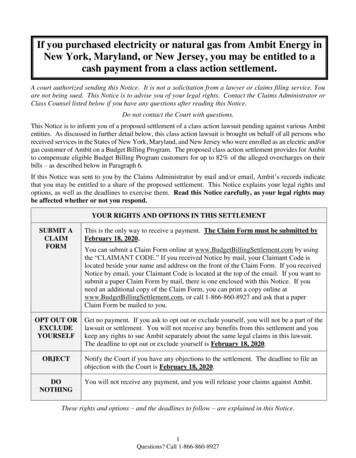

Transcription

Liquefied Natural Gas:Understanding the Basic Facts

Liquefied Natural Gas:Understanding the“I strongly support developingnew LNG capacity in theUnited States.”—President George W. BushPageAbout This ReportThis report was prepared by the U.S.Department of Energy (DOE) incollaboration with the NationalAssociation of Regulatory UtilityCommissioners (NARUC). DOE’s Office ofFossil Energy supports technologyresearch and policy options to ensureclean, reliable, and affordable suppliesof oil and natural gas for Americanconsumers, working closely with theNational Energy Technology Laboratory,which is the Department’s lead centerfor the research and development ofadvanced fossil energy technologies.NARUC, a nonprofit organizationcomposed of governmental agenciesengaged in the regulation oftelecommunications, energy, and waterutilities and carriers in the 50 states, theDistrict of Columbia, Puerto Rico, andthe Virgin Islands, serves the publicinterest by improving the quality andeffectiveness of utility regulation.Design and editorial support: AkoyaSelect photos courtesy of: Anadarko PetroleumCompany; Atlantic LNG Company of Trinidad andTobago; British Petroleum; Chevron Texaco;ConocoPhillips; Dominion Cove Point LNG, LP;Excelerate Energy; HOEGH LNG; Pine Needle LNG, LLCNC; Texaco Production Operations; Tractebel LNGNorth America; Trunkline LNG24Growing Demandfor Natural GasEmergence of theGlobal LNG MarketNatural gas plays a vital role inthe U.S. energy supply and inachieving the nation’s economicand environmental goals.One of several proposedsupply options would involveincreasing imports of liquefiednatural gas (LNG) to ensurethat American consumers haveadequate supplies of naturalgas in the future.Although natural gas productionin North America is projectedto gradually increase through2025, consumption has begunto outpace available domesticnatural gas supply. Over time,this gap will widen.Liquefaction enables naturalgas that would otherwise be“stranded” to reach majormarkets. Developing countrieswith plentiful natural gasresources are particularlyinterested in monetizingnatural gas by exporting it asLNG. Conversely, moredeveloped nations with littleor no domestic natural gasrely on imports.

Basic Facts68Current Status of U.S.LNG ImportsComponents of theLNG Value ChainThe United States currentlyhas six LNG terminals—fouron the mainland, one in theoffshore Gulf of Mexico, andone in Puerto Rico—thatreceive, store, and regasify LNG.Some economists call for thedevelopment of more importcapacity to enable the UnitedStates to participate fully inworld LNG markets.If the United States is toincrease LNG imports,significant capital investmentwill be necessary by energyfirms across the entire LNG“value chain,” which spansnatural gas production,liquefaction capacity, transportshipping, storage, andregasification.Expanded LNG imports wouldlikely help to dampen naturalgas price volatility in the UnitedStates, particularly during peakperiods of demand. Suchexpanded imports would alsosupport U.S. economic growth.Over the past two decades,technology improvementshave been key to a substantialincrease in liquefactionefficiency and decrease inLNG costs.16Informed Decision MakingFor more than 40 years, thesafety record of the global LNGindustry has been excellent,due to attention to detail inengineering, construction,and operations. More than30 companies have recentlyproposed new LNG terminalsin North America, along theU.S. coastline or offshore. Eachproposal is rigorously evaluatedbefore an LNG terminal can beconstructed or expanded.Americans face the challengeof making sound and timelydecisions about LNGinfrastructure to assure anabundant supply of natural gasfor homes, businesses, industry,and power generators, in thenear and long term.

Growing Demand forNatural GasThe United States relies on clean-burning natural gasfor almost one quarter of all energy used. Natural gashas proven to be a reliable and efficient energy sourcethat burns much cleaner than other fossil fuels. In thelast 10 years, the United States produced between 85and 90 percent of the natural gas it consumed.1 Mostof the balance was imported by pipeline from Canada. The residential sector benefits from the higher fuelefficiency and lower emissions of gas appliances.One way to help meet rising demand would be toincrease imports of natural gas from outside NorthAmerica. Net imports of natural gas are projected tosupply 19 percent of total U.S. consumption in 2010(4.9 Tcf) and 28 percent in 2025 (8.7 Tcf).3 Thisnatural gas will be transported via ship in the form ofliquefied natural gas (LNG). Net imports of LNG areexpected to increase from 0.6 Tcf in 20044 to morethan 6 Tcf in 2025—at that point satisfying almost21 percent of total U.S. natural gas demand.5 The industrial sector relies on natural gas as afeedstock or fuel for manufacturing many of theproducts we rely on today, including pulp andpaper, metals (for computers, automobiles, andtelecommunications), chemicals, fertilizers, fabrics,pharmaceuticals, and plastics.Discussions of the benefits and risks of expanding LNGimports will be central to U.S. energy supply decisionsin the years ahead. A key consideration is the potentialof LNG imports to ensure that adequate and reliablesupplies of natural gas are available to support U.S.economic growth. The transportation sector is beginning to seenatural gas as a clean and readily availablealternative to other fossil fuels.Numerous recent studies have underscored theimportance of LNG in the nation’s energy future:Annual U.S. natural gas consumption is projectedto rise from 22.1 trillion cubic feet (Tcf) in 2004 to30.7 Tcf in 2025.2 Reasons for the increase include: Utilities realize advantages by using natural gasfired generators to create electricity (lower capitalcosts, higher fuel efficiency, shorter constructionlead times, and lower emissions).FIGURE 1Natural gas accounted for almost one-quarter of all energy usedin the United States from 1998-2003.Source: Energy Information Administration, Annual Energy Outlook 20052While U.S. demand is rising, production of natural gasin major mature provinces, including North America, isbeginning to decline. Lack of a steady supply increasesthe potential for higher energy prices and price volatility,which affect the profitability and productivity of industryand may spur certain gas-intensive industries to relocateto parts of the world where natural gas is less expensive.This, in turn, could impact jobs, energy bills, and theprices paid for consumer goods. A 2003 study by the National Petroleum Councilconducted at the request of the Secretary of Energyfound several keys to ensuring a reliable, reasonablypriced natural gas supply to meet future U.S.demand—including increased imports of LNG.6 A 2004 Energy Information Administration (EIA)study, Analysis of Restricted Natural Gas SupplyCases, included a forecast scenario based on a“restricted” expansion of U.S. LNG importterminals. The results showed an increasein natural gas prices, dampening consumption andeconomic growth. A 2004 study by the Manufacturers Allianceoutlined the critical role of natural gas inmanufacturing and the potential contribution ofLNG to improve U.S. industrial competitivenessin the global marketplace.7

Meeting Future DemandThe United States will not be the only nationcompeting for natural gas imports in the future. In2001 the worldwide community consumed about 90trillion cubic feet (Tcf) of natural gas. Consumption ofnatural gas worldwide is projected to increase by anaverage of 2.2 percent annually or 70 percent overallfrom 2001 to 2025, to about 151 trillion cubic feet.8Fortunately, global natural gas resources are vast—estimated at about 6,079 Tcf in recoverable gas as of2004, roughly 60 times the recent annual volumeconsumed.9 In total, worldwide natural gas resourcesare estimated at more than 15,000 Tcf, including gasthat has yet to be discovered.10The international LNG business connects natural gasthat is “stranded”—far from any market—with thepeople, factories, and power plants that require theenergy. It becomes necessary to transport natural gas asLNG because the distribution of the world’s supply ofnatural gas is not consistent with patterns of demand.Russia, Iran, and Qatar hold 58.4 percent of the world’snatural gas reserves, yet consume only about 19.4percent of worldwide natural gas. Such countries tendto “monetize” their gas resource—converting it into asalable product. LNG makes this possible.FIGURE 2LNG is mostly methane plus a few percent ethane, even lesspropane and butane, and trace amounts of nitrogen.FIGURE 3When natural gas is liquefied, it shrinks more than 600 timesin volume.The world’s major LNG-exporting countries hold about25 percent of total natural gas reserves. Two countrieswith significant reserves (Russia and Norway) arecurrently building their first liquefaction facilities. Atleast seven more are considering the investment tobecome LNG exporters in the near future.In some cases, conversion to LNG makes use ofnatural gas that would once have been lost. Forexample, Nigeria depends on its petroleum exports asa primary source of revenue. In the process of oilproduction, natural gas was flared—a wastefulpractice that adds carbon dioxide to the atmosphere.Converting this natural gas to LNG provides botheconomic and environmental benefits.1 Energy Information Administration (EIA), Annual Energy Review 2003, September 2004.2 EIA, Annual Energy Outlook 2005.3 EIA, Annual Energy Outlook 2005.4 DOE, Natural Gas Imports and Exports, Fourth Quarter 2004.5 EIA, Annual Energy Outlook 2005.6 National Petroleum Council, Balancing Natural Gas Policy–Fueling the Demands of a GrowingEconomy, September 2003.7 Norman, Donald A., Liquefied Natural Gas and the Future of Manufacturing, ManufacturersAlliance, September 2004.8 EIA, International Energy Outlook 2004.9 EIA, International Energy Annual 2003, released May 2005.10 U.S. Geological Survey, World Petroleum Assessment 2000.LNG.A SAFE FUEL IN A SMALL PACKAGENatural gas consists almost entirely of methane (CH4), the simplest hydrocarboncompound. Typically, LNG is 85 to 95-plus percent methane, along with a fewpercent ethane, even less propane and butane, and trace amounts of nitrogen(Figure 2). The exact composition of natural gas (and the LNG formed from it)varies according to its source and processing history. And, like methane, LNG isodorless, colorless, noncorrosive, and nontoxic.Natural gas is condensed to a liquid by cooling it to about -260 F (-162 C). Thisprocess reduces its volume by a factor of more than 600—similar to reducing thenatural gas filling a beach ball into liquid filling a ping-pong ball (Figure 3). Asa result, just one shipload of LNG can provide nearly 5 percent (roughly 3 billioncubic feet) of the U.S. average daily demand for natural gas, or enough energy toheat more than 43,000 homes for an entire year!11LNG is transported by ship to terminals in the United States, then stored atatmospheric pressure in super-insulated tanks. From storage, LNG is convertedback into gas and fed into the natural gas pipeline system. LNG is alsotransported by truck to satellite storage sites for use during peak periods ofnatural gas demand—in the coldest weather for heating and in hot weather forfueling electric power generators, which in turn run air conditioners.When liquefied, natural gasthat would fill a beach ball.becomes LNG that can fitinside a ping-pong ball.11 See LNG conversion tables, page 9.3

Emergence of theGlobal LNG MarketEfforts to liquefy natural gas for storage began in theearly 1900s, but it wasn’t until 1959 that the world’sfirst LNG ship carried cargoes from Louisiana to theUnited Kingdom, proving the feasibility of transoceanic LNG transport. Five years later, the UnitedKingdom began importing Algerian LNG, makingthe Algerian state-owned oil and gas company,Sonatrach, the world’s first major LNG exporter. TheUnited Kingdom continued to import LNG until1990, when British North Sea gas became a lessexpensive alternative.Japan first imported LNG from Alaska in 1969 andmoved to the forefront of the international LNG tradein the 1970s and 1980s with a heavy expansion ofLNG imports. These imports into Japan helped tofuel natural-gas-fired power generation to reducepollution and relieved pressure from the oil embargoof 1973. Japan currently imports more than 95percent of its natural gas and, as shown in Figure 4,serves as the destination for about half the LNGexported worldwide.FIGURE 4Japan has been the major client of the LNG business for 30 years, but thesize of the market and the number of importers are growing steadily.The United States first imported LNG from Algeriaduring the 1970s, before regulatory reform and risingprices led to rapid growth of the domestic natural gassupply. The resulting supply-demand imbalance(known as the “gas bubble” of the early 1980s) led toreduced LNG imports during the late 1980s andeventually to the mothballing of two LNG importfacilities. Then, in the 1990s, natural gas demand grewrapidly, and the prospect of supply shortfalls led to adramatic increase in U.S. LNG deliveries. In 1999 aliquefaction plant became operational in Trinidad andTobago, supplying LNG primarily to the United States.Current LNG Market StructureInternational trade in LNG centers on two geographicregions (see Figure 5):12 The Atlantic Basin, involving trade in Europe,northern and western Africa, and the U.S. Easternand Gulf coasts. The Asia/Pacific Basin, involving trade in SouthAsia, India, Russia, and Alaska.In addition, Middle Eastern LNG-exporting countriesbetween these regions supply Asian customersprimarily, although some cargoes are shipped toEurope and the United States.LNG prices are generally higher in the Asia/PacificBasin than in the Atlantic Basin. However, in theUnited States the price of LNG can rise with peakseasonal demand to attract short-term delivery ofLNG cargoes.LNG importers. Worldwide in 2003 a total of 13countries imported LNG. Three countries in theAsia/Pacific Basin—Japan, South Korea, andTaiwan—accounted for 67 percent of global LNGimports, while Atlantic Basin LNG importers tookdelivery of the remaining 33 percent.13Source: Cedigaz (1970-1992); EIA (1993-2003)4Japan remains the world’s largest LNG consumer,although its share of global LNG trade has fallenslightly over the past decade as the global market hasgrown. Japan’s largest LNG suppliers are Indonesiaand Malaysia, with substantial volumes also importedfrom Qatar, the United Arab Emirates, Australia,Oman, and Brunei Darussalam. Early in 2004 Indiareceived its first shipment of LNG from Qatar at thenewly completed facility at Dahej in Gujarat.

FIGURE 5LNG trading can be categorized by thegeographic region in which it takes place: theAtlantic Basin or the Asia/Pacific Basin.Source: Energy Information Administration andBritish PetroleumImports by Atlantic Basin countries are expected togrow as many expand storage and regasificationterminal capacity. France, Europe’s largest LNGimporter, plans two new terminals for receipt of gasfrom Qatar and Egypt. Spain’s LNG imports, roughlyhalf from Algeria, increased by 21 percent in 2003. AllSpanish regasification terminals are being expanded,with several new terminals starting up by 2007. Italyand Turkey receive LNG from Nigeria and Algeria.Belgium has one regasification terminal and receivesmost of its LNG from Algeria. In 2003 the DominicanRepublic and Portugal began operating regasificationterminals. Other potential Atlantic Basin LNGimporters include the Bahamas, Canada, Jamaica,Mexico, the Netherlands, and the United Kingdom.LNG exporters. Asia/Pacific Basin LNG producersaccounted for nearly half of total world LNG exportsin 2003 while Atlantic Basin LNG producersaccounted for about 32 percent. Liquefaction capacityin both regions is increasing steadily.14Indonesia is the world’s largest LNG producer andexporter, accounting for about 21 percent of theworld’s total LNG exports. The majority of Indonesia’sLNG is imported by Japan, with smaller volumesgoing to Taiwan and South Korea. Malaysia, theworld’s third-largest LNG exporter, ships primarily toJapan with smaller volumes to Taiwan and SouthKorea. Australia exports LNG from the NorthwestShelf, primarily to supply Japanese utilities. About 90percent of Brunei Darussalam output goes to Japanesecustomers. The only liquefaction facility in the UnitedStates was constructed in Kenai, Alaska, in 1969. Thisfacility, owned by ConocoPhillips and Marathon Oil,has exported LNG to Japan for more than 30 years.Russia is becoming the newest Asia/Pacific Basinexporter. Its first LNG plant is under construction onSakhalin Island off the country’s east coast. This largefacility is scheduled to begin operation in 2008.Planned expansions of existing plants coulddramatically increase Atlantic Basin liquefactioncapacity by 2007. Algeria, the world’s second-largestLNG exporter, serves mainly Europe (France,Belgium, Spain, and Turkey) and the United States viaSonatrach’s four liquefaction complexes. Nigeria exportsmainly to Turkey, Italy, France, Portugal, and Spain butalso has delivered cargos under short-term contracts tothe United States. Trinidad and Tobago exports LNGto the United States, Puerto Rico, Spain, and theDominican Republic. An Egyptian facility exported itsfirst cargo in 2005 and is expected to supply France,Italy, and the United States. Beginning in 2006 Norwayplans to export LNG from Melkøye Island to marketsin Spain, France, and the United States.12 EIA, The Global Liquefied Natural Gas Market: Status and Outlook, December 2003, andother sources.13 EIA, World LNG Imports by Origin, 2003.14 EIA, World LNG Imports by Origin, 2003.5

Current Status of U.S.LNG ImportsIn 2003 the United States imported 506.5 Bcf of LNGfrom a variety of exporting countries. Imports in 2004increased by 29 percent, reaching 652 Bcf.LNG arriving in the continental United States entersthrough one of five LNG receiving and regasificationterminals located along the Atlantic and Gulf coasts.While these facilities have a combined peak capacity ofmore than 1.3 Tcf per year, imports in 2004 totaled onlya little more than 0.65 Tcf.* However, future demandfor LNG will outgrow current and future capacity at thefive terminals. By 2008 these terminals should reach apeak capacity of 2.1 Tcf and then level off. On the otherhand, EIA projects LNG demand of 6.4 Tcf to meetU.S. natural gas needs by 2025. Clearly, the nation willneed to rely on additional import terminals or face aserious natural gas shortfall in coming decades. LNGreceiving terminals are located in:operations in March 2005 as the world’s first offshorereceiving port. The facility has a baseload capacity of183 Bcf per year and uses converted LNG carriers toregasify LNG through deck-mounted vaporizers.A sixth terminal, the EcoEléctrica regasificationfacility (capacity of 33.9 Bcf per year) in the U.S.Commonwealth of Puerto Rico, began importingLNG in 2000 to serve a 540-megawatt natural gas-firedpower plant that accounts for about 20 percent of theelectricity generated on the island.15 Capacities from EIA (LNG Markets and Uses: June 2004 Update), FERC, facility websites,and other sources.FIGURE 6Most U.S. LNG imports come from Trinidad and Tobago. The balance originatesfrom a mix of Middle Eastern, African, and Asian suppliers.Everett, Massachusetts. Owned and operated byTractebel LNG North America, the facility beganoperations in 1971 and now meets 15 to 20 percent ofNew England’s annual gas demand. A recent expansionraised baseload capacity to 265 Bcf per year.**Cove Point, Maryland. Operated by Dominion CovePoint LNG, the Cove Point terminal began operationin 1978, was mothballed for two decades, andreopened in July 2003. A proposed expansion projectwill increase baseload capacity from the current365 Bcf per year to about 657 Bc

before an LNG terminal can be constructed or expanded. Americans face the challenge of making sound and timely decisions about LNG infrastructure to assure an abundant supply of natural gas for homes, businesses, industry, and power g