Transcription

MFR PAPER 1318An Analysis of the Charter BoatFishing Industry on theTexas Gulf CoastROBERT B. DITTON, RICHARD N. JARMAN,and STEVE A. WOODSABSTRACT-This paper examines the nature, extent, and characteristics of theTexas Gulf Coast charter boat fishing industry and its implications for fisheriesmanagement. Personal interviews were completed with 41 of the 88 Texas GulfCoast charter operators in business during 1975. Data were obtained regardingcharter operators: Characteristics, business structure, charter fishing activities,and economic returns. This study revealed that the Texas charter industry lacks aformal industry organization, is compose a of small independent businesses whichyield insufficient incomes to keep operators in business full time, involves operatorswho are primarily con cered with the life-style afforded by charter fishing, and is anintegral part of the State's tourism industry.INTRODUCTIONAssessing the varied demandson marine fisheries resources is oneof the most difficult tasks confronting fisheries managers. Historically,emphasis has been placed on the commercial use of fisheries resources. As aresult, much of the available data concerning the biological, economic, andsocial impacts of fisheries utilizationpertain to commercial fishing industries. In recent years, however, increased recognition has been given tothe impacts of marine recreationalfishing. Deuel (1973) has pointed outthat in terms of the number of saltwatersport fishermen and the size of the rec-Robert B. Ditton, Richard N. Jarman,and Steve A. Woods are with theRecreation and Parks Department,Texas A&M University, College Station, TX 77843. This research wassupported by the Texas AgriculturalExperiment Station and the TexasA&M Sea Grant Program.Augusl /978reational catch, marine recreationalfishing can no longer be considered aninconsequential use of the nation'sfisheries resources.The economic impact of marine recreational fishing has also reached substantial proportions. The total retailsales of goods and services associatedwith marine recreational fishing wereestimated to be 1 ,333 million in 1972.These sales generated an estimated 510 million of value added and 285million in wages and salaries in business sectors where direct spending tookplace. In 1975 sport fishing consumerspurchased an estimated 1,840 millionworth of goods and services at the retaillevel. These sales generated approximately 699 million of value added and 343 million in related wages andsalaries (Centaur Management Consultants,Inc. I ).'Centaur Management Consultants, Inc. 1977.Economic activity associated with marine recreational fishing. Draft repon. Centaur Management Consultants, Inc., Washington, D.C.Aside from national and regionaltrends and averages of sport fishing activity and expenditures, however,decision-makers often lack sufficientinformation, particularly in state andlocal situations, for considering the impacts of recreational fishing in the development of marine fisheries management policies and regulations.Popular arguments contrasting recreational and commercial fishing oftenportray both fisheries as big business.Recreational fishing is characterized asa social luxury associated with fisheriesconservation, while commercial fishingis characterized as an economic necessity associated with fisheries exploitation (Carlton, 1975). Generalizedstatements concerning either' recreational or commercial fishing, however, provide a weak base for makingfisheries resource allocation and management decisions. If fisheries management is to reflect economic, social,and resource concerns as directed bythe U.S. Fisheries Conservation andManagement Act of 1976 (Public Law94-265), research is needed to developa comprehensive data base for evaluating both commercial and recreationaldemands.Although recreational fishing is oftenviewed as a homogeneous activity, anumber of distinct components orfishing sectors can be identified. Alongthe Texas Gulf Coast recreationalfishing can be grouped into three broadtypes: Onshore' or nearshore fishing,bay fishing, and offshore or Gulffishing. This paper is concerned with anindustry which provides a means forbay and Gulf fishing: the Texas charterfishing industry.In 1970, an estimated 15 percent ofthe sport fishermen in the entire GulfRegion used a charter or party boat atleast once, spending over 20 million incharter fees alone (Bureau of SportFisheries and Wildlife, 1972). Severalarea-specific studies indicated charteroperations can have substantialeconomic impact on local communitiesand contribute substantially to the totalrecreational economy in an area. In astudy of the Wisconsin charter fishingindustry, Ditton et al. (1975) found

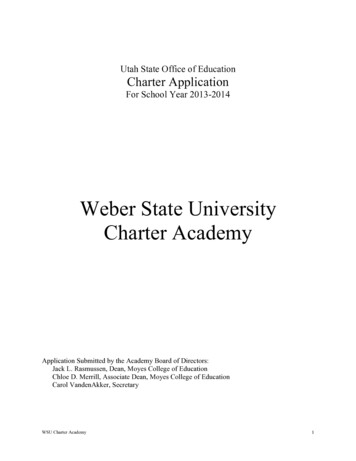

and discusses possible managementimplications.METHODSLOCATION t.eA; South Padre (7) 10Figure I.-Regional dislribution of Texas Gulf coast charter businesses operaling in 1975:Sample and size population.charter businesses had a sizableeconomic impact on shoreline .communities with a total statewideeconomic impact of approximately 4million. In Choctawatchee Bay, Fla.,and its adjacent Gulf of Mexico waters,charter and party boat fishing accountedfor 69 percent of the sport fishing effortand 75 percent of the sport fishi ng catchduring approximately a I-year period(Irby, 1974).During the summer of 1974, an extensive literature review and interviewswith representatives from various government agencies and private organizations familiar with saltwater sport2fishing in Texas revealed an absence ofinformation concerning the Texas GulfCoast charter industry (Ditton and Jarman 2 ). Even the basic parameters of theTexas charter fishing industry, such asthe number and location of charter operations, had not been identified. Thispaper presents the findings of a studyconducted to identify and to understandthe Texas charter boat fishing industry'Dillon, R. B., and R. Jarman. 1974. Development of a sport fishing focus in the TAMU SeaGrant Program - a program slatement. Proposalprepared for the Texas A&M Sea Granl Program,College Slation, 46 p.An inventory of Texas charter boatfishing businesses was compiled fromU.S. Coast Guard vessel documentation records, consultation with areamarine extension agents, local chambers of commerce, marina operators,telephone books, newspapers, andpromotional literature obtained fromcoastal communities. Owners of Texascoastal charter fishing businesses in operation during all of 1975 were contacted. Operators who had retired fromcharter fishing before 1975 or hadbegun charter fishing during 1975 wereexcluded. A study population of 88businesses was identified.Based on the geographic distributionof the 88 businesses, the Texas coastwas divided into five regions. A 50 percent random sample of the businesses ineach region was drawn. During the datacollection period from March throughMay 1976, efforts were made to contactthe charter boat owners to schedule aninterview. If an interview could not bescheduled after four attempts, the operator's name was removed from thesample and another one was randomlyselected. Using a structured interviewschedule adapted from that used by Ditton et al. (1975),41 personal interviewswere completed. Figure I shows thedistribution of the 88 business operating during 1975 and the number of interviews (in parentheses) completed ineach region. Data were collected to describe charter operators, their activities, resources, business structure,business revenue, and expenditures.FINDINGSIndustry OrganizationResponses to questions concerningmembership in state or local chapterfishing organizations revealed that theTexas charter fishing industry is notformally structured. No respondentsreported membership in or awarenessofa statewide charter fishing association. Only one local charter organiza-Marine Fisheres Review

tion, the Port Aransas Boatman's Association, was identified. Eighty-twopercent of the operators interviewed inthe Port Aransas area belonged to theassociation. Several of its members indicated a decline in recent years in theeffectiveness of the association as astandard setting and enforcing entity.Only 27 percent of the operators belonged to local chambers of commerce.When asked what services were provided, 64 percent of the operators belonging to a chamber of commerce saidthey were mentioned in brochures and36 percent said they received referrals.Eighteen percent of those operators belonging to a chamber of commerce reported they received no support.Although little formal organizationwas found, there appears to be a substantial degree of informal inter- andintra-industry organization. Sixty-eightpercent of the operators reported otherlocal charter operators and businessesreferred customers to them, and 66 percent said they referred customers toother local operators and businesses.Twenty-five percent reported payingcommissions for booking, but none reported receiving commissions for referrals.The Texas CharterBoat OperatorThe majority of charter operators interviewed engaged in charter fishing ona part-time basis. Twenty-seven of the41 fishermen were employed in otheroccupations either concurrently or during part of the year. Fourteen fishermensaid charter fishing was currently theironly occupation. Of the 14, II wereretired from other occupations, one hadmade a career of charter fishing and twowere unemployed and looking forwork. Present and past occupations ofthe charter operators included: Civilservant, auto mechanic, police officer,dentist, oil executive, motel owner,musician, military officer, and commercial fisherman. Only one said hehad been involved with charter fishingduring his entire working career.Thirty-nine charter operators responded to the question, "What percent of your income is derived fromAugusl /978charter fishing?" Charter fishing income averaged 41 .3 percent of the totalincome of the responding operatorswhile charter fishing accounted for anaverage of 61 .5 percent of the workingtime of the 41 operators interviewed.Although there appears to be a substantial difference between the percentageof total income derived from charterfishing compared to the percentage oftotal working time devoted to charterfishing, the difference is due primarilyto the number of operators who wereretired from other occupations. Adjusting for the operators who were retiredfrom other occupations results in an average of 39.8 percent of the operators'total income attributable to charterfishing and an average of 41.9 percentof working time.Although the discrepancy betweenthe amount of income and the amountof working time may suggest the respondents are not following soundbusiness procedures, the majority saidthey had not entered the charter fishingbusiness for economic reasons. Whenrespondents were asked what led themto become charter operators, only IOpercent said money was the mainreason. Thirty-seven percent of the respondents referred to their enjoymentof fishing; 24 percent said their charterfishing business began as a hobby; andthe remaining 29 percent referred to theopportunity to live in a particular community, the enjoyment of boating, andthe involvement of friends or relativeswith charter fishing. Most of thereasons given were noneconomic.Many respondents volunteered thatmonetary returns of operating a charterboat were often a discouraging ratherthan an encouraging aspect of the business.Respondents reported operating acharter fishing business on the Texascoast for an average of 11.5 years. Thiscontrasts sharply with studies of othercharter fishing industries. Wisconsin(Lake Michigan) charter operators hadbeen in business an average of only 3.8years (Ditton et aI., 1975) and morethan half of the Georgia (Atlantic) charter operators had been in business lessthan 3 years (Brown and Holemo,1975). The relatively long history of therespondents' charter fishing involvement suggests charter fishing is awell-established industry on the Texascoast. Also the length of time the respondents operated a charter businessindicates they are experienced charteroperators and have apparently receivedsufficient economic and noneconomicbenefits to remain in business.The charter operators have operatedfrom their current home port for an average of 10.5 years. The respondentssaid they do not shift ports in responseto fish migrations or seasonal weatherchanges. Only one operator reportedregularly changing ports during theyear in response to customer demand.Business CharacteristicsOf the 41 businesses surveyed, 34were single proprietorships, 4 werepartnerships, and 3 were corporations.Thirty-five of the businesses had onlyone vessel, three businesses had twovessels, and three businesses had threevessels-making a 50-boat charterfishing fleet.The average length of the vessels is30.6 feet with an average gross weightof 8.6 tons. Respondents estimated thecurrent market value of their vessels atan average (single vessel) value of 16,826. The majority of the vesselswere equipped with a fathometer (78percent) and a VHF or CB radio (96percent). Twenty-eight percent of thevessels were equipped with a fish finderand 28 percent with loran. Only fourpercent had no electronic equipment.Even though many of the vessels hadsome electronic equipment for selecting a fishing site, the majority of theoperators said the equipment was usedinfrequently. Experience was reportedas the key factor in selected fishingsites.There are numerous differences invessel length, boat market value, andparty size when charter operations areviewed on the basis of where they usually take people fishing: bay only, Gulfonly, and a bay/Gulf combination. Bayboats averaged 24 feet in length, had anet boat value of 9,265, and generally3

0100::E"'Cl:IIIEQ)-9093% , . - - 89%C Q)E80.--01;;:s79%c. 70 F.60i550IIII IIl:0::El:Q) (3'"l:.;:;III"'ii40.--r---3032%32%.: g 20 Q)a.010'0*'4%JANFEBMARAPRMAYJUNJULAUGSEPT OCTI4%NOVIDECFigure 2.-DiSITibution of respondents by reponed "best" CUStomer demand months.carried 3-4 customers. Gulf boats averaged 34 feet in length, had a net boatvalue of 22,232, and generally carried4-6 customers. Boats used for fishingboth bay and Gulf were more like bayboats with an average length of 27 feetand a net boat value of 10,331. Thirtyof the vessels were each operated by acaptain and one crew member (generally Gulf boats), and 20 vessels wereeach operated with only a captain (generally bay boats).Charter Fishing ActivitiesThe price of a charter fishing tripvaried considerably among the 41businesses represented in the study.The factors influencing the price structure were: Number of fishermen in aparty, type of vessel, length (in hours)of a trip, and the type of trip (either bayor Gulf fishing). Assuming a four person party, the charter fee ranged fromapproximately 25 to 75 per personwith Gulf charters the most costly. Theprice of a charter trip is intended to4cover the use of the charter vessel andthe experience of the vessel's captain.For the majority of the businesses, theowner was also the captain. The feealso included fishing instructions. Sixtypercent of the respondents reported thebase rate included the provision of bait,and 56 percent reported the provision oftackle.Sixty-three percent of the respondents said their vessels were availablefor charter all year. However, Maythrough September were the months ofhighest demand with July the bestmonth (Fig. 2). The charter operators'season or period of greatest activity corresponds roughly with the ending andbeginning of the school year.Surprisingly few operators used theirvessels for activities such as scuba charters, carrying oil rig crews, or privateuse to increase their earnings.The 41 respondents reported providing charter services to 16,648 fishermen in 1975. If each of the 50 vesselsowned by the respondents was usedequally, the average number of fishermen carried during 1975 would be 333per boat. However, three of the ownersof multiple boat businesses did not havea captain for each vessel. At anyonetime, only 46 charter vessels could beused. Based on the total of 46 vesselscapable of being used, the averagenumber of fishermen carried during1975 increases to 362 per boat. Although many of the charter vessels werelicensed to carry a maximum of six passengers plus the captain and crewmember, operators indicated an average of four fishermen were carried oneach charter.As discussed, the respondents provided charter service to both bay andGulf waters. To obtain informationwhich may aid in the siting of artificialreefs, operators were asked to indicatethe average one-way distances traveledduring a bay and Gulf charter. Theone-way distance traveled to a fishingsite in bay waters ranged from 4 to 26miles with over 50 percent of theoperators traveling less than 10 miles.For Gulf fishing, the one-way distancetraveled ranged from 5 to 50 miles withover 50 percent of the operators traveling less than 20 miles. Based on thenumber of charters in bay and Gulf waters, 24 percent of the operators chartered primarily to bay waters, 56 percent chartered primarily to Gulf waters,and 20 percent chartered approximatelyequally to bay and Gulf waters.Respondents were asked to identifythe principal target species of their charter fishing efforts (Table I). FewTable 1.-"Primary speciessought" as reported Spotted seatroutRed drumLingRed ine Fisheries Review

operators reported only one targetspecies. Freeport, Tex., operatorsfished primarily for king mackerel,Scomheromorus caval/a, from May toSeptember and red snapper, Lutjanuscampec'hanus, during the remainingmonths. The Rockport and PortO'Connor, Tex., operators fishedprimarily for spotted seat rout , Cynoscion nebulosus, and red drum,Sciaenops ocel/ata. Port Aransas operators fishered for king mackerel, Scomberomorus caval/a, with some spottedseatrout and red snapper, Lutjanuscampec'hanus, fishing in the spring,fall, and winter months. Charter operators in the South Padre region fished fora variety of species including red drum,spotted seatrout, tarpon, Megalops atlantica, sailfish, lstiophorus platypterus, red snapper, and grouper,Epinephelus spp., and Mycteropercaspp.Charter FishingFinancial InformationData were obtained on the fixed andvariable expenses associated with theoperation of charter vessels during1975. For multiple businesses, expensedata was obtained for each vessel. Acomprehensive cost accounting formwas used to insure the identification ofthe expenses incurred during 1975 withthe exception of interest payments andincome taxes. A revenue total for eachvessel was calculated based on thenumber and type of fishing trips takenduring 1975 and the cost of these tripsbased on the average number of customers each operator took fishing.For the purposes of the financialanalysis, three multiple-boat businesses which involved the use of only oneboat at a time were considered singlevessel operations. In these three cases,all revenue and expenditures associatedwith each vessel were attributed to asingle hypothetical vessel. In essence,the revenues and costs incurred by thesebusinesses were simi lar to the revenuesand costs incurred by a single boatbusiness. The per boat economicanalysis was therefore based on 46rather than 50 boats.Based on these 46 vessels, the aver-Augusl /978Table 2.-Pretax profitability per boaI (n 46) in dollars.D'ESTOlaldivided byno. ofrespondentsC'No. ofrespondentsdivided bytotal no.of boatsTotaldivided bytotal no.of boats'% of expo 621.169.00 13.503.6746/46 13.503.67 0 29/4628/4639/465,466/4618/46 A'B2Tolal reported Dock leesOffice rentLocal RepairsFuelWagesBaitTackleIceOlherTolalTotal expensesNel profit (loss) before875.4120682634.3656000252502.464.67 2,273.85 4.993.76 .004,795.007,835.00 623/4625/4632/4621/466/46 33 9.35074 14,344.50 5,425.37 7.699.22(840.83) 5.804.45interest and taxestolalexpo Incol. -70.4'Column A is the sum of all responses lor each item.2Column B is the total amount tor a given item (Column A) divided by the number of boats incurring that expense(numeralor 01 Column C).'Column C is Ihe number of boals incurring an expense divided by the lolal number of boals. For example, the totalinsurance expense incurred by all operators was 525.387. Twenty-nine of Ihe forty· six boats. 65.2 percent. incurredan insurance expense. The average premium lor Ihe twenly-nine boats was 525.387129 or 875.41.'Multipiying Column B by Column C gives Column D, Ihe TOlal Expenditure Iigure divided by Ihe lotal number ofboats. SUbtracting the expenses from the income in Column 0 gives the average net pretax and interest profit perboat.5Co!umn E shows the percentage an expense item is to the tOlal expenses. This column should be viewed cautiouslybecause charter operators simply approach their business differently. Several operalors paid their dockage lees on acommission basis. Others paid higher dock 'ees but received free bookings, bait. and/or ice. Some value judgmentswere necessary 10 delermine which category best fil the expense figure given by the operalor.age profit in 1975 was 5,804 per boat(Column D, Table 2). This representsthe average net profit before any interest payments and income taxes. Variable expenses (repairs, fuel, wages,bait, and tackle) accounted for approximately 70 percent of the total expensesassociated with the operation of a TexasGu If Coast charter boat in 1975. If theowner of a hypothetical average chartervessel had incurred the average of eachof the expenses reported, he wouldhave lost 840.84 in 1975 (Column B,Table 2).More detail on the profitability ofoperating a charter fishing vessel isshown in Table 3 where the net profitsassociated with vessels used for bayfishing, Gulf fishing, and a combinationof bay/Gulf fishing are compared. In1975, the 10 vessels used primarily forbay fishing returned an average netprofit of 5,137 per boat; the 28 Gulfvessels average a net profit of 4,265per boat: and the eight vessels used forboth bay and Gulf fishing averaged anet profit of 12.3 17 per boat. Usingthe reported value of the charter vesselsas a measure of the initial investmentneeded to begin a gi ven type of charteroperation. the initial investment isgreatest for Gulf-only operations followed by combination bay/Gulf operations and bay-only operations.DISCUSSIONThis paper provides a perspective onthe dynamics' of the Texas charterfishing industry which should be usefulto fisheries managers. If the Gulf Regional Fishery Management Councilidentifies charter fishing as a managerially important fishery, an understanding of the nature and characteristics of5

the charter industry throughout the Gulfregion will be necessary to determine ifand how particular fisheries resourceswill be allocated to this fishing sector.Regional differences in charterfishing catch and effort may require thatmeasures like catch quotas or seasonlimits (if considered at all) be specifically designed for particular areas orStates within the region. Different solutions may be needed because Texasand Florida charter industries, forexample, may be different in terms ofthe scale of the businesses involved,operating season, and the magnitudeand composition of catch.Practically no information is available on the size and composition of theTexas charter fishing catch. Although acreel survey has been conducted in several Texas bay systems (Heffernan etal., 1976), data specific to charter boatshave been collected at only one location, and no catch data have been collected for offshore Gulf charter fishing.Identification of the charter fishingcatch, however, is important to determine if catch limits are necessary. Besides harvest concerns, the FisheryConservation and Management Act directs the Regional Councils to considereconomic and social matters.This study indicates that the Texascharter fishing industry is made up ofsmall independent businesses whichoperate at moderate to high profit margins but which do not yield sufficientcash to keep a large number ofoperators in business full time. Thismay be due in part to the relatively shortcharter fishing season, as determinedby customer demand for charter fishingon the Texas coast. Although the industry lacks formal organization at theState and local level, there is a substantial degree of informal organization inlocal communities as evidenced by customer referrals among operators and related businesses. It appears that theTexas charter industry has developedmore as a result of the life style whichcharter fishing affords than solely out ofany monetary benefits which may accrue to its members.Although the exact relationship of6Table 3.-Comparative financial data by type of charterfishing operator.how the charter fishing industry shouldbe viewed in the context of fisheriescombinamanagemenl. Should charter fishing beBayGulftiononlyitemonlymanaged as a commercial or recre10288No. of boatsational fishing industry? Since the 17.198.13Income 8.454.60 14.251.46Texas charter boat operators receiveeconomic benefits from the utilizationE)(pensesFixedof common property fisheries re757.32210.00Insurance130.20sources, the industry may be, and often148.21153.31Advenising41.50574.21661.25Dock fees270.40is in many areas, viewed as a form of98.21Ottice rent5.00000Local taxes102.5014.826.25commercial fishing, However, theDepreciation662001.240.86375.00methods and techniques of charterTotal 1.211.60 2.83363 1.405.81fishing are indistinguishable from thoseVariableof the recreational fisherman who isCommisable to purchase and use his own vessel.sions xas charter fishing industry 00therefore be viewed as a recreationalBait515.39109.5060625service industry which 0fishermen with a means of access (for a278.573.500.00Olherfee) to fisheries resources. 2,105.80 7.152.74 3.475.13TotalHow the charter fishing industry isTotal (all ex 3,317.40 9,98637 4,880.94penses)regulated may have a direct influenceNet profitbefore interon the industry's viability. It is difficultest and taxes 5.137.20 4.265.09 12.317.19to determine what the impact of catchTotalquotas and other regulations would beboat value 9,555.00 25,554.00 11.112.00on the industry. Since the economic115.7068.00134.12TripsPretax proviability of the industry is partially refit' marginlated to customer demand, the imposiper trip104.39102.3254.87Trips requirtion of quotas on the number, size, ored to' break14even per year2228species of fish which may be taken mayCash flowor may not act to discourage this deper year:) 5,799.20 5,505.95 12,692.19mand. Other management measures, Income-tolal vanable expensestripssuch as designating a charter fishingseason or controlling the number ofFixed expensesPretax profit margin per triPcharters an operator can take are moreeasily related to the industry's viability.JNet profit before interest and taxes plus depreciation.For example, the Texas charter fishingseason was found to be essentially 5months when charter businesses recei ved the bul k of their revenue. Reducing the season or the number of charterscharter fishing and coastal tourism was an operator could take by regulationnot specifically determined in this could be critical to some operators. Thestudy, the degree of informal cooperamarginal operators would be unable totion between the charter industry and compete and would be forced out of theother tourism elements like hotels, resindustry. Although charter operatorstaurants, and sport shops suggests theindicated monetary benefits were not acharter industry is an integral part of primary motive for their involvement incoastal tourism, particularly in small the industry, it is unlikely that mostcommunities.would continue to operate if confrontedStudy findings suggest several points with no chance of economic gain orwhich will require consideration in the certain economic loss.formulation of any management regulaAnother important factor is the magtions for the Texas charter fishing innitude of the variable operating exdustry. There is the basic question of penses. As noted, approximately 70Bay/GulfMarine Fisheries Review

percent of the operating expenses incurred by respondents during 1975 werevariable costs. Rising fuel costs combined with a limited season again willsurely force some operators out of business. This will reduce the economicbenefits which accrue to local communities as a result of charter operations.This study also points to the need fora mechanism for monitoring changes inthe size and distribution of the Texascharter boat fishing industry. Due to theabsence of a continuous licensing orregistration system to identify membersof the Texas charter fishing industry,this study was limited to a single studyyear. To consider the continuing impacts of the charter industry, it is i mportant that managers be able to identifywhether the industry is growing or declining by location. This could be easilyachieved by altering the current Texasguide license so that charter fishingoperators could be differentiated fromthe variety of activities presently covered by the gu ide license.ACKNOWLEDG MENTSThis research was supported by theTexas Agriculture Experiment Stationand the Texas A&M Sea Grant Program.LITERATURE CITEDBrown. E. E . and F. J. Holemo. 1975. Aneconomic analysis of Georgia's marine charterboat lishing industry. Mar. Fish. Rev.37(4): 11-1

Texas Gulf Coast charter boat fishing industry and its implications for fisheries management. Personal interviews were completed with 41 of the 88 Texas Gulf Coast charter operators in business during 1975. Data were obtained regarding charter operators: Characteristics, business structure, charter fishing activities, andeconomic returns.