Transcription

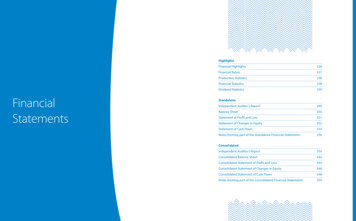

HighlightsFinancialStatementsFinancial Highlights236Financial Ratios237Production Statistics238Financial Statistics238Dividend Statistics239StandaloneIndependent Auditor’s Report240Balance Sheet250Statement of Profit and Loss251Statement of Changes in Equity252Statement of Cash Flows254Notes forming part of the Standalone Financial Statements256ConsolidatedIndependent Auditor’s Report334Consolidated Balance Sheet342Consolidated Statement of Profit and Loss344Consolidated Statement of Changes in Equity346Consolidated Statement of Cash Flows348Notes forming part of the Consolidated Financial Statements350

PerformanceSnapshotFINANCIAL HIGHLIGHTSAboutTata SteelLeadershipStrategyStakeholdersand cialStatementsFINANCIAL RATIOS( crore)Tata Steel StandaloneRevenue from operationsProfit/(loss) before taxProfit/(loss) after taxDividendsRetained earningsCapital employedNet worthBorrowingsNet debt to EquityNet worth per Share as at year endEarnings per Share:BasicDilutedDividend per Ordinary ShareEmployees (Numbers)Shareholders (Numbers)Tata Steel GroupTata Steel 8.30Ratio0.24 1Ratio0.98 EBITDA/TurnoverPBET/TurnoverReturn on average capital employedReturn on average net worthAsset turnoverInventory turnover (in days)Debtors turnover (in days)Gross block to net blockNet debt to equityCurrent ratioInterest service coverage ratioNet worth per share ( )Basic earnings per share ( )Dividend payoutP/E ratioEBITDA/Turnover (EBITDA: PBT /(-) Exceptional Items Net Finance Charges Depreciation and amortisation - Share of results ofequity accounted investments) (Net Finance Charges: Finance costs - Interest income Dividend income from current investments - Net gain/(loss) on sale of current investments)(Turnover: Revenue from Operations)2.PBET/TurnoverProfit before exceptional items and tax/Turnover3. Return on Average Capital Employed: EBIT/AverageCapital Employed (Capital Employed: Total Equity Non-current Borrowings Current maturities of Non-current borrowings andLease Obligations Current Borrowings Deferred taxliabilities) (EBIT: PBT /(-) Exceptional Items Net Finance Charges)4. Return on Average Net worth: PAT/Average Net worth (Net worth: Total equity)5. Asset Turnover: Turnover/(Total Assets - Investments Advance Against Equity)6. Inventory Turnover: Average Inventory/Sale of Productsin days236Integrated Report & Annual Accounts 2020-21 114th Year7.Debtors Turnover: Average Debtors/Turnover in days8.Gross Block to Net Block: Gross Block/Net BlockTata Steel 4 (Gross Block: Cost of property, plant and equipment Costof right-of-use assets Capital work-in-progress Cost ofintangible assets Intangible assets under development) (Net Block: Gross Block - Accumulated depreciation andamortisation - Accumulated impairment)9.Net Debt to Equity: Net Debt/Average Net Worth (Net debt: Non-current borrowings Current borrowings Current maturities of long-term borrowings and leaseobligations - Current investments - Cash and cashequivalents - Other balances with banks (including noncurrent earmarked balances))10. Current Ratio: Current Assets including assets held forsale (excluding current investments)/Current Liabilitiesincluding liabilities held for sale (Current liabilities: Trade Payables Short-term provisions Other current liabilities - Current maturities of Noncurrent borrowings and Lease Obligations)11. Interest Service Coverage Ratio: EBIT/Net Finance Charges(excluding interest on short-term debts)12. Net worth per share: Net Worth/Number of Equity Shares13. Basic Earnings per share: Profit attributable to OrdinaryShareholders/Weighted average number of OrdinaryShares14. Dividend Payout: Proposed dividend for the year/Profitafter tax15. P/E Ratio: Market Price per share/Basic Earnings per shareStandalone237

PerformanceSnapshotPRODUCTION STATISTICSAboutTata SteelLeadershipStakeholdersand nceFinancialStatementsDIVIDEND STATISTICS’000 6011,68312,48213,22813,15212,192Rolled/Forged nishedfor 1FINANCIAL STATISTICS( crore)YearCapital fitbeforeTaxTaxProfit Dividend#afterTaxYearFirst Preference( 150)Second Preference( 100)Total lakhOrdinary( 10)Rate Dividend lakhRate Dividend@ lakhTax ondividend �–860.801,496.58 ate* Dividend@ lakhTax ondividend lakh3.502.50 a3.00 b3.50 c4.50 9.911,03,740.4092,627.7492,471.6918,157.49 1,34,703.2212,872.6990,569.916,618.86 �––10.0010.00 �–aOn the Capital as increased by Rights Issue of Ordinary Shares during the financial year 1992-93.bOn the Capital as increased by Ordinary Shares issued during the financial year 1993-94 against Detachable Warrants.cOn the Capital as increased by Ordinary Shares issued during the financial year 1994-95 against Detachable Warrants and Foreign Currency Convertible Bonds.d On the Capital as increased by Ordinary Shares issued during the financial year 1995-96 against Detachable Warrants, Foreign Currency Convertible Bonds andNaked Warrants.eIncludes Dividend of 22.30 lakh on 9.25% Cumulative Redeemable Preference Shares for the period April 1, 2000 to June 27, 5,694.0610,533.191,370.78fIncludes Dividend of 1,198.40 lakh on 8.42% Cumulative Redeemable Preference Shares for the period June 1, 2000 to March 31, 2001.2019-203,421.1373,416.9941,422.87 20.126,610.98(132.82)6,743.801,787.38gDividend paid for 74 days.4,188.51 13,606.621,145.93hOn the Capital as increased by Rights Issue of Ordinary Shares during the financial year 2017-18.*Dividend proposed for the year@Includes tax on dividend.2020-211,977.56 89,293.33 28,348.30 1,03,702.76 79,243.59 57,470.73 65,506.89 43,724.443,987.32 17,795.13 Capital includes Equity share capital, Hybrid perpetual securities and Share application money pending allotment.*Expenditure includes excise duty recovered on sales, exceptional items and excludes depreciation.#paid during the year and includes tax on dividend.238Integrated Report & Annual Accounts 2020-21 114th 99,660.44Standalone239

PerformanceSnapshotINDEPENDENT AUDITOR’S REPORTOpinion1. We have audited the accompanying standalone financialstatements of Tata Steel Limited (“the Company”),which comprise the balance sheet as at March 31, 2021,and the statement of Profit and Loss (including OtherComprehensive Income), statement of changes in equityand statement of cash flows for the year then ended, andnotes to the standalone financial statements, includinga summary of significant accounting policies and otherexplanatory information (hereinafter referred to as “theStandalone Financial Statements”).2. In our opinion and to the best of our information andaccording to the explanations given to us, the aforesaidstandalone financial statements give the informationrequired by the Companies Act, 2013 (“the Act") in themanner so required and give a true and fair view inconformity with the accounting principles generallyaccepted in India, of the state of affairs of the Companyas at March 31, 2021, and total comprehensive income(comprising profit and other comprehensive income),changes in equity and its cash flows for the year thenended.Basis for Opinion3. We conducted our audit in accordance with the Standardson Auditing (SAs) specified under section 143(10) ofthe Act. Our responsibilities under those Standards arefurther described in the Auditor’s Responsibilities for the240Integrated Report & Annual Accounts 2020-21 114th YearLeadershipStrategyStakeholdersand cialStatementsKey audit matters5. Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of thestandalone financial statements of the current period. These matters were addressed in the context of our audit of thestandalone financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinionon these matters.To the Members of Tata Steel LimitedReport on the audit of the Standalone financial statementsAboutTata SteelAudit of the Standalone Financial Statements sectionof our report. We are independent of the Company inaccordance with the Code of Ethics issued by the Instituteof Chartered Accountants of India together with theethical requirements that are relevant to our audit of thestandalone financial statements under the provisions ofthe Act and the Rules thereunder, and we have fulfilledour other ethical responsibilities in accordance withthese requirements and the Code of Ethics. We believethat the audit evidence we have obtained is sufficient andappropriate to provide a basis for our opinion.Emphasis of Matter4. We draw your attention to Note 6(vi) to the standalonefinancial statements which states that the ability of theTata Steel Europe (TSE), the step-down subsidiary ofT Steel Holdings Pte Ltd (TSH), a subsidiary of the Company,to continue as a going concern is dependent on theavailability of future funding requirements, which couldhave a consequential impact on the carrying amountof investment of 20,854.89 crore (net of provision forimpairment amounting to 860.00 crore) in TSH as atMarch 31, 2021. Further, the auditors of TSE have, without modifyingtheir opinion, reported a Material Uncertainty Relatedto Going Concern vide their report dated May 4, 2021on the financial information of TSE for the year endedMarch 31, 2021. Our opinion is not modified in respect of this matter.Key audit matterHow our audit addressed the key audit matterAssessment of litigations and related disclosure ofcontingent liabilitiesOur audit procedures included the following:[Refer to Note 2 (c) to the Standalone financial statements–“Use of estimates and critical accounting judgements –Provisions and contingent liabilities”, Note 36 (A) to theStandalone Financial Statements – “Contingencies” and Note37 to the Standalone financial statements – “Other significantlitigations”].As at March 31, 2021, the Company has exposures towardslitigations relating to various matters as set out in theaforesaid Notes.Significant management judgement is required to assesssuch matters to determine the probability of occurrenceof material outflow of economic resources and whether aprovision should be recognised or a disclosure should bemade. The management judgement is also supported withlegal advice in certain cases as considered appropriate.As the ultimate outcome of the matters are uncertain andthe positions taken by the management are based on theapplication of their best judgement, related legal adviceincluding those relating to interpretation of laws/regulations,it is considered to be a Key Audit Matter. We understood, assessed and tested the design andoperating effectiveness of key controls surroundingassessment of litigations relating to the relevant laws andregulations; We discussed with management the recent developmentsand the status of the material litigations which werereviewed and noted by the Audit Committee; We performed our assessment on a test basis on theunderlying calculations supporting the contingentliabilities/other significant litigations disclosed in theStandalone Financial Statements; We used auditor’s experts/specialists to gain anunderstanding and to evaluate the disputed tax matters; We considered external legal opinions, where relevant,obtained by management; We evaluated management’s assessments byunderstanding precedents set in similar cases andassessed the reliability of the management’s pastestimates/judgements; We evaluated management’s assessment around thosematters that are not disclosed or not considered ascontingent liability, as the probability of material outflowis considered to be remote by the management; and We assessed the adequacy of the Company’s disclosures.Based on the above work performed, the assessment inrespect of litigations and related disclosures relating tocontingent liabilities/other significant litigations in theStandalone Financial Statements is considered to bereasonable.Standalone241

PerformanceSnapshotKey audit matterHow our audit addressed the key audit matterAssessment of carrying value of equity investmentsin subsidiaries, associates and joint ventures and fairvalue of other investments[Refer to Note 2 (c) to the Standalone Financial Statements –“Use of estimates and critical accounting judgements –Impairment and fair value measurements of financialinstruments”, Note 2 (m) to the Standalone FinancialStatements – “Investments in subsidiaries, associates andjoint ventures”, Note 2(n)(I) to the Standalone FinancialStatements – “Financial assets”, Note 6 to the StandaloneFinancial Statements – “Investments in subsidiaries, associatesand joint ventures”, Note 7 to the Standalone FinancialStatements – “Investments” and Note 39 (b) to the StandaloneFinancial Statements – “Fair value hierarchy”]Our audit procedures included the following:The Company has equity investments in various subsidiaries,associates, joint ventures and other companies. It also hasmade investments in preference shares in certain subsidiaries/associates and debentures in a joint venture.The Company accounts for equity investments in subsidiaries,associates and joint ventures at cost (subject to impairmentassessment) and other investments at fair value.For investments carried at cost amounting to 28,444.61crore where an indication of impairment exists, the carryingvalue of investment is assessed for impairment and whereapplicable an impairment provision is recognised.For investments carried at fair values, a fair valuation is doneat the year-end as required by Ind AS 109. In case of certaininvestments, cost is considered as an appropriate estimateof fair value since there is a wide range of possible fair valuemeasurements and cost represents the best estimate of fairvalue within that range as permitted under Ind AS 109.The accounting for investments is a Key Audit Matter asthe determination of recoverable value for impairmentassessment/fair valuation involves significant managementjudgement and estimates.The impairment assessment and fair valuation for suchinvestments have been carried out by the management inaccordance with Ind AS 36 and Ind AS 113 respectively. Thekey inputs and judgements involved in the impairment/ fairvaluation assessment of unquoted investments include: Forecast cash flows including assumptions on growthrates Discount rates Terminal growth rate Economic and entity specific factors incorporated in thevaluation.242Integrated Report & Annual Accounts 2020-21 114th Year We obtained an understanding from the management,assessed and tested the design and operating effectiveness ofthe Company’s key controls over the impairment assessmentand fair valuation of material investments. We evaluated the Company’s process regarding impairmentassessment and fair valuation by involving auditor’s valuationexperts to assist in assessing the appropriateness of thevaluation model including the independent assessmentof the underlying assumptions relating to discount rate,terminal value etc. We assessed the carrying value/fair value calculations ofall individually material investments, where applicable,to determine whether the valuations performed by theCompany were within an acceptable range determined byus and the auditor’s valuation experts. We evaluated the cash flow forecasts (with underlyingeconomic growth rate) by comparing them to the approvedbudgets and our understanding of the internal and externalfactors. We checked the mathematical accuracy of the impairmentmodel and agreed the relevant data with the latest budgets,actual past results and other supporting documents. We assessed the sensitivity analysis and evaluated whetherany reasonably foreseeable change in assumptions couldlead to impairment or material change in fair valuation. We discussed with the component auditors of certain entitiesto develop an understanding of the operating performanceand outlook used in their own valuation model and to assessconsistency with the assumptions used in the model. We had discussions with management to obtain anunderstanding of the relevant factors in respect of certaininvestments carried at fair value where a wide range of fairvalues were possible due to various factors such as absenceof recent observable transactions, restrictions on transfer ofshares, existence of multiple valuation techniques, investee’svaried nature of portfolio of investments for which significantestimates/judgements are required to arrive at fair value. We have discussed the key assumptions and sensitivities forcertain investments with those charged with governance. We evaluated the adequacy of the disclosures made in theStandalone Financial Statements.Based on the above procedures performed, we did not identifyany significant exceptions in the management’s assessmentin relation to the carrying value of equity investments insubsidiaries, associates and joint ventures and fair value of otherinvestments.AboutTata SteelLeadershipStrategyStakeholdersand MaterialityOther Information6. The Company’s Board of Directors is responsible for theother information. The other information comprises theinformation included in the Integrated Report, Board’sReport along with its Annexures and Financial Highlightsincluded in the Company’s Annual Report (titled as ‘TataSteel Integrated Report & Annual Accounts 2020-21’)but does not include the financial statements and ourauditor’s report thereon. Our opinion on the standalone financial statements doesnot cover the other information and we do not expressany form of assurance conclusion thereon. In connection with our audit of the standalone financialstatements, our responsibility is to read the otherinformation and, in doing so, consider whether the otherinformation is materially inconsistent with the standalonefinancial statements or our knowledge obtained in theaudit or otherwise appears to be materially misstated. If,based on the work we have performed, we conclude thatthere is a material misstatement of this other information,we are required to report that fact.We have nothing to report in this regard.Responsibilities of management and those charged withgovernance for the standalone financial statements7. The Company’s Board of Directors is responsible for thematters stated in section 134(5) of the Act with respect tothe preparation of these standalone financial statementsthat give a true and fair view of the financial position,financial performance, changes in equity and cash flowsof the Company in accordance with the accountingprinciples generally accepted in India, including theAccounting Standards specified under section 133 ofthe Act. This responsibility also includes maintenanceof adequate accounting records in accordance with theprovisions of the Act for safeguarding of the assets ofthe Company and for preventing and detecting fraudsand other irregularities; selection and application ofappropriate accounting policies; making judgmentsand estimates that are reasonable and prudent; anddesign, implementation and maintenance of adequateinternal financial controls, that were operating effectivelyfor ensuring the accuracy and completeness of theaccounting records, relevant to the preparation andpresentation of the standalone financial statementsthat give a true and fair view and are free from materialmisstatement, whether due to fraud or error.8. In preparing the standalone financial statements,management is responsible for assessing the Company’sability to continue as a going concern, disclosing, asapplicable, matters related to going concern and using thegoing concern basis of accounting unless managementeither intends to liquidate the Company or to atementsoperations, or has no realistic alternative but to do so. TheBoard of Directors are also responsible for overseeing theCompany’s financial reporting process.Auditor’s responsibilities for the audit of the standalonefinancial statements9. Our objectives are to obtain reasonable assurance aboutwhether the standalone financial statements as a wholeare free from material misstatement, whether due to fraudor error, and to issue an auditor’s report that includes ouropinion. Reasonable assurance is a high level of assurancebut is not a guarantee that an audit conducted in accordancewith SAs will always detect a material misstatement when itexists. Misstatements can arise from fraud or error and areconsidered material if, individually or in the aggregate, theycould reasonably be expected to influence the economicdecisions of users taken on the basis of these standalonefinancial statements.10. As part of an audit in accordance with SAs, we exerciseprofessional judgment and maintain professionalskepticism throughout the audit. We also: Identify and assess the risks of material misstatementof the standalone financial statements, whether dueto fraud or error, design and perform audit proceduresresponsive to those risks, and obtain audit evidencethat is sufficient and appropriate to provide a basisfor our opinion. The risk of not detecting a materialmisstatement resulting from fraud is higher than forone resulting from error, as fraud may involve collusion,forgery, intentional omissions, misrepresentations, orthe override of internal control. Obtain an understanding of internal control relevantto the audit in order to design audit proceduresthat are appropriate in the circumstances. UnderSection 143(3) (i) of the Act, we are also responsiblefor expressing our opinion on whether the companyhas adequate internal financial controls with referenceto standalone financial statements in place and theoperating effectiveness of such controls. Evaluate the appropriateness of accounting policiesused and the reasonableness of accounting estimatesand related disclosures made by management. Conclude on the appropriateness of management’s useof the going concern basis of accounting and, basedon the audit evidence obtained, whether a materialuncertainty exists related to events or conditionsthat may cast significant doubt on the Company’sability to continue as a going concern. If we concludethat a material uncertainty exists, we are required todraw attention in our auditor’s report to the relateddisclosures in the standalone financial statements or, ifsuch disclosures are inadequate, to modify our opinion.Standalone243

PerformanceSnapshotOur conclusions are based on the audit evidenceobtained up to the date of our auditor’s report. However,future events or conditions may cause the Company tocease to continue as a going concern. Evaluate the overall presentation, structure and contentof the standalone financial statements, including thedisclosures, and whether the standalone financialstatements represent the underlying transactions andevents in a manner that achieves fair presentation.11. We communicate with those charged with governanceregarding, among other matters, the planned scopeand timing of the audit and significant audit findings,including any significant deficiencies in internal controlthat we identify during our audit.12. We also provide those charged with governance witha statement that we have complied with relevantethical requirements regarding independence, and tocommunicate with them all relationships and othermatters that may reasonably be thought to bear on ourindependence, and where applicable, related safeguards.13. From the matters communicated with those chargedwith governance, we determine those matters thatwere of most significance in the audit of the standalonefinancial statements of the current period and aretherefore the key audit matters. We describe thesematters in our auditor’s report unless law or regulationprecludes public disclosure about the matter or when, inextremely rare circumstances, we determine that a mattershould not be communicated in our report because theadverse consequences of doing so would reasonably beexpected to outweigh the public interest benefits of suchcommunication.Report on other legal and regulatory requirements14. As required by the Companies (Auditor’s Report) Order,2016 (“the Order”), issued by the Central Government ofIndia in terms of sub-section (11) of section 143 of the Act,we give in the Annexure B a statement on the mattersspecified in paragraphs 3 and 4 of the Order, to the extentapplicable.15. As required by Section 143(3) of the Act, we report that:(a) We have sought and obtained all the information andexplanations, which to the best of our knowledge andbelief were necessary for the purposes of our audit.(b) In our opinion, proper books of account as requiredby law have been kept by the Company so far as itappears from our examination of those books.(c) The Balance Sheet, the Statement of Profit andLoss (including other comprehensive income), theStatement of Changes in Equity and Cash FlowStatement dealt with by this Report are in agreementwith the books of account.244Integrated Report & Annual Accounts 2020-21 114th Year(d) In our opinion, the aforesaid standalone financialstatements comply with the Accounting Standardsspecified under Section 133 of the Act.(e) On the basis of the written representations receivedfrom the directors taken on record by the Board ofDirectors, none of the directors is disqualified as onMarch 31, 2021 from being appointed as a directorin terms of Section 164 (2) of the Act.(f) With respect to the adequacy of the internal financialcontrols with reference to standalone financialstatements of the Company and the operatingeffectiveness of such controls, refer to our separateReport in “Annexure A”.(g) With respect to the other matters to be included inthe Auditor’s Report in accordance with Rule 11 ofthe Companies (Audit and Auditors) Rules, 2014, inour opinion and to the best of our information andaccording to the explanations given to us:i. The Company has disclosed the impact ofpending litigations as on Marc

Naked Warrants. e Includes Dividend of 22.30 lakh on 9.25% Cumulative Redeemable Preference Shares for the period April 1, 2000 to June 27, 2000. f Includes Dividend of 1,198.40 lakh on 8.42% Cumulative Redeemable Preference Shares for the period Jun