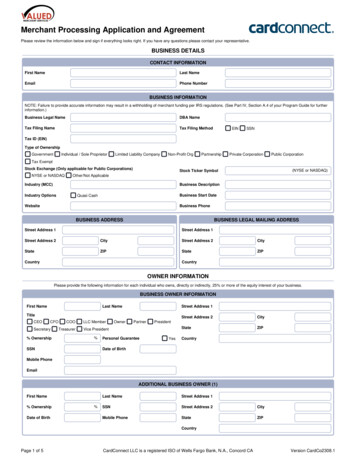

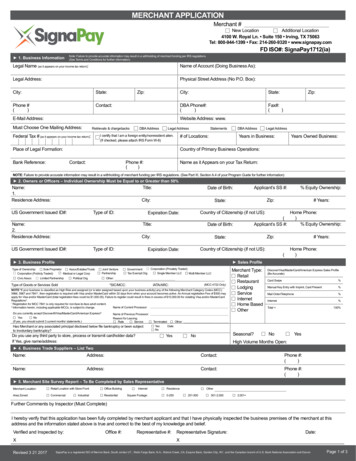

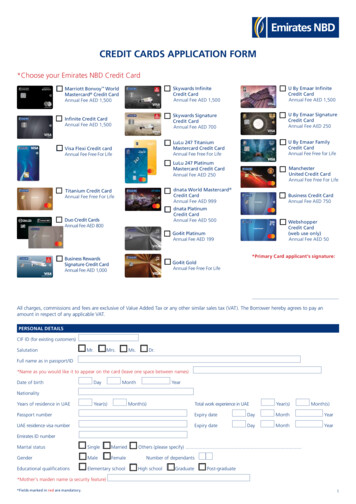

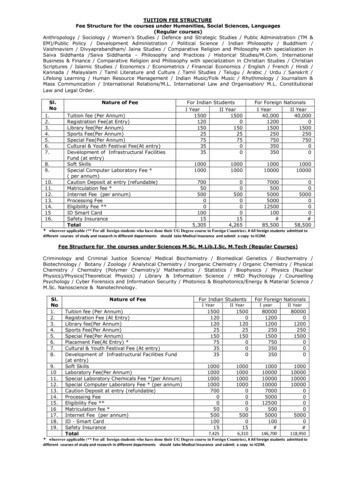

Transcription

404(a) annual participant fee disclosureFrequently asked questionsAssisting plan sponsorsQ1.A1.Q2.A2.What must the plan sponsor of an ERISAgoverned plan do to comply with the404(a)participantfeedisclosureregulation?The regulation requires plan sponsors toprovide certain plan- and investment-relatedinformation to participants, beneficiaries ofdeceased participants with a balance, andeligible employees on an annual basis andcertain fee and expense information toparticipants on a quarterly basis. AlthoughLincoln is preparing quarterly disclosuresand a sample annual disclosure on behalf ofthe plan sponsor, the plan sponsor mayneed to edit portions of the annual disclosurethat cannot be populated from theinformation contained in our recordkeepingsystems.What is Lincoln responsible for doing tocomply with the 404(a) participant feedisclosure regulation?The plan sponsor has a fiduciaryresponsibility to comply with the participantfee disclosure regulation. Lincoln continuesto help plan sponsors satisfy participant feedisclosure by making the web componentsavailable to participants and preparing asample annual disclosure on behalf of theplan sponsor using the information containedin our recordkeeping systems. Lincoln helpsplan sponsors satisfy quarterly feedisclosure requirements through the deliveryof a redesigned participant retirementstatement that displays the required fees oneach statement.Q3.A3.Q4.A4.Is there a penalty for not complying withthe regulation?Although there’s no explicit penalty for notcomplying with the 404(a) participant feedisclosure regulation, a plan sponsor doeshave a fiduciary duty to comply. A breach offiduciary duty could be a liability.What steps has Lincoln taken to assist plansponsors in complying with the 404(a)participant fee disclosure requirements?Each year, Lincoln creates a sample 404(a)annual participant fee disclosure documentwith the information contained in ourrecordkeepingsystemfollowingtheguidelines of the regulation. In addition,Lincoln has taken the following steps: We made web components available toboth participants and non-participants We enhanced our retirement statements toinclude fee informationBeyond the requirements, Lincoln providedplan sponsors with the following: A Participant’s Guide to UnderstandingRetirement Plan Fee Disclosure Newsletter articlesQ5.A5.What steps has Lincoln taken to assist inthe education of participants on the 404(a)participant fee disclosure requirements?Lincoln created A Participant’s Guide toUnderstandingRetirementPlanFeeDisclosure, which has been included as astatement insert with quarterly participantretirement statements.Lincoln Financial Group is the marketing name for Lincoln National Corporation and its affiliates. Affiliates are separately responsible fortheir own financial and contractual obligations.

In addition, messages have been includedon the quarterly participant retirementstatements and in newsletter articles. Wealso provided a web-based informationalpresentation for participants.Delivery of the 404(a) annual participant feedisclosure documentsQ6.A6.Q7.A7.Q8.A8.Who should receive a copy of the 404(a)annual participant fee disclosure?The disclosure must be delivered to all planparticipants, beneficiaries of deceasedparticipants with a balance, and eligible nonparticipating employees.Does the 404(a) annual participant feedisclosure need to be distributed toparticipants on the beginning date of theplan year?No; the only requirement is that thedisclosure is to be delivered annually. For thispurpose, “annually” means at least once inany 14-month period, without regard towhether the plan operates on a calendar yearor fiscal year basis.Has the timing for ongoing annualdisclosure been determined?Yes. Annual disclosure must be furnished toparticipants no later than 14 months from thedate the previous annual disclosure wasprovided.Mailing of the 404(a) annual participant feedisclosure documentsQ9.A9.Can plan sponsors provide the annualdisclosure to their participants via email?The Department of Labor (DOL) has strictrules regarding electronic delivery. Emaildelivery is allowed as long as the plansponsor adheres to the DOL rules forelectronic disclosure delivery. The generalrequirements are: The plan sponsor must take appropriatemeasures to ensure that the system forfurnishing electronic documents results inactual receipt of the information byparticipants The information must be written andpresented in a manner that’s easilyunderstood by the average participant The participant must have a right to requesta paper disclosure document free of charge The participant must receive a notice ofthe significance of the electronicallydelivered document if the significance isnot otherwise reasonably evidentWith regard to consent to receive a disclosureelectronically, the DOL regulation dividesparticipants (including active and inactiveparticipants and eligible employees) into twogroups:Certain participants who are activeemployees – A plan sponsor may discloseinformation electronically to active employeeswhose work duties require accessing anelectronic information system if the generalconditions are met.All other participants and eligibleemployees – A plan sponsor may discloseinformation electronically if the followingrequirements are met: The person has affirmatively consented toreceive documents through electronicmedia and has not withdrawn such consent In the case of documents to be furnishedthrough the internet or other electroniccommunication network, the person hasconsented or confirmed consent in theelectronic form that will be used to furnishdocuments and has provided an addressfor the receipt of electronically furnisheddocuments(i.e.,thepersonhasdemonstrated his or her ability to receivethe information from the internet or otherelectronic communication network) Prior to consenting, the person is provided aclear statement indicating:- The types of documents to which theconsent will apply- That consent can be withdrawn at anytime without charge- The procedures for withdrawing consentand updating contact information- The right to request and obtain a paperversion of an electronically furnisheddocument- The description of any hardware and/orsoftware requirements needed forelectronic delivery- Certain information regarding systemchanges2

The delivery methods must satisfy thegeneral conditions (referenced earlier)Q10. May a plan sponsor use funds from theirforfeiture account to pay for the printing andpostage costs incurred from mailing the404(a) annual participant fee disclosure?A10. Yes, if permitted by the terms of the plan.Printing and postage costs associated withdelivering the 404(a) participant feedisclosure are reasonable expenses ofadministering a plan. A plan should be able topay for such expenses from the plan’sforfeiture account. To do so, the plan sponsorneeds to provide us with documentation tosubstantiate that the expenses were directlyincurred in the administration of the plan.Multi-vendor plansQ11. Will Lincoln provide the annual disclosureto another vendor?A11. No. Lincoln will provide the annual disclosureto the plan sponsor. The plan sponsor mayforward the disclosure to another vendor, asdesired.Q12. Will Lincoln provide a data file of the annualdisclosure information to the plan sponsor? A12. No. Lincoln will make available a MicrosoftWord version of the completed disclosuredocument.Q13. Can Lincoln receive a data file fromanother vendor and create one documentwhich aggregates all vendor data?A13. No. Lincoln cannot accept a data file.Fees on quarterlystatementsparticipantretirementQ14. What information does a participant seeon his or her quarterly retirementstatement?A14. Quarterly participant retirement statementsinclude a Fees and Expenses field under theAccount Summary, Activity by Source, andActivity by Investment sections showing thedollar amount of the fees and expensesactually charged to or deducted fromindividual retirement accounts. For example,if a loan is initiated, the Loan Activity sectionwill display more detailed fee information forthe loan setup fee. In addition, a Fees andExpenses section was added, and moredetails are available in the Activity Detailssection, if applicable.Q15. When will fees appear on a quarterlyparticipant retirement statement?A15. Fees appear if they’ve been deducted duringthe statement time frame.Q16. Do investment fees display on the quarterlyparticipant retirement statements?A16. No. Investment fees aren’t listed on thequarterly participant retirement statement.Investment fees are displayed in thecomparative chart on the annual participantfee disclosure.Q17. Do fees display on retirement statementsfor non-ERISA plans?A17. No; 404(a)-compliant fee information willdisplay on statements for ERISA plans only.Q18. Can a plan sponsor request that fees bedisplayedonquarterlyparticipantretirement statements for non-ERISAplans?A18. No; 404(a)-compliant fee information willdisplay on statements for ERISA plans only.Annual participant fee disclosure documentQ19. What information does the annualparticipant fee disclosure documentcontain?A19. The annual participant fee disclosurecontains general information about the plan,including information about investmentoptions available under the plan and fee andexpense information. In addition, the annualparticipantfeedisclosurecontainscomparative charts with performance data,benchmarking information, and fee andexpense information about each investmentoption available under the plan.Q20. What are the comparative charts?A20. The comparative charts are a part of the404(a) participant fee disclosure that provideinformation about investment performanceand fees and expenses participants pay forvariable and fixed investments. The chartsare intended to allow participants to make anapples-to-apples comparison of fees andexpenses between plans.3

Q21. What information is included on thecomparative charts?A21. There are four comparative charts in the404(a) participant fee disclosure. They include:Chart 1 – Variable return investmentsThis chart focuses on the performance ofinvestment options without a fixed or statedrate of return. It illustrates how theseinvestment options have performed over timeand compares the investments with theappropriate benchmark for the same timeperiods.Chart 2 – Fixed return investmentsThis chart focuses on the performance ofinvestment options with a fixed or stated rateof return. It illustrates the annual rate of returnfor each option, as well as the term or lengthof time a participant will earn the stated rate.Chart 3 – Fees and expensesThis chart illustrates fee and expenseinformation for the investment options listed incharts 1 and 2. This chart displays the totalannual operating expenses (expenses thatreduce the rate of return of the investmentoption) of chart 1. In addition, shareholder-typefees (fees that are in addition to the totalannual operating expenses) are representedon the chart.Chart 4 – Annuity optionsThis chart focuses on the annuity distributionoptions, if any, available under the plan.Annuity distribution options are insurancecontracts that allow participants to receive aguaranteed stream of payments at regularintervals, usually beginning at retirement andlasting until death.Q22. Why would a plan sponsor need to editportions of the annual disclosure?A22. Lincoln provides all the information we have onfile that’s needed to support the disclosure.Some pieces of information, such as TPA fees,are not kept in our recordkeeping systems.Additionally, plan contact information may notbe housed in our recordkeeping system or theinformation may not be the most up-to-date.Therefore, a plan sponsor will need to discloseinformation that isn’t maintained by Lincoln orthat has changed.Q23. If a plan has one or more TPAs, are TPAfees included?A23. TPAs were given an opportunity to provide theirfees to Lincoln. Lincoln populates the TPA feepage in the participant fee disclosure templatewith any information the TPA provided. If TPAfees weren’t provided, the TPA fee page ispopulated with X.XX for the fee.Q24. How will the plan sponsor edit the annualdisclosure document?A24. The document is available as an editable Microsoft Word document, and the plansponsor will be able to delete or edit text as needed using Microsoft Word 2000 or newer.Note: Multi-Fund Individual variable annuity, MultiFund Select variable annuity, Multi-Fund groupvariable annuity, Lincoln Group Variable Annuity,and Group Fixed Annuity plan sponsors will not haveaccess to electronic versions of their participant feedisclosure and will need to request electronicversions from their account managers.Q25. Do plan sponsors need additionalsoftware to view and edit the annualdisclosure document? A25. Plan sponsors will need Microsoft Word2000 or newer to edit the 404(a) participantfee disclosure document.Q26. Is there a requirement to provide theannual disclosure in other languages?A26. General ERISA disclosure rules may requirea plan sponsor to provide assistance to planparticipants who are literate only in a nonEnglish language, if certain conditions aremet. Assistance may not need to involvewrittenmaterials.Lincolnprovidesdisclosures in English.Q27. What’s the difference between standardperformance and net of fees performance?A27. Standard performance includes surrendercharges, if applicable, so it generally is lowerthan net of fees performance, which doesn’tinclude surrender charges.Here’s an example using the American FundsGrowth Income fund:StandardNet of %-3.98%-2.81%-2.27%10-year1.63%2.12%4

Notice the difference in performance in the 1year number. The large surrender chargehampers standard performance.and updates a general glossary of terms onLincolnFinancial.com.ERISA vs. non-ERISA plansWeb disclosuresQ28. Who has access to the investmentinformation on the web?A28. Lincoln made the plan’s investmentinformation available to participants and plansponsors through a secure website. Thisincludes active participants, eligible nonparticipating employees, and beneficiaries ofdeceased participants with a balance.Active participants will log in with their user IDand password to see the disclosures. Eligiblenon-participating employees may access thedisclosures following the instructions providedto them by the plan sponsor.Q29. What information can a non-participatingemployee view on the web?A29. For each plan investment, an eligible nonparticipating employee may view: Name of the issuerInvestment objectives and strategyPrincipal riskTurnover rateInvestment performanceFee and expense informationGlossary of termsQ30. Howwilleligiblenon-participatingemployees of a plan access the webcomponents?A30. Plan sponsors will receive in their cover letterand disclosure instructions that may bepassed on to participants. The instructionswill include the web address (URL), plan IDand plan name that may be used by anemployee to access the plan fund informationpage.Web glossaryQ31. What do the regulations say aboutproviding a glossary of terms?A31. The regulations require the plan sponsor toprovide a general glossary of terms to assistparticipants in understanding their investmentalternatives. As needed, Lincoln maintainsQ32. Will an employer with more than oneERISA plan receive a separate annualdisclosure for each plan?A32. An employer with more than one ERISA planwill receive a separate disclosure for each plan.Q33: How will I let Lincoln know if my planstatus changes from non-ERISA toERISA?A33: Please notify your account manager of thechange.Sample documentsQ34. Is there a sample annual participant feedisclosure?A34. Yes. Sample 404(a) annual disclosures may berequested from your account manager or fromthe Lincoln Customer Contact Center.MiscellaneousQ35. Will the Summary Plan Description (SPD)change to help plan sponsors comply withthe 404(a) participant fee disclosure?A35. No. Although some of the disclosures can beincorporated into the SPD, Lincoln does notuse the SPD as the delivery vehicle forparticipant fee disclosure. This is due to thefact that timing requirements for SPD deliveryare different from those for the participant feedisclosure for existing employees.Q36. I made changes to my plan afterdistributing the 404(a) annual participantfee disclosure. Do I need to send a newdisclosure?A36. Changes to general plan information,administrative information, and individual feeinformation generally require you to notifyparticipants and eligible employees of thechanges no less than 30 days and no morethan 90 days before the changes take effect.For example, if you add or remove aninvestment option from the plan’s investmentfund lineup, you must notify participants ofthe change no less than 30 days and no morethan 90 days before the change takes effect.5

Changes to the investment comparative chart performance and fee informationgenerally don’t need to be disclosed mid-year (other than on the website).Under extraordinary circumstances, the duties of prudence and loyalty underSection 404 of ERISA may require you to inform participants and eligibleemployees of important changes to investment-related information before thenext comparative chart is required under the regulation.Q37. Will my advisor/TPA/consultant receive a copy of my disclosures?SMA37. For Lincoln Director plans, TPAs, advisors, and consultants who have accessto their clients’ websites will be able to access the 404(a) annual participant feedisclosure materials online. For Lincoln Alliance plans, intermediaries will need to contact AccountManagement to request copies of fee disclosure documents.Q38. Can ERISA plan participant accounts that are excluded from that plan’sForm 5500 report filing also be excluded from 404(a) disclosurerequirement?A38. Yes, if certain conditions are met. The DOL specifically excluded 403(b) annuitycontracts and custodial accounts that meet certain requirements (e.g., vestedaccounts issued to a current or former employee before January 1, 2009, forwhich the employer ceased to have any obligation to make contributions) fromForm 5500 and DOL Regulation Section 2550.408b-2 ‘covered service provider’disclosure requirements.In DOL Field Assistance Bulletin No. 2012-02R, the DOL extended the rules forexempt accounts for Form 5500 purposes and covered service providerdisclosure to the 404(a) annual disclosure requirements.You’re In Charge 2016 Lincoln National CorporationLincoln Financial Group is themarketing name for Lincoln NationalCorporation and its affiliates.Affiliates are separately responsiblefor their own financial and 2810Affiliates of Lincoln National Corporation include, but are not limited to, The LincolnNational Life Insurance Company, Lincoln Life & Annuity Company of New York, andLincoln Retirement Services Company, LLC, herein referred to as “Lincoln.”Annuity products are issued by The Lincoln National Life Insurance Company, FortWayne, IN, and distributed by Lincoln Financial Distributors, Inc. The Lincoln NationalLife Insurance Company does not solicit business in the state of New York, nor is itauthorized to do so. Contractual obligations are subject to the claims-paying abilityof The Lincoln National Life Insurance Company. Annuity products sold in New Yorkare issued by Lincoln Life & Annuity Company of New York, Syracuse, NY, anddistributed by Lincoln Financial Distributors, Inc. Contractual obligations are subjectto Lincoln Life & Annuity Company of New York.Product and features subject to state availability. Limitations and exclusions may apply.The Lincoln Alliance program includes certain services provided by Lincoln FinancialAdvisors Corp. (LFA), a broker-dealer (member FINRA) and an affiliate of LincolnFinancial Group, 1300 S. Clinton St., Fort Wayne, IN 46802. Unaffiliated broker-dealersalso may provide services to customers.Microsoft, Encarta, MSN, and Windows are either registered trademarks or trademarksof Microsoft Corporation in the United States and/or other countries.6For plan sponsor use only. Not for use with plan participants.

Annual participant fee disclosure document Q19. What information does the annual participant fee disclosure document contain? A19. The annual participant fee disclosure contains general information about the plan, including information about investment options available under the plan and fee and expense information.