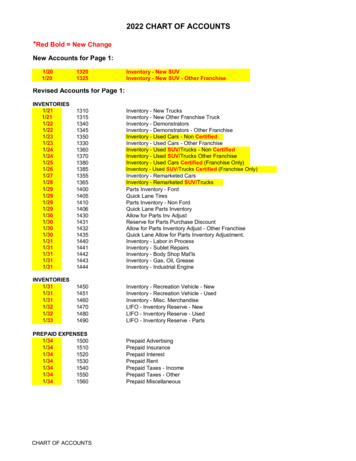

Transcription

Futureof RetailBankingKPMG Connected Enterprisefor Retail BankingJanuary 2021home.kpmg/ae/forb2020Future of Retail Banking

ForewordAs the industry adjusts to the effects of Covid-19 and looks towards the future,the retail banking landscape has undergone considerable transformation. Banksmust negotiate a multitude of shifting factors — from changing customerbehavior to economic headwinds, intensifying competition, regulatory pressureand technological disruption.But while there are challenges, change also brings opportunity. Banks that candrive a differentiated proposition—putting the customer experience at the heartof everything they do and connecting it across the enterprise—have thepotential to secure a significant competitive advantage.G oncalo T raquinaPartner, Digital and InnovationKPMG Lower GulfE: gtraquina@kpmg.comAbbas BasraiPartner Head of Financial ServicesKPMG Lower GulfE : abasrai1@kpmg.co.ukIt is this notion of becoming a Connected Enterprise that we explore in thisreport, setting out the hallmarks of the future of retail banking and how this maymanifest itself across what we believe will be the three dominant bankingmodels in the new reality.The trends we discuss are not new in most markets, including in the UAE, butthey have been significantly intensified by Covid-19. Banks in the region havealready been investing significant sums in AI and new technologies to improvethe customer experience, as our recent KPMG UAE Customer ExperienceExcellence Research 2020 shows. A growing number of disruptors, includingfintech firms and tech titans, have been raising the bar for customers’experience and expectation and we see this intensifying in the near future withthe plethora of neobanks entering the market. Neobanks are direct banks thatoperate exclusively online without traditional physical branches.Now though, the stakes are higher. We found that globally, as well as in theUAE, a significant gap has already opened up between leading customer-centricbanks who demonstrate strength across a range of capabilities critical forenabling digital transformation against their peers. Our research indicates thisgap in capability may widen further, and more dramatically, due to theacceleration of changes brought on by the Covid-19 crisis.To be successful, UAE organizations would do well to recognize that solutionsand architectures will require more focus, flexibility and finesse than simplybolting on new pieces of technology. Prioritization of effort in certain areas willmake a difference, including designing optimal experiences for customers,putting innovation at the heart of product development and servicing, andcreating an ecosystem of partners that can be used to accelerate solutions andincrease agility.Becoming a connected bank takes commitment and determination. Achieving ithas become more important than ever; it is the key to providing consumers withthe enhanced customer experience that is fundamental to future success.Ankit UppalDirector, Digital and InnovationKPMG Lower GulfWe hope you find this report valuable in illustrating the future of retail banking.Please contact us if you would like to discuss how we can help you evaluateand make progress on your bank’s connected path.E: auppal1@kpmg.comThroughout this document, “we”, “KPMG”, “us” and “our” refers to the global organization or to one or more of themember firms of KPMG International Limited (“KPMG International”), each of which is a separate legal entity.Future of Retail Banking 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.2

ContentsSignals of change04Customer signals05Competitive signals06Economic signals08Regulatory signals10Technological signals11The successful retail bank of the future requires a winningbusiness model supported by a connected operating model12Business models in the market today13Banking business models of the future14Strategic themes15A successful operating model is built upon eight connectedcapabilities16High maturity organizations continue to outpace their lessmature peers17Prioritizing connected banking capabilities18Connected capabilities enabling a winning operating model19Evaluating your capability maturity20Case studies21Making it happen22Future of Retail Banking 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.3

Signals of changeRetail banking faces a more complex environment than perhaps ever before.Driven by COVID-19, the social and economic landscape has been radicallyreshaped while customer needs and expectations continue to dynamically evolve.CustomerThe global impact of COVID-19 has accelerated consumer expectations and shifted priorities. Those banksthat are able to deliver seamless and personalized experiences to their customers, based on relevant dataand insights will be best placed to grow market share.CompetitiveIncumbent banks are being challenged from all sides for market by a combination of neo banks andnon-traditional participants. Longer term, customers will turn to alternative providers if their needs canbe met more effectively.EconomicThe adverse economic headwinds of COVID-19 will challenge retail banking margins. Traditional profitpools are under threat causing retail banks to rethink their business and operating models in order toachieve profitable growth.RegulatoryGlobally, regulators will take an interventionist approach to increase competition, drive greater enterpriseresilience, increase cyber security, protect data and support vulnerable customers. Retail banks will need toremain agile in their risk management approach.TechnologicalTechnology will continue to redefine the relationship between customer and retail bank. Banks need toprioritize their investment in current technologies in order to enable profitable growth and future agility, aswell as to substantially reduce the cost of operations through automating manual, paper-based processes.Future of Retail Banking 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.4

Customer signalsCOVID-19 has had an immediate and widespread impact across all countries anddemographics, heightening consumer expectations and shifting priorities.Consumers have become more demanding ofdigital experiences. COVID-19 has amplified theneed for easy access to products, services andinformation. Most customers are now comfortableusing online channels to buy what they need.They are reducing physical purchase occasions andare gravitating towards touchless shopping andcontactless payments. Eighty-two percent ofconsumers say they are more likely to use digitalwallets or cards in the future.Trust has become multi-dimensional. Customershave become more aware of environmental andcorporate behaviors. They are more questioning ofbrand behavior relating to environment and socialissues.““Value and price are becoming equals for customerloyalty. Consumer spending has been impacted byboth a decrease in disposable income and thepsychological impact of COVID-19. Cost or valuenow has greater impact on how a customer’sassessment of their experiences translates intoadvocacy and loyalty. This year our CustomerExperience Excellence 2020 research has found thatfor those countries experiencing severe economicimpact, value as a determinant of loyalty is secondonly to personalization.1Retail banks need toconsider how they candrive customer loyalty.Key purchase drivers63%Value for money42%Ease of buying41%Trust in the brandMy personal safety40%37%Range of products and services35%Customer experienceStaff/people policy19%Direct communications19%Brand’s values match my own18%Support for local communities18%Brand’s social conscience18%Brand’s approach to the environmentPersonalization17%14%% proportion of consumers who rate each as important in their decision-makingWhich of the following are important to you when buying a product or service?1KPMGCustomer experience in the new reality — Global customer experience excellence research:The COVID-19 special edition: Consumers and the new reality, KPMG International, June 2020Future of Retail Banking 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.5

Competitive signalsIncumbent banks are being challenged from all sides for market share by acombination of neo banks and non-traditional participants.Globally, the market hasbeen flooded with a newwave of growing neobanks. Unburdened bylegacy technology andoperating with greateragility, neo banks are ableto offer personalizedexperience and seamlessinteraction craved by ageneration who demand asmart digital experience.Incumbents are also being challenged by a series ofnon-traditional players. In Asia, social mediaplatforms such as WeChat have enjoyed success inoffering banking services. Similar well-establishedonline retailers such as Alibaba have begun to offerbanking services drawing on their advancedtechnology and well-established customer base.The market has also seen the introduction of morespecialist providers, operating in previouslyunexplored areas of the market. In Africa and Asia,micro-financing providers like Paytm are enablingunbanked customers to transfer funds using atelephone network without the complexity and feesof bank accounts. These are significant threats forincumbent banks who have been able to rely ondirect customer relationships to ensure ‘stickiness’and an opportunity to sell additional productsand services.However it is not all bad news for the incumbentbanks. The chart on page 7 shows that while newentrants are growing fast, customers primarilyuse neo banks for ancillary services. In the UK,80 percent of Monzo customers were also usingan incumbent’s banking app.Neo banks are still not widely used as a primarybanking service. This is likely due to customerinertia or feeling that there is a lack of trusted viablealternative especially in light of the recentpandemic. However, we believe over the longerterm, customers will turn to alternative providers iftheir needs can't be more effectively met. In fact,in parts of Asia such as Singapore and Malaysia,regulators have recently started to proactively issuedigital banking licenses and are encouraging nontraditional banks from outside these countriesto apply.Future of Retail Banking 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.6

Neo banks may defer profitability for scale and move towards larger, moreexclusive customer base, thus challenging retail banks. Retail banks need todecide where to emulate competitors or band together to form partnerships toretain competitive advantage.Market quadrant of UK banks2Small but very exclusiveLargest and most exclusiveNatwest70%65%Lloyds60%Most exclusive tarlingBank20%Revolut15%5%0%Santander llest and least exclusive123456789Large and least exclusive10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26Largest audience (monthly unique users) (%)2Fintechusers just can’t get enough of traditional banks, Financial Times, January 7, 2020Future of Retail Banking 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.7

Economic signalsThe adverse economic headwinds of COVID-19 will challenge retail banking margins.The global economy remains in recession with thetiming and path to recovery unclear. Consumerconfidence is low, with redundanciescommonplace. Our research shows that onaverage, four out of 10 are financially worse off,with another 13 percent deferring major purchases,limiting the volume of transactions and key revenuestreams for retail banks.3With the route to economic recovery uncertain,value for money has become the single mostimportant factor in customer decision-making. Halfof respondents across all global markets feel this ismore important now than pre-COVID-19.4With traditional profitpools under threat, retailbanks need to considerchanges to their businessand operating model.Digital transformation hasbecome an imperative forretail banks’ success.Due to this economic uncertainty, retail banksaround the world are being forced to provisionfunds against anticipated future losses oncestimulus funding and debt can no longer beserviced.Income will be reduced due to an increase in baddebt and low interest rates limiting the capitalavailable to retail banks for more profitable lendingactivity and applying further pressure to margins.We see some international banks retrenching fromglobal markets and putting greater focus on theirhome markets. This is likely to have implicationsfor customers.The viability of existing credit models within bankswill be reduced, leading to a tightening of creditand limiting the appetite to lend until confidenceis restored.3,4 KPMG Customer experience in the new reality — Global customer experience excellence research:The COVID-19 special edition: Consumers and the new reality, KPMG International, June 2020Future of Retail Banking 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.8

Just over half of consumers feel financially comfortable or secure versus 43 percentwho feel overwhelmed or vulnerable5Financially overwhelmed— Much worse offFinancially sensitive— Struggling to coveressentials— Slightly worse off— Stopped non-essentialpurchases— Vulnerable— Overwhelmed and anxious28%Financially comfortable15%— Not affected financiallyFinancially secure— Spending as before— Better off— Spending as before onessentials, but havedeferred major purchases44%— Calm13%— OptimisticWhile the overall picture is undoubtedly challenged, 57 percent of respondents nevertheless say they are comfortableor secure — representing a growth opportunity for retail banks to support those segments of customers who arebetter off and will look to accumulate wealth or continue their spending.6Source: Consumer and the new reality, KPMG International, June 2020Sixty three percent of consumers said value for money is the most importantpurchase driver, with forty-seven percent saying it has become more importantas a result of COVID-197Value for money as a key purchase driver by alia70%Hong Kong(SAR), ChinaConsumers and the new reality, KPMG International, June 2020Future of Retail Banking 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.9

Regulatory signalsGlobally, regulators are likely to take an interventionist approach to increasecompetition, drive greater enterprise resilience, increase cyber security, protectdata and support vulnerable customers. Regulators will also need to balance theneed for banks to extend credit to support economic recovery efforts.A growth in cyber attacks — for criminal gain or as adisruptive weapon — will result in an increasedregulatory focus on security and cyber controls.How these operate in a cloud-based environmentwill become a particular area of scrutiny.Regulators will continue to drive competitionthrough intervention, reducing barriers to entry andtargeting incumbents with ‘open banking’ stylerequirements to open up APIs to access accountinformation and payment functionality. Open Dataecosystems will create broader and more complexinteractions with players from different sectorswhere the regulatory landscape is not level.Compliance with these regulations will not onlypresent an increased overhead for banks, but willalso challenge their top line growth as new ‘digitalfirst’ competitors flood the market.Data privacy regulation will accelerate. Regulationwill focus on collection and ownership of personaland biometric data in the context of emergingtechnology. Additionally, it will be critical to balanceprivacy with the introduction of various forms ofopen banking/finance occurring in many markets.Increased clarity of requirements coupled withgreater enforcement by local regulators will beneeded to underpin customer trust.The disruptive impact of COVID-19 will mean thatenterprise resilience remains a top priority forregulators globally. Requirements will focus onproviding continuity of technology systems andbusiness services, with clear business interruptionplanning to manage incidents.“Retail banks need toconsider how well theyare organized toefficiently fulfil theirsignificant regulatory andcompliance obligations.“During the ongoingCOVID-19 pandemic, manygovernments have providedstimulus funding to protectconsumers and the widereconomy. We expect thisinterventionalist approach tocontinue with regulatorsgiven sharper teeth to pushforward with the regulatoryagenda.Unfortunately, the lasting financial impacts ofCOVID-19 will lead to a higher number ofvulnerable customers. Banks will need to have aclear and justifiable approach to identifying andmanaging diverse types of vulnerable customer,supporting them in appropriate ways.Future of Retail Banking 10 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.

Technological signalsTechnology will continue to redefine the relationship between customers and retailbanks. Our research indicates efforts around a digitally enabled technologyarchitecture, experience centricity, and insight-driven strategies and actions will beamong banks' top priorities to support their digital transformation moving forward.8Retail banks continue to investin technology to achieve costreduction, processimprovement and efficiency.Cloud solutions, for example.are replacing the traditional useof data centers at some bankslooking for increased security,greater resilience andscalability. Seventy-five percentof our survey respondents saidthey are leveraging Cloudcomputing to enable theirdigital transformation.9The growth in the power of data & analytics and theincrease in the volume of data available has enabledgreater personalization of all customer interactionsfrom marketing through to sales, on-boarding andservicing. Seventy-one percent of our surveyrespondents said it is a key priority to support theirdigital transformation moving forward.10“Retail banks need todecide which combinationof technologies to invest into enable profitable growthand future agility.“8,9,10However, many incumbent banks may not currently beusing the information as effectively as they could.Furthermore, open banking/open data is reshapingglobal ecosystems and creating new business modelsthat banks should evaluate.Leading banks are already systematically deployingautomation solutions such as RPA and chat bots to increaseefficiency and leverage insights. This will become the defaultapproach in the bank of the future.Many banks will need to accelerate and scale their owninfrastructure and cloud programs to drive digitalfunctionality, fulfilment and personalization — which willoften be in partnerships or joint ventures with agile,innovative fintech players. They will need to utilizesophisticated data & analytics information to target theright products and services to individual customers, withthe right frequency, through the right channels.It will also be key that banks have an unrelenting focuson the operational resilience and security of theirservices, particularly against cyber attacks, as moreservices move online and to digital. In the middle andback offices, it will be crucial to leverage newtechnologies to move processes onto a more digitalfooting, replacing manual and paper-based operationswith greater levels of automation and straight-throughprocessing.New technology has given rise to a set of newinteraction channels such as APIs which are beingembraced by leading financial services firms to reachnew customers. Technology will continue to evolve atpace and emerging concepts such as augmentedreality and distributed ledger technology will furtherredefine the nature of banking services.The above technologies will combine to redefine thebank-customer relationship, making banking morepersonalized across customer devices.Now, with low code development, ease of integrationcapabilities and cloud, the technology element of digitaltransformation is no longer the difficult part. It is withinthe other signals where the challenges lie.Base: 412 professionals involved with customer strategy decisions at retail banking organizationsSource: A commissioned study conducted by Forrester Consulting on behalf of KPMG, September 2020Future of Retail Banking 11 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.

The successfulretail bank of thefuture requiresa winningbusiness modelsupported by aconnectedoperating modelFuture of Retail Banking 12 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.

Business modelsin the market todayThere are five main types of retail banking business models we see in themarket today.0102030405These are banks that provide the full range of banking services acrossbroad customer segments, from retail and business banking tocommercial and investment banking. Most of these banks alreadyprovide bancassurance or wealth management related productsand services.Full service banksE.g. HSBC, Citibank, Deutsche Bank, Banco Santander,Bank of BarodaSpecialist banks focus on retail and small business customers, andtend to have a strong understanding of the needs of their targetcustomer segment. The bulk of their revenue tends to be interestincome from products such as mortgages. This category also includesthe small digital neo banks.Specialist banksE.g. DBS, Equitable Bank, MonzoConsumer credit focused banks mainly target under-served sectionsof the community. These banks often started out as non-bankfinancial institutions such as auto loan providers, subprime credit cardproviders or gold lenders, but have since taken deposits to reducetheir funding costs.Consumer creditprovidersE.g. American Express, Capital One, MastercardThese banks have the main objective of furthering financial inclusion.They usually have a limited range of basic banking products, such asdeposit accounts and remittances, but have a widespread networkeither through branches or networks provided by others such asretailers or post offices.Money transferprovidersE.g. Grameen Bank, Western Union, PayPalBanks that employ the wallet model focus on the customerexperience in digital transactions. They are typically born from fintechcompanies that interface with social media platforms, and haveexpanded to provide deposit and lending services.Digital walletprovidersE.g. WeChat Pay, Ant Financial, PaytmThe signals of change are driving an evolution across the retail banking sector,and our research tells us that in order to achieve profitable growth and bettermanage the impacts, banks will need to pivot to business model ecosystemsto succeed in the future.Future of Retail Banking 13 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.

Banking businessmodels of the futureIn the future, we believe three retail banking models are more likely to dominatethe market, including a new type of ambient bank. The customer will be core tothe strategies of all three models.010203Universal banksTransaction-focused banksAmbient banksUniversal bank margins are beingsqueezed on both ends, with highoperating costs and downwardpressure on transaction fees andinterest income. Consequently,universal banks need to be datadriven and develop ecosystems oftheir own drawing on their largecustomer base. This will enable themto expand into new profit pools,such as helping consumers andhouseholds save in major spendcategories, like utilities, groceries,telco/internet, etc. The ability toutilize transaction data will be key tothis, to enable a deeperunderstanding of customer behaviorand opportunities to support them.Transaction-focused banks areprimarily payment service providersby nature. They are heavily focused onunit economics, having to ensure thatthe unit cost of transactions can becovered by revenue to guaranteesustained profitability. They adopt ahighly focused model and targetspecific customer segments,constantly innovating on those sets ofcustomer needs to expand theirservices.Ambient banks don’t act asstandalone entities, but rather are the‘invisible’ agents embedded withinevery day Internet of Things (IoT)devices to facilitate transactions.Having access to data from many IOTdevices also will give the bank adeeper understanding of customers’spending habits and credit needs.Universal banks will retain some oftheir branch network, whether toserve high margin customersegments that desire in-personinteraction, or rural communities thatlack digital proficiency and access.Despite this, the operating model willneed to be as automated as possibleto drive cost efficiency.With large customer bases andbenefiting from rich customertransaction history data, the success ofthese banks will be facilitated by openbanking — which could also enable bigtech companies to take a slice of theaction and perform an increasingnumber of banking transactions fortheir customers.The ambient bank is an enabler ofecosystems such as those ofSamsung and Microsoft. As a result,the focus is on building and providingAPIs, micro services and modularbased technology architecture.Some traditional banks are exploringthe ambient bank model. FINN byING Bank, for instance, allows smartdevices to make autonomouspayments on behalf of the user.Goldman Sachs has launched an APIportal for developers, seeing itself asan API producer in the ecosystem.We believe one key attribute of the banking business models of the future will bea greater resilience to economic shocks such as those resulting from COVID-19.Future of Retail Banking 14 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.

Strategic themesThere are five strategic themes that we believe will significantly impact all threebusiness models.Strategic theme010203I. Universal banksII. Transaction-focused banksIII. Ambient banksIdentifying andserving customerneedsB2B and B2C model —experience-centricity is crucialand universal banks have toleverage their large volumes oftransactional data to createdigitally enabled, insightdriven strategies.B2B and B2B2C models —transaction-focused banksinterface with multipleecosystems and have toprovide seamless interactionsand commerce with them.B2B model — ambient banksare part of everyday IOTdevices and will createinnovative products andservices on the back of thegrowth of smart, connectedtechnologies’.Focusing on anddriving costefficiencyCost pressures result inuniversal banks reducingtheir branch network andachieving operational efficiencyby creating responsiveoperations and supply chains.High emphasis on automationas transaction costs need to belower than revenue. There is aneed to invest in digitallyenabled technologyarchitecture to drive processefficiency.Minimal employee costs asfocus is almost entirely onprovision of technologicalinfrastructure such as APIs.Evolution of front officeworkforce towards millennialsmeans universal banks need toembrace new ways of workingto create an aligned andempowered workforce.Front office is more technologyoriented and the workforce isfocused on back office activitiesrather than customerinteractions.Front office is more technologyoriented and workforce isfocused on back office ratherthan customer interactions.Adopting new waysof working04Complying withincreased volume ofregulatory drivenchange05Identifying rolewithin widerecosystemsAgility comes from skilledworkforce and technology.Bank employees shift theirfocus to managing strategicpolicies and escalation.Agility comes from technologyand automation, with bankemployees shifting their focusto manage strategic policiesand escalation.Agility comes from technologyand automation. Escalations aremanaged by AI as datascientists build strategicdirection into algorithms.Risk and regulatoryframework already fullydeveloped, with pace ofregulatory change increasing.Full set of established bankingrisks and regulations apply.Evolving risk and regulatoryframework, with some crosssector regulations applicable(e.g. e-commerce). Fraud riskand incorrect transactions canrepresent a large proportion oftotal costs.Risk and regulatoryframework still nascent. Highlevels of cyber and tech risksfrom IOT as each product anddevice becomes a potentialcybersecurity vulnerability.Universal banks act as theanchor of ecosystems, creatingintegrated partner andalliance networks.Participants of as manyecosystems as possible, inorder to increase volume oftransactions and thereforerevenue.Embedded in ecosystems asenablers. They are part ofservices and products, withinIOT devices such as televisions,refrigerators or cars.In order to deliver on these strategic themes, KPMG professionals haveidentified eight capabilities that banks will need to embed within theiroperating model.Future of Retail Banking 15 2020 Copyright owned by one or more of the KPMG International entities. KPMG International entities

Future of Retail Banking. Foreword. As the industry adjusts to the effects of Covid-19 and looks towards the future, the retail banking landscape has undergone considerable transformation. Banks must negotiate a multitude of shifting factors —from changing customer behavior to economic headwinds, intensifying competition, regulatory pressure