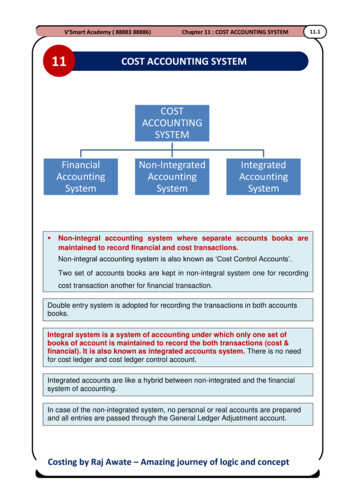

Transcription

Material Flow Cost Accounting – Proposals for Improving the Evaluationof Monetary Effects of Resource Saving Process Designs111R. Sygulla , A. Bierer , U. Götze1Chair of Management Accounting and Control, Faculty of Economics andBusiness Administration – Chemnitz University of Technology, GermanyAbstractThere is no doubt about the need for a sustainable production. However, the development of resource savingprocess designs raises the question how to appraise the economic effects of appropriate alternative process(chain) configurations and technologies. The paper discusses the material flow cost accounting as apotential approach to reveal the quantitative and monetary effects in the frame of material flow management.It gives an introduction to its basic ideas, identifies methodical shortcomings and presents twoenhancements for improvement: the explicit regard of energy (loss) flows and a procedure for a moredetailed analysis and forecast of system costs.Keywords:Material flow cost accounting, Material flow management, Process appraisal1 INTRODUCTIONThe world’s material and energy usage, in particular theindustrial demand for oil, steel, aluminum etc. has beendramatically increased over the last 30 years and willincrease further. Moreover, compared to other cost items(e. g., personnel costs, depreciation) the costs of materialand energy use represent – with about 50% – the highestportion of costs in the manufacturing industry. Thus,reducing the use of material and energy will have positiveecological effects like reduced wastes as well as energylosses and may result in material, energy and disposalcost savings. Therefore, it would promote a sustainableeconomic and environmental management [1].In the manufacturing industry, the extent of material andenergy use as well as material and energy losses mainlydepends on the design of the processes which areperformed to produce a certain product program. Since agiven product program can be manufactured withdifferent process (chain) configurations and technologies,the optimum solution with respect to the pursued targetsof high material and energy efficiency and low costs hasto be found.The design of highly integrated process chains with areduced total energy demand and reduced energy losses(as well as material demand and losses), is also a maintarget in the eniPROD (‘Energy-efficient Product andProcess Innovations in Production Engineering’) researchproject [2]. The activities aiming at such processimprovements are related to different levels: a singlemanufacturing step (e. g., a turning process) andcombinations of two or more steps up to a process chaincovering all required manufacturing activities to producea certain product (or component). In this context, theresearch question arises: how to appraise the economiceffects of such alternative process chain configurationsand technologies? To address this research question, thematerial flow cost accounting (MFCA) will be discussedas a means to identify and quantify monetary effects ofreducing material/energy use and losses.The remainder of the paper is organized as follows. Insection 2, the underlying framework of the material flowmanagement is introduced. Thereafter, in section 3, thematerial flow cost accounting is presented as a methodto overcome the shortcomings of other ecologicallyand/or economically oriented accounting and evaluationmethods. The basic procedure is described and thebenefits from the MFCA in the given context areanalyzed. Section 4 presents two methodologicalenhancements of the MFCA approach that aim atimproving the appraisal of economic effects of alternativeprocess (chain) configurations and technologies: themodeling of energy use, losses and costs by separatedenergy flows and the refinement of MFCA costs analysisand planning. The summary and conclusions of the paperthare presented in the 5 section.2 MATERIAL FLOW MANAGEMENTMaterial flow management (MFM, sometimes also calledflow management) is seen as a holistic, life cycleoriented approach. It supports a targeted, responsibleand efficient manipulation of industrial material andenergy flows in order to achieve an ecologically andeconomically efficient use of natural environmentalresources including the minimization of relevant emissionand waste [3]. In MFM, with a broad view a material flowis defined as the ‘way’ of a material (or an energy)starting with its extraction as a raw material, passingseveral stages of converting and manufacturing, its usein form of products, possible stages of reuse or recycling,and ending with its disposal. But the managementapproach also comprises the narrower view of anindividual company that strives for reducing its materialand energy use and loss by managing and controlling theflow of materials and energy from entering the companyup to leaving it as outputs or waste.As shown in figure 1, MFM can be considered to be acontinuous improvement process. In order to ensuredirected activities and high quality results, suitable goalshave to be identified to guide the improvementprocesses. Therefore, – like for every managementcycle – the initial step of MFM is goal setting. Sincematerial flow management is part of a superordinatemanagement concept, the goals of MFM arise from thenormative and strategic goals of the company.The actual MFM cycle starts with modeling thestructure. In this phase, the system boundaries aredefined and the possible ‘ways’ of all (relevant) materialsCite as: Sygulla, R.; Bierer, A.; Götze, U. (2011): Material Flow Cost Accounting – Proposals for Improving the Evaluation of Monetary Effects of Resource SavingProcess Designs. In: Proceedings of the 44th CIRP Conference on Manufacturing Systems, 1-3 June 2011, Madison, Wisconsin, USA (6 pages).URL: inOffen/44thCIRP MFCA.pdf

and energies throughout the process chain are identified.On the basis of this information, a flow model isdeveloped. To provide detailed information, the flowshave to be differentiated into flows which result in desiredgoods and flows of material and energy losses (e. g.,clippings, chips or waste heat).Set sEvaluatePlanactionsFigure 1: Flow management model.After the flow structure has been modeled, the flows arequantified by measuring the flowed amounts within adefined period. The resulting values are added to the flowmodel.In the evaluation phase, the as-is state of the flows hasto be valued with respect to their resource and costefficiency. As decisions may concern the design ofindividual processes as well as of process chains, bothare potential objects of evaluation and a methodology isneeded that can be applied to both of them.Based on the evaluation results, specific actions areplanned (here, alternative manufacturing steps, processconfigurations and/or technologies) in order to improvethe as-is state. To support decision making, the potentialimpacts of the individual actions on the examinedprocess chain (i.e., the extent of efficiency improvementand the effects on the costs) have also to be evaluated(dashed arrow in figure 1). The potential actions shouldthen be compared among each other and with respect tothe as-is state. Thereafter, efficiency improving and costsaving actions are realized by implementing specificprocess configurations and technologies.A performance check analyzes the process chain’s newas-is state. This verification will provide information aboutadditional improvement opportunities. Pursuing them orreacting on a change of the underlying goals, initiatesnew improvement projects, and therewith, new passes ofthe management cycle.In the various steps of MFM methodological support isneeded. The available approaches mainly differdepending on the underlying goals, the ways of analyzingand evaluating quantified flows and the use of physicaland/or monetary evaluation criteria. In the following,several established approaches and their shortcomingswith respect to the required needs of a sophisticatedevaluation and analysis in MFM will be presented briefly.The environmental management tool of Life CycleAssessment (see, e. g., [4]) aims at revealing the lifecycle-related impacts of products and services on thenatural environment. In fact, ecologically intendedapproaches like this support the reducing ofenvironmental damages. But they do not make clearcontributions to cost savings or corporate profits [5].An economically and flow oriented approach is ValueStream Mapping (see, e. g., [6]). Its focus lies on theefficient, customer oriented analysis and design ofbusiness processes by preventing non value addingactivities (in terms of the approach: ‘waste’). Therefore,the analysis of material flows is restricted to a logistic andorganizational few. Material and energy losses are largelyignored [5]. A methodological enhancement of valuestream mapping by Erlach and Westkämper strives fortotal energy savings and analyzes every manufacturingstep in order to detect energy wastes [7]. This approachis directed at incremental improvements of individualprocesses, and does therefore not consider effects onother processes or even the internal infrastructure ofenergy supply. Moreover, the basic approach of ValueStream Mapping and its energy related enhancement donot provide sufficient methodical support for a monetaryevaluation of the design alternatives – but, costappraisals are an essential basis for a meaningfuldecision making.However, for the (monetary) evaluations of processesintended here, traditional cost accounting methodsseem not to be suited very well, too. Commonly, theyhave a strong departmental orientation and most of thematerial cost are considered to be direct cost (andtherefore, are assigned directly to products). This entailsthat traditional cost accounting provides only insufficientknowledge about the internal use of materials and energyas well as the manufacturing’s material and energylosses.Environmental cost accounting approaches like theenvironmentally oriented full cost accounting [8] andwaste costing [9] have been developed to overcome theshortcomings of the traditional methods by explicitlyintegrating economic effects of environmental protectionand damage. Partly, they are flow oriented and able toidentify and analyze environmental costs and costs ofmaterial and material flows, but not in detail. Some costblocks with high cost-saving potential (packaging,material losses) as well as the energy consumption andthe energy losses are still untouched.In summary, it can be pointed out that the previouslypresented approaches neglect the complexity of internalmaterial and energy flows. Moreover, they fail to integratethe ecologic and economic dimension of material flowmanagement. The recent approach of material flow costaccounting, which will be examined in the followingsection, overcomes the mentioned shortcomings, and istherefore more suitable for appraising the benefits ofalternative – material and energy saving – processconfigurations and technologies.3 MATERIAL FLOW COST ACCOUNTINGMaterial flow cost accounting (MFCA) aims at supportingmaterial flow oriented analyzes and decision making toimprove resource and cost efficiency. It integrateseconomic and ecological objectives in order to contributeto a reduced or more efficient material use. It is importantto note here, that energy flows are usually subsumedunder the term of material flows or even neglected (e. g.,[10] [11] [12] [13]). In particular, with MFCA it is possibleto visualize and quantify material losses and shift theminto the focus of the managerial decision making. This isachieved by improving the overall transparency of thematerial flows in physical and monetary terms [11].Examples of the implementation of MFCA in practice canbe found in Germany and Japan (see, e. g., [5] [14] [15]),where the approach has been developed [5]. Due to theabove mentioned focus on material it is in particularsuitable for the manufacturing and the process industry.While the number of German examples remains still low,the extensive promotion of MFCA by the JapaneseMinistry of Economy, Trade and Industry entailed a more

rapid spread [5] (Nakajima mentioned more than 50Japanese companies in 2004 [13]).Material flow cost analyzes can be made at differentprocess levels, from individual technical processes ormanufacturing steps up to whole value creation chainsincluding several independent companies. Like most ofother environmental cost accounting methods, MFCAdoes not replace the already existing body of costknowledge from traditional cost accounting methods, butcan be understood as a specific partial accountingmethod to improve economic and environmental decisionmaking with respect to material (and energy) usage.MFCA’s general procedure corresponds with some of thesteps of flow management: flow structure modeling,quantification of flows, and evaluation (see Figure 1).Process 2Process 3(Internal waste management) Material costs are determined by multiplying thephysical amount of the particular materials by theirspecific input prices and summing up the results. Theuse of fixed input prices allows a consistent appraisalfor all manufacturing steps. CustomerProcess 1Cost appraisals of the quantified flowsThe sole accounting of quantities does not providesufficient support for decision making. Thus, anadditional principal item of MFCA is the cost appraisal ofthe flows which are perceived as cost objects. The socalled flow costs which have to be assigned to theminclude all costs which are caused by the flows or whichcan be related to them [19]. MFCA’s recent interpretationby ISO suggests the following major cost items for acategorization of the flow costs [19]:If at all specified, energy costs are calculated similarto the material costs. Otherwise, as energy is oftensubsumed under the term of material, the energycosts are understood as part of the material costs. DisposerSupplierFlow structure modelingI

flow of materials and energy from entering the company up to leaving it as outputs or waste. As shown in figure 1, MFM can be considered to be a continuous improvement process. In order to ensure directed activities and high quality results, suitable goals have to be identified to guide the improvement processes. Therefore, – like for every management –the initial step of MFM is goal .