Transcription

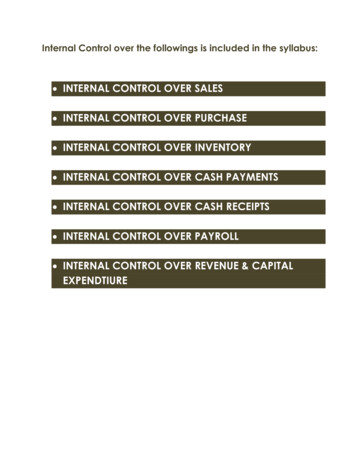

Internal Control over the followings is included in the syllabus: INTERNAL CONTROL OVER SALES INTERNAL CONTROL OVER PURCHASE INTERNAL CONTROL OVER INVENTORY INTERNAL CONTROL OVER CASH PAYMENTS INTERNAL CONTROL OVER CASH RECEIPTS INTERNAL CONTROL OVER PAYROLL INTERNAL CONTROL OVER REVENUE & CAPITALEXPENDTIURE

Internal Control over SalesAssertionControl objectives One person is notOccurrenceresponsible for takingand existenceControlsTests of controls Segregation of duties. Observe and evaluatewhether propersegregation of duties isoperating.orders, recordingsales and receivingpayments. Recorded sales Sales recorded onlytransactions representapproved sales ordergoods shipped.form and shippingdocumentation. Goods and servicesare only supplied tocustomers with goodcredit ratings. Test a sample of salesinvoices for authorizedsales order form andshippingdocumentation. Examine applicationcontrols forauthorization. Accounting for Review and test entity’snumerical sequences ofprocedures forinvoices.accounting fornumerical sequences of Monthly customerinvoices.statements sent out and Review entity’scustomer queries andprocedures for sendingcomplaints handledout monthlyindependently.statements and dealingwith customer queries Authorization of creditand complaints.terms to customers Review entity’s(senior staffprocedures for grantingauthorization,credit to customers.references/credit checksfor new customers,regular review of creditlimits) Authorization by senior

staff required forchanges in othercustomer data such asaddress etc. Orders not acceptedunless credit limitsreviewed first. Goods and servicesare provided atauthorized prices andon authorized terms. Customers areencouraged to paypromptly.Completeness All revenue relating togoods dispatched isrecorded. All goods and servicessold are correctlyinvoiced. Authorized price listsand specified terms oftrade in place. Examine a sample ofsales orders forevidence of propercredit approval by theappropriate senior staffmember. Examine applicationcontrols for creditlimits. Review all newcustomer files toensure satisfactorycredit reference havebeen obtained. Compare prices andterms on a sample ofsales invoices to theauthorized price listand terms of trade. Examine applicationcontrols for authorizedprices and terms. Accounting for Review and test entity’snumerical sequences ofprocedures forinvoices.accounting fornumerical sequences ofinvoices. Shippingdocumentation ismatched to salesinvoices. Sales invoices arereconciled to the daily Trace a sample ofshipping documents tothe sales invoices andledger. Review a sample ofreconciliations

AccuracyCut-offClassification All sales andadjustments arecorrectly journalized,summarized andposted to the correctaccounts. Transactions havebeen recorded in thecorrect period. All transactions areproperly classified inaccounts.sales report. An open-order file ismaintained andreviewed regularly. Sales invoices andmatching documentsrequired for all entries. All shippingdocumentation isforwarded to theinvoicing section on adaily basis. Daily invoicing of goodsshipped. Charts of accounts inplace. Codes in place fordifferent types ofproducts or services.performed. Inspect the open-orderfile for unfiled orders. Vouch recorded sales tosupporting documents. Compare dates on salesinvoices with dates ofcorrespondenceshippingdocumentation. Compare dates on salesinvoices with datesrecorded in the salesledger. Review sales ledger forproper classification. Examine a sample ofsales invoices forproper classification. Test applicationcontrols for propercodes.

Internal Control over PurchasesAssertionControl objective Recorded purchasesOccurrencerepresent goods andand existenceservices received.Completeness All purchasetransactions thatoccurred have beenrecorded.ControlsTests of controls Authorization Inspect policies andprocedures and policiesprocedures and inquirein place for orderingabout them.goods and services. Observe and evaluate Segregation of duties.segregation of duties. Purchase orders raised Examine a sample offor each purchase andpurchase orders toauthorized byensure they have beenappropriate seniorappropriatelypersonnel.authorized. Review the delegatedlist of authority forpurchases. Approved purchase For a sample of orders,order for each receiptexamine the goodsof goods.received note (GRN)and match it to theorder. Staff receiving goods; Observe receipt ofcheck them to thegoods by staff topurchase order.confirm whether thecheck is done. Stores clerks sign for Inspect a sample togoods received.confirm whether storesstaff undertakes thischeck. Purchase orders and Examine supportingGRNs are matched withdocumentation for athe suppliers’ invoices.sample of invoices. Purchase orders and Examine supportingGRNs are matched withdocumentation for athe suppliers’ invoices.sample of invoices. Periodic accounting for Review entity’s

pre-numbered GRNsand purchase orders. Independent check of amount recorded in thepurchase journal. Rights andobligationsAccuracy,classificationand valuation Recorded purchasesrepresent theliabilities of the entity. Purchase transactionsare correctly recordedin the accountingsystem. Purchase orders and GRNs are matched withthe suppliers’ invoices. Purchase orders and GRNs are matched withthe suppliers’ invoices. Mathematical accuracy of the supplier‘s invoiceis verified. Amount posted togeneral ledger isreconciled to thepurchase ledger. Chart of accounts inplace.Cut-off Purchase transactionsare recorded in thecorrect accountingperiod. All goods receivedreports forwarded toaccounts payabledepartment daily. Procedures in placethat require recordingof purchases as soon aspossible aftergoods/servicesreceived. procedures foraccounting for prenumbered documents.Examine applicationcontrols.Examinedocumentation forevidence of this check.Examine supportingdocumentation for asample of invoices.Examine supportingdocumentation for asample of invoices.Recalculate themathematical accuracyof a sample ofsuppliers’ invoices.Review reconciliationsfor evidence of thischeck. Review purchasesjournal and generalledger forreasonableness. Compare dates onreports to dates onrelevant vouchers. Compare dates onvouchers with datesthey were recorded inthe purchase journal.

Internal Control over InventoryAssertionControl objectivesOccurrence All inventoryand existencemovements areauthorized andrecorded.ControlsTest of controls Pre-numbered Reviewdocumentation suchdocumentation inas GDNs and GRNs inuse.use. Reconciliations of Review a sample ofinventory recordsreconciliations towith general ledger.confirm they areperformed and thenreviewed by anindependent person. Segregation of Observe andduties.evaluate propersegregation ofduties. Inventory included Physical safeguardson the statementin place to ensureof financial positioninventory is notphysical exists.stolen. Separateresponsibilities formaintenance ofrecords andcustodianship. Inventory countedregularly. Review securitysystems in place(e.g. lockedwarehouse, CCTVetc). Review policies andprocedures in place;discuss procedureswith relevant staff. Review proceduresfor countinginventory. Attend inventorycount.

Completeness All purchases and Procedures in placesales of inventoryto include inventoryhave beenheld at third partiesrecorded in theand excludeaccounting system.inventory held onconsignment forthird parties. Reconciliations ofaccounting recordswith physical withphysical inventory.Rights andobligations Inventory recordsonly include itemsthat belong to theentity.Accuracy, Inventoryclassificationquantities haveand valuationbeen accuratelydetermined. Inventory isproperly stated atthe lower of costand net realizable Procedures in placeto include inventoryheld at third partiesand excludeinventory held onconsignment forthird parties. Periodic or annualcomparison ofinventory withamounts shown incontinuous(perpetual)inventory records. Standard costsreviewed bymanagement. Review entity’sprocedures relatingto consignmentinventory. Reviewreconciliationsperformed andwhether reviewedby independentperson. Review entity’sprocedures relatingto consignmentinventory. Review and testentity’s proceduresfor taking physicalinventory. Review and testentity’s proceduresfor developingstandard costs.

Review the costaccumulation andvariance reports. Inventory managersreview inventoryregularly to identityslow-moving,obsolete and excessinventory. All purchases and All dispatchsales of inventorydocumentsare recorded in theprocessed daily tocorrect accountingrecord the dispatchperiod.of finished goods. All goods inwardsreports processeddaily to record thereceipt of inventory. Reconciliations ofinventory recordswith general tions Inventory Orders for materialstransactions andand production databalances areforms used toproperly identifiedprocess goodsand classified in thethroughfinancialmanufacturing.statements. Inspect variancereports produced. Discuss withinventory managershow this is done. Observe theprocedures beingperformed. Inspectdocumentation toconfirm dailyprocessing. Inspectdocumentation toconfirm dailyprocessing. Reviewreconciliationsperformed. Review entity’sprocedures anddocumentation usedto classify inventory. Disclosures relating Approvals by finance Review entity’sto classification anddirector.working papers for

valuation aresufficient.evidence.

Internal Control over PayrollAssertionControl objectives ControlsTests of controls Payment is made Segregation of duties Observe and evaluateOccurrenceonly to bona fidebetween HR and payrollproper segregation ofand existenceemployees of theentity.functions. Personnel files held forall employees. Authorizationprocedures for hiring,terminating, timeworked, wage rates,overtime, benefits etc. Any changes inemployment status ofemployees (e.g.maternity, special leaveetc) informed to HumanResources department. Use of time clocks torecord time worked. Clock cards approved bysupervisor. duties.Review a sample ofstarters and leavers inthe year to ensurecorrectdocumentation is inplace.Review and testauthorizationprocedures in place.Review policies andprocedures in placefor charging status andconsider whetheradequate.Review personnel filesfor a sample ofemployees whosestatus changed in theyear. Observe employees’use of time clock. Inspect a sample ofclock cards forevidence of approvalby appropriate level Only employees withmanagers.valid employee numbers Review and testare paid.procedures forentering and removingemployee numbers

Payroll budgets in placeand reviewed bymanagement.Completeness All payroll costs arerecorded for workdone by employees. Pre-numbered clockcards in use. from the payrollmaster file. Review budgetingprocedures. Review numericalsequence of clockcards.Segregation of duties. Observe and evaluateproper segregation ofAuthorization of wageduties.cheque cashedIf wages are paid in cash Encashment ofcheque. Attend the pay-out of Security of paywages to confirm thatpackets.the official procedures Security of transit.are being followed. Security and Before the wages areprompt bankingpaid compare payrollof unclaimedwith wages packets towages.ensure all employeesVerification ofhave a wage packet.distributions.Preparation andauthorization ofcheques and banktransfer lists. Examine receipts givenComparison of chequeby employees; checkand bank transfer listunclaimed wages arewith payroll.recorded in unclaimedMaintenance andwages book.reconciliation of wages Observe whether anyand salaries bankemployee receiveaccount.more than one wagePreparation andpacket.authorization of cheque Inspect the unclaimedand bank transfer list.wages book entriesComparison of cheques

and bank transfer listwith payroll.with the entries on thepayroll to ensure theyagree. Maintenance and Check that unclaimedreconciliation of wageswages are bankedand salary bank account.regularly by inspectionof bank statementsand supportingdocumentation. Inspect that unclaimedwages books to checkit shows reasons whywages are unclaimed. Review pattern ofunclaimed wages inunclaimed wage book;variations mayindicate failure torecord.Holiday pay Verify a sample ofpayments with theunderlying recordsand check thecalculation of theamounts paid byrecalculation. For salaries, reviewwhether comparisonsare being madebetween paymentrecords. Examine paid chequesor a certified copy ofthe bank list foremployees paid bycheque or bank

Accuracy,classificationand valuation All benefits anddeductions (tax,pension etc) arecomputed correctly. Verification of payrollamounts and benefitscalculations. Payroll budgets in placeand reviewed bymanagement. Agreement of grossearnings and total taxdeducted with taxationreturns. Payroll transactions Changes to mastercorrectly recorded inpayroll file verifiedthe accountingthrough before andsystem.after reports. Payroll master filereconciled to generalledger.Cut-off Payroll transactionsare recorded in thecorrect accountingperiod. All starters, leavers,changes to salaries anddeductions are reportedpromptly to payrolldepartment andchanges are updated tothe payroll master filepromptly. Chart of accounts.Presentationanddisclosureassertions Payroll transactionsare properlyclassified in the Independent approvalfinancial statements.and review of accountscharged to payroll. Payroll budgets in placetransfer. Recalculate benefitsand deductions for asample of employees. Review budgetingprocedures. Inspectdocumentation forevidence ofmanagement’s review. Review reconciliationbefore and afterreports to payrollmaster file. Review reconciliationpayroll master file togeneral ledger.Confirm whetherdiscrepancies arefollowed-up promptlyand resolved. Review entity’sprocedures forreporting changes tothe payrolldepartment. Check sample ofstarters and leavers. Review chart ofaccounts. Review procedures forclassifying payrollcosts. Review budgeting

and reviewed bymanagement.procedures.

Internal Control over Cash ReceiptsAssertionOccurrenceControl objectivesControlsTests of controls All valid cash receiptsare received anddeposited. Segregation of duties. Observe and evaluateproper segregation ofduties. Examine applicationcontrols for electroniccash receipts transfer. Review monthly bankreconciliations toconfirm performed andreviewed. Use of electronic cashreceipts transfer norreceived or deposited. Monthly bankreconciliationsperformed andindependentlyreviewed. Use of cash registers or Observe cash salespoint-of-sale devices.procedures. Periodic inspections of Inquire of managerscash sales procedures.about results ofinspections. Restrictive Observe mail opening,endorsement ofincluding endorsementcheque immediately onof cheques.receipt. Mail opened by two Observe mail openingstaff members.procedures. Immediate preparation Observe preparation ofof cash box or list ofcash receipts’ records.mail receipts. Independent check of Review documentationagreement offor evidence ofcash/cheques to beindependent check.deposited at bank withregister totals andreceipts listing. Independent check of Review documentationagreement of bankfor evidence ofdeposit slip with dailyindependent check.

Completeness All cash receipts arerecorded.cash summary. Segregation of duties. Use of electronic cashreceipts transfer notreceived or deposited. Monthly bankreconciliationsperformed andindependentlyreviewed. Daily cash receiptslisting reconciled withposting to customeraccounts. Customer statementsprepared and sent outon a regular basis.Accuracy,classificationand valuation Cash receiptsrecorded at correctamounts. Observe and evaluateproper segregation ofduties. Examine applicationcontrols for electroniccash receipts transfer. Review monthly bankreconciliations toconfirm performed andreviewed. Review reconciliation. Inquire ofmanagement abouthandling of customerstatements. Examine a sample ofcustomers and notefrequency ofstatements. Daily remittance report Review reconciliations.reconciled to controllisting of remittanceadvices. Monthly bank Review reconciliationsstatement performedfor evidence they wereand reviewedperformed andindependently.independentlyreviewed. Cash receipts posted Daily remittance report Review reconciliations.to correct receivablesreconciled daily withaccounts and to thepostings to cash

general ledger.receipts journal andcustomer accounts. Monthly customerstatements sent out. Monthly cash receiptsjournal agreed togeneral ertions Cash receipts arerecorded in thecorrect accountingperiod. Cash receipts arecharged to thecorrect accounts. Review entity’sprocedures for sendingout statements. Review journal andposting to generalledger. Receivables’ ledgerreconciled to controlaccount. Bank reconciliation atperiod-end. Review reconciliations. Chart of accounts. Review cash receiptsjournal for unusualitems. Trace cash receiptsfrom listing to cashreceipts journal forproper classification, Review and testreconciliation.

Internal Control over Cash PaymentsAssertionOccurrenceControl objectivesControlsTest of controls Only valid cashpayments are made. Segregation of duties. Observe and evaluateproper segregation ofduties. Review procedures forreconciling supplierstatements.Completeness All cash paymentsthat occurred arerecorded. Supplier statementsindependentlyreviewed andreconciled to tradepayments records. Monthly bank Review reconciliationsreconciliationsto confirm whetherprepared and reviewed.undertaken andreviewed. Only authorized staff Review delegated list ofcan make electronicauthority for cashcash payments andpayments.issue cheques. Electronic cash Inspect relevantpayments and chequesdocumentation forprepared only after allevidence of approval bysource documents havesenior personnel.been independentlyapproved. Segregation of duties. Observe and evaluateproper segregation ofduties. Supplier statements Review procedures forindependentlyreconciling supplierreviewed andstatements.reconciled to tradepayable records. Monthly bank Review reconciliationsreconciliationsto confirm whetherprepared and reviewed.undertaken andindependently

Cash paymentsAccuracy,recorded correctly inclassificationthe ledger.and valuation Reviewed managerbefore release. Daily cash paymentsreconciled to posting topayables accounts. Use of pre-numberedcheques. Reconciliation of dailypayments report toelectronic cashpayment transfers andcheques issued. Supplier statementsreconciled to payableaccounts regularly. Monthly bankreconciliations of bankstatements to ledgeraccount. reviewed.Inspect sample oflistings for evidence ofsenior review.Review a sample ofreconciliations forevidence that they havebeen done.Examine evidence ofuse of pre-numberedcheques.Review reconciliation toensure performed,reviewed and anydiscrepancies followedup on a timely basis.Review reconciliationsfor a sample ofaccounts.Review bankreconciliations forevidence it was doneand independentlyreviewed. Cash payments posted Supplier statementsto correct payablereconciled to payableaccounts and to theaccounts regularly.general ledger. Agreement of monthlycash payments journalto general ledgerposting. Review reconciliationsfor a sample ofaccounts. Review postings fromjournal to generalledger. Payable accountsreconciled to generalledger control account. Review reconciliation,to ensure performedreviewed and anydiscrepancies followed

Cut-off Cash payments arerecorded in thecorrect ns Cash payments arecharged to the correctaccounts. Reconciliation ofelectronic fundstransfers and chequesissued with postings tocash payments journaland payable accounts. Chart of accounts. Independent approvaland review of generalledger accountassignment.up on a timely basis. Review reconciliationand check it is carriedout regularly. Review cash paymentsjournal to assessreasonableness ofcharging of accounts. Review assignment ofgeneral ledger account.

Internal Control over Revenue and capital pletenessControlsTests of control All expenditure is authorized. Review policies andprocedures in place. Examine a sample of ordersfor appropriate authorization. Orders for capital items should beauthorized by appropriate levels ofmanagement. Order should be requisitioned onappropriate (different to revenue)documentation. Invoices should be approved by the personwho authorized the order. Invoices should be marked with theappropriate general ledger code. All expenditure is classified correctly in thefinancial statements as capital or revenueexpenditure. All the standard controls over purchasesare relevant here (see section 2). All non-current assets are correctlyrecorded in the accounting system. Capital items should be written up in thenon-current asset ledger. The non-current asset register should bereconciled regularly to the general ledgerand any differences investigated andresolved promptly. See section 2. Review reconciliation toensure it is regularly carriedout, review by a more seniorperson, and that alldiscrepancies are followed upand resolved on a timely basis.

Internal Control over Sales Assertion Control objectives Controls Tests of controls Occurrence and existence One person is not responsible for taking orders, recording sales and receiving payments. Recorded sales transactions represent goods shipped. shipping Go