Transcription

ANNUAL FINANCIAL REPORTJOHNSON COUNTY, TENNESSEEFOR THE YEAR ENDED JUNE 30, 2020DIVISION OF LOCAL GOVERNMENT AUDIT

ANNUAL FINANCIAL REPORTJOHNSON COUNTY, TENNESSEEFOR THE YEAR ENDED JUNE 30, 2020COMPTROLLER OF THE TREASURYJUSTIN P. WILSONDIVISION OF LOCAL GOVERNMENT AUDITJAMES R. ARNETTEDirectorMARK TREECE, CPA, CGFMAudit ManagerBRANDON HAMMESMORGAN HAMILTON-PIGGGREG BRUSH, CISAState AuditorsMARIE TIDWELL, CPAROBERT ANDERSON, CPA, CGFMSenior AuditorsThis financial report is available at www.comptroller.tn.gov2

JOHNSON COUNTY, TENNESSEETABLE OF CONTENTSExhibitPage(s)Summary of Audit Findings6INTRODUCTORY SECTION7Johnson County Officials8FINANCIAL SECTION9Independent Auditor's ReportBASIC FINANCIAL STATEMENTS:Government-wide Financial Statements:Statement of Net PositionStatement of ActivitiesFund Financial Statements:Governmental Funds:Balance SheetReconciliation of the Balance Sheet of Governmental Fundsto the Statement of Net PositionStatement of Revenues, Expenditures, and Changes inFund BalancesReconciliation of the Statement of Revenues, Expenditures,and Changes in Fund Balances of Governmental Fundsto the Statement of ActivitiesStatements of Revenues, Expenditures, and Changes in FundBalances - Actual (Budgetary Basis) and Budget:General FundHighway/Public Works FundFiduciary Funds:Statement of Fiduciary Assets and LiabilitiesIndex and Notes to the Financial StatementsREQUIRED SUPPLEMENTARY INFORMATION:Schedule of Changes in Net Pension Liability (Asset) and Related RatiosBased on Participation in the Public Employee Legacy Pension Planof TCRS – Primary GovernmentSchedule of Changes in Net Pension Liability (Asset) and Related RatiosBased on Participation in the Public Employee Pension Planof TCRS – Primary GovernmentSchedule of Contributions Based on Participation in the Public EmployeeLegacy Pension Plan of TCRS – Primary GovernmentSchedule of Contributions Based on Participation in the Public EmployeePension Plan of TCRS – Primary GovernmentSchedule of Contributions Based on Participation in the TeacherRetirement Plan of TCRS – Discretely Presented JohnsonCounty School DepartmentSchedule of Contributions Based on Participation in the TeacherLegacy Pension Plan of TCRS – Discretely Presented JohnsonCounty School DepartmentSchedule of Proportionate Share of the Net Pension Asset in theTeacher Retirement Plan of TCRS – Discretely PresentedJohnson County School -4105E-5106E-6107E-7108

Schedule of Proportionate Share of the Net Pension Liability (Asset) in theTeacher Legacy Pension Plan of TCRS – Discretely PresentedJohnson County School DepartmentSchedule of Changes in the Total OPEB Liability and Related RatiosLocal Government Plan - Primary GovernmentSchedule of Changes in the Total OPEB Liability and Related RatiosLocal Education Plan - Discretely Presented Johnson County School DepartmentNotes to the Required Supplementary InformationCOMBINING AND INDIVIDUAL FUND FINANCIALSTATEMENTS AND SCHEDULES:Nonmajor Governmental Funds:Combining Balance SheetCombining Statement of Revenues, Expenditures, and Changesin Fund BalancesSchedules of Revenues, Expenditures, and Changes in FundBalances – Actual (Budgetary Basis) and Budget:Public Library FundSolid Waste/Sanitation FundDrug Control FundGeneral Capital Projects FundMajor Governmental Fund:Schedule of Revenues, Expenditures, and Changes in FundBalance – Actual and Budget:General Debt Service FundFiduciary Funds:Combining Statement of Fiduciary Assets and LiabilitiesCombining Statement of Changes in Assets and Liabilities –All Agency FundsComponent Unit:Discretely Presented Johnson County School Department:Statement of ActivitiesBalance Sheet – Governmental FundsReconciliation of the Balance Sheet of Governmental Fundsto the Statement of Net PositionStatement of Revenues, Expenditures, and Changes in FundBalances – Governmental FundsReconciliation of the Statement of Revenues, Expenditures,and Changes in Fund Balances of Governmental Fundsto the Statement of ActivitiesCombining Balance Sheet – Nonmajor Governmental FundsCombining Statement of Revenues, Expenditures, and Changesin Fund Balances – Nonmajor Governmental FundsSchedules of Revenues, Expenditures, and Changes in FundBalances – Actual (Budgetary Basis) and Budget:General Purpose School FundSchool Federal Projects FundCentral Cafeteria FundOther Education Special Revenue 138139-140I-7141I-8I-9I-10I-11142-143144-145146147

Miscellaneous Schedules:Schedule of Changes in Bonds and Capital LeasesSchedule of Long-term Debt Requirements by YearSchedule of Transfers – Primary Government and DiscretelyPresented Johnson County School DepartmentSchedule of Salaries and Official Bonds of Principal Officials –Primary Government and Discretely Presented JohnsonCounty School DepartmentSchedule of Detailed Revenues – All Governmental Fund TypesSchedule of Detailed Revenues – All Governmental Fund Types –Discretely Presented Johnson County School DepartmentSchedule of Detailed Expenditures – All Governmental Fund TypesSchedule of Detailed Expenditures – All Governmental Fund Types –Discretely Presented Johnson County School DepartmentSchedule of Detailed Receipts, Disbursements, and Changes inCash Balance – City Agency 3-164J-6J-7165-168169-186J-8187-201J-9202203SINGLE AUDIT SECTIONAuditor's Report on Internal Control Over Financial Reporting and onCompliance and Other Matters Based on an Audit of FinancialStatements Performed in Accordance With GovernmentAuditing StandardsAuditor's Report on Compliance for Each Major Federal Program; Reporton Internal Control Over Compliance; and Report on the Schedule ofExpenditures of Federal Awards Required by Uniform GuidanceSchedule of Expenditures of Federal Awards and State GrantsSummary Schedule of Prior-year FindingsSchedule of Findings and Questioned CostsManagement's Corrective Action PlanBest Practice5204-205206-208209-211212213-218219-224225

Summary of Audit FindingsAnnual Financial ReportJohnson County, TennesseeFor the Year Ended June 30, 2020ScopeWe have audited the basic financial statements of Johnson County as of and for the yearended June 30, 2020.ResultsOur report on Johnson County’s financial statements is unmodified.Our audit resulted in four findings and recommendations, which we have reviewed withJohnson County management. Detailed findings, recommendations, and management’sresponses are included in the Single Audit section of this report.FindingsThe following are summaries of the audit findings:OFFICES OF COUNTY MAYOR, DIRECTOR OF SCHOOLS, ROADSUPERINTENDENT AND DIRECTOR OF ACCOUNTS AND BUDGETS The offices had deficiencies in purchasing procedures.OFFICE OF CIRCUIT AND GENERAL SESSIONS COURTS CLERK A cash overdraft occurred during the year in General Sessions Court.OFFICE OF CLERK AND MASTER Special commissioner fees exceeded the percentage authorized by state statute.OFFICE OF ASSESSOR OF PROPERTY The assessor did not maintain an adequate program of visual inspections.6

INTRODUCTORY SECTION7

Johnson County OfficialsJune 30, 2020OfficialsMike Taylor, County MayorJeff Wagner, Road SuperintendentMischelle Simcox, Director of SchoolsLisa Crowder, TrusteeMatthew Lewis, Assessor of PropertyTammie Fenner, County ClerkMelissa Hollaway, Circuit and General Sessions Courts ClerkSherrie Fenner, Clerk and MasterFreida May Gwinn, Register of DeedsEdward Tester, SheriffDustin Shearin, Purchasing AgentRussell Robinson, Director of Accounts and BudgetsBoard of County CommissionersRick Snyder, ChairmanBill AdamsBerna ArnoldEugene CampbellJerry GentryRobert GrindstaffEvelyn HillJimmy LoweScott MastGina MeadeMegan McEwenDavid McQueenJoey NorrisFreddy PhippsTommy PooreBoard of EducationHoward Carlton, ChairmanKevin LongGary MathesonMike PayneJo Ann ReeceAudit CommitteeSally Snyder, ChairmanEugene CampbellGina Meade8

FINANCIAL SECTION9

Independent Auditor's ReportJohnson County Mayor andBoard of County CommissionersJohnson County, TennesseeTo the County Mayor and Board of County Commissioners:Report on the Financial StatementsWe have audited the accompanying financial statements of the governmental activities, the aggregatediscretely presented component units, each major fund, and the aggregate remaining fund informationof Johnson County, Tennessee, as of and for the year ended June 30, 2020, and the related notes to thefinancial statements, which collectively comprise the county’s basic financial statements as listed in thetable of contents.Management's Responsibility for the Financial StatementsManagement is responsible for the preparation and fair presentation of these financial statements inaccordance with accounting principles generally accepted in the United States of America; this includesthe design, implementation, and maintenance of internal control relevant to the preparation and fairpresentation of financial statements that are free from material misstatement, whether due to fraud orerror.Auditor's ResponsibilityOur responsibility is to express opinions on these financial statements based on our audit. We conductedour audit in accordance with auditing standards generally accepted in the United States of America andthe standards applicable to financial audits contained in Government Auditing Standards, issued by theComptroller General of the United States. Those standards require that we plan and perform the auditto obtain reasonable assurance about whether the financial statements are free from materialmisstatement.An audit involves performing procedures to obtain audit evidence about the amounts and disclosures inthe financial statements. The procedures selected depend on the auditor's judgment, including theassessment of the risks of material misstatement of the financial statements, whether due to fraud orerror. In making those risk assessments, the auditor considers internal control relevant to the entity'spreparation and fair presentation of the financial statements in order to design audit procedures thatare appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectivenessof the entity's internal control. Accordingly, we express no such opinion. An audit also includes evaluatingthe appropriateness of accounting policies used and the reasonableness of significant accounting10

estimates made by management, as well as evaluating the overall presentation of the financialstatements.We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour audit opinions.OpinionsIn our opinion, the financial statements referred to above present fairly, in all material respects, therespective financial position of the governmental activities, the aggregate discretely presentedcomponent units, each major fund, and the aggregate remaining fund information of Johnson County,Tennessee, as of June 30, 2020, and the respective changes in financial position thereof and the respectivebudgetary comparison for the General and Highway/Public Works funds for the year then ended inaccordance with accounting principles generally accepted in the United States of America.Other MattersRequired Supplementary InformationManagement has omitted the management’s discussion and analysis that accounting principles generallyaccepted in the United States of America require to be presented to supplement the basic financialstatements. Such missing information, although not a part of the basic financial statements, is requiredby the Governmental Accounting Standards Board, who considers it to be an essential part of financialreporting for placing the basic financial statements in an appropriate operational, economic, or historicalcontext. Our opinion on the basic financial statements is not affected by this missing information.Accounting principles generally accepted in the United States of America require that the schedules ofchanges in the county’s net pension liability and related ratios, schedules of county and schoolcontributions, schedules of school’s proportionate share of the net pension liability, and schedules ofcounty and school changes in the total other postemployment benefits liability and related ratios, aslisted in the table of contents, be presented to supplement the basic financial statements. Suchinformation, although not a part of the basic financial statements, is required by the GovernmentalAccounting Standards Board who considers it to be an essential part of financial reporting for placingthe basic financial statements in an appropriate operational, economic, or historical context. We haveapplied certain limited procedures to the required supplementary information in accordance withauditing standards generally accepted in the United States of America, which consisted of inquiries ofmanagement about the methods of preparing the information and comparing the information forconsistency with management's responses to our inquiries, the basic financial statements, and otherknowledge we obtained during our audit of the basic financial statements. We do not express an opinionor provide any assurance on the information because the limited procedures do not provide us withsufficient evidence to express an opinion or provide any assurance.Supplementary and Other InformationOur audit was conducted for the purpose of forming opinions on the financial statements that collectivelycomprise Johnson County’s basic financial statements. The combining and individual nonmajor fundfinancial statements, budgetary comparison schedules of nonmajor governmental funds and the GeneralDebt Service Fund, combining and individual fund financial statements of the Johnson County SchoolDepartment (a discretely presented component unit), miscellaneous schedules and other informationsuch as the introductory section are presented for purposes of additional analysis and are not a requiredpart of the basic financial statements. The schedule of expenditures of federal awards is also presented11

for purposes of additional analysis as required by Title 2 U.S. Code of Federal Regulations Part 200,Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, andis not a required part of the basic financial statements.The combining and individual nonmajor fund financial statements, budgetary comparison schedules ofnonmajor governmental funds and the General Debt Service Fund, combining and individual fundfinancial statements of the Johnson County School Department (a discretely presented component unit),schedule of expenditures of federal awards, and miscellaneous schedules are the responsibility ofmanagement and were derived from and relate directly to the underlying accounting and other recordsused to prepare the basic financial statements. Such information has been subjected to the auditingprocedures applied in the audit of the basic financial statements and certain additional procedures,including comparing and reconciling such information directly to the underlying accounting and otherrecords used to prepare the basic financial statements or to the basic financial statements themselves,and other additional procedures in accordance with auditing standards generally accepted in the UnitedStates of America. In our opinion, the combining and individual nonmajor fund financial statements,budgetary comparison schedules of nonmajor governmental funds and the General Debt Service Fund,combining and individual fund financial statements of the Johnson County School Department (adiscretely presented component unit), schedule of expenditures of federal awards, and miscellaneousschedules are fairly stated in all material respects in relation to the basic financial statements as a whole.The introductory section has not been subjected to the auditing procedures applied in the audit of thebasic financial statements, and accordingly, we do not express an opinion or provide any assurance on it.Other Reporting Required by Government Auditing StandardsIn accordance with Government Auditing Standards, we have also issued our report dated October 30,2020, on our consideration of Johnson County’s internal control over financial reporting and on our testsof its compliance with certain provisions of laws, regulations, contracts, and grant agreements and othermatters. The purpose of that report is solely to describe the scope of our testing of internal control overfinancial reporting and compliance and the results of that testing, and not to provide an opinion on theeffectiveness of Johnson County’s internal control over financial reporting or on compliance. That reportis an integral part of an audit performed in accordance with Government Auditing Standards inconsidering Johnson County’s internal control over financial reporting and compliance.Very truly yours,Justin P. WilsonComptroller of the TreasuryNashville, TennesseeOctober 30, 2020JPW/tg12

BASIC FINANCIAL STATEMENTS13

Exhibit AJohnson County, TennesseeStatement of Net PositionJune 30, y in Pooled Cash and InvestmentsAccounts ReceivableDue from Other GovernmentsProperty Taxes ReceivableAllowance for Uncollectible Property TaxesPrepaid ItemsRestricted Assets:Amounts Accumulated for OPEB BenefitsAmounts Accumulated for Pension BenefitsNet Pension Asset - Agent PlanNet Pension Asset - Agent Plan - LegacyNet Pension Asset - Teacher Retirement PlanNet Pension Asset - Teacher Legacy Pension PlanCapital Assets:Assets Not Depreciated:LandConstruction in ProgressAssets Net of Accumulated Depreciation:Buildings and ImprovementsInfrastructureOther Capital AssetsTotal Assets 38,36711,208,82137,325877,6963,948,895(84,828)0 26727,159,851 DEFERRED OUTFLOWS OF RESOURCESDeferred Charge on RefundingPension Changes in ExperiencePension Changes in AssumptionsPension Contributions after Measurement DatePension Changes in ProportionOPEB Changes in ExperienceOPEB Changes in AssumptionsOPEB Benefits Paid after Measurement DateTotal Deferred Outflows of Resources 306,51528,00975,382218,18201,55211,809977642,426 258,3803,77978,16713,2465,55643,524 3,507,706LIABILITIESAccounts PayableAccrued PayrollPayroll Deductions PayableAccrued Interest PayableDue to State of TennesseeOther Current Liabilities 40,6094,046445,1170058,030(Continued)14

Exhibit AJohnson County, TennesseeStatement of Net Position rimaryGovernmentGovernmentalActivitiesLIABILITIES (Cont.)Noncurrent Liabilities:Due Within One Year - DebtDue Within One Year - OtherDue in More Than One Year - DebtDue in More Than One Year - OtherTotal Liabilities 950,173309,3767,073,8381,006,8079,742,846 047,15904,900,6005,495,561DEFERRED INFLOWS OF RESOURCESDeferred Current Property TaxesPension Changes in ExperienceNet Pension Changes in Investment EarningsPension Changes in ProportionOPEB Changes in ExperienceOPEB Changes in AssumptionsOPEB Changes in ProportionTotal Deferred Inflows of Resources 3,745,723206,280177,4940159,27268,32404,357,093 ,0938,493,096Net Investment in Capital AssetsRestricted for:General GovernmentFinanceAdministration of JusticePublic SafetyPublic Health and WelfareHighwaysEducationPensionsCapital OutlayUnrestricted 9,479,553 13,564,196Total Net Position NET 309,5101,436,1535,149,387The notes to the financial statements are an integral part of this 369,450) 16,678,900

Exhibit BJohnson County, TennesseeStatement of ActivitiesFor the Year Ended June 30, 2020Functions/ProgramsPrimary Government:Governmental Activities:General GovernmentFinanceAdministration of JusticePublic SafetyPublic Health and WelfareSocial, Cultural, and Recreational ServicesAgriculture and Natural ResourcesHighwaysEducationInterest on Long-term DebtExpensesCharges forServicesNet (Expense) Revenue andChanges in Net ySchoolGovernmentalActivitiesDepartmentProgram RevenuesOperatingCapitalGrants andGrants andContributionsContributions 1,953,060 107750217,253797,569 457,239341,719760,205564,5247,58806,18800123,179 00008,246043,65800 ,367)(115,680)(260,091)(750)(136,818) 0000000000Total Primary Government 11,183,567 2,935,032 2,895,951 445,689 (4,906,895) 0Component Unit:Johnson County School Department 21,082,864 440,633 3,889,120 0 0 (16,753,111)Total Component Unit 21,082,864 440,633 3,889,120 0 0 (16,753,111)(Continued)16

Exhibit BJohnson County, TennesseeStatement of Activities (Cont.)Functions/ProgramsExpensesCharges forServicesGeneral Revenues:Taxes:Property Taxes Levied for General PurposesProperty Taxes Levied for Debt ServiceLocal Option Sales TaxesHotel/Motel TaxWheel TaxLitigation Tax - GeneralLitigation Tax - Special PurposeLitigation Tax - Jail, Workhouse, or CourthouseBusiness TaxMixed Drink TaxMineral Severance TaxWholesale Beer TaxGrants and Contributions Not Restricted to Specific ProgramsUnrestricted Investment IncomeGain on InvestmentsMiscellaneousGain on Disposal of Capital AssetsTotal General RevenuesNet (Expense) Revenue andChanges in Net ySchoolGovernmentalActivitiesDepartmentProgram RevenuesOperatingCapitalGrants andGrants andContributionsContributions ,243,136 ,026018,470,602Change in Net PositionNet Position, July 1, 2019 1,336,24116,664,923 1,717,49114,961,409Net Position, June 30, 2020 18,001,164 16,678,900The notes to the financial statements are an integral part of this statement.17

Exhibit C-1Johnson County, TennesseeBalance SheetGovernmental FundsJune 30, 2020NonmajorFundsOtherGovernmentalFundsMajor FundsGeneralASSETSHighway dsCashEquity in Pooled Cash and InvestmentsAccounts ReceivableDue from Other GovernmentsDue from Other FundsProperty Taxes ReceivableAllowance for Uncollectible Property TaxesRestricted Assets 30,001 6,816 1,174,255428331,90400000 6,215,691026,669111,112530,944(11,406)01,550 2137,325877,696112,1923,948,895(84,828)31,713Total Assets 5,609,248 1,513,403 6,873,010 2,174,520 16,170,181 230,377 3,77961,805111,1124,79730,001441,871 2,966 016,36207596,81726,904 0 000000 25,037 001,08006,70632,823 07 86,80648,7533,094,366 0 0171,941171,941 503,626 14,77616,170534,572 283,290 8,3113,908295,509 s PayableAccrued PayrollPayroll Deductions PayableDue to Other FundsDue to State of TennesseeOther Current LiabilitiesTotal Liabilities DEFERRED INFLOWS OF RESOURCESDeferred Current Property TaxesDeferred Delinquent Property TaxesOther Deferred/Unavailable RevenueTotal Deferred Inflows of Resources (Continued)18

Exhibit C-1Johnson County, TennesseeBalance SheetGovernmental Funds (Cont.)NonmajorFundsOtherGovernmentalFundsMajor FundsGeneralFUND BALANCESRestricted:Restricted for General GovernmentRestricted for FinanceRestricted for Administration of JusticeRestricted for Public SafetyRestricted for Public Health and WelfareRestricted for Capital OutlayRestricted for Hybrid Retirement Stabilization FundsCommitted:Committed for Public Health and WelfareCommitted for Social, Cultural, and Recreational ServicesCommitted for Highways/Public WorksCommitted for Capital OutlayCommitted for Debt ServiceAssigned:Assigned for General GovernmentAssigned for Public SafetyAssigned for Highways/Public WorksUnassignedTotal Fund BalancesTotal Liabilities, Deferred Inflows of Resources, and Fund BalancesHighway /PublicWorks 177,672 65,97179,09495,64326,770031,713000000 000000GeneralDebtService0 000000TotalGovernmentalFunds0 ,314,5587,4916,338,438001,314,5580000006,338,438 356,131387,772247851,9982,073,011 00001,314,558 00006,338,438 00001,846,188 356,131387,772247851,99811,572,195 5,609,248 1,513,403 6,873,010 2,174,520 16,170,181The notes to the financial statements are an integral part of this statement.19

Exhibit C-2Johnson County, TennesseeReconciliation of the Balance Sheet of Governmental Fundsto the Statement of Net PositionJune 30, 2020Amounts reported for governmental activities in the statementof net position (Exhibit A) are different because:Total fund balances - balance sheet - governmental funds (Exhibit C-1)(1) Capital assets used in governmental activities are notfinancial resources and therefore are not reported inthe governmental funds.Add: landAdd: buildings and improvements net of accumulated depreciationAdd: infrastructure net of accumulated depreciationAdd: other capital assets net of accumulated depreciation(2) Long-term liabilities are not due and payable in the currentperiod and therefore are not reported in the governmental funds.Less: bonds payableLess: capital leases payableAdd: deferred amount on refundingLess: compensated absences payableLess: landfill postclosure care costsLess: other postemployment benefits liabilityLess: accrued interest on bondsLess: other deferred revenue - premium on debt(3) Amounts reported as deferred outflows of resources and deferredinflows of resources related to pensions and OPEB will be amortized andrecognized as components of pension and OPEB expense in future years.Add: deferred outflows of resources related to pensionsLess: deferred inflows of resources related to pensionsAdd: deferred outflows of resources related to OPEBLess: deferred inflows of resources related to OPEB(4) Net pension assets of the agent plans are not current financialresources and therefore are not reported in the governmental funds.Add: net pension asset - agent planAdd: net pension asset - agent plan - legacy 27,596)(275,459)3,7811,274,0161,277,797(5) Other long-term assets are not available to pay forcurrent-period expenditures and therefore are deferredin the governmental funds.350,665 Net position of governmental activities (Exhibit A)The notes to the financial statements are an integral part of this statement.2011,572,19518,001,164

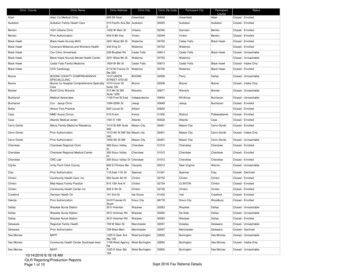

Exhibit C-3Johnson County, TennesseeStatement of Revenues, Expenditures,and Changes in Fund BalancesGovernmental FundsFor the Year Ended June 30, 2020NonmajorFundsOtherGovernmentalFundsMajor FundsHighway /PublicWorksGeneralRevenuesLocal TaxesLicenses and PermitsFines, Forfeitures, and PenaltiesCharges for Current ServicesOther Local RevenuesFees Received From County OfficialsState of TennesseeFederal GovernmentOther Governments and Citizens GroupsTotal Revenues ExpendituresCurrent:General GovernmentFinanceAdministration of JusticePublic SafetyPublic Health and WelfareSocial, Cultural, and Recreational ServicesAgriculture and Natural ResourcesOther OperationsHighwaysDebt Service:Principal on DebtInterest on DebtOther Debt Service GeneralDebtServiceTotalGovernmentalFunds3,666,657 8,8247,840,525 243,227 00044,94002,173,03178,0914432,539,732 902,085 000001,6820264,1541,167,921 374,436 032,873577,653119,261061,4522,44083,7591,251,874 01655,980587,18012,800,052635,303 33959,9640 00000003,205,0450 00000000122 24918,151(Continued)21

Exhibit C-3Johnson County, TennesseeStatement of Revenues, Expenditures,and Changes in Fund BalancesGovernmental Funds (Cont.)NonmajorFundsOtherGovernmentalFundsMajor FundsGeneralHighway dsExpenditures (Cont.)Capital ProjectsTotal Expenditures 0 7,490,932 0 3,313,795 0 1,049,201 259,400 1,000,313 Excess (Deficiency) of RevenuesOver Expenditures 349,593 (774,063) 118,720 251,561 (54,189) 0 11,6610011,661 149,200 7,32458,6100215,134 0 0000 0 00(58,610)(58,610) 149,20018,98558,610(58,610)168,185Other Financing Sources (Uses)Capital Leases IssuedInsurance RecoveryTransfers InTransfers OutTotal Other Financing Sources (Uses) 259,40012,854,241Net Change in Fund BalancesFund Balance, July 1, 2019 361,254 1,711,757(558,929) 1,873,487118,720 6,219,718192,951 1,653,237113,99611,458,199Fund Balance, June 30, 2020 2,073,011 1,314,558 6,338,438 1,846,188 11,572,195The notes to the financial statements are an integral part of this statement.22

Exhibit C-4Johnson County, TennesseeReconciliation of the Statement of Revenues, Expenditures, andChanges in Fund Balances of Governmental Funds to theStatement of ActivitiesFor the Year Ended June 30, 2020Amounts reported for governmental activities in the statementof activit

Johnson County, Tennessee For the Year Ended June 30, 2020 . Scope . We have audited the basic financial statements of JohnsonCounty as of and for the year ended June 30, 2020. Results . Our report on Johnson County's financial statements is unmodified. Our audit resulted in four findings and recommendations, which we have reviewed with