Transcription

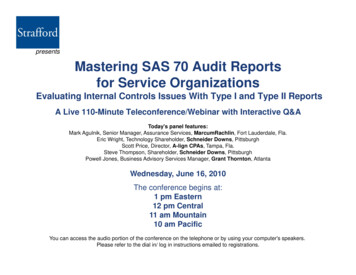

presentsMastering SAS 70 Audit Reportsfor Service OrganizationsEvaluating Internal Controls Issues With Type I and Type II ReportsA Live 110-Minute Teleconference/Webinar with Interactive Q&AToday's panel features:Mark Agulnik, Senior Manager, Assurance Services, MarcumRachlin, Fort Lauderdale, Fla.Eric Wright, Technology Shareholder, Schneider Downs, PittsburghScott Price, Director, A-lign CPAs, Tampa, Fla.Steve Thompson,p, Shareholder,, Schneider Downs,, PittsburghgPowell Jones, Business Advisory Services Manager, Grant Thornton, AtlantaWednesday, June 16, 2010The conference begins at:1 pm Eastern12 pm Central11 am Mountain10 am PacificYou can access the audio portion of the conference on the telephone or by using your computer's speakers.Please refer to the dial in/ log in instructions emailed to registrations.

For Continuingg Education purposes,please let us know how many peopleg at yyour location byyare listening closing the notification box and typing in the chat box yourcompany name and the number ofattendees.attendees Then click the blue icon beside the boxto sendsend.For live event only.

If the sound quality is not satisfactoryand you are listening via your computerspeakers please dial 1speakers,1-866-873-1442866 873 1442and enter your PIN when prompted.psend us a chat or eOtherwise,, pleasemail sound@straffordpub.comimmediately so we can address theproblem. If you dialed in and have any difficultiesduring the call, press *0 for assistance.

Mastering SAS 70 AuditReports For ServiceOrganizationsgWebinarJune 16, 2010Mark Agulnik, MarcumRachlinmark.agulnik@marcumrachlin.comScott Price, A-lign CPAsscott.price@aligncpa.comEricEi Wright,W i ht SSchneiderh id DDownsewright@sdcpa.comSteve Thompson,StThSchneiderS h id DDownssthompson@sdcpa.comPowell Jones, Grant Thorntonpowell.jones@gt.com

Today’ss ProgramTodayKey Terms Of SAS 70(Mark Agulnik)Slides 6-30Changing Uses Of SAS 70 ReportsSlides 31-37(Scott Price)A dit Requirements,AuditR it PreparationPti TacticsT tiSlidesSlid 38-5138 51(Eric Wright and Steve Thompson)SSAE 16/ISAE 3402Slides 52-63(Powell Jones)5

Keyy Terms Of SAS 70Mark Agulnik, MarcumRachlin

What Is SAS 70? Statement on Auditing Standards (SAS) No. 70, Service Organizations, is a widelyrecognized auditing standard developed by the American Institute of Certified PublicAccountants (AICPA).(AICPA) It represents that a service organization has been through an in-depth audit of itscontrol objectives and control activities. In today'sy globalgeconomy,y, service organizationsgor service pproviders mustdemonstrate that they have adequate controls and safeguards when they host orprocess data belonging to their customers. SOX has also affected the importance of SAS 70 audit reports, as many serviceorganizations or service providers including data centerscenters, credit car processingcenters and payroll processors host and/or process critical data.SAS 70 does not provide any prescribed guidance regarding scope definition, testingapproach or requirements to establish compliance. The standard leaves theresponsibilityibilit tot theth servicei providerid andd auditordit tot defined fi appropriateness.i tFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN7A Division of Marcum LLP

History Of Internal Control/SAS 70 GuidanceStatementDate IssuedTitle of StatementSAP No. 29October 1958Scope of the Independent Auditor’s Review of Internet ControlSAP No. 41November 1971Reports on Internal ControlSAP NNo. 54NNovemberb 1972Th Auditor’sTheA dit ’ StudySt d andd EvaluationE l ti off InternalI tl ControlC t lSAP No. 3December 1974The Effects of EDP on the Auditor’s Study and Evaluation of Internal ControlSAS No. 44December 1982Special-Purpose Reports on Internal Accounting Control at Service OrganizationsSAS No. 48July 1984The Effects of Computer Processing of the Audit of Financial StatementsSAS NNo. 55A il 1988AprilCConsiderationid tioff InternalI tl ControlC t l ini a FinancialFii l StatementSt tt AuditA ditSAS No. 70April 1992Service OrganizationsSAS No. 78December 1995Consideration of Internal Control in a Financial Statement Audit: An Amendment toStatement on Auditing Standards No. 55SAS No. 88December 1999Service Organizationsgand Reportingpg on ConsistencyySAS No. 94May 2001The Effect of Information Technology on the Auditor’s Consideration of InternalControl in a Financial Statement AuditPCAOB No. 2March 2004An Audit of Internal Control over Financial Reporting in Conjunction with an Auditof Financial Statements. Note: Appendix B refers to Service Organizations.PCAOB No.No 5May 2007An Audit of Internal Control over Financial Reporting that is Integrated with an Auditof Financial Statements. Note: Appendix B17-B27 covers Service Organizationconsiderations.ISAE No. 3402December 2009Assurance Reports on Controls at a Service Organization.SSAE No. 16June 2010Reporting on Controls at a Service OrganizationFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN8A Division of Marcum LLP

Relevant Definitions User organization - The entity that has engaged a serviceorganization and whose financial statements are being audited User auditor - The auditor who reports on the financialstatements of the user organization Service organization - The entity (or segment of an entity) thatprovides services to a user organization that are part of theuser organization's information system Service auditor - The auditor who reports on controls ofa service organization that may be relevant to a userorganization's internal control as it relates to an audit offinancial statementsFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN9A Division of Marcum LLP

Relevant Definitions (Cont.) Report on controls placed in operation (KNOWN AS A SAS 70 TYPE 1) - Aservice auditor's report on a service organization's description of itscontrols that mayy be relevant to a user organization'sginternal controlas it relates to an audit of financial statements, on whether such controlswere suitably designed to achieve specified control objectives, and onwhether they had been placed in operation as of a specific date Report on controls placed in operation and tests of operating effectiveness(KNOWN AS A SAS 70 TYPE 2) - A service auditor's report on a serviceorganization's description of its controls that may be relevant to a userorganization'sorganizations internal control as it relates to an audit of financialstatements, on whether such controls were suitably designed to achievespecified control objectives, on whether they had been placed in operationas of a specific date, and on whether the controls that were tested wereoperatingtiwithith sufficientffi i t effectivenessff titto provideid reasonable,bl butb t nottabsolute, assurance that the related control objectives were achievedduring the period specifiedFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN10A Division of Marcum LLP

Guidance To Service Auditors On Assessing A ServiceOrganization’s Internal Controls And Issuing A Report The service auditor is responsible for the representations in his or her reportand for exercising due care in the application of procedures that supportthose representations. Although a service auditor's engagement differs from an audit of financialstatements conducted in accordance with generally accepted auditingstandards, it should be performed in accordance with the general standardsand with the relevant fieldwork and reporting standards. Although the service auditor should be independent from the serviceorganization, it is not necessary for the service auditor to be independentfrom each user organization. The service auditor may become aware of illegal acts, fraud or uncorrectederrors attributable to the service organization’sorganization s management or employeesthat may affect one or more user organizations. The service auditor errors,fraud and illegal acts are discussed in Sect. 312, Audit Risk and Materialityin Conducting an Audit, and Sect. 317, Illegal Acts by Clients.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN11A Division of Marcum LLP

Guidance To Service Auditors On Assessing ServiceOrganization’s Internal Controls And Issuing A Report (Cont.) No single specific test of controls is always necessary, applicable or equallyeffective in every circumstance and every engagement. Therefore, theauditor should use professional judgment to determine what constitutessufficient appropriate audit evidence under the specific circumstances of theengagement.engagement Meet with management prior to commencement of SAS 70 and determinewho wants the SAS 70 and for what purposepurpose. The SAS 70 only has value ifit is meeting the user’s objectives.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN12A Division of Marcum LLP

Guidance To User Auditors Of Financial Statements ForAn Entity Using One Or More Service Organizations As required by SAS 109, an auditor should obtain anunderstandingdt dioff eachh off theth fivefi componentst off theth entity'stit 'internal control sufficient to assess the risks of materialmisstatement and to design the nature, timing and extentof further audit proceduresprocedures. The auditor should use such knowledge to: A: Identify types of potential misstatements and considerfactors that affect the risks of material misstatements B: Design tests of controls to determine the nature, timingand extent of procedures to be performedFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN13A Division of Marcum LLP

Guidance To User Auditors Of Financial Statements For AnEntity Using One Or More Service Organizations (Cont.) If the user organization significantly uses a service organization, in obtaining anunderstanding of the entity's internal control sufficient to assess the risks of materialmisstatement, the auditor may need to obtain an understanding of the controls of theservice organizationorganization. High degree of interaction: When the user organization initiates transactions and the service organizationexecutes and does the accounting processing of those transactionstransactions, there is ahigh degree of interaction between the activities at the user organization andthose at the service organization. If the user organization implements highly effective internal controls over theprocessingi off transactionsttiatt theth servicei organization,i titheth user auditordit maynot need to gain an understanding of the controls at the service organization inorder to plan the audit. For example, if the user organization has such controls, the userauditordit couldld obtainbt i an understandingd t di off ththe controlst l bby performingfi awalk-through at the user organization.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN14A Division of Marcum LLP

Guidance To User Auditors Of Financial Statements For AnEntity Using One Or More Service Organizations (Cont.) Low degree of interaction: When the service organization initiates, executes and does the accountingpprocessingg of the user organization’sgtransactions,, there is a lower degreegofinteractionbetween the activities at the user organization and those at the serviceorganization. In these circumstances, it may not be practicable for the user organization toimplementeffective controls for those transactions. If the user organization has a low degree of interaction and has not placed into operationeffective internal controls over the activities of the service organization, the userauditorwould most likely need to gain an understanding of the relevant controls at the serviceorganization in order to plan the audit. The understanding can be obtained by: ReviewingR i i a copy off ththe servicei auditor’sdit ’ reportt on theth servicei organization’si ti ’description of its controls, and/or Contacting the service organization to obtain specific information, and/or Visiting the service organization to make inquiries and observations, reviewdocumentation and perform the necessary procedures, and/or Requesting that a service auditor be engaged to perform procedures that willprovide the necessary informationFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN15A Division of Marcum LLP

Guidance To User Auditors Of Financial Statements For AnEntity Using One Or More Service Organizations (Cont.) Information about the nature of the services provided by a serviceorganization that are part of the user organization’s information system,and the service organization’s controls over those services, may beavailable from a wide variety of sourcessources, such as the following: User manualsSystem overviewsT h i l manualsTechnicallThe contract between the user organizationand the service organizationReports by service auditors, internal auditorsor regulatory authorities on the serviceorganization’s controlsIf the user auditor is unable to obtain sufficient audit evidence to achievehi or herhish auditdit objectives,bj titheth user auditordit shouldh ld qualifylif hishi or herhopinion or disclaim an opinion on the financial statements because ofa scope limitation.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN16A Division of Marcum LLP

Guidance To User Auditors Of Financial Statements For AnEntity Using One Or More Service Organizations (Cont.) When the user obtains an understanding of the internal control,including reviewing the user organization’s SAS 70, the user auditor mayidentify certain user organization controls that, if effective, would permit theuser auditor to assess control risk as low or moderate for particular assertionsassertions. Note: Although a type 1 report is sufficient for the user auditor to obtain anunderstanding of the internal control to determine whether the controls aredesigned and implemented, it is not sufficient in assess control risk belowmaximumiiin orderd tto reducedsubstantiveb t ti procedures.d In order for the user auditor to assess risk below maximum (relating to theservice auditors internal controls), the user auditor may: A: Rely on the service auditor’s report on controlsplaced in operation and tests of operating effectiveness(type 2 SAS 70 report) B:B Tests of controls performed byb the userser auditora ditorat the service organization C: Test the user organization’s controls over theactivities of the service organizationgFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN17A Division of Marcum LLP

Guidance To User Auditors Of Financial Statements For AnEntity Using One Or More Service Organizations (Cont.) If the user auditor decides to use a service auditor’s report, the user auditorshould consider the extent of the evidence provided by the report about theeffectiveness of controls intended to prevent or detect material misstatementsin the particular assertions. A user auditor should determine whether the specific tests of controls andresults in the service auditor’sauditor s report are relevant to assertions that aresignificant in the user organization’s financial statements. The user auditor remains responsible for evaluating the evidence presented bythe service auditor and for determining its effect on the assessment of controlrisk at the user organization. In evaluating these factors, user auditors shouldalso keep in mind that, for certain assertions, the shorter the period covered bya specific test and the longer the time elapsed since the performance of the test,the less support for control risk reduction the test may provideprovide.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN18A Division of Marcum LLP

Guidance To User Auditors Of Financial Statements For AnEntity Using One Or More Service Organizations (Cont.) In considering whether the service auditor’s report is satisfactoryfor his or her purposes, the user auditor should make inquiriesconcerning the service auditor'sauditor s professional reputation. Appropriatesources of information concerning the professional reputation of theservice auditor are discussed in Sect. 543, Part of Audit Performedby Other Independent Auditors. When assessing a service organization’s controls and how theyinteract with a user organization's controls, the user auditor maybecome aware of the existence of significant deficiencies or materialweaknesses in internal control. In such circumstances, the user auditorshould consider the guidance provided in Sect. 325, CommunicatingInternal Control Related Matters Identified in an Audit (SAS 112/115).FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN19A Division of Marcum LLP

Type 1 - Reports On Controls Placed In OperationNote: The following apply to both type 1 and type 2 reports The information necessary for a report on controlsplaced in operation ordinarily is obtained throughdiscussions with appropriate service organizationpersonnell andd throughthh referenceftot variousiformsfof documentation, such as system flowchartsand narratives. The description should contain a discussion of thefeatures of the service organization’s controls thatwould have an effect on a user organization'sginternal control.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN20A Division of Marcum LLP

Type 1 - Reports On Controls Placed In Operation (Cont.) They may include controls within the control environment,risk assessment, control activities, information andcommunication and monitoring components of internal control.communication,control The control environment may include hiring practices andkey areas of authority and responsibility. Risk assessment may include the identification of risksassociated with processing specific transactions. Control activities may include policies and procedures overthe modification of computer programs, and are ordinarilydesigned to meet specific control objectives. Information and communication may include ways in whichuser transactions are initiated and processed. Monitoring may include the involvement of internal auditors,audit committeecommittee, etcetc.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN21A Division of Marcum LLP

Type 1 - Reports On Controls Placed In Operation (Cont.) Although a service auditor’s report on controls placed in operation isas of a specified date, the service auditor should inquire aboutchanges in the service organization’sorganization s controls that may have occurredbefore the beginning of fieldwork. If the service auditor believes that the changes would be consideredsignificantgbyy user organizationsgand their auditors,, those changesg shouldbe included in the description of the service organization’s controls. If the service auditor concludes that the changes would be consideredsignificant by user organizations and their auditors, and the changes arenot included in the description of the service organization’sorganization s controls,controls thenthe service auditor should describe the changes in his or her report. Suchchanges include: Procedural changes made to accommodate provisions of a newStatement of Financial Accounting Standards Major changes in an application to permit online processing Procedural changes to eliminate previously identified deficienciesFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN22A Division of Marcum LLP

Type 1 - Reports On Controls Placed In Operation (Cont.) Changes that occurred more than 12 months before thedate being reported on normally would not be considered significant,because they generally would not affect user auditorsauditors’ considerations. The description of controls and control objectives required for thesereports may be prepared by the service organization. If the serviceauditor prepares the description of controls and control objectives,objectivesthe representations in the description remain the responsibility of theservice organization. A service auditor’s report expressing an opinion on a description offcontrols placed in operation at a service organization should contain: A: A specific reference to the applications, services, products orotherth aspectst off theth servicei organizationi ti covered.d B: A description of the scope and nature of the serviceauditor’s procedures.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN23A Division of Marcum LLP

Type 1 - Reports On Controls Placed In Operation (Cont.) C: Identification of the party specifying the control objectives D: An indication that the purpose of the service auditor’s engagementwas to obtain reasonable assurance about whether (1) the serviceorganization’s description presents fairly, in all material respects, theaspects of the service organization's controls that may be relevant toa user organization’s internal control as it relates to an audit offinancial statements; (2) the controls were suitably designed toachieve specified control objectives; and (3) such controls had beenplaced in operation as of a specific date. E: A disclaimer of opinion on the operating effectiveness of the controls F: The service auditor’s opinion on whether the description presents fairly,in all material respects, the relevant aspects of the service organization’scontrols that had been placed in operation as of a specific date andwhether, in the service auditor's opinion, the controls were suitablydesigned to provide reasonable assurance that the specified controlobjectives would be achieved if those controls were complied withsatisfactorilyFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN24A Division of Marcum LLP

Type 1 - Reports On Controls Placed In Operation (Cont.) G: A statement of the inherent limitations of the potential effectiveness ofcontrols at the service organization and of the risk of projecting to futureperiods any evaluation of the description H: Identification of the parties for whom the report is intended If the service auditor believes that the description is inaccurate oriinsufficientlyffi i tl completel t ffor user auditors,ditthenth theth servicei auditor’sdit ’report should so state and should contain sufficient detail to provideuser auditors with an appropriate understanding. If there are significant deficiencies in the design or operation of theservice organization’s controls that preclude the service auditor fromobtaining reasonable assurance that specified control objectiveswould be achieved,achieved then the report should be modified.modifiedFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN25A Division of Marcum LLP

Type 1- Reports On Controls Placed In Operation (Cont.) In our opinion, except for the matter referred to in the preceding paragraph,the accompanying description of the aforementioned application presentsfairly, in all material respects, the relevant aspects of XYZ ServiceOOrganization’si ti ’ controlst l ththatt hadh dbbeen placedld iin operationti as off [i[inserttdate].For the service auditor to expresspan opinionpon whether the controlswere suitably designed to achieve the specified control objectives,it is necessary that: A: The service organization identify and appropriately describesuch control objectives and the relevant controls B: The service auditor consider the linkage of the controls tothe stated control objectives C: The service auditor obtain sufficient appropriate auditevidence to reach an opinionFLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN26A Division of Marcum LLP

Type 2 - Reports On Controls Placed In OperationAnd Tests Of Operating EffectivenessIn addition to the requirements of type 1, there are additional requirementsto type 2 Similarto type 1,1 the information necessary for a report on controlsplaced in operation ordinarily is obtained through discussions withappropriate service organization personnel and through reference tovarious forms of documentation, such as system flowcharts andnarratives. However with a type 2, the service auditor mustperform tests of controls. Theservice auditor applies tests of controls to determine whetherspecific controls are operating with sufficient effectiveness toachieve specified control objectives. Sect. 350, Audit Sampling,as amended, provides guidance on the application and evaluationof audit sampling in performing tests of controls.FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN27A Division of Marcum LLP

Type 2 - Reports On Controls Placed In OperationAnd Tests Of Operating Effectiveness (Cont.) A service auditor’s report expressing an opinion on a description ofcontrols placed in operation at a service organization and tests ofoperating effectiveness should contain: A: A specific reference to the applications, services, products or otherof the service organization covered [same as type 1] B: A description of the scope and nature of the service auditor’sprocedures [same as type 1] C: Identification of the party specifying the control objectives[same as type 1] D: An indication that the purpose of the service auditor’s engagementwas to obtain reasonable assurance about whether (1) the serviceorganization’s description presents fairly, in all material respects, the aspectsof the service organization’s controls that may be relevant to auserorganization’s internal control as it relates to an audit of financialstatements; (2) the controls were suitably designed to achieve specifiedcontrol objectives; and (3) such controls had been placed in operationas of a specific date [same as type 1]FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE aspectsGRAND CAYM AN28A Division of Marcum LLP

Type 2 - Reports On Controls Placed In OperationAnd Tests Of Operating Effectiveness (Cont.) E: The service auditor’s opinion on whether the description presents fairly, inall material respects, the relevant aspects of the service organization’scontrols that had been placed in operation as of a specific date and whether,in the service auditor’sauditor s opinionopinion, the controls were suitably designed toprovide reasonable assurance that the specified control objectives would beachieved if those controls were complied with satisfactorily [same as type 1] F: A reference to a description of tests of specific service organizationcontrols designed to obtain evidence about the operatingeffectiveness of those controls in achieving specified controlobjectives. The description should include the controls that weretested,, the control objectivesjthe controls were intended to achieve,,the tests applied, and the results of the tests. The description shouldinclude an indication of the nature, timing and extent of the tests, aswell as sufficient detail to enable user auditors to determine the effectof such tests on user auditors'auditors assessments of control risk. To theextent that the service auditor identified causative factors forexceptions, determined the current status of corrective actions, orobtained other relevant qualitative information about exceptionsnoted such information should be provided [only type 2].noted,2]FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN29A Division of Marcum LLP

Type 2 - Reports On Controls Placed In OperationAnd Tests Of Operating Effectiveness (Cont.) K: A statement that the service auditor has performed no procedures toevaluate the effectiveness of controls at individual user organizations[ l type[onlyt2] L: A statement of the inherent limitations of the potential effectiveness ofcontrols at the service organization and of the risk of projecting to thefuture any evaluation of the description or any conclusions about theeffectiveness of controls in achieving control objectives[same as type 1] M: Identification of the parties for whom the report is intended[same as type 1]FLORIDAPII OPAASS SS NEWO NNYORK NEWY I TCONNECTICUTPENNEEENCEI N JERSET E G RYE XX CCE LL SLLYLE VAN NICAE GRAND CAYM AN30A Division of Marcum LLP

Changing Uses Of SAS 70RReportstScott Price, AA-lignlign CPAs

Original Uses Of SAS 70 Reports Communicate operational controls to comply with SAS 55 Communicate controls and control testing results needed for userorganization financial statement audit purposes CommunicateCi t controlst l andd controlt l testingt ti resultslt tot companymanagement and Board of Directors32

Evolution Of SAS 70 Report Uses Comply with contractual obligations Comply with regulatory requirements– HIPAA– Gramm-Leach-Bliley– FFIEC– FDIC33

Evolution Of SAS 70 Report Uses(Cont.) Communicate business continuity/disaster recovery controls–

What Is SAS 70? Statement on Auditing Standards (SAS) No. 70, Service Organizations, is a widely recognized auditing standard developed by the American Institute of Certified Public Accountants (AICPA)Accountants (AICPA). It represents that a service organizationhas been through an in-depth audit of its control objectives and control activities.