Transcription

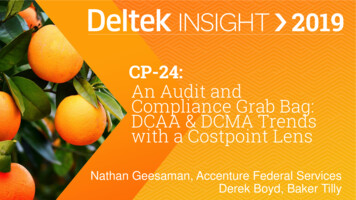

CP-24:An Audit andCompliance Grab Bag:DCAA & DCMA Trendswith a Costpoint LensNathan Geesaman, Accenture Federal ServicesDerek Boyd, Baker Tilly

Agenda Regulatory Updates Managing Audit Requests Hot Topic Areas Where Costpoint Can Help2

National Defense Authorization ActSection 809 Panel Reports and DocumentationCase Law UpdateDCAA UpdateOn the Horizon

Regulatory UpdatesFY19-20 National Defense Authorization Act (NDAA)– 2019 NDAA– Passed by House 7/26/18; passed with amendments by Senate 8/1/18– Signed into law by President 8/13/18Section 821Increase of the micro-purchasethreshold applicable to DoDSection 822Department of Defensecontracting disputes13244Section 836Commercial ItemsSections 851-853Small business matters4

Regulatory UpdatesSection 809 Panel– FY16 NDAA Section 809 required the Secretary of Defense to appoint apanel to streamline the defense acquisition process– The Panel has made a number of recommendations to DoD, published inthe Panels January 2018, June 2018, and January 2019 reports– Professional Practice Guide (PPG) now referenced in DCAA Memorandums– DCAA Recommendations – refocus on mission to help the acquisition team– Policy Recommendations – increased reliance on contractor internal controls– Cost Accounting Standards – decouple from TINA and increase thresholds5

Regulatory UpdatesCase Law Update– COFC: The Boeing Company v. United States (Civil No. 17-1969C) – May 29, 2019– Boeing challenged that CAS benefits the government by not permitting offsets in impacts ofsimultaneous cost accounting practice changes– COFC ruled in favor of the Government, noting a lack of jurisdiction upon failing to raise via pre-awardprotest or contract negotiations– Impacts: How GDMs are completed, plus may lead to an increase in pre-award protests for ‘extra’ FARclauses in contract solicitations– ASBCA: Raytheon Co. (No. 55743) - August 28, 2018– Raytheon challenged several cost allowability issues– The primary ruling in favor of the government stated that salaries for unallowable political activity (i.e.,lobbying) were expressly unallowable and subject to penalties (even though FAR 31.205-22 does notexplicitly discuss salaries or compensation, it is “common sense” that these are included in the principle)6

Regulatory UpdatesDCAA Update – Recent Memorandums for Regional Directors– 18-PSP-006(R) – Audit Guidance on Revised Treatment of Incomplete orInadequate Prime Contractor Cost or Price AnalysesCostpoint Impacts– Alternate procedures for proposed subcontractor costs vs. defaulting to‘unsupported’– 19-PIC-001(R) – Audit Guidance on Revised Policies and Procedures forAuditing Incurred Subcontract and Inter-Organizational Transfer Costs– Plan to increase DCAA coordination for subcontract assist audits withannual ICS audit– 19-PAC-002(R) – Audit Alert on Identifying Expressly Unallowable Costs– DCAA notes to FAR 31 cost principles to support what expresslyunallowable means– 19-PAS-003(R) – Audit Guidance on Materiality in Incurred Cost Audits(CAM 6.107)– Quantified materiality thresholds for ICS audits pursuant to Sec 809 PPG7

Regulatory UpdatesDCAA Update – Updated Audit Programs (AP)– Nearly 50 AP updates in 2019 per DCAA Website – Major changes include:– Incurred Cost Audits– MAARs (e.g., 6-Floorchecks, 13-Purchase Existence and Consumption)– Accounting System audits– CAS Audits8

Regulatory UpdatesOn The HorizonCostpoint Impacts– Mergers & Acquisitions– Continued M&A activity in government contractingmarketplace (large companies)– New entrants, especially private equity firms new tomarketplace– Cybersecurity Maturity Model Certification (CMMC)– DOD requiring contractors to have internal IT systems certifiedby a third-party auditor in 2020, and will begin using as tablestakes for contractors to bid on RFPs– NIST 800-171 (100 requirements), and then some– Draft CMMC summarizing requirements, capabilities, andcertification levels in Sept 2019– Plan to finalize version 1.0 by Jan 2020 and will begin toincorporate into RFPs in Sept 20209

Best PracticesIncurred Cost AuditsMandatory Annual Audit Requirements (MAARS)Proposal/Pricing AuditsContractor Business System Audits

Managing Audit RequestsBest Practices– Confirm appropriate staff members and establish a liaison in a timely manner– Ensure company POC is a knowledgeable and experienced employee– Identify potential issues with achieving stated deadlines quickly after receiving a request– Each data request should be entered on a log and updated daily– Thoroughly review responses/data prior to submitting back to DCAA/DCMA– Incorporate prior year requests into current year preparations– Maintain ongoing logs of all incoming requests and outgoing responses/documentation, including fields for:– Request Number– Date of anticipated contractor response– Assignment number– Date of actual response– Date of receipt of request– Requestor– Date of requested response– Description of Request– Priority Level of Request(low/medium/high)– Status of response (opened/closed)– POC for response (contractor side)11

Managing Audit RequestsIncurred Cost AuditsCostpoint Impacts– Timeline Impacts – DCAA Policy of 60-day adequacy and 1-yearaudit completion– Increased use of third-party auditors (IPA)– Re-adoption of DCAA assist audits from other agencies– Multi-year audits and negotiations– Incurred Cost Submission reporting strategy and Costpoint datavalidation12

Managing Audit RequestsKey Mandatory Annual Audit Requirements (MAARS)– Performed During the Fiscal Year– MAARS 6 – Labor Floor Checks or Interviews– MAARS 13 – Purchase Existence and Consumption– Performed During an FPR or ICS Audit– MAARS 2 – Contract Cost Analysis and Reconciliation to Books– MAARS 10 – Adjusting Entries and Exception Reports– MAARS 3 – Permanent Files– MAARS 12 – Auditable Subcontracts/Assist Audits– MAARS 4 – Tax Returns and Financial Statements– MAARS 14 – Pools and Bases Reconciliation to Books– MAARS 5 – General Ledger, Trial Balance, Income and/or CreditAdjustments– MAARS 15 – Indirect Cost Comparison with Prior Years andBudgets– MAARS 7 – Changes in Charging Direct/Indirect Costs– MAARS 16 – Indirect Account Analysis– MAARS 8 – Comparative Analysis-Sensitive Labor Account– MAARS 17 – Indirect Allocation Bases– MAARS 9 – Payroll/Labor Distribution Reconciliation and Tracing– MAARS 19 – Indirect Rate Computations13

Managing Audit RequestsPricing/Proposal Audits– Proposals may include evaluations of entire proposal, selectedcost elements, or other selected items (as agreed-uponprocedures)– It’s easier to question an estimated cost than an actual costAudit TypeExceptionPercentSustainedForward Pricing61.6%Incurred Cost24.1%Special Audits68.3%Other Audits45.2%Total (Weighted Avg)51.4%– DCAA Sustention Rates – FY18– Even if a pre-award audit isn’t completed, post-award audits arestill possible (i.e., Defective Pricing)– Tripling the number of Truthful Cost and Pricing Audits next fiscal year14

Managing Audit RequestsContractor Business System Audits– Changes in DCAA audit approach – System Description Narrative Template– Risk-based Approach – System risk factors (e.g., CR contracts, ERP system changes, contractor size, timebetween audits)– Renewed Focus – Significant increase in DCAA business system audits expected in the next few years15

Labor Cost AccountingTotal Incurred and Claimed Cost UniversesBilling HistoryProposal Population

Hot Topic Areas Where Costpoint Can HelpLabor Cost Accounting - Direct versus Indirect LaborPAG SetupCOA Setup17

Hot Topic Areas Where Costpoint Can HelpLabor Cost Accounting - Payroll versus Labor and ICS Schedule LADP Interface18

Hot Topic Areas Where Costpoint Can HelpLabor Cost Accounting - Project ChargeabilityManage Employee Work ForceEmployees Linked to PLCs19

Hot Topic Areas Where Costpoint Can HelpLabor Cost Accounting - Labor ReportingProjectLaborSummaryReport(CostReimb &T&M)20

Hot Topic Areas Where Costpoint Can HelpTotal Incurred and Claimed Cost Universes - Incurred Cost Submission Schedules– Incurred versus Claimed Cost on Incurred Cost Submission – Schedules H, I, K– DCAA Incurred Cost Electronically does not inherently differentiate between incurred vs. claimed– Full versus partial claim of indirect rate allocationSchedule of Direct Costs by Contract/Subcontractand Indirect Expense Applied at Claimed RatesFiscal Year End - mm/dd/yyyyJOBORDERCONTRACT NUMBERA. COST TYPE(no entry on title orTravelMaterialODCContractsDirectCosts PlusO/HG&ABase(TCI)ClaimedG -----------------------------------E. TOTAL COMMERCIAL WORK------------TOTAL CONTRACT COSTS------------A. TOTAL COST TYPE:B. OTHER FLEXIBLY PRICEDB. TOTAL OTHER FLEXIBLY PRICEDC. TIME & MAT'LC. TOTAL TIME & MAT'LD. FIXED PRICED. TOTAL FIXED PRICEE. COMMERCIAL WORK21

Hot Topic Areas Where Costpoint Can HelpTotal Incurred and Claimed Cost Universes - Reconciliation of Costs to InvoicesProject Status Report- ITD Billed Amount- CTD Total Expense 22

Hot Topic Areas Where Costpoint Can HelpBilling History - iRAPTCreate iRAPT Billing Files23

Hot Topic Areas Where Costpoint Can HelpBilling History - Track Prior Period BillingsManage Billing HistoryManage Closed Billing Detail24

Hot Topic Areas Where Costpoint Can HelpProposal Population– Required as part of estimating business system audit– Schedule of price proposals submitted to the government for the past 12 months showing thecustomer, contract type, proposed value for each major cost element (e.g., direct material,interdivisional, subcontracts, direct labor, ODC, indirect expenses, COM), and elements that werepartly or entirely estimated using standard costs or a cost estimating relationship (CER). [Paraphrasedfrom DCAA Audit Program 24010 B.01(C)]– Contractor should also have certified cost or pricing data elements tracked as part of this schedule– Level of testing on a proposal will vary by contractor risk profile and prior auditexperience– No direct linkage to Costpoint data– Seek to identify data connection points in Project Setup process between proposal tracking systemand Costpoint25

Summary and Wrap-up– Look out for upcoming industry compliance activity– FY20 NDAA– Incorporation of other Section 809 Panel recommendations– CMMC– Track audit activity and requests - and make sure your contractor’s response toaudits are incorporated into final audit reports!– Leverage Costpoint functionality with adequate system configuration– Costpoint pillar adjustments– Use of PAGs, Workforce, PLCs, Customized reports, etc.26

-Timeline Impacts -DCAA Policy of 60-day adequacy and 1-year audit completion -Increased use of third-party auditors (IPA) -Re-adoption of DCAA assist audits from other agencies -Multi-year audits and negotiations -Incurred Cost Submission reporting strategy and Costpoint data validation Costpoint Impacts