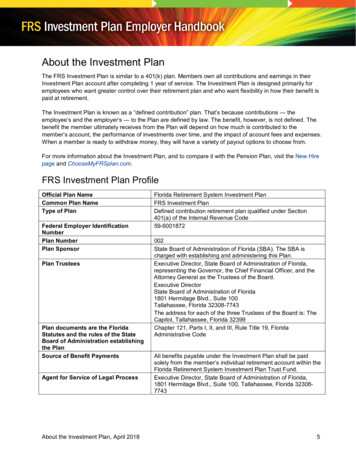

Transcription

Global infrastructureinvestmentThe role of private capital in the deliveryof essential assets and services

ForewordAt the core of GIIA’s agenda is theneed for an evidence basedaccount of the contribution privatecapital can play in assistinggovernments around the world todeliver high quality essential assetsand services to the communitiesthey serve.There is now a wealth of evidencefrom bodies such as the WorldEconomic Forum on the‘infrastructure gap’ that exists inboth the developed and developingworld. Likewise, it is widelyrecognised that high qualityinfrastructure serves societies interms of contributing to economicgrowth, local jobs and strong andvibrant communities.Private investors, workingalongside governments, can play aprofound and positive role in thedelivery of world classinfrastructure. This report,produced in partnership with PwC,provides examples of the impactthat has been made globally. Thefunds, which often representindividuals investing in theirpensions for their retirement, arelooking for long-term stable returns.Professional investors who are thecustodians of these funds take along-term view by investing in theassets they own, oftentranscending political andeconomic cycles, to improve theperformance of the businesses andservices they own.There are wide ranging views of therole of private capital forinfrastructure assets. We believethat the case studies in thisdocument demonstrate the positiveoutcomes that can be achievedwhere the public sector, regulatorsand investors collaborate to createfair, transparent and openframeworks that both attractinvestment and represent theinterests of the consumers thatultimately pay for the servicesprovided.We welcome an open dialogue onthe future of infrastructureinvestment and the positivecontribution private capital canplay in helping societies achievetheir ambitions.If you wold like to find out moreabout GIIA and its advocacy role,please visit www.giia.net.I am grateful to PwC and GIIAmembers for their contribution tothis report.Andy RoseCEO, GIIAPrivate investors,working alongsidegovernments, canplay a profound andpositive role in thedelivery of worldclass infrastructure2Global Infrastructure Investment

PwC and GIIA3

Contents4Executive summary5The need for private investment into global infrastructure – and its impacts8A snapshot of global infrastructure investment16Case studies: Chilean water privitisation Australian airport privatisation Peel Ports and Global Container Terminals UK water privatisation Azure Power1824303642Find out more45Global Infrastructure Investment

ExecutivesummaryA global transformation ininfrastructure ownershipThe last decade has seen atransformation in the ownership of theworld’s economic infrastructure – withmuch now resting in the hands ofspecialist private investors who haveinherited it through acquisitions fromgovernments, major corporates andtake-private transactions.This transformation has been driven byan influx of capital seeking long-term,stable returns. More than US 200bnhas been raised by specialist fundssince 20061, with at least the sameagain allocated by pension funds andother direct investors.Combined with a strong supply ofassets, enhanced by the post-crisisneed for governments and majorcorporates to reduce debt and focusexpenditure, the impact has beenpronounced, with US 1.7 trillion beinginvested into infrastructure assetsglobally since 20102. In the UK alone,some 56% of water assets, all of theUK’s major airports, most ports and allpassenger rail rolling stock now sitwithin specialist infrastructure investorvehicles3.Understandably, questions have beenraised around the financial andperformance impacts this has had oninfrastructure spending andperformance, on the provenance andextraction of funds, and on the securityof essential services within privateinvestors’ hands.1InfraDeals fundraising analysis Jan 2006 to Sep 20162InfraDeals analysis of global transaction activity from Jan 2010 to Sep 20163PwC, The role and impact of specialist investors in UK infrastructure, 2015PwC and GIIA5

This report, commissioned by the Global InfrastructureInvestor Association and prepared jointly with PwC, drawsfrom a global evidence base and presents a series ofillustrative case studies. Whilst not a definitive researchstudy itself, there are notably consistent themes comingout of the analysis:1. A specificinvestment approachgeared towards longterm essential assets2. A desire to drivesignificantperformanceimprovementsThe infrastructure investorcommunity brings a longterm mind-set towards assetownership. Of the capitalraised by infrastructurefunds since 2006, 48% hasbeen by vehicles with amaturity of greater than 10years4. Capital investmentdecisions are typicallyweighted towards assetperformance and long-termvalue creation, rather thanshort-term gain.Management incentives arecommonly aligned to thesegoals (as opposed to theshorter term incentivestypically seen in privateequity and some corporatestructures). Even wheninvestors are consideringselling their assets, this istypically done viapresentation of a long-termbusiness plan backed bymanagement teams.Investors’ desire to improvetheir assets – commonlythrough improving efficiencyand customer experienceand exceeding regulator-setperformance targets.Objective analysis hasshown performanceimprovements acrossprivate-investedinfrastructure with examplesincluding:46 In Australia, privateowners of the electricitydistributors haveoperated their assets atleast 15% and as muchas 33% more efficientlythan public ownedassets. In the UK, watercompanies haveachieved an annualreduction in waterleakage of 13% annually,a saving equivalent tothe entire consumptionof Wales.PwC analysis of InfraDeals fundraising informationGlobal Infrastructure Investment3. Specialist investorsunderstand andembrace the keyeconomic and socialroles of theirinfrastructure assetsThe investors we haveinterviewed as part of thisreport have consistentlyreferred to their roles ascustodians of infrastructureassets rather than businessowners.This is demonstrated in awillingness to invest inassets throughout theeconomic cycle and a desireto engage with regulatorsand municipal bodies toensure public needs arebeing met.4. Appropriate returnsexpectationsweighted towards thelonger termAs more investors haveentered the market,competition for availableinvestments has increased.This, in turn has reducedthe level of return targetedby infrastructure fundsglobally to reduce from anaverage of 14.0% in 2004 to10.6% in 20164.Access to low-cost, longterm capital is providingsignificant benefits toconsumers – with ownersand regulators alikedemanding substantialperformance improvementsto mitigate the need forsignificant increases incustomer bills to fund therequired investment.

Looking forward With a major gap between the world’s infrastructure needs and countries’ abilities tofund construction, combined with governments globally committed to infrastructure asa mechanism for driving growth, harnessing the large pools of low-cost capitalpresented by specialist infrastructure investors would appear an obvious solution.Evidence of recent performance suggests that investors are responsible, appreciatethe needs and public status of their assets, and are committed long-term stewards.However, evidence is still relatively limited, and this industry remains less than 20years old. It would be complacent to ignore the challenges, and the onus will remainon the industry to prove its capabilities as custodians of the world’s infrastructure.Committed asset managementto continue to driveimprovement and investmentBy their nature as essential publicservices, infrastructure businessesrequire a lot of effort and ongoingexpenditure to keep them operating well,particularly those meeting the needs ofexpanding cities and increasinglydemanding consumers.Whilst new entrants to directinfrastructure investment are bringingwith them lower return requirements andeven longer investment horizons thantheir predecessors, they also ofteninvest in minority stakes and are stilldeveloping their asset managementcapabilities.We consider it important for the industrythat investors continue to support activeasset management to ensure theperformance improvements achievedover the last decade continue goingforwardTransparent governancestructures should be embracedWe consider it important that globalinfrastructure investors continue torecognise there is valid public interest intheir investments and that, given themonopolistic nature of many regulatedcompanies, the highest standards ofgovernance are required. In order tofurther build confidence in the sector,investors in essential services shouldcommit to good governance and robustownership principles.Continued dialogue to enablegreenfield investmentWhilst there is a recognised need to fundnew infrastructure across the world, therisks and challenges of investing ingreenfield construction projects meansthat such projects typically remain beyondthe remit of many institutional investors.To bridge the global infrastructure gap, itwill be incumbent on both the industry andgovernments to devise, sponsor andchampion innovative structures in order toenable low cost capital to be better usedin meeting the world’s infrastructureneeds.PwC and GIIA7

The need forprivateinvestmentinto globalinfrastructure –and its impacts8Global Infrastructure Investment

BackgroundThe desire to invest in infrastructure as anasset class has never been stronger. Hugeamounts of capital have been made availableby pension, insurance and sovereign wealthfunds and, as a consequence, many ownersof infrastructure assets – government andprivate alike – have taken advantage of thesharp rise in asset values by putting assetsup for sale.Specialist investors have bought into a widerange of the developed (and in certain cases,developing) world's infrastructure – rangingfrom Australian airports to UK watercompanies with a wide array of port, energyand telecoms infrastructure in between.At the same time, strong questions havebeen raised about the quality and sufficiencyof the world’s existing infrastructure. AMcKinsey study in June 2016 estimated thatUS 3.3 trillion needs to be invested eachyear to 2030 in order to support currentgrowth rates5. Visitors to major capitals justneed to spend time on Los Angeles'6congested roads, in long security lines atNew York's airports7 or London's packedunderground8 to experience this forthemselves.Politicians have responded to pressure bypromising new major improvements – withthe Trump administration pledging US 1trillion of investment in roads, bridges,schools and hospitals9 – to be largely fundedthrough tax-incentivised private capital.Such commitments are mirrored aroundthe world, with Theresa May’s new UKadministration sponsoring high valueinvestment into “infrastructure and innovationto boost productivity”10, Angela Merkelpledging to raise spending on roads,railways and broadband with “no newdebts”11, and the Chinese governmentsetting aggressive targets to improve manykey infrastructure sectors between now and202012.Hence the need for high-quality, privatelyfunded infrastructure has never been clearer –a position articulated back in 2008 bylibertarian US think tank Cato Institute that“most nations face daunting infrastructureproblems. To solve them, well-tested methodsof private provision must be embraced”.A 2011 OECD study also concluded that“increased private sector investment instrategic transport infrastructure willbe essential”.However, given many of the investors remainrelatively unknown private organisations, it isperhaps not surprising that the public can besceptical about these organisations’ actionsand motivations. Examples include headlinesaround “asset-stripping” and “morallyquestionable” structures. With limited publicreporting on infrastructure performance,investment and return requirements, it hasbeen difficult to date for the industry to respond.This document brings together availablecommentary and analysis, exploring theimpact that private investors have had – andare having – on the world’s infrastructure,and the impacts this is bringing to countries,economies and societies worldwide.5Source: McKinsey Global Institute, Bridging Global Infrastructure Gaps, June 20166Research by consultancy INRIX indicates Los Angeles tops the list of the world’s most gridlocked cities, withdrivers spending 104 hours in congestion in 2016 during peak time periods7PwC, Future-ready airports, rports.pdf8Source: http://static.guim.co.uk/ni/1411375335657/Tube graphic s-congress10 1611 Source: ebs/BKin/Suche/DE/Solr Mediathek formular.html?id 2068864&cat podcasts&doctype AudioVideo12 turePwC and GIIA9

The creation of these specialist vehicles andteams has, unsurprisingly, led to a sharp rise inthe volume and value of infrastructuretransactions over the last decade (see Figure 2),and a significant rise in asset valuations13, asacquirers have accepted lower returns on theirinvestments.The key question, of course, is the impact theseinvestments have had on customer pricing andquality of -20062007200820102011Aggregate fund -2010201120122013North AmericaMiddle East & Africa20142015Q3 2016 LTMLatin AmericaGlobal transcation volumeSource: InfraDealsFigure 3: Global infra investment – Equity and PPP by type of ownerOtherSovereign wealth fundPension fund5%8%5%32%Global Infrastructure Investment2016FFigure 2: Global infrastructure transaction activityInfrastructure fund102015No. of closed funds50%13 cture-Aug-15.pdf2014Source: InfraDealsEuropeAsia / AustraliaInfraDeals estimatesthat over US 110bn ofdry powder is availableto deploy globally fromunlisted equity funds.2009Number of funds60,000Source: InfraDealsCorporateNumber of transactionsIt is estimated that at least the same amountagain has been allocated to infrastructure byorganisations seeking to invest directly rather thanthrough investment funds. Typically, theseorganisations will be major pension, insuranceand sovereign wealth funds; all of whom haveneeds for long-term investments.USD millionsIn the decade since the Global Financial Crisis,more than US 200bn (see Figure 1) has beenraised by investment funds to deploy long termcapital into infrastructure investments.Figure 1: Global unlisted infrastructure fundraisingUS billionsA global desire to investinto Infrastructure

A reduction in annual water leakage by 13%annually – equivalent to the entire consumptionof Wales (see Figure 7)Reductions in electricity supply interruptions by29% and length of average outage by 39%(see Figure 5)High investment levels: in every year between2004 and 2014, water companies and electricitydistribution network operators invested moreper customer than was generated in profitsIn their review, PwC UK attributed theseimprovements to a number of factors created by thechange in ownership, including: A long-term perspective on the asset, withfocus on performance and value creation Focus on the underlying infrastructure, ratherthan ancillary commercial businesses Desire to work with regulators for the long-termbenefit of consumers An alignment of management incentives withlong-term performancePwC concluded overall that its analysis showed“a notable improvement in performance across allmajor asset classes, which we consider is in nosmall part due to the focus and investment capitalprovided by specialist investors”. (See Figures 3and 4).Key examples of the above can be seen in the casestudies. Analysis of Thames Water’s performancefollowing Macquarie’s investment shows a 31%reduction in leakage since 2006, beating regulatorset targets in each year, something it had beenfiercely criticised for under previous ownership.Another water company featured in this report,Affinity, has seen marked improvements in itscustomer engagement and cost efficiencies sinceacquisition by Morgan Stanley and Prudential’sinfrastructure arm in 2012.Figure 4: Average customer minutes lost (CML)Average customer minutes lost UK electricity distribution100806040202003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Average actual CMLOfgem average target CMLSource: OfgemFigure 5: Average customer interruptions (CI)Average customer interruptionsWhilst there is limited direct analysis on the impactof investors on infrastructure as a sector, it ispossible to look at specific sectors where privateinvestment is most developed. In its paper The roleand impact of specialist investors in UKinfrastructure14, PwC reviewed the performance ofthe UK’s airports, energy distributors, water andsewerage companies, which had seen apronounced shift in ownership over the ten years to2015. Highlights of this analysis 102003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Average actual CIOfgem average target CISource: OfgemUK Water and WastewaterFigure 6: Water infrastructure serviceability rating for overallnetwork100%% of total networkInfrastructure asset performance80%60%40%20%0%2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013ImprovingStableMarginalDeterioratingSource: OfwatFigure 7: Total leakage across England and Wales 3673,3003,3003,2003,2393,1003,3133,3463,1033,113 3,0963,0002,90014 alistinvestors-in-uk-infrastructure.html2,8002003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014Leakage (Ml/day)Source: OfwatPwC and GIIA11

The regulator of the water sector in England andWales (Ofwat), in its latest price review, was ableto reduce bills in real terms by 5%, despite strongand continued improvements in target servicelevels. As Ofwat stated, “Companies are set tospend more than 44bn (or around 2,000 perhousehold) by 2020 customers will benefit fromsubstantial improvements”15.The above has only been possible throughinvestors’ desires to put significant amounts ofcapital into the industry, seeking increasinglymodest returns. Analysis by PwC of funds raisedsince 2004 shows a clear downward trend inreturn expectations from 14% in 2004 to 10.6% in2016 (see Figure 8). Many regulators have takenadvantage of investors’ desire to deploy capital ininfrastructure, by allowing ever-lower returns ineach regulatory review over the last decade (seeFigure 9).In October 2016 a review by PwC Australia intothe impact of privatisation on the Australianelectricity market demonstrated that, on acost-per-customer basis, private owners of theelectricity distributors in Australia operated theirassets at least 15% and as much as 33%cheaper than publicly owned assets (see Figures10 and 11)16. Further, this document highlighted a2014 review by the NSW Treasury, which foundelectricity bills in Victoria and South Australia(where the electricity networks are held in privateownership) increased at lower rates than in NSWand Queensland (where at the time theyremained in public hands17).15.0%14.0%13.0%Target IRRThe vast majority of addressable evidence in factappears to suggest the opposite – that privateinvestment in infrastructure typically drivesimprovements for consumers with either a) theneed to compete (for non-monopolisticinfrastructure such as seaports and airports),which leads to a shift in strategy towardscustomers; or b) regulators setting demandingefficiency targets and price constraints. Typically,regulators appear to become emboldened whendealing with privately run companies rather thanstate-owned 042005200620072008200920102011Average target 9return201220132014201520162017Linear (Average target 9return)Source: PwC analysis of InfraDeals fundraising informationFigure 9: Historical development of regulated Weighted Average Cost ofCapital (WACC)7.0%WACC (vanilla, real)One of the charges commonly levelled againstprivate sector investors is that their focus onimproving profits can only be achieved to thedetriment of customer service and reducedmaintenance of the assets.Figure 8: Average targeted return of funds raised 072008Electricity distribution - UKRail - UKWater - Northern Ireland2009 2010 2011Year of price review20122013Airports - UKWater - UKWater - Victoria201420152016Water - NSWWater - South AustraliaSource: PwC analysis of regulatory settlementsFigure 10: Total cost per customer compared with customer density(average 2009-2013)1,600ERG1,400Total user cost per customer ( )Profit versus service GDENDCIT200UED JEN0102030405060708090100110Customer density (customer/ km line length)PublicPrivateLinear (Public)Linear (Private)Figure 11: Multilateral total factor productivity for each distributorPublicly-owned networks are dashed lines2.01.81.61.41.21.00.8200615 Source: wn/16 PwC Australia “The case for change – Privatisation ofWestern Australia’s electricity networks” October 201617 Across 2015 and 2016 NSW has subsequently privatisedboth its electricity transmission and distribution networks12Global Infrastructure DTND20112012JENESS*ACT power networks are owned through a public/private joint venture.Source: Australian Energy Regulator, Electricity distribution network serviceproviders1818 ber%202014 0.pdf2013PCRAGD

Similar outcomes are expected from both PeelPorts expansion of Liverpool 2 in the UK andGlobal Container Terminal's (GCT) investment intoimproving Deltaport in Vancouver. These projectsare expected to facilitate the creation of 5,000 and5,500 jobs and 1.1bn and C 500m of economicvalue respectively.Of course, public needs may require more thanimproved airports or shipping and tourism growth.In some cases, they're driving critical investment toimprove people's health and wellbeing. Less than20 years ago, most Chilean cities were stillroutinely dumping raw sewage into seas and rivers– with less than 15% of sewage being treated priorto disposal20.Chile’s answer incorporated the harnessing ofprivate capital alongside strict regulatoryobjectives, in particular the ambitious goal ofproviding 90% of the population with treatedsewage. Partial privatisation of Chile’s watercompanies from 1998 encouraged long-terminvestors such as Ontario Teachers’ Pension Planto invest alongside global water companies.The result of the programme has been seismic,with huge improvements in water quality andsupply, and a steep decline in hospital admissionsfor typhoid and shigellosis – illnesses typicallycontracted from unclean water (see Figure 15)20. 19 s/BAC%20Sustainability%20Report%20FY2016.pdf20 SISS (Superintendence of Sanitary Services), 2011 OfficialEnvironment Status report50,000 50,00040,00030,00021,00020,00010,0004,700-1996 / 97Actual2015 / 16Actual2033 / 34EstimateSource: BAC annual sustainability report, 2016Figure 13: Job and economic value 3.810,0005,0005,000-3.05,5001.40.4JobsGVABrisbane airportrunway expansionJobsGVAJobsLiverpool 21.5GVA (USD Billiions)Brisbane’s owners have recently committed tofurther development – with an A 3.3bn runwayexpected to deliver incremental economic benefitsto the region of A 5bn per annum and a further29,000 jobs by 2035 as the airport’s capacitycontinues to grow19. The privatisation has clearlybeen a factor in total economic growth.60,000FTEsOn investigation, evidence from the case studiesindicates the long term nature of infrastructureinvestors also contradicts this claim. Analysis ofBrisbane Airport Corporation’s (BAC) performancefollowing privatisation in 1997 (owned by aconsortium of Australian superannuation funds, ledby infrastructure specialist First State Investments),shows nearly A 2.5bn in capital investment up to2016 (see Figure 22), driving a doubling inpassenger numbers over the same period. Indeedit has also been responsible for the creation of over16,000 jobs, whilst being run as a commercialenterprise.Figure 12: BAC – employment at the airportJobsArguments are also often put forward thatinfrastructure operated on a commercial basis,weakens the ability to use it as a tool for economicdevelopment.GVADeltaportSource: BAC annual sustainability report, 2016; Superport Action Plan,2011; Deltaport Terminal, Road and Rail Improvement Project ConsultationDiscussion Guide, 2011Figure 14: Chile – urban coverage of drinking and wastewater100%% coverageResponding to public needs99.6% 99.8% 100.0%99.8%96.8%93.1% 95.2%82.3%75%50%25%20.9%0%2000Drinking nt**Until 2010, Sewage treatment was calculated over the total urbanpopulation. From 2011 onwards, it has been calculated over populationconnected to sewage.Source: Superintendence of Sanitary Services (SISS)Figure 15: National urban coverage of sewage water treatmentand hospital discharges, 2003-2007Hospital Discharge (cases)1200SWTP Coverage (MM 70Source: Superintendence of Sanitary Services (SISS)PwC and GIIA13

IndustrychallengesWhilst the overall picture hasbeen positive, it would be naïveto assume that all infrastructureinvestments have found stablehomes and will continue toperform excellently for theforeseeable future.1. Committed asset managementBy their nature as essential public services, infrastructurebusinesses require a lot of effort and ongoing expenditureto keep them operating well, particularly those meeting theneeds of expanding cities and increasingly demandingconsumers.Whether it is city centre water companies needing toreplenish ageing networks to meet the needs of growingpopulations, airport owners needing to respond to airlinedemands, or telecoms businesses rolling out fibreinfrastructure capable of filling the appetites of technologyhungry consumers, all will require high qualitymanagement supported by committed shareholders whoare focused on the challenges facing their assets.Following our review, we have identified three principalchallenges facing the industry, which investors will need torespond to if they are to continue building their reputationsas good custodians of the world’s infrastructure assets: (i)committed asset management, (ii) good governance and(iii) continued investment into new infrastructure.14Global Infrastructure InvestmentMuch of the initial wave of infrastructure investment,which is explored in this report, was driven byinfrastructure funds with strong asset managementcapabilities, harnessing private capital to acquire longterm infrastructure assets, primarily from corporate andgovernment vendors. These organisations typically hadboth the scale and appetite for heavy assetmanagement roles, which in our view have contributedsignificantly to the improvements in performanceevidenced throughout this report.The industry has evolved since then, with many newentrants (which had previously invested in infrastructurefunds) choosing now to invest directly instead. Many ofthese new entrants represent pension funds, insurancecompanies and sovereign investment funds.As a group these organisations have brought muchlower cost capital into the sector, often with even longerterm investment horizons than the funds which theyreplace – both of which have the benefits of continuingto support high levels of investment whilst keepingend-user costs down. However, they also often investin minority stakes, and many haven’t yet achieved thescale or appetite for major asset management roles.We consider it important for the industry that itsinvestors continue to evolve and strengthen their assetmanagement capabilities in order to drive the nextwave of improvements and investment across theworld’s infrastructure base.

2. Transparent governanceUnderstandably, with an expanding universe of investorsacquiring assets regarded by consumers as essential services,scepticism has been expressed around whether investors’motivations and structures are in the public interest.This point has been articulated by many stakeholders includingregulators, who understandably believe that the monopolistic,high profile, nature of many regulated companies requires thehighest standards of governance.Academics in the industry have also highlighted the long termbenefits of robust governance. Recent studies have shown thatlong term, sustainable approaches to management are not justin consumers’ interests, but companies, too: “88% of reviewedsources find that companies with robust sustainability practicesdemonstrate better operational performance, which ultimatelytranslates into cash flows.” 21This is a view that is recognised and shared by numerous globalinvestors (and GIIA members), which have clearly stated aimstowards good governance. One such member, HermesInvestment Management, made its position explicit in a 2017position statement: “It may be that the case for implementing aformal, separate governance regime for infrastructurebusinesses that provide essential public services is consideredby some as impractical and undesirable . However, we arestrong advocates of an enhanced code applicable to privatelyowned

out of the analysis: 6 Global Infrastructure Investment 1. A specific investment approach geared towards long-term essential assets The infrastructure investor community brings a long-term mind-set towards asset ownership. Of the capital raised by infrastructure funds since 2006, 48% has been by vehicles with a maturity of greater than 10 .