Transcription

PERFORMANCE REVIEW

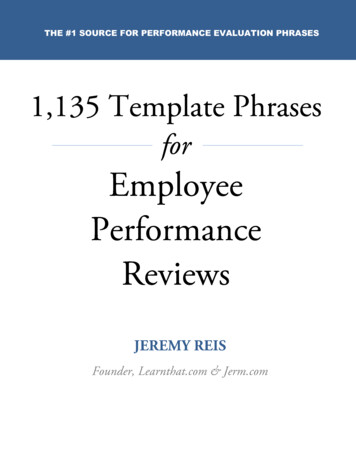

Five-Year Financial Highlights.73Five-Year Financial & Operating Highlights.74Share Performance 2017/Market Capitalisation. 76

THE WORLD’SBESTJUST GOTBETTERAirAsia bagged another Skytrax World's Best Low-Cost Airline award in 2017

PERFORMANCE REVIEWAirAsia Group Berhad[ 73 ]FIVE-YEARFINANCIAL HIGHLIGHTS201320142015INCOME STATEMENT (RM Million)Revenue5,1125,4166,298Net total expenses4,2494,5904,702Operating profit8638261,596Profit before taxation36123215Taxation160326Net Profit36283541BALANCE SHEET (RM Million)Deposits, cash and bank balances1,3801,3382,427Total assets17,85620,66421,316Net debt (Total debt - Total Cash)8,79011,39010,186Shareholders’ equity5,0014,5554,451CASH FLOW STATEMENTS (RM Million)Cash flow from operating activities9613022,204-2,346-2,154-103Cash flow from investing activitiesCash flow from financing activities5091,779-1,303Net Cash Flow-876-73798FINANCIAL PERFORMANCE (%)Return on total assets20.42.5Return on shareholders’ equity7.21.812.26.35.210.9R.O.C.E. (EBIT/(Net Debt Equity))Operating profit margin16.915.325.3Net profit margin7.11.58.6OPERATING STATISTICSPassengers 7,98028,073,16030,079,666Load factor (%)807981RPK (million)26,60727,27430,006ASK (million)33,40134,59037,408Aircraft utilisation (hours per day)12.112.312.4Average fare (RM)166165157Revenue per ASK (sen)14.0813.3614.2Cost per ASK (sen)12.8512.7612.21Cost per ASK - excluding fuel (sen)5.846.246.86Revenue per ASK (USc)4.444.073.6Cost per ASK (USc)4.053.893.1Cost per ASK - excluding fuel (USc)1.841.91.74Number of stages151,709155,962167,002Average stage length (km)1,1441,2171,247728180Size of fleet at year end (AirAsia Berhad)Size of fleet at year end (Group)154172171Number of employees at year end6,0896,3046,636Percentage revenue via internet (%)858470RM-USD average exchange rate3.173.283.942016Restated2017 620512,404704.28NOTE:1. In 2017, AirAsia Berhad’s financials and key operating statistics comprise the consolidated AOCs, namely AirAsia Malaysia, AirAsia Indonesia and AirAsiaPhilippines

[ 74 ]AirAsia Group BerhadPERFORMANCE REVIEWFIVE-YEARFINANCIAL & OPERATINGHIGHLIGHTSREVENUEOPERATING PROFITRM millionRM millionRevenueTOTAL ASSETSSHAREHOLDERS’EQUITYDEPOSITS, CASH ANDBANK BALANCESTotal AssetsShareholders’ EquityDeposits, cash and bank balancesRM millionRM millionRM 4,5558268635,4164,4515,00113 14 15 16 171,74217,8561,5966,8466,29813 14 15 16 175,11220,6642,1612,0669,7102,427Operating Profit13 14 15 16 1713 14 15 16 1713 14 15 16 17

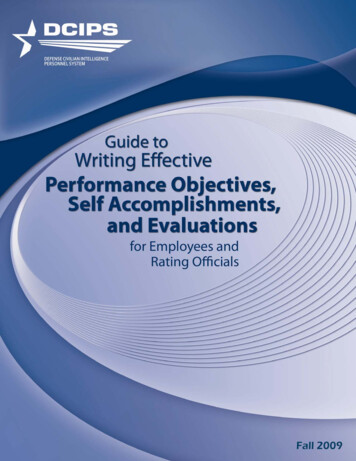

PERFORMANCE REVIEWREVENUEPER ASKCOSTPER ASKRevenue per ASK (USc)Cost per ASK (USc)senpaxPassengers CarriedSIZE OFFLEETAirAsia Berhad1Size of fleet at year end (Malaysia)11613.1313 14 15 16 17113 14 15 16 17AirAsia Berhad refers to AirAsia Malaysia, AirAsia Indonesia and AirAsia 3 14 15 16 112.8539,092,972senPASSENGERSCARRIED13 14 15 16 17AirAsia Group Berhad[ 75 ]

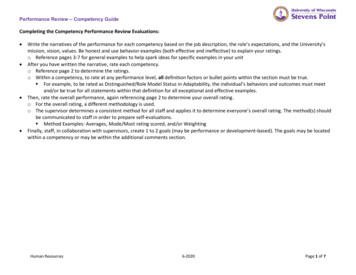

[ 76 ]AirAsia Group BerhadPERFORMANCE .353.533.293.143.00SHARE PRICE ,000VolumeDec 17Nov 17Oct 17Sep 17Aug 17Jul 17Jun 17May 17Apr 17Mar 17Feb 17Jan 170Dec 160Price HighPrice LowMARKETCAPITALISATIONAS AT 31 DECEMBER 3,79420063,55320053,723RM million

World Travel Awards 2017WORLD’S LEADINGLOW-COSTAIRLINECABIN CREWAT YOUR SERVICE

t h e m r o l a b . c o mAs an Airline MRO, Air France Industries KLM Engineering & Maintenance has developed a uniqueportfolio of know-how and engineering capabilities reflected in its development of a wide range ofvalue-adding innovations."The MRO Lab" is the program where all the innovations developed by AFI KLM E&M and itsnetwork of affiliates converge. Specially tailored to the challenges of aircraft maintenance, theinnovations are the fruit of continuous development aimed at satisfying the requirements of airlineoperating performance.The know-how deriving from mastery of these technologies benefits AFI KLM E&M clients bygenerating scale effects and optimizing fleet performance.

Believe in yourselfand make ithappen.Tanus Kerdsombut (Thai)Then Ground StaffNow Business Development Manager

PERSPECTIVE

Management Discussion & Analysis. 86

[ 86 ]AirAsia Group BerhadPERSPECTIVEMANAGEMENTDISCUSSION& ANALYSIS2017 WAS YET ANOTHER PHENOMENAL YEAR. WE TOOK DELIVERY OF29 AIRCRAFT - A RECORD FOR THE LAST FOUR YEARS; EXPANDED THEROUTE NETWORK OF EACH COUNTRY’S OPERATIONS; SAW OUR FIRSTFLIGHT IN JAPAN TAKE TO THE SKIES WHILE LAYING THE GROUNDWORKTO START UP IN VIETNAM AND CHINA.

PERSPECTIVEAirAsia Group Berhad[ 87 ]WE ARE PROUD TO ANNOUNCE A NEW GROUP STRUCTURE WHICHSEGREGATES OUR AIR TRANSPORTATION BUSINESS FROM OUR DIGITALAND SUPPORT BUSINESSES, ENABLING ALL THREE PILLARS TO GROWWITH ENHANCED CLARITY AND FOCUS. THE DIGITAL BUSINESSES WECURRENTLY HAVE WILL BE ABLE TO EXPAND INTO MAJOR TECHNOLOGYPLAYERS IN THEIR OWN RIGHT.

[ 88 ]AirAsia Group BerhadPERSPECTIVEMANAGEMENT DISCUSSION & ANALYSISOVERALL PERFORMANCEIt is hard to believe another year hasgone. They say time flies when you’rehaving fun. While we certainly have hadour share of fun, the team at AirAsia hasalso been working extremely hard; andit is probably more accurate to say thatour time has flown by so swiftly becauseof the sheer amount that we achieved.2017 was yet another year of phenomenalgrowth as a result. We took delivery of 29aircraft – a record for the last four years;expanded the route network of eachcountry’s operations; saw our first flightin Japan take to the skies while layingthe groundwork to start up in Vietnamand China; and worked to secure an overUSD1.18 billion deal revolving aroundthe divestment of our aircraft leasingoperations that are currently undertakenby Asia Aviation Capital Limited (AACL).While others in the region were reducingcapacity, we grew ours by 13%, adding newroutes and increasing frequencies. As atyear end, the Group’s fleet of 205 AirbusA320 aircraft were serving 293 routesto 119 destinations in 21 markets withinAsia. With effective route management,we increased our aircraft utilisation froman already very respectable 12.14 hoursa day in 2016 to 12.82 hours. Tappingexisting demand while stimulatingdemand on unique routes, we filled up ourflights, seeing our load factor grow twopercentage points to 88% and the totalnumber of guests carried increase 16% to65.5 million. That truly is an astronomicalfigure, roughly a tenth of the entire Aseanpopulation.In Malaysia, we dominate both thedomestic and international air travelmarkets. With over 1,900 flights a weekfrom six hubs, we account for no less than54% of the total number of flights withinthe country. Even more gratifying, we also“FOLLOWING THE COMPLETION OF THE INTERNAL REORGANISATIONOF AIRASIA BERHAD (AAB) AND THE TRANSFER OF ITS LISTINGSTATUS TO AIRASIA GROUP BERHAD (AAGB) ON 16 APRIL 2018, AAB ISNOW A WHOLLY-OWNED SUBSIDIARY OF AAGB. THIS MANAGEMENTDISCUSSION AND ANALYSIS REPRESENTS AAB’S FINANCIALACHIEVEMENTS, RESULTS, BUSINESS PLANS AND STRATEGIES FOR THEFINANCIAL YEAR ENDED 31 DECEMBER 2017 (THE FINANCIAL YEAR),WHICH WILL BE ADOPTED BY AAGB IN THE NEXT FINANCIAL YEAR.”saw accelerated growth in all our associateairlines, with the exception of Indonesiawhere operations were disrupted due tovolcanic activities in Mt Agung. Having saidthat, we were still able to successfully listthe airline at year end. Additionally, we areproud that all our Asean operations alsorecorded full-year profits.Despite a 23.3% increase in fuel cost, aswell as a depreciating Ringgit againstthe US Dollar, AirAsia Berhad (namelyAirAsia Malaysia, AirAsia Indonesia andAirAsia Philippines) achieved a full-yearnet operating profit of RM1.58 billion,exceeding the record set in 2016 by8.5% on a proforma basis. Hedgingour fuel and foreign exchange (forex)helped to minimise the impact of the oilprice increase and unfavourable forexenvironment. In addition, we have beenable to reap the benefits of some earlywins of our digital transformation whichtook off in earnest, completely revampingour business approach in ways madepossible only by better data analysis andmining.Further building our efficiencies, westarted integrating our operationsacross the Group as we move towardsbecoming One AirAsia. The idea of OneAirAsia is to streamline our operations forenhanced efficiencies and better revenuemanagement leading to greater costreductions. Working as one, we present astronger voice in procurement as well aswhen negotiating deals. In the longer term,we envisage consolidating the financialresults of all our country operations as thiswould present a more accurate picture ofthe Group’s overall performance and value.Towards this end, we are pleased to sharethat as of the first quarter of 2017, we havebeen consolidating the financial figures ofour Indonesian and Philippine associateswith that of Malaysia when presenting ourresults in terms of profit and loss, and ourbalance sheet.We are proud of our financial performancefor the year, which was boosted byUSD100 million in proceeds from thedivestment of Asian Aviation Centre ofExcellence (AACE). We also monetisedour ground handling unit and firmed upa transaction for our leasing business.Proceeds from these latter twotransactions will be reflected in our 2018financial figures.GROUP AT A GLANCETOTALALLSTARS19,314PASSENGERS FLOWNTO DATE435MILLIONTOTALFLEET205AIRBUS A320PASSENGERS CARRRIEDIN 201765.5MILLIONBy “the Group” we refer to AirAsia Malaysia, AirAsia Indonesia, AirAsia Philippines, AirAsia Thailand, AirAsia India and AirAsia Japan. Although the Group’s total fleet size stood at205, this included three aircraft on lease to third parties, six that were grounded for redeployment to other affliates in 1Q18 and eight operated by AirAsia X Indonesia.1

PERSPECTIVEAirAsia Group Berhad[ 89 ]AIRASIA GROUPLOAD FACTOR88%PASSENGERS CARRIED IN ESAIRASIAINDIA5.3MILLIONFINANCIAL REVIEWFor the financial year ended 31 December2017, AirAsia Berhad3 recorded a 42%increase in revenue from RM6.85 billionin 2016 to RM9.71 billion. This wascontributed by a 10% year-on-yearincrease in capacity and 11% increase innumber of guests carried to 39.1 million.Revenue was further boosted by a 6%increase in ancillary income per guest23AIRASIATHAILANDMILLION4.4MILLIONto RM49, while our average fare wasmaintained at RM176 given the plannedcapacity expansion.We achieved a full-year operating profitof RM2.16 billion, 5% higher than RM2.07billion in 2016. Despite a 5% reductionin average stage length, our overallcost per available seat kilometre (CASK)including fuel increased by 16% to 13.13sen as a result of the fuel price hike. CASK6.7 million (including passengers carried by 8 A320 aircraft operated by AirAsia X Indonesia)AirAsia Berhad refers to the consolidated units of AirAsia Malaysia, AirAsia Indonesia and AirAsia N0.03MILLIONexcluding fuel stood at 8.29 sen, whichwas 15% higher than in 2016 due to anincrease in staff cost, mainly that for pilotsand talent retention supporting the Group’scontinuous growth. Revenue per availableseat kilometre (RASK) increased by 7% to15.13 sen. Profit was also boosted by 16%growth in ancillary revenue year-on-yearto RM1.93 billion.

[ 90 ]AirAsia Group BerhadPERSPECTIVEMANAGEMENT DISCUSSION & ANCILLARY REVENUERM 15.136.852.16RASKSEN2.07OPERATING PROFITRM BILLION9.71REVENUERM BILLION17%16%INCREASEINCREASE20172016Cash Flow & DebtCash inflow from operations stood atRM1.91 billion, compared to RM2.24 billionin the previous year. As at 31 December2017, our cash position amounted toRM1.88 billion. We ended the year witha reduced total debt of RM9.31 billion ascompared to RM10.58 billion and a netdebt of RM7.43 billion as compared toRM8.84 billion in 2016 after offsettingour cash balances of RM1.88 billion.Net gearing, meanwhile, improvedsubstantially from 1.33 times as at end2016 to 1.11 times as at end 2017, followingthe repayment of borrowings and the20172016equity injections of RM1,006.2 million bythe two of us. As a result, AirAsia Berhad’scash position grew to approximatelyRM1.88 billion as at the end of December2017.Meanwhile, to mitigate the company’sexposure to fuel price risks, currencyrisks and interest rate risks, we hedgedapproximately 78% of AirAsia Berhad(AAB)’s fuel consumption requirement for2017 at USD60 per barrel, about 57% ofAAB’s USD currency risk, and 100% of ourinterest rate risks. For the year, the USDollar to Ringgit exchange rate averaged4.2812.Capital ExpenditureIn 2017, as part of our fleet renewalprogramme, and to meet the Group’sexpansion plans, we received 20 newaircraft – 17 Airbus A320neo and threeAirbus A320ceo. These aircraft werefinanced via asset-backed bank financingand sale and leaseback for tenuresbetween 12 and 15 years. In addition, wereturned two Airbus A320ceo aircraftthat were on lease to AirAsia Philippinesto the third-party lessors and sourced 11additional Airbus A320ceo aircraft fromoperating lessors’ portfolios to increaseour fleet growth to 29 aircraft.

PERSPECTIVEAirAsia Group Berhad[ 91 ]DIVIDEND OF24SENPER SHARE PAID INFINANCIAL YEAR 2017In 2018, we aim to receive 23 new aircraft– 13 Airbus A320neo and 10 AirbusA320ceo – for further Group expansion.These aircraft will be financed via saleand leaseback for tenures between 12 and15 years. In addition, we seek to returnthree leased Airbus A320ceo aircraftfrom AirAsia Philippines to the third-partylessors and have sourced four moreaircraft – two used Airbus A320neo andtwo used Airbus A320ceo – from lessors toincrease our net fleet growth to 24 aircraft.Capital StructureOn 26 January 2017, we completed theissuance of 559,000,000 new ordinaryshares of RM0.10 each in AirAsia Berhadto Tune Live Sdn Bhd at an issue price ofRM1.80 per share. As a result, we raised atotal of RM1,006.20 million.Dividend PolicyIn 2013, the Group announced a dividendpolicy of paying an annual dividend of upto 20% of our net operating profit (as perthe audited financial statements of AirAsiaBerhad), rounded to the nearest whole sen,provided this would not be detrimental toour cash flow requirements. We have todate fulfilled this policy; and during thefinancial year 2017, paid a dividend of 12sen per share for the financial performanceof 2016, and another 12 sen per share asinterim dividend for the financial year 2017.The total dividend paid represents a 7%yield based on the share closing price ofRM3.35 as at 31 December 2017.We have also committed to a biennialdistribution of special dividends from themonetisation of non-core assets. Havingmonetised our ground handling servicesin an agreement with SATS, we intend todeclare a special dividend in 2018.

[ 92 ]AirAsia Group BerhadPERSPECTIVEMANAGEMENT DISCUSSION & ANALYSISPERFORMANCE OF ASSOCIATE COMPANIES (REVENUE)INCREASE20162016DECREASE20172016AIRASIA INDIA(INR BILLION)48%INCREASE86%8.2610.8015.3615.93AIRASIA PHILIPPINES(PHP BILLION)20172%INCREASE20173,88911%3,8188%AIRASIA INDONESIA(IDR BILLION)32.4035.93AIRASIA THAILAND(THB BILLION)5.956.44AIRASIA MALAYSIA(RM BILLION)INCREASE20172016PERFORMANCE OF COUNTRYOPERATIONSAirAsia MalaysiaWith seven new aircraft, AirAsia Malaysiacontinued to grow its route network bothdomestically and regionally to furtherentrench its position as the leading airlinein the country, contributing to the Group’s54.3% and 30.8% share of the domesticand international markets respectively.Its 8% increase in capacity also saw theairline fly 10% more guests totalling 29.2million. Strong performance, as indicatedby an 89% load factor; aircraft utilisation20172016of 14 hours a day; and 2% increase inrevenue per guest, led to AirAsia Malaysiaachieving a 2% increase in RASK to 14.49sen. For the full year, its revenue grew 8%to RM6.44 billion while net operating profitwas recorded at RM1.51 billion.AirAsia ThailandDespite the government’s crackdown onzero-dollar tours from China and mourningover the passing of their King, AirAsiaThailand pulled together a robust set ofresults. While increasing its capacity by11%, it flew 15% more guests year-on-yeartotalling 19.80 million and grew its loadfactor three percentage points to 87%. Thiscontributed to an 11% surge in revenuefrom THB32.40 billion to THB35.93 billion.Although CASK – including fuel and ahike in excise tax on jet fuel consumptionfor domestic flights – increased by 7% toTHB1.52, its RASK grew 2% to THB1.61,enabling our associate to record a profitafter tax of THB2.69 billion, making it theonly profitable airline in the country forthe year. Meanwhile, its EBIT and EBITDARmargins stood at 9% and 27%, respectively.

PERSPECTIVEAirAsia IndonesiaAirAsia PhilippinesAfter a couple of years of capacityrationalisation, in 2017 AirAsia Indonesia(PT Indonesia AirAsia) welcomed a newaircraft, increasing its fleet to 23, andintroduced two new international routes,further reaffirming AirAsia’s leadershipas the airline group with the largestinternational travel market share in thecountry. Despite volcanic activity impactingtravel into Indonesia in the fourth quarter,our associate flew a total of 6.7 millionguests for the year, down only 1% from thenumber in 2016, and maintained a healthyload factor of 84%. Its net operating profitstood at IDR378.5 billion while profitbefore tax was IDR300.30 billion. Sincethe official listing of PT AirAsia IndonesiaTbk, the holding company of PT IndonesiaAirAsia, on 29 December 2017, retailinvestor interest in PT AirAsia IndonesiaTbk has been growing.We are extremely proud of the turnaroundby our Philippine operations, proving thatperseverance and our business modeltruly work. Despite numerous one-offcosts for aircraft redeliveries, maintenanceand overhaul throughout 2017, AirAsiaPhilippines grew its revenue 48% fromPHP10.80 billion in 2016 toPHP15.93 billion and achieved a netoperating profit of PHP686.4 millionbacked by ASK growth of 37%. Revenuewas boosted by a 32% increase in numberof guests carried and 8% increase inaverage fare. While increasing its capacityby 31% our Philippines operationsalso maintained its load factor at 87%.Meanwhile, ancillary income per guestgrew 26% from PHP419 to PHP528.AirAsia IndiaOur associate airline in India achievedtremendous growth in 2017, increasingits revenue 86% from INR8.26 billion toINR15.36 billion, boosted by an 81% hike inAirAsia Group Berhad[ 93 ]number of guests carried. The delivery ofsix aircraft during the year enabled AirAsiaIndia to increase its capacity by 80% viaroute network expansion that includedfive new destinations. Ancillary incomeper guest also grew 8% from INR376to INR408 while its load factor stood at87%, an increase from 86% in 2016. Mostencouragingly, our associate recorded itsfirst net operating profit of INR144 million,in the fourth quarter. With its affordablefares, AirAsia India is stimulating demandin the country.AirAsia JapanAirAsia Japan took off commercially on29 October 2017, stamping its operationswith a high level of efficiency, its singleaircraft achieving an on-time performanceof 90% on the twice daily route betweenNagoya and Sapporo. With two aircraftin 2018, our associate will focus on routeexpansion.EXPANSION INTO THE REGIONWe have come a long way from ourhumble beginnings, yet are still somedistance from filling all the dots withinthe Asean, and certainly the Asian, map.In 2017, however, we managed to makepositive advances in this regard, clearing apath towards setting up operations in twomarkets that have great appeal and thatwould help us complete the loop of airlineswe have created within the Asia-Pacificregion.After years of eyeing Vietnam, we havefinally found suitable partners for a jointventure there. The country has alwaysattracted us because of its sizeablepopulation of 95 million, fast-expandingmiddle income segment and rapid growthin air travel which, in the last two years,was the fastest in the world. This growth,moreover, is set to continue in doubledigits over the next decade . We are veryexcited by the prospect of being part of thisgrowth, and indeed to stimulate it further.

[ 94 ]AirAsia Group BerhadPERSPECTIVEMANAGEMENT DISCUSSION & ANALYSISthe different AirAsia operations in thecountry. Operational as of 1 January 2018,the WFOE enables us to create greaterefficiencies through shared resources andeconomies of scale, further reducing ourdistribution and marketing costs.Indeed, China is one of our strongestmarkets, and one that we intend to furthergrow via our LCC operations by connectingmore tier 2 and 3 cities with our multiplehubs. Having already established avery strong base in southern China, andparticularly Shenzhen and Guangzhou,we now seek to expand more extensivelyinto central China while creating links withnortheast China through long-haul routes.This would not only support the One BeltOne Road initiative but also our own visionto create bridges between China andAsean.We also entered into a memorandumof understanding (MoU) with ChinaEverbright Group in May to enable us tostart LCC operations in China. Everbrightis a state-owned financial servicesconglomerate and a major shareholder inChina Aircraft Leasing Group Holdings.in the country, and are today the topforeign carrier at 11 Chinese airportsincluding Chongqing, Wuhan, Changsha,Shenzhen, Hangzhou, Xi’an, Guangzhou,Nanning, Kunming, Chengdu and Shantou.Five of our country operations serve 45routes to 15 cities in mainland China, with12 routes unique to AirAsia. In 2017 itself,we added five new routes: Kuala LumpurWuhan, Manila-Guangzhou, LangkawiShenzhen, Kuching-Shenzhen and KaliboShanghai while increasing the frequenciesof four routes, ending the year with noless than 360 flights a week. Togetherwith AirAsia X, we have carried more than40 million guests to the country, earningourselves the title of being The MostInfluential Foreign Airline in China.AirAsia was the first foreign LCC to entergreater China in 2005 with our inauguralBangkok to Macao flight on 5 July. Wehave since rapidly deepened our presenceSupporting our operations in China, weestablished a wholly foreign-ownedentity (WFOE) in Guangzhou to serve as abase for all current Allstars representing“FIVE OF OUR COUNTRY OPERATIONSSERVE 45 ROUTES TO 15 CITIES INMAINLAND CHINA, WITH 12 ROUTESUNIQUE TO AIRASIA. IN 2017 ITSELF, WEADDED FIVE NEW ROUTES.”ANCILLARYAirAsia Berhad’s ancillary business hascontinued to grow, marking a 16% increasein revenue from RM1.66 billion in 2016to RM1.93 billion for the year, whichaccounted for 20% of our total revenue.While maintaining our zeal to introducenew and exciting products that guestswould find irresistible, a key focus duringthe year was to increase their uptakethrough a dynamic pricing strategy aswell as more personalised communicationbased on data analysis of guests’ pastpurchasing behaviour. In the third quarter,we introduced more tiers in the pricingmechanisms for check-in baggage andseat selection, which led to a 21% increasein baggage fees to RM925.4 million; andan 18% increase in revenue from seatselection to RM114.8 million.

PERSPECTIVEIn October, we started to personalise ourcommunication with guests using dataanalysis. This helped to increase the takeup of a range of services – from inflightfood to duty-free.Among our ancillary services, we wereespecially pleased with Fly-Thru,which is a key differentiator for AirAsia,providing our guests an extensive networkthat includes the routes of all countryoperations as well as those of our sisterAirAsia X Group. During the year, Fly-Thrufor both AirAsia and AirAsia X Groups saw a37% increase in take-up to 3.01 million. Thiswas aided by the addition of 497 new citypairs, to total 1,845 routes. klia2 continuedto be the top transit hub, accounting for85% of the overall Fly-Thru traffic, with2.5 million guests passing through theairport during the year. Meanwhile, ouroperations in India saw the highest growthin Fly-Thru traffic, its hubs in Bengaluru,Kolkata and New Delhi accommodating a677% increase in transit guests. Overall,AirAsia and AirAsia X Groups recordedRM204.1 million from Fly-Thru in 2017, andwe foresee higher uptakes in coming yearsas we integrate our operations more fullyand efficiently.As our digital transformation progresses,we will be able to capture even moredata on our guests and use this for moretargeted up-sell and cross-sell of ancillaryproducts. Towards the end of the year,we started using electronic point of sales(ePOS) devices for inflight transactions,and have integrated the data obtained ontoour centralised platform. This enhancesour guest profiles and will guide us inserving them better. It also gives us theconfidence to target achieving RM60in ancillary income per guest by 2020from RM49 as at end 2017. Some say it isambitious, but we ‘dare to dream’.ADJACENCY BUSINESSESAdjacency businesses are those we haveestablished – mostly in partnership withother companies, but some also on ourown steam – to generate income from ourassets and resources. A number of thesecompanies have begun to earn sizeablerevenue, prompting us to monetise them torecognise their value. The process beganin 2015, when we disposed of 25% of ourequity in AirAsia Expedia, our online travelAIRASIA GROUP FLY-THRU(Including AirAsia X Group)3.01MILLION GUESTSin 2017, 37% morethan in 201685%of Fly-Thru guests transitedin Kuala Lumpur677%increase in transit guestsin India in 2017AirAsia Group Berhad[ 95 ]company. The year 2017 was significantas we took our monetisation programme anotch higher.In August, we concluded the sale of AACE,the training company we had establishedin 2011 with CAE International HoldingLtd (CAE), to our Canadian partner forUSD100 million. This effectively gives CAEfull control over AACE’s training centresin Sepang, Singapore and Ho Chi MinhCity – as well as its share of the PhilippineAcademy of Aviation Training (PAAT), ajoint-venture between AACE and CebuPacific, located in Manila. As our exclusivetraining partner, CAE will continue toprovide the highest quality training ofpilots and cabin crew at agreed rates forthe entire Group until 2036.

[ 96 ]AirAsia Group BerhadPERSPECTIVEMANAGEMENT DISCUSSION & ANALYSISIn October, we entered into a 50%partnership for our ground handlingbusiness (Ground Team Red HoldingsSdn Bhd) with Singapore-based SATS,a gateway services and food solutionsprovider. In return, we acquired 40%effective stake in SATS Ground ServicesSingapore Pte Ltd (SGSS), which servesChangi Airport’s new Terminal 4, andretained 51% of Ground Team Red SdnBhd, our Malaysian ground handlingoperations, for SGD119.3 million in cash,which was received in January 2018. Ourjoint venture, SATS Ground Team RedHoldings Sdn Bhd, will take over groundhandling of all AirAsia stations in Malaysiaand Singapore. With SATS as our partner,we expect to drive down our unit aircraftturnaround costs by approximately 16% inthe first year of operations.Additionally, during the year, the teamat our leasing arm Asia Aviation CapitalLimited (AACL) worked around the clockto finalise a deal with BBAM LimitedPartnership (BBAM) for selected aircraftleasing portfolio. On 1 March 2018, wewere able to announce an agreementreached worth USD1.18 billion. For us,this deal validates the huge investmentswe made over the years in aircraftacquisitions, and is a clear indication of thestrategic thought behind all our actions. Asa result of various transactions containedwithin the agreement, we will receiveUSD902 million cash in the later part of2018, while eliminating residual risks andreducing our debt significantly.In the midst of these monetisation deals,we also acquired a 50% stake in travelstart-up Touristly, which offers attractivepromotions on tours, attractions, activities,spas and restaurants around the region.Touristly will take over and managedeals.airasia.com and the online versionof our travel magazine, travel360.com,to present a comprehensive site whereholiday-makers can discover interestingplaces to visit, exciting things to do whilethey are there, and even book theiractivities. It represents a new stream ofrevenue under an increasingly more digitalAirAsia.DIGITALISATIONSince setting up our Digital and Data teamin 2016, the process of digitalising AirAsiahas been gaining momentum, and hasaccumulated a number of snapshot wins.Our mobile conversion rate has increased70% from 3.39% in 2016 to 5.75%. Sincedigitalising our ancillary business inSeptember, the take-up rate of productshas improved by 6.6% with an estimatedrevenue generation of USD1.7 millionper month. From the recently launchedsimplified payment enhancement, ourbooking conversion has increased from7.46% to

operating profit rm million cost per ask sen total assets rm million passengers carried pax shareholders' equity rm million size of . volume 0 0 100,000,000 0.50 50,000,000 1.50 150,000,000 2.00 200,000,000 2.50 250,000,000 3.00 300,000,000 3.50 400,000,000 350,000,000 . & analysis 2017 was yet another phenomenal year. we took delivery of