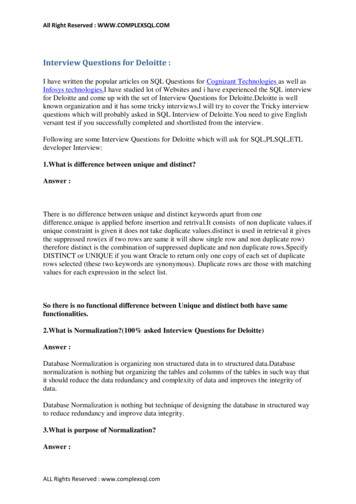

Download the third issueIntroductionEvaluating services tobe providedTransfer pricing in thefamily officeFraud in the family officeResourcesFamily officeEvaluating services to be providedOne of the most important decisions afamily office must make is identifying theservices the family office will provide. Thesecan vary widely, depending upon the family’sneeds and expectations, as well as theextent and complexity of assets managed.Most family offices coordinate an extensivearray of services for family members(Figure 1), using both in-house andexternal resources.Since wealthy families have numerousoptions for obtaining personal andfinancial services, one success factor informing a family office is to engage theright people to do the right work. Findingan optimal balance between servicesperformed in-house by competent familyoffice employees and those outsourced toqualified service providers is important forlong-term success. The family office shouldregularly reassess whether its servicesshould be insourced or outsourced. Overtime, new family members may be born andothers may pass, trusts may be created, andnew investments may be made. All of theselife events will impact how the family officechooses to serve its clients.Our experience with hundreds of familyoffices in the past decade has revealedthe following insights about insource vs.outsourced services (Figure 2 on next page): Many in-house services (dark blue)address daily activity at a granular level.Figure 1How would you describethe service offeringsof your SFO?28%Limited service72%Full service(investment management,legal, accounting, concierge, etc.)Source: Deloitte’s National Family Office Forum surveyKeeping these services in-houseprovides immediate access to, andcontrol over, the information. It is alsolikely to be more cost efficient andexpedient than outsourcing. Other services (light blue) may beperformed by family office staff, outsideproviders, or some combination of thetwo. This can offer the best of bothworlds—costs savings on work thatinvolves lower risk or is less complicatedand cutting-edge planning and qualityassurance for more complicated work.For some of these services, the familyoffice may initially rely on outsideproviders to establish core practicesor processes for the family office tofollow. Once the set-up is complete, thefamily office can hire talent to maintainthe processes that were established. The services outsourced most often(green) typically require highly specializedskills or significant infrastructure. In manyinstances, the services within this categoryrequire individuals to have deep technicalskills and experience with current tax andregulatory matters. Few family offices havethe appropriate structure, professionalsor resources to provide these servicesin-house from a risk-return perspective.2017 Essential Tax and Wealth Planning Guide Family office7

Download the third issueFamily officeEvaluating services to be providedFigure 2IntroductionEvaluating services tobe providedInsource vs. outsourced servicesTransfer pricing in thefamily officeFraud in the family officeResourcesFamily rcesTechnologyplatformRecordkeeping andrecordingOfficepolicies andproceduresTechnologycontrolsInsuranceTax and TaxcomplianceInvestmentmethodology —development/implementationFamilystrategies oldhelpCloudcomputingBudgetingand cashflow diligenceFamilyeducationFamily DuediligenceTravelCybersecurityMost often in-houseSometimes in-houseMost often outsourced2017 Essential Tax and Wealth Planning Guide Family office8

Download the third issueFamily officeEvaluating services to be providedTalent impacts the decisionIntroductionEvaluating services tobe providedTransfer pricing in thefamily officeFraud in the family officeResourcesThe decision to insource or outsourcespecific services may also be impacted bythe talent in the geographical area wherethe family office is located. For certainkey family office roles, it may be easy toidentify and attract talent to the familyoffice. However, for more junior roles,the family office may be competing fortalent with other family offices and willneed to consider alternative strategies toattract and retain talent. This may includeflexible work arrangements, increasedopportunities to work in different areas ofthe family office, and training opportunitiesto help talent continue to develop newskills. If the decision is made to insourcemany functions, investing in the talents’professional and technical skills will beimperative for the family office to remaincurrent and cutting edge.Each family office is as unique as thefamily it serves. In some situations, familymembers will want control over theinsourcing versus outsourcing decision.In other situations, transparency on thisissue is not necessary and family memberssimply require the services to be seamlesslydelivered. Regardless, in either situation,the family office will need to quantify thecost and the quality of any service that willbe delivered and determine whether itshould be insourced or outsourced. Thisassessment should be performed regularlyas significant life events occur. Furthermore,as new leaders join the family office orfamily members become more involved inthe family office, this offers an opportunityto reevaluate the services provided and toconfirm that services are executed in themost timely and cost effective manner, whileconsidering the family’s complexity andtolerance for risk.The decision to insource oroutsource specific servicesmay also be impactedby the talent in thegeographical area wherethe family office is located.2017 Essential Tax and Wealth Planning Guide Family office9

Download the third issueFamily officeTransfer pricing in the family officeIntroductionEvaluating services tobe providedWhile a family office is created to serve one ormultiple generations, the goal is to create a businessorganization that is appropriately compensated for thecustomized services it delivers to its clients.Transfer pricing in thefamily officeFraud in the family officeResourcesWhile a family office is created to serve oneor multiple generations, the goal is to createa business organization that is appropriatelycompensated for the customized servicesit delivers to its clients. Once the familyoffice determines the services it will provideto its clients, it must determine how muchit will charge for such services. In manyinstances, the family office is owned byfamily members or trusts for the benefit offamily members. Given the related partyinteractions between the family office andthe clients it serves, there is a risk thatthe Internal Revenue Service (IRS) couldchallenge the compensation charged by thefamily office for the services it provides.For example, pricing for services providedto family members that is lower than marketrates may result in a deemed gift betweenfamily members. Alternatively, pricing forservices provided to a private foundation orcharitable trust that is higher than marketrates could be interpreted to be an actof self-dealing, which may result in theimposition of an excise tax. As such, thefamily office and the clients it serves areboth motivated to determine market-basedcompensation that is comparable to thatcharged by an unrelated third party.The Treasury Regulations under section 482and section 6662 govern how to establishand document pricing between taxpayersunder common control (controlled servicetransactions). During an examination,the IRS may request the support anddocumentation for payments madebetween related parties. A transfer pricinganalysis and related documentation cansupport the pricing of services and mitigatepenalties if the IRS successfully challengesthe amounts charged. Risk mitigation isthe primary benefit of a transfer pricingstudy based on section 482 and section6662 guidance.2017 Essential Tax and Wealth Planning Guide Family office10

Download the third issueIntroductionEvaluating services tobe providedTransfer pricing in thefamily officeFamily officeTransfer pricing in the family officeWhat triggers transfer pricing considerations?Services provided by a family officeMany of the services a family office provides can be analyzed and documented using methods providedin Internal Revenue Code (IRC) section 482, yservicesConciergeservicesFraud in the family officeResourcesCommon family office structures and arrangementsThe diagram below is representative of many family office structures whereby the family office providesaccounting, administrative and investment management services to individuals, trusts, entities, andfoundations related to the family.Private trustcompany (PTC)Trustee servicesprovided by PTCfor a trustee feeAdministrativeservices providedby FO for a feeFamilymembersFamilyoffice (FO)Administrativeservices providedby FO for a rvices provided by FOfor management feeand/or profits allocationTrustsMarketable LPPrivate LP2017 Essential Tax and Wealth Planning Guide Family office11

Download the third issueIntroductionEvaluating services tobe providedTransfer pricing in thefamily officeFraud in the family officeResourcesFamily officeTransfer pricing in the family officeWhile a transfer pricinganalysis and relateddocumentation cansupport pricing ofservices and mitigatepenalties if the IRSsuccessfully challengesthe amounts charged, itcan also be a beneficialexercise to demonstrateto family membersand fiduciaries that theamounts they are payingfor services are consistentwith those that would becharged by an unrelatedthird party.Which method fits your family?Section 482 provides six alternativemethods that can be used to benchmarkand document transfer pricing for variouscontrolled services transactions. Once theright method for a service is determinedby the family office, the method should beapplied in a consistent and reliable manner.When completing a transfer pricing analysis,the first step involves interviews with familyoffice executives who provide services tofamily members or to entities controlled byfamily members. The purpose of this factgathering step is to understand the servicescurrently offered by the family office andto whom those services are provided, aswell as how the family office is currentlycompensated for its services. For newfamily offices that are just being created,this discussion will relate to the servicesthe family office plans to deliver to clients.Through these discussions, the family officeis able to identify the controlled servicestransactions that will be evaluated throughthe transfer pricing analysis.Once the controlled service transactionsare identified, the next step is to use variouspublic sources to identify and analyzeindustries that provide similar services tothe ones offered by the family office. Thisprocess helps to identify relevant marketbenchmarks for the services provided.All of this information is then used by thefamily office to select the best method todetermine the appropriate price for theservice(s) offered. After this analysis andidentification of the applicable methodoccurs, a transfer pricing report is preparedto summarize the controlled servicestransactions analysis, the industry analysis,the benchmarks selected and applied, andthe methods ultimately used to determinethe pricing for services.While a transfer pricing analysis andrelated documentation can support pricingof services and mitigate penalties if theIRS successfully challenges the amountscharged, it can also be a beneficial exerciseto demonstrate to family members andfiduciaries that the amounts they are payingfor services are consistent with those thatwould be charged by an unrelated thirdparty. In addition, it provides an opportunityto re-educate family members on theservices offered, as well as engage withthe family on how the talent employed bythe family office and third-party serviceproviders serve the family.Maintaining a family office may requiresignificant costs to rise to the level of thecustomization that the family office desires.A transfer pricing analysis may providecomfort to family members that the familyoffice is carefully managing these costs, whiledelivering valuable services to its clients.2017 Essential Tax and Wealth Planning Guide Family office12

Download the third issueIntroductionEvaluating services tobe providedTransfer pricing in thefamily officeFraud in the family officeResourcesFamily officeFraud in the family officeFamily office fraud is not often in the newsdue to the private nature of the industry,but fraud does occur. Many family officesserve as investment managers, givingemployees proximity to cash and otherassets. In addition, they are often smallorganizations, where a single employeecan have significant control over financesand be the sole person handling allcommunications to family members. Thesefactors, among others, make family officesprime targets for fraud.The overarching goal for fraud preventionis for the family to establish a culture thatvalues integrity and transparency andencourages employees to report anysuspicious activity. There are several stepsthat family offices can take to limit fraud, thefirst of which is to accept and acknowledgethat fraud is a real threat. Then familyoffices and family members should becomeeducated on fraud, perform periodic riskassessments within the family office, andstructure and train the staff to prevent fraud.Get educatedEmployees engaged in fraud have a clearpattern of behavior that family membersand other employees can be trainedto detect. For example, hallmarks ofembezzlers include a tendency to work verylong hours, often arriving before and leavingafter other employees. Embezzlers alsotend to work weekends and generally donot take long vacations. These are all signsof employees working hard to “cover theirtracks.” The challenge is that these traitscan also be characteristics of dedicatedemployees and are not in any way proofof a fraud. They are merely red flags andcan be a prompt for additional research.One simple technique is to require atleast two weeks of consecutive vacationfor all employees above a certain level orwith access to the cash ledger. It is verychallenging for an employee to keep a fraudhidden during a two-week absence fromthe office when another employee assumestheir duties. Another technique that canlimit fraud is periodic unannounced jobrotations that require employees to switchjob responsibilities.Perform a periodic fraud riskassessmentAnother good practice is to perform aperiodic test, not just of the controls, butalso of the entire operating environment.As mentioned, there are likely areas offraud, such as payroll, expense accounts,and accounts payable, which are mostoften abused. These can be examinedusing data analytics that will flag suspiciousactivity or unanticipated patterns, suchas an abundance of checks being writtenjust under a control level or invoices to asingle vendor that have been split to avoidthe additional oversight of higher checkamounts. The risk assessment does nothave to happen every year or even on aregular basis; however, it is considereda prudent use of a family’s resources toperform one periodically. Even if no fraudis uncovered, the clean bill of healthgives the family a level of comfort andpeace of mind.A risk assessment does not have to happen every year or evenon a regular basis; however, it is considered a prudent use of afamily’s resources to perform one periodically.2017 Essential Tax and Wealth Planning Guide Family office13

Download the third issueFamily officeFraud in the family officeSolve for the staffing problemIntroductionEvaluating services tobe providedTransfer pricing in thefamily officeFraud in the family officeResourcesOne common trait of family offices is thatmany have long-term employees. This isoften a sign of loyalty and a productivework environment, but it can also lead to anoverreliance on the trust and goodness ofhuman beings. For example, a family officewith trusted employees might not have theproper checks and balances in place forfinancial transactions. It can be challengingfor a family to impose proper checks andbalances when most employees are honest.However, one individual with too muchcontrol and access can cause an enormousamount of financial or reputational damage.The small staff at most family officesmakes establishing checks and balancesvery difficult. However, the segregation ofduties is one of the simplest ways a familyoffice can prevent fraud. For example, afamily office should consider separatingthe individuals who handle cash from thosewho record cash on the ledger, whichshould then be reconciled by another party.At first glance, this may seem like a tediousand unnecessary process, especially for asmaller family office that is trying to run ina lean and efficient manner. However, sucha system is a proven and effective way tocombat fraud and more likely will pay foritself many times over. Placing a family officeemployee in a situation where he or she hasaccess to cash, without the proper controls,can encourage fraudulent behavior. Eventhe most honest and trustworthy employeemay at times be under financial pressureand can find it challenging to resist takingadvantage of such a situation. Thesecontrols may feel inefficient to some andthat is because they are not meant to beefficient—they are meant to be effective. Ifthey are working well, fraud will have muchless opportunity to take root.The bottom lineThe best way to prevent fraud is to acceptthat it occurs and to make a decisionto prevent it. While it is often hard for afamily to accept that they are being takenadvantage of, experience shows that fraudis often perpetrated by trusted individuals.Once the fraud issue is a focus of the family,it is very possible to promote the cultureand controls designed to thwart it. Doingso does not have to be overly intrusive orexpensive; the solution is finding the rightbalance between trusting employees andverifying that they are being trustworthy.Family offices that do not make this a focusrisk serious financial and reputational harmto the family. In addition, family officesmay ultimately spend more time andeffort on damage control than theywould have in prevention.Looking into 2017While each family office is unique, theyare businesses that are offering tailoredservices to satisfy their clients’ needs whilebeing compensated for the high-touchdelivery that they provide. Reevaluating theservices that are offered, how the familyoffice is compensated for such services,and who should provide such services isone of the leading practices family officescan employ. In addition, family offices mayconsider performing a fraud assessmentto mitigate risk within the operatingenvironment. Family office leaders mustbe able to understand the challengesfaced, determine priorities and developand execute an action plan to addressthese matters.Once the fraud issue isa focus of the family, it isvery possible to promotethe culture and controlsdesigned to thwart it.2017 Essential Tax and Wealth Planning Guide Family office14

Download the third issueResourcesPrivate wealthPrivate Wealth: Sustain, enhance and protect your wealthTax policy and electionsTax News and ViewsIndividual income tax planningPrivate wealth tax controversies: Deep experience navigatinginteractions with taxing authoritiesWealth transfer planningWealth Planning: securing your legacyUS estate and gift tax rules for resident and nonresident aliensUnique investmentsArt & Finance: Art is your passion.Tax is oursPrivate aircraft: Flying private makes sense for those with the rightinformationPost-election tax policy updateTax policy decisions ahead: Impact of the 2016 electionsPost-mortem considerationsPost-mortem considerations — Keeping a complex process focusedPhilanthropyPrivate foundations: Establishing a vehicle for your charitable visionTax implications of fund investingInvestment Management Industry Outlook — Capitalizing onthree disruptive forces; Impact investing and hedge funds:A sustainable strategyFamily officeTransfer pricing for family officeTax controversies and the family officeGlobalizationTax planning for US individuals living abroad—2016Taxation of foreign nationals by the US—20162017 Essential Tax and Wealth Planning Guide Resources24

Download the third issueAbout DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private companylimited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL andeach of its member firms are legally separate and independent entities. DTTL (also referred toas “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about fora detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about fora detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain servicesmay not be available to attest clients under the rules and regulations of public accounting.Copyright 2017 Deloitte Tax LLC. All rights reserved.2017 Essential Tax and Wealth Planning Guide 25

chosen to form a single family office that is devoted to the personal needs and desires of the family. And regardless of how long a family office has been in existence, we consistently find that individuals and families want to assess the services the family office provides to the individuals, trusts, and entities ("clients") served by