Transcription

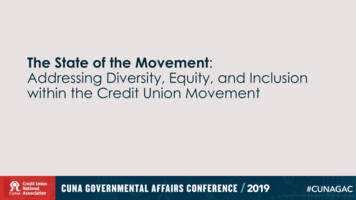

The State of the Movement:Addressing Diversity, Equity, and Inclusionwithin the Credit Union Movement

Framing the SituationEric HansingVP, Multicultural and Corporate Strategy // CUNA Mutual Group

America’s Population is Diverse and Multicultural

Each Generation is Becoming More Racially DiverseRacially Diverse (all other)

Diversity Matters to Business PerformanceAfrican AmericanWhite/OtherHispanicAsian

Diverse Teams Make Better Business Decisions

The Business Imperative for Diversity and rienceDiversity Equity &InclusionMulticultural Marketing& Business LeadershipBusinessPerformance

Connecting to our Shared HistoryWho is today’s “little man?”

Modernizing Our Shared History

Modernizing Our Shared History

Diversity, Equity & Inclusion at CUNAMutual GroupAngela RussellVP, Diversity, Equity and Inclusion // CUNA Mutual Group

What do we mean by ‘Diversity and Inclusion’?Diversity is the wide rangeof differences that existamong people Visible characteristics Less obvious characteristicsInclusion is a workenvironment whereeveryone can participateand is valued regardlessof difference.Source: Diverse Team. Lee, Gardenswartz, and Rowe. Burr Ridge, IL: Irwin Professionals,1994. Note: Internal Dimensions and External Dimensions are adapted from MarilynLoden and Judy Rosener, Workforce America! Burr Ridge, IL: Irwin Professionals, 1991

Source: Interaction Institute for Social Change, ity-vs-equity/Source: Interaction Institute for Social Change, ity-vs-equity/

What isCUNAMutualDoing?

Leadership at the topBob TrunzoCEO, CUNA MutualGroupCreated INCLUSION as acorporate value uponbecoming CEO in 2014

Key Wins in our 1st 4 years Launched 12 ERGs Developed and launched D&ILearning Series Created and launched theInclusion Institute. Created an Early in CareerRotation Program Integrated inclusion into anumber of our policies,procedures and practices. 100% on the Human RightsCampaign Corporate EqualityIndex for 3 years in a row

ransWomen ofDistinctionAsianAmericanEstesSocietyWomen inTechnologyAllies forDisabilitiesWomen inLeadershipDomesticAbuseAwarness

What canyou do?

Common Themes & Emerging Best Practices High level of support Long term commitment Employee Resource Groups/AffinityGroups/BRNs Training: Awareness and skillsbuilding Asking the question: Who benefitsand who is burdened? Data: Quantitative and Qualitative Collaboration and alignment withother efforts Recognition of early winsArt source: Sew Fresh Fabrics - https://www.etsy.com/listing/90138867/

YourorganizationYour TeamYou

Diversity, equity, and inclusion within theCU movementAn analysis of DEI at credit unions and how CUs areserving diverse membersSamira Salem, PhD, Senior Policy Analyst // Credit Union National Association

Diversity, equity and inclusion at CUNA“CUNA is an employer that values an inclusive workspace where employees feelvalued, included and respected for their individuality.” – CUNA CorporateDiversity Statement"CUNA, uniquely positioned to unify the movement, will use its role as thoughtleader to call awareness to Diversity & Inclusion and will provide supportivetraining & education and enable networking opportunities to provoke thoughtfuldialogue and action." – CUNA Board".I challenge all of us in the movement to consider the addition of an eighthcooperative principle: Diversity and inclusion." –Maurice Smith, CUNA Board Chair

Why DEI? Value alignmentDEI aligns with the credit union movements’ principles of “democracy and voluntary membershipwithout discrimination” and of its philosophy of “people helping people.” A solid business caseThere is a decades worth of research showing that organizations that are more diverse tend to performbetter, have better customer orientation and decision-making, are more collaborative, and attractand retain top talent. This suggests that more diverse CUs will be more successful—earning more andgrowing faster. Our core demographicShrinking middle class in the U.S. is struggling high and growing inequality in the U.S. CUs weredesigned to address financial inclusion and the needs of this demographic. We need to redouble ourefforts around equity/financial inclusion. Policy makers and regulators careNewly elected congressional leaders, as well as regulators, have made it clear that they care aboutdeepening financial inclusion for diverse and underserved populations.

DEI is a market imperativePercent Change in U.S. Population,Racial Profile of U.S. Population, 20452010-20503.8% 0.9%Mixed/Other184%Native American3%Asian or Pacific atinoWhite7.9%29%0%50%100%150%200%Source: U.S. Census Bureau, Woods and Poole Economics Inc., Policy Link/PERE National Equity ck*Asian*Multiracial*Other*Source: William H. Frey analysis of U.S. Census Bureau Population Projections, released March 13, 2018 andrevised September 6, 2018, Brookings Institution Metropolitan Policy Program.

CUNA research on DEI at credit unions Our research seeks to answer two questions What does diversity and inclusion look like at credit unions? How are credit unions reaching and serving diverse members? We gather and analyze data HMDAFederal Reserve SCFNCUA Call ReportCUNA Membership Survey and other CUNA SurveysFilene ReportsInclusiv and Coopera Disseminate results via presentations, video economic updates, trendlines articles,white papers, and policy briefs

Credit union leadershipand DEI

Credit union CEO diversity: survey resultsCUCEOsAmericanIndian orAlaska NativeAsianAmericanBlack orAfricanAmericanHispanic/LatinxTwo or MoreRacesWhiteU.S.Fortune 6%2.2%18.1%2.2%1.0%89.8%2.7%60.7%-95.2% The overwhelming majority of CEOsat a typical credit union are whitefollowed by Hispanic/Latinx. Just over 5% of CU CEOs at atypical credit union are people ofcolor—slightly better than Fortune500 companies. The majority of CU CEOs are over 56years old.Source: Credit Union National Association.Source: Credit Union National Association, Census, Forbes, Wall St. Journal and Diversity Inc.

2018 CUNA member survey results The typical credit union board 90% White 8% Black/African American The typical Fortune 500 company board 83.9% White 16.1% People of Color (POC) 8.6% Black/African American3.8% Hispanic/Latinx3.7% Asian/Pacific Islander0.1% Other(Source: Alliance for Board Diversity, 2019) The typical credit union’s leadership team 90% White 5% Black/African American

Credit unions: reaching andserving diverse members

Credit union member diversity: age, employment,education, and incomeCredit Unions MembersAre younger:50.7 years oldAre employed at a higherrate:63.1% employedHave more education:64.4% some college or a BAHave higher median income: 58,955Have (much) lower averageincome: 78,201Have (much) lower averagenet worth: 309,583Bank ClientsCredit unions serve middle-income membersvs. banks serve low- and high-income clients52.3 yearsold60.9%54.1%55.2%employed62.7% somecollege or aBA21.0%20.2% 54,6828.0%4.5% 101,835Credit Union 698,03816.9%14.4% 25,000Bank 25,000 - 100,000 100,000 - 200,00 200,000Source: Federal Reserve, Survey of Consumer Finance, 2016.

Place mattersCUs have a higher percentage of their branches in low-income, modest means, and diverse areasthan banks50% higher proportion of CUbranches in low-incomeareas than banks!7.8%25.80%23.70%Higherpercentage of CUbranches inmodest meansand diverse areasthan banks!29.30%24.40%5.2%11.80%Modest meansLow-incomeCU branches as % of total CU branchesBank branches as % of bank branches10.51%Diverse areas (more than30% Non White)CU branches as % of total CU branchesUpper-incomeBank branches as % of bank branchesSource: NCUA 2018, FDIC 2018, UW-Applied Population Lab, Credit Union Nationall Association.

CUs originate a higher percentage of mortgageloans to Blacks and Hispanics than banksMortgage originations as % of total mortgage originations21.0%20.3%6.6%7.9%5.2%Black/African American7.3%Hispanic/LatinxCredit UnionMinorityBanksNote: “Minority” combines information reported on race and ethnicity. Minority means all races or those of Hispanic/Latinx origin other than White andWhites of Hispanic/Latinx origin.Source: Home Mortgage Disclosure Act (HMDA), 2017.

CUs receive a higher percentage of mortgage loanapplications from people of colorApplications/total applications24%9%10%6%Black/African American9%Hispanic/LatinxCredit Unions23%MinorityBanksNote: Minority” combines information reported on race and ethnicity. Minority means all races or those of Hispanic/Latinx origin other than White andWhites of Hispanic/Latinx origin.Source: HMDA 2017.

All groups saved on their auto loan interest rates atcredit unions, but people of color saved moreAverage interest rate on auto loans8.6%7.3%6.9%6.2%5.9%5.3%4.5%Black/African AmericanHispanic/LatinxCUs4.3%OtherWhiteBanks and Other Financial InstitutionsSource: Federal Reserve, Survey of Consumer Finance, 2016.

Minority Depository Institutions (MDI) CUs outnumberMDI banks, despite FOM restrictions!Race/Ethnicity MDI CUs asset size range: 20.2K to 2.8B MDI CU median assets: 6.1M MDI CU memberships: 3.9M memberships(3.5% of CU memberships)CUBankMDIMDIBlack AmericanHispanic AmericanAsian AmericanNative AmericanTwo or More Races278984913113233875181Total MDI5511525,5485,477MDIs Percent of Total10%3%MDIs Percent of TotalAssets3%1%Total All DepositoryInstitutionsSource: NCUA Call Reports (2018Q3), Credit Union National Association, and FDIC MDI Bank Report (2018 Q3).

Effective ways for CUs to engage people of colorPercentage of responding iveproducts topricing forlow-income higher risk (lowhouseholdsincome) etingMDI CUsNew branches Staff trainingNon-MDI ource: Luis G. Dopico” Reaching Minority Households,” Filene Research Institute, 2016.

Addressing the connection betweenCredit Unions and CU AssociationsAdrian JohnsonSVP/CFO, MECU of Baltimore // Chairman of the Board, AACUC

African-AmericanCredit UnionCoalition

AACUC Strives to: Be the “go to” organization to identify executive talent for creditunion organizations. Work diligently to maintain sound and healthy partnerships thatcan safely adapt to members’ changing needs. Engage young professionals. Provide professional development and networking opportunities. Advocate for credit unions and collaborate with our partners.

Important Statistics – African American CEOs 164 as of August 31, 2018 94 led by Women 48 credit unions less than 1 million in assets 30 led by Women 39 credit unions 1- 6 million in assets 29 led by Women

Important Statistics – African American CEOs 19 credit unions 6 - 20 million in assets 7 led by Women 16 credit unions 20 - 40 million in assets 8 led by Women 12 credit unions 41 - 85 million in assets 6 led by Women

Important Statistics – African American CEOs 4 credit unions 100 - 300 million in assets 1 led by a Woman, Lynette Smith, Board Secretary of the AACUC 8 credit unions over 400 million in assets 1 led by a Woman, Tiffany Ford ( 857)

Important Statistics – African American CEOs4 credit unions over 1billion in assets Tyrone Muse, Visions Credit Union Don Lewis, Aberdeen Proving Ground FCU John Hamilton, MECU of Baltimore, Inc. Maurice Smith, Local Government FCU

CUNA’s Collaborationwith AACUC2002 30K Grant to create2002Internship Program20022015 to Present Promotion ofthe African American Credit2015Union Hall Of Fame recipientsand Networking Receptionduring the GAC2016 to PresentBronze Sponsor atAnnual ConferencesCUNA names Nate Burns,CUNA EngagementConsultant, as the officialAACUC liaison20162002 to PresentBooth at the GAC2016 to PresentProduce marketing videosand press releases2016Diversity Exchange Project(CU Development Educators2018& AACUC Members attendeach other’s conferences)2018

Financial Inclusion within theCredit Union MovementCathie MahonPresident & CEO // Inclusiv(formerly the National Federation of Community Development Credit Unions)

What is an Inclusive Economy? Economic Inclusion is equal and fair access to the means by whichindividual(s) can pursue economic mobility and advancement An inclusive economy is one without unequal barriers or obstacles tothat economic mobility whether it be fair and equal access toeducation, employment or capital. US Economy has been moving in the wrong direction. The incomeearners have more than doubled their share of the nation’s incomesince the middle of the 20th century. The bottom 90% of all earnersearn less than half of all income.

Wealth Inequality In the US Only 40% of Americans havesufficient savings to withstand a 400 emergency. Median whitehousehold possessed 13 in netwealth for every dollar held by themedian black household; and 10for each dollar held by the medianLatino/a household. (Survey ofConsumer Finances)Homeownership by 0.0%47.2%54.4%10.0%0.0%WhiteAfrican Americansource: Prosperity Now 2019 ScorecardLatino\aAsianNative American

Lower-income and communities of color havedisproportionately less access to financial servicesSource: Mapping Financial Opportunity, Terri Friedline, University of Kansas, 2016.

A History of Addressing Race DiscriminationAnd Building Wealth Through CUs

Where We Are Today: CUs dedicatedto Building Inclusive Economies

But We Must Work to Preserve It

Celebrating Our Legacy of Inclusiv Credit Unions Inclusiv and AACUC celebrated African Americancredit unions with a social media and printcampaign for Black History Month Featured impact stories, testimonials, memberspotlights and profiles from two dozen credit unionswith 12 social media posts and a new 16-page printpiece, African American Credit Unions Build StrongCommunities Launched test of inclusivcommunities.org forconsumers in NY to find an African American CUnear them

Inclusiv Communities: Reaching financially “excluded” consumers and bridging theracial wealth gap by building the reach and capacity of credit unions Strengthening African American and JuntosAvanzamos Credit Unions Capital investments in the form of deposits,secondary capital and mortgage purchase Building ties with trusted partners to expand accessto CU services and products Direct to consumer marketing and supportingplatforms for consumers to access these vitalinstitutions

Panel DiscussionModerator: Eric Hansing, VP Multicultural and Corporate Strategy // CUNA Mutual GroupAngela Russell, VP Diversity, Equity, and Inclusion // CUNA Mutual GroupSamira Salem, PhD, Senior Policy Analyst // CUNAAdrian Johnson, SVP/CFO, MECU of Baltimore // Chairman of the Board, AACUCCathie Mahon, President/CEO // inclusiv

Thank you!

loans to Blacks and Hispanics than banks 6.6% 7.9% 20.3% 5.2% 7.3% 21.0% Black/African American Hispanic/Latinx Minority Mortgage originations as % of total mortgage originations Credit Union Banks Source: Home Mortgage Disclosure Act (HMDA), 2017. Note: "Minority" combines information reported on race and ethnicity. Minority means all races or those of Hispanic/Latinx origin other than .