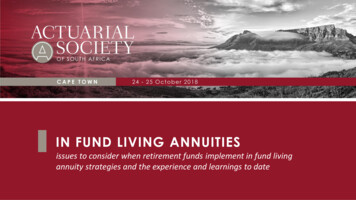

Transcription

IN FUND LIVING ANNUITIESissues to consider when retirement funds implement in fund livingannuity strategies and the experience and learnings to date

SETTING THE SCENE

Nat i o nal Tre as ury C o nc e rns“Currently workers benefit from a strong support structure provided by the retirement system while theyare employed, which is effectively withdrawn for the vast majority of these workers after they retire.At retirement the workers are then left to the retail market, where they must bear the risks of retirementon their own, including the risks of poor financial advice, poor decisions, and high charges.““In order to increase the competitiveness of the market for retirement income products, toprovide a greater degree of assistance to members of retirement funds who retire, and torequire funds to use their considerable purchasing power and skill to provide their memberswith cost-effective annuitisation options”

Nat i o nal Tre as ury C o nc e rns“National Treasury has put forward a series of regulations that all retirement funds are supposed toimplement as of the second quarter of 2019, which will see the fund trustees being obligated to paymore attention to the retirement income products that their membership are offered and topotentially offer an in-fund default option, which the trustees can impose further limits on.”Jaco van Tonder, Advisor Services Director, Investec Asset ManagementSeptember 2018

Imagi ne y o u are re ac hi ng re t i re me nt age ri ght no w Which of the following options would you choose?All RespondentsA pension from your employer's retirement fund50324047.7%SANLAM BENCHMARK 2015

ASISA L i fe Ins uranc e s t at i s t i c sFor the period to 31 December 2016

ASISA L i fe Ins uranc e s t at i s t i c s2016 New Business Statistics - Living Annuities# PoliciesSingle PremiumsAverage SinglePremiumLiving Annuities55,086R 56,810,000,000R 1,031,297Compulsory Annuities13,950R 5,286,000,000R 378,9252017 Living Annuities SurveySouth Africans had R421.9 billion of their retirement savings invested in 447 560 living annuities

Sc o pe o f re s e arc h Living annuities are the de facto annuity of choice for retiring South Africansdespite shortcomings Default Regulations specifically mention both In Fund and Out of Fund livingannuities Therefore we aim to contrast these two types of living annuity and shareexperiences and learnings to date We are not specifically focusing on:o Living annuity v life annuityo Optimal transitioning strategies from living annuity to life annuitythough these are important subjects for further research

L i vi ng annui t i e s 10 k e y di ffe re nc e s (be s i de s c o s t s )In Fund living annuitiesOut of Fund living annuities (via insurer)Subject to Pension Funds ActSubject to Long Term Insurance ActGovernance overseen by Board of TrusteesIndividual insurance contract37C of Pension Fund Act (currently) applies on deathBeneficiary nomination prevails on deathRegulation 28 appliesRegulation 28 does not apply yetRegulation 39 applies – trustees to monitor sustainabilityNo explicit sustainability monitoring by trusteesCan be converted to ex fund living annuityCannot be converted to in fund living annuityASISA standards good practice (EAC & disclosure)ASISA standards mandatory (EAC & disclosure)FAIS categorization debatableFAIS Retail Pension Benefits appliesFICA requirement less burdensome upon implementationFICA applies upon implementationSection 37A & 37B – significant protection from creditorsLess certain protection from creditors

SANLAM ADMINISTRATOR DATA ANALYSIS

Si ze o f B o o kJune 2018June 2017Number of retirement funds offering IFLAs *109Number of IFLAs698557R2 091 543 014R1 609 576 979Total IFLA asset valuesAverage fund value* All retirement funds comprising R1b assets - 300 000 active membersR 2 996 480R2 889 725

Drawdo wn Anal y s i sSanlamJune 2018ASISADecember 2017R13 963R7 133Average drawdown rate (unweighted)7.39%9.08%Average drawdown rate (weighted by asset value)5.59%6.64%Average monthly pension

Sanl am IF L A vs ASISA L i vi ng Annui t y dat a

The Po we r o f Sc al eLiving annuity income drawdownR5 000 000 consideration and 1% cost saving per annumMonthly income (R)10000 R50 000 extra annual pension R4 000 extra monthly pensionLife expectancy line50000Retail ILLAInstitutional ILLA16111621Drawdown period in years26

Ave rage C o s t s Anal y s i s ( ac ro s s t he bo o k )SanlamIFLA2018Major LISP A Major LISP B20182018Treasury2012 *Administration0.05%0.39%0.52%0.48%Advice %Investment Management0.76%Total1.77%* Sample of one LISP mentioned in 2012 Treasury paper** Average advice fee for annuitants paying for advice

‘The challenge going forward will be to get somewhere in between,i.e. you cannot deliver a retail service and product at wholesale costs and vice versa .the pricing gap is big, but some of it is for a reason Institutional businesses are not geared for retailDawie de VilliersChief ExecutiveSanlam Employee Benefits’

RETIREMENT FUND SURVEY

Surve y Ove rvi e w Retirement funds offering In Fund Living Annuities (“IFLAs”)Various administratorsVoluntary participationFund officials with knowledge of offeringOnline survey softwareRespondents identifiableResponses during September 201845 questionsAverage completion time of 26 minutes15 retirement funds22 respondentso 1 trustee, 8 principal officers, 8 consultants, 3 valuators & 2 employersEXTREME CAUTION : SAMPLE SMALL BUT RESPONDENTS CREDIBLE!!

Surve y re s ul t sWhen IFLA introduced?# ResponsesBefore 2011102011 to 20140Since 201512Es t i mat e s o f IF L A me mbe rs hi p 3 890 annuitants at 30 June 2018 291 new annuitants in past year 72 annuities ceased in past year 19% of retirees opt for an IFLA

3 Mai n R e as o ns fo r Trus t e e s Int ro duc i ng IF L A?Possible Responses# SelectionsAdministration cost savings18Investment management fee savings15Wary about the quality of financial advice in retail market6Wary about the cost of financial advice in retail market5Continue with pre-retirement investment strategy5Seamless transition at retirement5

3 Mai n R e as o ns fo r R e t i re e s C ho o s i ng IF L A?Possible Responses# SelectionsInvestment management fee savings18Administration cost savings14Wary about the cost of financial advice in retail market10Continue with pre-retirement investment strategy8Seamless transition at retirement8

INVESTMENT & DRAWDOWN RATE RISKS

D o T r u s te e s f o r m a l l y r e g u l a r l y r e v i e w ?I F L A i n v e s tm e n tchoicesI F L A s e l e c te dd r a w d o w n r a te sYes1314No97I am not sure00

W o u l d T r u s te e s i n te r v e n e ?S u b - o p ti m a linvestmentchoicesU n s u s ta i n a b l yhigh drawdownr a te sDefinitely310Probably105Might or might not31Probably not54Definitely not00

H as s uc h i nt e rve nt i o n e ve r be e n ne c e s s ary t o dat e ?IFLAInvestment ChoicesI F L A s e l e c te dd r a w d o w n r a te sYes19No2013I am not sure10

Is there a cap imposed by the trustees for drawdown rates?# SelectionsNo cap aside from the regulatory 17.5% limit10A flat cap of X% (answers ranged from 6% to 10%)3An age-related cap below the regulatory 17.5%9

W o u l d y o u p r e f e r a f i x e d d r a w d o w n r e v i e w d a te e a c h y e a r ?# SelectionsNo6Yes12Maybe3

Numbe r o f Avai l abl e Inve s t me nt Po rt fo l i o s fo r IF L As ?# Selections112–4105 – 10711 - 204 200

W o u l d y o u p r e f e r th a t R e g u l a ti o n 2 8 d o e s n o t a p p l y to I F L As ?# SelectionsYes7No13Maybe2

F o c us o n ri s k sPath dependency / sequence of returns risk Poor returns upfront reduce likelihood of successful retirement To maintain real income drawing down many “cheap” unitsReckless conservatism Too conservatively invested Need appropriate CPI return over 20-30 year horizon Else income not keeping pace with inflation

Se que nc i ng o f re t urnsCu m u l a ti v e r e tu r n s o v e r 2 0 y e a r s f o r e v e r y R 1 i n v e s te dR7R6R5SequenceReverse sequenceR4R3R2R1R0123456789 4151617-8% -12% 10%1819201%-9%-4%Sequence20% 10% 18% 13% 10% 19% 26%9%5%31%7%14% 22%-5%Reversed-4%22% 14%7%31%5%26% 19% 10% 13% 18% 10% 20%-9%1%10% -12% -8%-5%9%article by Glacier

Se que nc i ng o f re t urnsR 1 m l i v i n g a n n u i ty - 6 % i n f l a ti o n ; s ta r t 6 % d r a w d o w n (i n f l a ti o n e s c a l a ti o n everse 891011121314151617-8% -12% 10%1819201%-9%-4%Sequence20% 10% 18% 13% 10% 19% 26%9%5%31%7%14% 22%-5%Reversed-4%22% 14%7%31%5%26% 19% 10% 13% 18% 10% 20%-9%1%10% -12% -8%-5%9%article by Glacier

Mitigating sequence return riskReal pension & 5% drawdownNegative return environment (5% Percentile)ConservativePercentileSustainable Years5%14.625% 00030,00020,00010,000051015Conservative; 5%20Max 25% SB; 5%25Aggressive; 5%3035

Mitigating sequence return riskReal pension & 5% drawdownNegative return environment (5% Percentile)ConservativePercentileSustainable Years5%14.625% SmoothedBonus5%14.8Average return environment (50% Percentile)AggressiveConservative5%12.850%23.025% 0,00030,00020,00010,00005Conservative; 50%10Max 25% SB; 50%15Aggressive; 50%20Conservative; 5%25Max 25% SB; 5%30Aggressive; 5%35

Does the Fund facilitate life annuity quotations# SelectionsI am not sure3No7Yes12

Conversion to a guaranteed annuityR1m available at retirement in guaranteed annuity60655% guaranteed escalation annuity start with a pension of R99 978 p.a. increase each year with 5% p.a. pension of R121 524 p.a. at age 70707580

Conversion to a guaranteed annuityR1m available at retirement in living annuity6065707580living annuity – withdraw same income as guaranteed annuity 5 years later - to buy guaranteed pension of R121 524 p.a. (age 70) need R1.050 m Yield curve and mortality basis unchanged what living annuity return needed - to afford guaranteed annuity after 5 years?

Conversion to a guaranteed annuityR1m available at retirement in living annuity60fixed 5%escalationannuity65return neededto afford samepension707580after 5 years- 14.13%after 10 years- 15.29%after 15 years- 16.01%

DEFAULT REGULATIONS

R e gul at i o n 39W i l l I F L A f o r m p a r t o f F u n d ’ s a n n u i tys tr a te g y i . t. o . R e g u l a ti o n 3 9 ?W i l l I F L A b e p r e f e r r e d a n n u i ty i . t. oR e g u l a ti o n 3 9 f o r q u a l i f y i n g r e ti r e e s ?# Selections# SelectionsYes17Yes8No1No3I am not sure4I am not sure6

Anticipated changes to IFLA to comply with default regulations?Possible Responses# MentionsThe minimum Rand amount to enroll will be reviewed2The drawdown caps will be reviewed4The number of available investment options will be reviewed6The current fees will be reviewed2None7We have not yet considered7

ADVICE

U WR F De faul t Annui t y Expe ri e nc e The University of the Witwatersrand Retirement Fund offered all retiring membersa default annuity from the mid-to-late 1990s to its discontinuance in 2003. Herethe default annuity was a Guaranteed Annuity in the name of the Fundattractively priced and on a commission free basis. The actual experience was that no retiring member elected the default annuityoption upon retirement, and all chose to invest their retirement proceedselsewhere. It might be that the Fund’s default annuity option did serve a usefulpurpose as a reference point for retirees to benchmark other options against,but from a commercial / take-up perspective, it was a dismal failure.

F e at ure s o f a go o d de faul t annui t y s t rat e gy Make access simple & unpressurised Same member experience pre- and post-retirement Contributions cease and pensions begin Seamless Align with pre-retirement investment strategy No time out of the market No up front costs Avoid discontinuities Not irreversible Can switch to ILLA or guaranteed annuity at any point Optionality is very valuable for retirees with 20 years life expectancy Accommodate financial advisersInertia is the most powerful force in the universe!

Institutional v retail worlds are colliding

F i nanc i al Advi s e r F e e dbac k‘Living annuities are complex when compared to conventional life annuitiesOwners of living annuities make / review several choices annually. These decisions could haveserious consequences that only become apparent years later.Buyers of living annuities must: Choose an investment mix from extensive options Choose a drawdown rate (between 2.5% and 17.5%) Select a provider or change their existing providerDecisions are dependent on a range of factors that vary from individual to individual, including: The level of support they can expect from family Access to post-retirement medical aid cover Risk aversion Bequest motives Life expectancy’

EB C o ns ul t ant F e e dbac k‘ Make provision for advisers’ fees (I was against it initially) but cap it!! Most of theadvice work is done by the Trustees (with age banded caps aiming to ensuresustainability and the investment menu is vetted). Don’t underestimate the power of the adviser (I made that mistake) their relationshipand influence over the retiring member is such that they will talk the members out ofit. I will see the Board as seriously failing their fiduciary duties, being complicit to orfacilitating the fleecing of members and to quote John Vorster “too ghastly tocontemplate”.’

H a s F u n d Ap p r o v e d a R e s tr i c te d P a n e l o f Ad v i s e r s f o r I F L As ?# SelectionsYes11No11I am not sure0

Does Fund Facilitate Payment of Advice Fees to IFLA Advisers?# SelectionsYes9No13I am not sure0

If no , who pro vi de s advi c e o n IF L As ?# SelectionsSalaried retirement counsellor paid by the Fund4Salaried retirement counsellor paid by the Employer3Member must seek and pay for own advice outside the Fund6

Ec o no mi c s 101 fo r fi nanc i al advi s e rs Fund Credit# RetirementsRetirement Amounts 1m312R804m500k-1m157R106m150k - 500k371R103m25k - 150k380R28m0-25k175R2mTotal1,395R1,042m R500k33.6%87.4%based on Sanlam Umbrella Fund exits 2016viable

Impac t o f Advi c eNumber of pensionersAverage drawdown rateAverage fund valueWith adviceWithout advice886105.03%5.66%R 2 651 170R 3 046 295

LEARNINGS & RECOMMENDATIONS

De s c ri be up t o 3 fe at ure s y o u l i k e abo ut IF L AsOur Categorisation# MentionsCost effective19Seamless transition at retirement12Flexibility of living annuities7Trustees can add value post-retirement5

De s c ri be up t o 3 fe at ure s y o u di s l i k e abo ut IF L AsOur Categorisation# MentionsMonitoring burden for Trustees10Administration burden for Trustees8Fear of possible risks e.g. drawdown rates & investments8Death benefit complications5Communication & reporting challenges5

B e t t e r R e t i re me nt Out c o me s“Provided that the Board can do a decent job (and are prepared to take on the extra governance),the odds favour a better retiree outcome with an in-fund strategy.”Ant Lester, Willis Towers WatsonAugust 2018

S AI F AA P r e s e n ta ti o n 2 0 1 7 – F i n a l T h o u g h ts In Fund Living Annuities are a viable / compelling option for many retirees Savvy affluent retirees are the initial base of investors Pricing differences between institutional and retail likely to narrow over time Good advisers should be putting these options on the table Retirement funds must consider solutions holistically e.g. how to assist all members on anational basis Important to guide members on switching to other annuity products over time e.g.guaranteed or hybrid annuities to protect longevity risk. Product in infancy and retirees relatively young – longer term risks might not yet beapparent

2018 – Additional Final Thoughts Recent emergence of institutionally priced Out of Fund Living Annuities Will be interesting to see the outcome of default regulations post 1 March 2019 Not clear to what extent fees quoted represent marketing ahead of implementation of defaultregulationsWorth analysing costs in future researchSome retirement funds only at start of deliberations on Regulation 39Planned FSCA notice on maximum drawdown rates, sustainability and communicationIFLAs are a valid product proposition with pros and cons compared to other annuity options Main raison d’etre is lower costs compared to other living annuities so long term take-up will beimpacted by cost reduction trends in respect of such alternative annuities.Possibly not a viable option for retirement funds with R1 billion assets?

7 R e c o m m e n d a ti o n s – L e v e l p l a y i n g f i e l d s (w h e r e a p p r o p r i a te ) Strengthen competition and improve client value proposition by allowing consolidationof IFLAs and Out of Fund Living Annuities Strengthen competition by opening transferability between IFLAs and Out of Fund LivingAnnuities Beneficiary nomination not S37C desirable for allocation of IFLA death benefits ASISA standards should be implemented for IFLAs (requires legislative change) Retirement fund trustees need to rethink advice and support for IFLAs Annual drawdown rate reviews at a fixed date per retirement fund an improvement FAIS categorizations need rethinking to cater for In Fund preservation and annuities(based on skill set as opposed to licensing)

Cr e d i tsDerek Smorenburg2017 living annuity workshopsAnnelie de Kockdata extractionWagieda Pathersurvey supportLorraine Loubserpresentation formattingAnton Swanepoellegal wisdomPG Maraislegal technical detailGrant Baseofficial reviewerJaco van Tonderexpert criticismSurvey participantssharing experiences

THANK YOU

R1m available at retirement in living annuity living annuity -withdraw same income as guaranteed annuity 5 years later - to buy guaranteed pension of R121 524 p.a. (age 70) need R1.050 m Yield curve and mortality basis unchanged what living annuity return needed - to afford guaranteed annuity after 5 years?