Transcription

IFRS US GAAPRobert Mládek

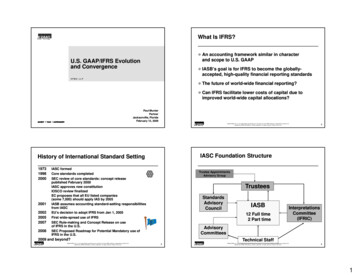

IFRS US GAAP training manual including examplesIFRS US GAAP training manual including examples . 3Introduction . 3Recognition . 6Measurement . 8Disclosure. 9Conceptual Framework . 10Accounting Elements . 11“The Principles” . 15“Revenue Recognition Principal”. 15Revenue Recognition Standard . 16Constraints . 17Materiality . 17Probability . 17Fair Value . 18The Statement of Financial Position (balance sheet) . 20Cash and Cash Equivalents . 22Short-Investments . 24Receivables, Contract Assets and Selected Revenue Recognition Issues. 31Recognition . 31Measurement . 31Related Parties . 58Subsequent Measurement . 59Inventory and Selected Revenue Recognition Issues . 63Recognition . 63Measurement . 63Subsequent Measurement . 65Derecognition (revenue recognition). 88Accruals . 89Property, Plant and Equipment (PP&E) . 91Recognition . 91Measurement . 92Subsequent Measurement . 110Intangible Assets . 118Recognition . 118Measurement . 119Subsequent Measurement . 119Goodwill . 120Leasing . 121Recognition (lessee) . 121Measurement (lessee and lessor) . 122Subsequent Measurement (lessee) . 123Real Estate. 132Lessor . 138Other Fixed Assets . 148Liabilities. 149Recognition . 149Measurement . 149Extinguishment (derecognizing) . 149Provisions Contingent Liabilities . 156Equity . 157Statement of Changes in Financial Position (statement of income, statement of profit and loss) . 159Recognition and Disclosure . 161Inventoriable (product) Costs. 162Non-inventoriable (period) Costs . 163Research and Development . 164Services . 166Percentage of Completion (POC) . 167Appendix . 173Impairment . 173Fair Value Examples . 176Investments, Financial Instruments . 180Derivatives . 181IFRS 10 Consolidation Decision Tree . 183Consolidation Basics . 184Government Grants . 187Foreign Currencies. 187Segments . 196Statement of Changes in Equity, Statement of Cash Flow . 197Basic IFRS US GAAP Compatible Chart of Accounts . 198IFRS US GAAP online . 200Copyright and terms of use . 206Copyright Robert Mládek May 7, 20222

IFRS US GAAP training manual including examplesIFRS US GAAP training manual including examplesIFRS US GAAP studijní materiál s příkladyIntroductionÚvodLanguage / JazykIFRS preface: The approved text of any discussion document, exposure draft or IFRS is that approved by the IASB in the Englishlanguage. The IASB may approve translations in other languages, provided that the translation is prepared in accordance with aprocess that provides assurance of the quality IFRS předmluva: Schválené znění všech diskusních dokumentů, návrhů či standardů IFRS schválených IASB v anglickém jazyce. IASBmůže schválit překlady v jiných jazycích, za předpokladu, že překlad je připraven v souladu s procesem, který poskytuje záruku nakvalitou IFRS US GAAPFramework Based Teaching1 / Výuka založená na koncepčním rámciConceptual Framework: CF CON / Koncepční rámecStandards: IFRS, IAS ASC / StandardyInterpretations2: IFRIC, SIC / InterpretaceObjective of Financial Reporting / Účel finančního výkaznictvíUsers of Financial Information / Uživatelé finanční informace123 n/Documents/IASB Staff event for teachers/Teaching material 2014.pdfUS GAAP “interpretations” (EITF consensus opinions) are integrated into the ASC (asc.fasb.org). Unless explicitly stated, they are as authoritative as all otherASC guidance. To determine if the source of particular guidance the EITF, one would examine the original ASU, for example ASU 2019-02.2Copyright Robert Mládek May 7, 20223

IFRS US GAAP training manual including examplesStatutory Accounting (“National GAAP”) vs. Financial Reporting (IFRS US GAAP) / Národní účetní standardy versus IFRS & US GAAPStatutory Accounting / Statutární účetnictvíServe a wide range of stakeholdersSlouží širokému okruhu zainteresovaných stranFinancial Reporting / Finanční výkaznictvíServe capital providers (investors and creditors)Slouží investorům (vlastníkům a věřitelům)Promulgated by governmentsUpravované zákonem (tvořené státem)Promulgated by independent (non-governmental) panel of expertsNeupravované zákonem (tvořené nezávislou radou expertů)LegalisticPrávně formalistické (zaměřené na postupy)Principles basedZaložené na zásadách a úsudku (zaměřené na výstupy)Procedural / Založení na postupechPrescribed chart of accountsPředepsaná struktura (směrná účtová osnova)Judgmental/ Založení na výstupechNo particular chart of accounts defined or discussedKaždá entita má právo definovat vlastní osnovuPrescribed accounting proceduresNařízené postupy účtování (souvztažnosti)Accounting procedures established using professional judgmentUpravují, jak aplikovat zásady na transakce a událostiAccounting statements define form and contentPředepisují formálně definované účetní závěrkyFinancial reports give priority to substance over formVyžadují srovnatelné finanční zprávyStatutární účetnictví / Statutory AccountingČÚS 19.4 21: Účtová skupina 60 - Tržby za vlastní výkony a zboží: Ve prospěch účtů této účtové skupiny se účtují na základě příslušnýchdokladů (například faktur) tržby se souvztažným zápisem na vrub příslušných účtů účtové skupiny 31 - Pohledávky (krátkodobé idlouhodobé), popřípadě příslušného účtu účtové skupiny 21 - Peníze.CAS 19. 4.2: Account group 60 - Revenues from own performances and merchandise: In favor of accounts of the accounting group [60] arecredited, on the basis of relevant documents (such as invoices), revenues with the corresponding entry debited to the respective accountsof account group 31 – Receivables (short and long term) or the relevant account of account group 21 – Cash.Financial Reporting / Finanční výkaznictvíIFRS 15.31 ASC 606-10-25-23: .An entity shall recognize revenue when (or as) the entity satisfies a performance obligation bytransferring a promised good or service (i.e. an asset) to a customer. An asset is transferred when (or as) the customer obtains control ofthat asset.IFRS US GAAP: . Entita uzná výnos, když (nebo jak) splňuje výkonnostní povinnosti tím, že převádí slíbené zboží (výrobek) nebo službu (tj.majetek) na zákazníka. Majetek se převedl, přebere-li (přebírá-li) zákazník kontrolu tímto majetkem.Substance over form2 / Podstata nad formouCF (2018) CON 8 QC12: Financial reports represent economic phenomena in words and numbers. To be useful, financial information mustnot only represent relevant phenomena, but it must also faithfully represent the substance of the phenomena that it purports torepresent. In many circumstances, the substance of an economic phenomenon and its legal form are the same. If they are not the same,providing information only about the legal form would not faithfully represent the economic phenomenon (see paragraphs 4.59–4.62).IFRS US GAAP: Finanční zprávy představují ekonomické jevy ve slovech a číslech. K tomu, aby byly užitečné, musí finanční informacenejen představovat významné jevy, ale také musí věrně představovat podstatu jevů, které má představovat. V mnoha případech jepodstata hospodářského jevu a jeho právní forma stejná. Pokud tomu tak není, poskytnutí informací pouze o právní formě nebude věrněpředstavení ekonomického jevu (viz body 4.59-4.62).1Source: Czech national standards conforming to the EU accounting directive.CF (2010) BC2.12 CON 8 BC3.26: Substance over form is not considered a separate component of faithful representation because it would be redundant.Faithful representation means that financial information represents the substance of an economic phenomenon rather than merely representing its legal form.Representing a legal form that differs from the economic substance of the underlying economic phenomenon could not result in a faithful representation.CF (2018) BC2.33: In developing the 2018 Conceptual Framework, the Board noted that some stake holders had inferred that the 2010 deletion of thereference to substance over form meant that the Board was no longer committed to depicting the substance of an economic phenomenon. The Board did notintend to imply such a change. Accordingly, to avoid any further misunderstandings and to high light the Board’s intention, the Board reinstated in paragraph2.12 of the 2018 Conceptual Framework an explicit reference to the need to faithfully represent the substance of an economic phenomenon. The Boardexplained further how to provide a faithful representation of the substance of contractual rights and contractual obligations in paragraphs 4.59–4.62 of the2018 Conceptual Framework.2Copyright Robert Mládek May 7, 20224

IFRS US GAAP training manual including examplesRecognition, Measurement and DisclosureRozpoznání (zaúčtování), Měření (ocenění), Vykazování1st Recognition (a.k.a. classification)Rozpoznání (zaúčtování)2nd Measurement (a.k.a. valuation)Měření (ocenění)3rd Disclosure (reporting, presentation)VykazováníThe accounting equation1 / Účetní rovnice1Physical versus financial concept of capital: CON 8.4 E77: The financial capital concept is the traditional view and is generally the capital maintenanceconcept in present primary financial statements.CF 8.2 (revised): The selection of the appropriate concept of capital by an entity should be based on the needs of the users of its financial statements. Thus, afinancial concept of capital should be adopted if the users of financial statements are primarily concerned with the maintenance of nominal invested capital orthe purchasing power of invested capital. If, however, the main concern of users is with the operating capability of the entity, a physical concept of capitalshould be used. The concept chosen indicates the goal to be attained in determining profit, even though there may be some measurement difficulties inmaking the concept operational.CF 8.2 (revised): The selection of the measurement bases and concept of capital maintenance will determine the accounting model used in the preparation ofthe financial statements. Different accounting models exhibit different degrees of relevance and reliability and, as in other areas, management must seek abalance between relevance and reliability. This Conceptual Framework is applicable to a range of accounting models and provides guidance on preparing andpresenting the financial statements constructed under the chosen model. At the present time, it is not the intention of the Board to prescribe a particularmodel other than in exceptional circumstances, such as for those entities reporting in the currency of a hyperinflationary economy. This intention will,however, be reviewed in the light of world developments.Copyright Robert Mládek May 7, 20225

IFRS US GAAP training manual including examplesRecognitionRozpoznání Elements / Prvky1.Assets / Majetek2.Liabilities / Závazky3.Equity1 / Kapitál4.Revenue2 / Výnosy (tržby)5.Expenses / Náklady6.Gains / Zisky (přírůstky)7.Losses / Ztráty (úbytky)8.Investments by owners / Kapitálové vklady9.Distributions to owners / Výplaty vlastníkům10. Comprehensive income / Úplný (souhrnný) hospodářský výsledek Function of expense3 / Účel nákladůProduction: cost of sales, cost of revenue / Výroba: náklady na prodané zboží, služby a výrobkySales: distribution costs, selling and marketing expense / Odbyt: distribuce, odbyt a marketingAdministration: general and administrative expense / Správa: administrativní a obecní nákladyPeripheral activity: other/financial income & exp. / Periferní činnost: ostatní/finanční výnosy a nákladyEvents & circumstances: gains & losses / Události a okolnosti: zisky (přírůstky) a ztráty (úbytky) Nature of expense4 / Druhové členění nákladůIncrease (decrease) in inventories / Změna zásob výrobků a nedokončené výrobyOther work performed by entity and capitalised / Aktivace vlastní práceRaw materials and consumables used / Přímý a nepřímý materiálEmployee benefits expense / Zaměstnanecké požitkyDepreciation and amortisation expense / Odpisy hmotného a nehmotného majetku1IFRS aggregates assets, Liabilities and equity as financial position.IFRS aggregates revenue and gains as Income, expenses and losses as Expenses.3IAS 1.99: An entity shall present an analysis of expenses recognised in profit or loss using a classification based on either their nature or their function withinthe entity, whichever provides information that is reliable and more relevant. .4IAS 1.104: An entity classifying expenses by function shall disclose additional information on the nature of expenses, including depreciation and amortisationexpense and employee benefits expense.2Copyright Robert Mládek May 7, 20226

IFRS US GAAP training manual including examplesSummary of basic balance sheet sub-classifications / Přehled běžných sub-klasifikací rozvahyAssets LiabilitiesMajetek EquityZávazkyKapitálCurrentCurrentPaid in capitalBěžnýKrátkodobéVložený kapitálCash, Cash equivalents and short-term investmentsPayables- At parPeníze, peněžní ekvivalenty a krátkodobé investiceBěžné závazky- V nominální hodnotěReceivablesAccrued Liabilities- In addition to parPohledávkyČasové rozlišení (akruály)- Emisní ažioInventoryShort-term loansRetained earningsZásobyPůjčkyNerozdělený ziskAccrued assetsOther current Liabilities- UnappropriatedČasové rozlišení (akruály)Ostatní krátkodobé závazky- DisponibilníNon-currentNon-current- Appropriated (reserves)DlouhodobýDlouhodobéLong-term Investments (financial instruments)Bonds payableAccumulated OCIDlouhodobé Investice (finanční nástroje)DluhopisyKumulace OÚHV*Property plant & equipmentLoans payableOther equity itemsHmotný majetekPůjčkyOstatní kapitálové položkyIntangible assets (including goodwill)Lease obligationsNehmotný majetek (včetně goodwill)LeasingResources, biological and other assetsProvisions (contingent Liabilities)Zdroje, biologický a ostatní majetekRezervy- Fondy ze ziskuIFRS1 XBRL balance sheet sub-classifications / IFRS XBRL sub-klasifikace rozvahyAssets Equity LiabilitiesNon-currentIssued capitalNon-currentProperty, plant and equipmentRetained earningsNon-current provisionsInvestment propertyShare premiumEmployee benefitsGoodwillTreasury sharesOther provisionsIntangible assets other than goodwillOther equity interestTrade and other payablesInvestments, equity methodOther reservesDeferred tax LiabilitiesSubsidiaries, joint ventures, associatesEquity attributable to parentCurrent tax Liabilities, non-currentNon-current biological assetsNon-controlling interestsOther financial LiabilitiesTrade, other non-current receivablesOther non-financial LiabilitiesNon-current inventoriesDeferred tax assetsCurrent tax assets, non-currentOther non-current financial assetsOther non-current non-financial assetsNon -cash assets pledged as collateralCurrentCurrentCurrent inventoriesCurrent provisionsTrade and other current receivablesTrade and other current payablesCurrent tax assets, currentCurrent tax Liabilities, currentCurrent biological assetsOther financial LiabilitiesOther current financial assetsOther non-financial LiabilitiesOther current non-financial assetsLiabilities in disposal groupsCash and cash equivalentsNon-cash assets pledged as collateralNon-current assets or disposal groups1A US GAAP XBRL balance sheet comprises 606 line items: #Copyright Robert Mládek May 7, 20227

IFRS US GAAP training manual including examplesMeasurementOceňováníArm’s length transaction / Transakce na délku paže (transakce za obvyklých podmínek)Unrelated parties / Nezávislé stranyActing voluntarily, willing / Jednající dobrovolně, jsou ochotníFully informed / Disponující s dostatkem informacíOrderly transaction between market participants / Řádné uzavřené transakce mezi účastníky trhuMarket participants / Účastníci trhuIndependent (not related parties) / Nezávislí (nejsou spřízněnými stranami)Knowledgeable (have a reasonable understanding & all available information)Informovaní (rozumně chápou situaci a disponují s veškerými dostupnými informacemi)Willing (are motivated but not forced or otherwise compelled)Ochotní (jsou motivováni, nikoli pod nátlakem nebo v tísni)Able (have the wherewithal to transact) / Schopní (disponují s dostatkem prostředků)Orderly transaction / Řádně uzavřená transakceNot forced (not a forced liquidation or distress sale)Nebyla nucena (není nucený likvidační prodej nebo nebyla uzavřená v tísni)Was exposed to the market (customary and usual marketing was undertaken)Transakce byla nabídnuta na trhu (uskutečnil se obvyklý a běžný marketing)Not orderly / Transakce nebyla řádně uzavřenáCustomary marketing activities (given current market conditions) were not undertaken.Obvyklý marketing (vzhledem k současným podmínkám na trhu) nebyl proveden.Marketing was performed, but asset or liability was marketed to a single market participant.Marketing proveden, ale majetek nebo závazek byl nabídnut pouze jednomu účastníkovi trhu.The seller was distressed (near bankruptcy or receivership).Prodávající byl v nouzi (připravoval se na něj konkurz nebo nucená správa).The seller was forced (compelled by law or regulation).Prodávající byl nucen (přinucen buď zákonem nebo regulací).The transaction price is an outlier compared with other recent prices.Cena, za kterou se transakce uzavřela, byla výrazně odlišná od podobných cen za poslední dobu.Copyright Robert Mládek May 7, 20228

IFRS US GAAP training manual including examplesDisclosureVykazováníDisclosure: published information / Zveřejňování: zveřejněná informaceReporting: the financial report1 (a complete set of financial statements2) / Výkaznictví: finanční zpráva (závěrka)The financial statements / Finanční výkazyStatement of Financial Position (SFP) Balance Sheet (B/S) / Výkaz finanční pozice (Rozvaha)Statement of Profit or Loss (P&L) and Other Comprehensive Income (OCI)3 Income Statement4 (I/S)Výkaz úplného výsledku hospodaření (Výsledovka)Statement of C

3 US GAAP aggregates gains and losses (events) and other revenue and expense (peripherals operations) as gains and losses. 4 IAS 1.99 An entity shall present an analysis of expenses recognised in profit or loss