Transcription

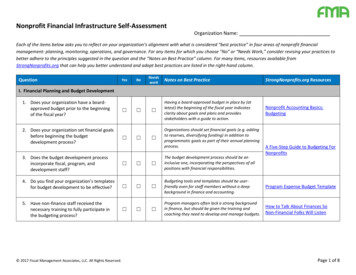

Nonprofit Financial Infrastructure Self-AssessmentOrganization Name:Each of the items below asks you to reflect on your organization’s alignment with what is considered “best practice” in four areas of nonprofit financialmanagement: planning, monitoring, operations, and governance. For any items for which you choose “No” or “Needs Work,” consider revising your practices tobetter adhere to the principles suggested in the question and the “Notes on Best Practice” column. For many items, resources available fromStrongNonprofits.org that can help you better understand and adopt best practices are listed in the right-hand column.QuestionYesNoNeedsworkNotes on Best PracticeStrongNonprofits.org Resources Having a board-approved budget in place by (atlatest) the beginning of the fiscal year indicatesclarity about goals and plans and providesstakeholders with a guide to action.Nonprofit Accounting Basics:Budgeting Organizations should set financial goals (e.g. addingto reserves, diversifying funding) in addition toprogrammatic goals as part of their annual planningprocess.I. Financial Planning and Budget Development1. Does your organization have a boardapproved budget prior to the beginningof the fiscal year? 2. Does your organization set financial goalsbefore beginning the budgetdevelopment process? 3. Does the budget development processincorporate fiscal, program, anddevelopment staff? The budget development process should be aninclusive one, incorporating the perspectives of allpositions with financial responsibilities.4. Do you find your organization’s templatesfor budget development to be effective? Budgeting tools and templates should be userfriendly even for staff members without a deepbackground in finance and accounting.Program Expense Budget Template Program managers often lack a strong backgroundin finance, but should be given the training andcoaching they need to develop and manage budgets.How to Talk About Finances SoNon-Financial Folks Will Listen5. Have non-finance staff received thenecessary training to fully participate inthe budgeting process? 2017 Fiscal Management Associates, LLC. All Rights Reserved. A Five-Step Guide to Budgeting ForNonprofitsPage 1 of 8

Question6. Does the budget development processinclude the budgeting of revenues andexpenses by program / function?Yes No Needswork8. Does the budget process includedevelopment of a strategy for fundingoverhead (administrative) costs?9. Do you feel you have a goodunderstanding of the full costs of each ofyour organization’s programs andservices?10. Does the annual operating budget includedepreciation expenses?11. Is a methodology in place to budgetrevenue based on probability of receipt? 2017 Fiscal Management Associates, LLC. All Rights Reserved. StrongNonprofits.org Resources Organizational budgets should be constructed byprogram / function, giving insight into what itactually costs to conduct each of the organization’sactivities. Certain expenses (often including rent, utilities,office supplies, etc.) are typically shared amongmany or all of the organization’s programs andfunctions; in order to understand the full costs ofactivities the organization should adopt anappropriate basis (such as headcount/FTE or squarefootage) for spreading those costs among relevantareas. Organizations often find it challenging to securefunding for administrative costs; strategies forcovering such costs may include recovering indirectcosts on grants and contracts, raising unrestrictedfunds, and developing earned income streams.The Nonprofit Starvation Cycle Organizational budgets should be constructed byprogram / function, giving insight into what itactually costs to conduct each of the organization’sactivities.Nonprofit Cost Analysis Toolkit: SixSteps to Finding the True Costs ofPrograms Including depreciation expenses in the operatingbudget can help organizations ensure that they aresetting aside resources for future capital needs andavoid surprises when financial results are presented.Fixed Asset and DepreciationSchedule Revenue tends to be the area of greatest uncertaintyin nonprofit financial planning; estimating receiptprobabilities can help organizations identify andplan for best- and worst-case scenarios.Revenue Scenario Planning Tool7. Does your organization have amethodology for allocating shared costsacross programs and functions? Notes on Best PracticeProgram-Based Budget BuilderPage 2 of 8

QuestionYes12. Does your organization project itsexpected future cash receipts anddisbursements?13. Does your organization forecast year-endresults at particular points throughoutthe year?14. Does your organization have a process forevaluating funding opportunities prior toapplying? No NeedsworkNotes on Best PracticeStrongNonprofits.org Resources Cash flow projections are a critical managementtool; program and development staff should beinvolved on a regular basis in projecting the timingof cash receipts and payments.Cash Flow Projections Template Knowing where your organization is likely to finishthe year financially can allow decision-makers tomore proactively manage toward intended financialresults.Year-End Forecast Template Nonprofits often find themselves in challengingcircumstances as a result of taking on new fundingwithout fully considering whether the fundingopportunity is a good fit strategically,programmatically and financially.Funding Opportunity AssessmentToolII. Financial Reporting and MonitoringFinancial reporting should generally be done on amonthly basis for management and at leastquarterly for the board of directors.15. Does the organization produce anddistribute the following reports to theboard and senior management on aquarterly or monthly basis?a. Balance Sheet b. Organization-wide budget-toactual revenue and expense c. Program-level budget-to-actualrevenue and expense d. Narrative highlighting keyfinancial results and questions 2017 Fiscal Management Associates, LLC. All Rights Reserved.Nonprofit Accounting Basics:Internal Reporting for GoodManagementPage 3 of 8

Question16. Do department/program managersreceive monthly budget-to-actual reportsfor their areas of responsibility?17. Are the reports understandable toprogram managers who are notaccountants?18. Are members of the finance staff ableand available to answer the financerelated questions of other staff?19. Does your organization use “dashboards”to highlight performance on keyindicators?20. Does your organization forecast year-endfinancial results at particular pointsduring the year?21. Are there regular financial decisionmaking meetings among key staff at yourorganization? 2017 Fiscal Management Associates, LLC. All Rights Reserved.Yes No NeedsworkNotes on Best PracticeStrongNonprofits.org Resources As the people closest to the day-to-day decisionmaking about program delivery (and thereforespending), program managers should haveresponsibility for understanding and managing theirprograms’ finances. Program managers often lack a strong backgroundin finance but should be given the training andcoaching they need to develop and manage budgets. An organization’s finance team should have a“customer service” orientation with respect toprogram and other staff members who may needsupport in carrying out their financialresponsibilities. Dashboards are visual representations of a selectedset of key performance indicators (KPIs), and providedecision-makers with a quick summary of theorganization’s current status in relation toestablished goals (not limited to finance).A Nonprofit Dashboard and SignalLight for Boards Forecasting allows an organization’s leaders tounderstand where it is likely to end the year from afinancial perspective and indicates areas of action toensure that results ultimately align withorganizational goals.Year-End Forecast Template Organizations should establish a forum for teamdiscussion and decision making concerningsignificant financial issues.How to Talk About Finances SoNon-Financial Folks Will ListenPage 4 of 8

III. Financial Operations22. Does your organization’s front-lineaccounting staff have a solidunderstanding of nonprofit bookkeepingand accounting concepts and practices? 23. Do all finance staff members have clearand up-to-date job descriptions? 24. Are all staff members (not limited tofinance staff) aware of and trained in theorganization’s relevant fiscal policies andprocedures?25. Is your organization’s accountingsoftware capable of and configured toproduce appropriate financial reports?26. Does your finance office maintain anannual calendar of key activities andresponsibilities?27. Does your organization have a monthlyfinancial closing process with clearlydefined roles, responsibilities, anddeadlines? 2017 Fiscal Management Associates, LLC. All Rights Reserved. Some nonprofit accounting principles areconsiderably different from those in the for-profitsector; many academic accounting programs givelittle emphasis to nonprofit practice.Nonprofit Accounting Basics:Accounting 101 Finance office job descriptions provide clarity aboutthe roles and responsibilities of individual teammembers.Chief Financial Officer and FinanceJob Descriptions Fiscal policies and procedures should be understoodand followed organization-wide; for instance,program staff members should be familiar with theorganization’s policies and procedures concerningpurchasing, expense reimbursements, etc.Nonprofit Fiscal Policies andProcedures: A Template and Guide Nonprofit accounting systems should be configuredto report financial results for the organization as awhole as well as by program, funding source, andother relevant categories.Unified Chart of Accounts A nonprofit’s finance team has an ongoing list ofcritical responsibilities related to activities such asthe budget development process, annual audits,financial reporting, etc., which should be proactivelymanaged.Fiscal Management ActivitiesCalendar A financial close ensures that all relevant data isincluded in financial reports and that past datacannot be revised without appropriate authorizationand an audit trail.Checklist for Monthly ClosingProcessPage 5 of 8

28. Is there a process in place to reconciledonation records between the financeand development/fundraisingdepartments?29. Are fiscal workflow processes at yourorganization designed to minimizeduplicative work, manual data entry, andreliance on paper? Finance and fundraising records should be comparedand reconciled on at least a quarterly basis to ensureconsistency of reporting; systems integrationbetween accounting and fundraising databases cansignificantly improve efficiencies in this process.Using technology to automate processes whereverpossible can increase both the efficiency and thereliability of operations.Finance and Development OfficeRelationship Self AssessmentFinancial Integrity Requires Morethan Good AccountantsIV. Governance over Financial Matters30. Do the members of your organization’sboard of directors understand theirfiduciary roles and responsibilities?31. Do members of the board understand theorganization’s long-term financial trendsand key fiscal health metrics?32. Do members of the board understand thebasics of nonprofit accounting andfinancial reporting?33. Does the board have one or moremembers with professional-level financialexpertise? 2017 Fiscal Management Associates, LLC. All Rights Reserved. Board members are collectively responsible forseeing that a nonprofit organization operates inalignment with its mission, vision, and values and isin compliance with applicable laws and regulations.The Board’s Financial Leadership Ensuring financial sustainability is a key governanceresponsibility; understanding an organization’shistorical trends and current metrics helps to ensurethat decisions are made with sustainability in mind.Financial Health Analysis Nonprofit accounting and financial reporting aredifferent in important respects from that of the forprofit sector; board members whose experience andbackground is in the private sector may neededucation about the nuances of nonprofit finance.VIDEO: Understanding AuditedFinancial Statements It is advisable for at least some board members tohave a professional financial background (e.g.accountant, banker, business leader), particularlythose in the roles of treasurer and financecommittee chair.Board Job DescriptionsPage 6 of 8

34. Does the board finance committeeparticipate in the budget developmentprocess?35. Does the board receive and reviewfinancial reports regularly (i.e. on amonthly or quarterly basis)?36. Does the organization have a boardapproved manual on fiscal policies andprocedures outlining appropriatefinancial controls? The finance committee should review and offer inputinto the budget as it is being developed and shouldsign off before submission to the full board.Make Good Use of the Treasurerand Finance Committee Board members should review financial reports priorto each board meeting (at least quarterly) andshould understand the financial position and resultsof the organization, including any areas of concern.Helping Boards be ResponsibleFiscal Stewards The board (and specifically the audit committee orfinance committee) is the steward of theorganization’s internal controls and as such shouldadopt policies and procedures that ensure thesafeguarding of organizational assets.Nonprofit Fiscal Policies andProcedures: A Template and Guide Reserves are unrestricted net assets available forfinancing operations, investing in new opportunities,and guarding against financial challenges. Boardsshould encourage the development of reserves andset policies regarding their use and management.Nonprofit Operating Reserve PolicyToolkit Risk management is a key responsibility of theboard, which should identify and work to mitigatevarious types of risk (including financial, legal,operational, and reputational).What’s the Board Got to Do WithIt? T

Nonprofit Accounting Basics: Budgeting 2. Does your organization set financial goals before beginning the budget development process? Organizations should set financial goals (e.g. adding to reserves, diversifying funding) in addition to programmatic goals as part of their annual planning process. A Five-Step Guide to Budgeting For Nonprofits 3. Does the budget development process incorporate .