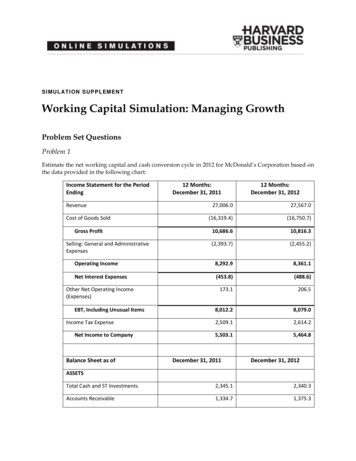

Transcription

Checking AccountSimulationUnderstanding Checking Accounts

What is a CheckingAccount? 1.7.1.G1Tool used to transfer funds deposited into theaccount to make a cash purchaseCould also be named a transaction accountCommon financial service used by many consumersAvailable at depository institutions Traditionally called banks Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

Checking Accountscontinued Services and fees will vary depending upon thefinancial institution Research the financial institution and type of accountbefore choosingMany financial institutions offer telephone andinternet banking services to customers Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman1.7.1.G1

1.7.1.G1Benefits Can help to manage moneyWritten record of expenses Check registerMakes bill paying more convenientReduces the need to carry large amounts of cashMost liquid of cash management tools Considered cash Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1How Do They Work? Money is deposited into the account with a depositslip Pay the transaction by: Writing a checkUsing an ATM and/or debit cardUsing electronic banking Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Characteristics Funds are easily accessible through: A checkAutomated teller machine (ATM)Debit cardTelephoneInternet Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1What is a Check? Used at the time of purchase as the form of payment Piece of paperpre-printedwith the account holder’s: NameAddressFinancial institutionIdentification numbers To completed check, fill inthe: AmountPayee To whom the check waswrittenDateSignature Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Bouncing a Check Check written for an amount over the current balanceheld in the account ‘BouncesBounces’Bounces due to insufficient fundsAssessed a substantial fee by both the financialinstitution and the payeeCan cause harm to credit report Financial institutions report to credit bureaus the accountholder’s failure/success to manage his/her checking accountproperly Used as a guide for future inquiries for credit Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

Other CheckingComponents Register Place to immediately record all monetary transactions fora checking account 1.7.1.G1Written checks, ATM withdrawals, debit card purchases,deposits, fees, etc.Checkbook Contains the checks and the register to track monetarytransactions Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1What is an ATM? Automated teller machine (ATM)Also called cash machinesElectronic computer terminals offering automated,computerized bankingAllows customers to perform transactions just asthey would through a teller Deposits, cash withdrawals, account transfers, checkaccount balances Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1ATMs continued Transactions at an ATM are automatically postedto accountImmediately record all transactions into thecheckbook registerGood option for evenings or weekends whenfinancial institutions are closed Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1ATM Availability Available most places around the U.S. givingcustomers access to money when away from home Can also be found worldwideFound in a variety of places including: Financial institutionsSupermarketsConvenience storesShopping centers Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1ATM Fees ATMs are owned by different financial institutionsFees may be charged to the account for ATM useFees range from 0.50 to 5.00 Usually free to account holders of the financialinstitution Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1ATM Card Card given to account holder to make financialtransactions at ATMsIn the shape of a credit card, but can only be used indesignated placesMust use personal identification number (PIN) toaccess the account A protected number given or chosen by the account holderto allow access to the account Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1PINs Required at ATM as a safety measure so otherpeople cannot access the account with the only theATM cardChoose a PIN which is not easily identified For example – phone number, birthdayInstead of requiring a PIN, some ATMs may read aperson’s face, fingerprint, or eye’s iris to confirmidentity Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1What is a Debit Card? Looks like a credit card, but is connected to thecardholder’s checking account for transactionsMoney is automatically withdrawn from accountwhen transaction occursPrevents overdrafts Transaction cannot be completed without sufficientfunds Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Debit Cards continued Some are dual function cards One card performs both functions forATMs and debit cardsClarify whether or not the card isan ATM card, a debit card, or both Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Using a Debit Card To make a purchase Debit card is swiped like a credit cardCardholder signs a printed receiptRecord transactions immediately into check registerMost can be used at retail establishments acceptingmajor credit cards Many have the Visa or MasterCard logo Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Debit Cards continuedPros ConvenientSmallCan be used like acredit cardAllows a person tocarry less cashDoes not allowoverspendingCons Can lose track of balance iftransactions are not immediatelywritten downOpens checking account up tocredit card fraudIf lost, anyone can use itSomeone else can gain access toaccount if card is found and PIN islearned Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

Types of AccountsAvailable Financial institutions offer different types ofchecking accounts 1.7.1.G1All have own characteristicsResearch all of the requirements and restrictions beforeopening the accountBasic types/guidelines include: Regular checkingFree checkingSpecial checkingInterest-Earning checking Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Regular Checking No monthly charge if minimum balance ismaintainedNo interest is givenUnlimited check writing Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Free Checking No charges or fees for using the accountNo minimum balance requiredUnlimited check writingUsually for a specific group: StudentsSeniors Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Special Checking Generally for people who write only a few checksand keep a low balanceBasic account which pays no interestMonthly service charge or fee for each transactionMay have restrictions on number of transactionseach month Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

InterestInterest-EarningChecking Pays interest on money in account Usually the lowest interest rate of all the cashmanagement toolsMinimum balance requiredUnlimited check writingCalled a share draft at credit unions Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman1.7.1.G1

Opening a CheckingAccount Most applications are completed on a computer toprocess quickly 1.7.1.G1Customer may have to complete a brief hand-writtenapplication to be entered into the computer by newaccounts personnelCustomer must have: Picture identificationName, address, phone number, and social security number Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Opening continued If customer is approved, he/she completes asignature card Contains account information about the new account andhis/her signatureUsed to verify the signature for each signed transactionfor the account to prevent fraudCompletion of the signature card means thecustomer agrees to all terms and conditions of theaccount Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Signature Card example Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Opening continued If offered, customers may choose to have an ATMand/or debit card for the account May be required to complete another formAn initial deposit must be made Amount will vary among different financial institutionsand type of account Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Ordering Checks New customers are provided starter checks to use until theordered checks arrive Generic checks with account number and financial institution preprintedCustomer information is hand writtenMany businesses do not accept starter checks Take this into consideration before making the initial depositOrdered checks may take 5 to 10 business days to arrive Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Ordering continued Personal information on checks NameAddressOptional: phone number, driver’s license numberDO NOT put the account holder’s social security number onthe check for security reasons Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Ordering continued Design of the check is customer’s choice Customer pays for checks Price depends on the styleStyle of the check does not change how a check worksSome financial institutions may offer basic checks free ofchargeSingle or duplicate checks are available Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Ordering continuedSingle Duplicate (carbon copy)No records of writtenchecksEach check must be loggedin the register immediatelyto track transactions Provides a written record ofeach check with the carboncopyConvenient in case the checkwas not recorded intoregister immediately Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Endorsing a Check Endorsement Three types Signature on the back of the check from receiving person approving it fordepositA check must be endorsed to be depositedBlankRestrictiveSpecialSafest way to endorse the check is to wait until going to thefinancial institution to deposit or cash the check Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Blank Endorsement Receiver of the check signshis/her nameAnyone can cash or depositthe check after has beensigned Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Restrictive Endorsement More secure than blankendorsementReceiver writes “fordeposit only” abovehis/her signature Allows the check to only bedeposited Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Special Endorsement Receiver signs and writes“pay to the order of (fill inperson’s name)”Allows the check to betransferred to a secondparty Also known as a two-partycheck Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1Making a Deposit Deposit slip Complete a deposit slip to make a deposit Contains the account holder’s account number and allows money(cash or check) to be deposited into the correct accountLocated in the back of the checkbookGive to financial institution along with cash and/or checkChecks must be endorsed to be depositedDeposited amount must be recorded in the check register tokeep the balance current Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

Completing a DepositSlip Date The date the deposit is being made Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman1.7.1.G1

Completing a DepositSlip Signature Line Sign this line to receive cash back Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman1.7.1.G1

Completing a DepositSlip Cash The total amount of cash being deposited Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman1.7.1.G1

Completing a DepositSlip 1.7.1.G1Checks List each check individually Identify each check on the deposit slip by abbreviating the nameof the check writer Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account SimulationFunded by a grant from Take Charge America, Inc. to the De

Checking Accounts 1.7.1.G1 continued Services and fees will vary depending upon the financial institution Research the f