Transcription

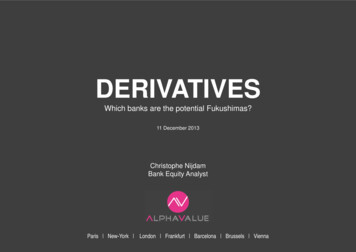

DERIVATIVESWhich banks are the potential Fukushimas?11 December 2013Christophe NijdamBank Equity AnalystParis New-York London Frankfurt Barcelona Brussels Vienna

DERIVATIVESWhy this research memo?As bank equity analysts, we are concerned with the two channels by which bank systemicrisk spread the most, i.e. liquidity and derivatives, destroying an enormous amount ofshareholder value in the process, not to forget other stakeholders (the real economy,taxpayers, depositors, bank employees, society as a whole, etc.)Christophe Nijdam’s headstart exposure in derivatives:1983 : co-founded the derivative group at CCF (now HSBC France)1985 : co-invented the so-called CIRCuS (cross interest rate and currency swaption)Supervised the unwinding/running-off of an off balance sheet OTC interest rate derivativeportfolio that had reached 6 times the size of the cash balance sheet at Crédit du Nord USA(then a Paribas subsidiary) in 1989-1990This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates2

3

Value-at-Risk (VaR) starts beingdisseminated around trading roomsBank of America, Derivatives 1995-2012Lehman failureSeptember 2008Gramm-Leach-Bliley Actrepeals the Glass-Steagall ActNovember 1999LTCM meltdownSeptember 1998Source : FDIC 80trn(3x 1998 GDP)This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates 630trn(10x 2012 GDP)4

DERIVATIVESWhat is a NOTIONAL derivative amount?The notional amount is the face value of the derivative contract: it is used as a reference to calculatepayments e.g. IRS fixed rate (4%) against Libor (0.5%) on 100M swap agreement ( 100M x 4%) –( 100M x 0.5%) 3.5M net interest payment( ) e.g. CDS 75% loss/25% recovery 100M x 75% 75M credit insurance net paymentThe notional amount does NOT reflect the risk associated with such contract (see above IRS/CDSexample)However, the notional amount indicates the volume of activities of a bank in derivatives: e.g., it’s the volume of credit insurance policies sold and/or bought (CDS), the volume of interest rate insurance policies sold and/or bought (IRS), etc.The industry prefers to speak about « gross market values », ie the cost of replacing the contract atcurrent market prices, as it downplays and understates the size of the actual risk (see CDS example) ina systemic crisisIf another indication of the relevance of the notional amount vs gross market value was needed, initialmargin requirements for CCP (see further) are computed on notionals This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates5

DERIVATIVESGross Market Values vs Notional Amounts (%)7,00%6,00%5,00%( )GMV multipliedby c.3x from 2.16%in H1 07 to 5.89%in H2 08 Gross Market Values/Notional AmountsSource: B.I.S., 1H22011H12012H22012H12013See further about « how much a loss in notional is needed to wipe out equity »This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates6

DERIVATIVESWhere do we find NOTIONAL derivative amounts? It’s an off-balance sheet information which is disclosed in the footnotes attached to financialstatements Most banks do not split notional amounts between assets and liabilities, giving rise to( )double-count The « counterparty risk » remains on full notional amounts (unless there is a valid nettingagreement between, e.g., two banks, or a bank and a corporate) What we find « on » balance sheets are fair (market, or worse, model) values of suchderivatives, also roughly equivalent to « gross market values of contracts » (ie thetheoretical cost of replacing the contracts at current market prices – see previous slide) There are accounting differences in « on » balance sheets between US GAAP (partial nettingof derivatives) and IFRS (no netting allowed); hence, IFRS balance sheets are larger vs USGAAP But there is no accounting difference in NOTIONAL amounts between US GAAP and IFRSThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates7

DERIVATIVESNotional derivative amounts (e.g. Goldman Sachs vs BNP Paribas)( )On balancesheetOff balancesheetThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates8

DERIVATIVESNotional derivative amounts (e.g. Goldman Sachs vs BNP Paribas)( )On balancesheetOff balancesheetThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates9

DERIVATIVESGlobal OTC derivative notional amounts (in US Billion, no double-count)Total notional derivativeso/w Interest rateo/w Forexo/w CDSSource: B.I.S.800 000 683,814bn700 000 706,884bn 692,908bn 100%( )600 000 561,299bn 81%500 000400 000300 000200 000 58,242bn 10% 73,121bn 11%100 000 24,349bn 4%H1 2006 H2 2006 H1 2007 H2 2007 H1 2008 H2 2008 H1 2009 H2 2009 H1 2010 H2 2010 H1 2011 H2 2011 H1 2012 H1 2012 H1 2013This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates10

DERIVATIVESFollowing the repeal of the Glass-Steagall Act,derivatives growth went haywireTotal notional derivatives by country of banks 1998-2013(source: Berruyer, B.I.S. and bank annual reports)Asian banks( )other European banksSwiss banksFrench banksBritish banks bnAmerican banksIn addition, please note thatLiborgate / Euriborgate isdriven by derivatives « within »Universal banks (only deposittaking banks can participate inthe rate-fixing panels; pureinvestment banks can’t)H1 98H1 00H1 02H1 04H1 06H1 08H1 10This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliatesH1 1211

DERIVATIVESWhat is a NAKED Credit Default Swap (CDS)? A naked CDS is buying a credit insurance policy without owning the underlying credit risk (bonds,loans, etc.), i.e. without an « insurable event » In ( )the insurance industry, you must own the underlying risk to have an « insurable event » and beallowed to insure that risk with an insurer In essence, a naked CDS is like bying a fire insurance policy on your neighbour’s house On top of that, with naked CDSs, there are no limits on the numbers of fire insurance policiesyou can buy on your neighbour’s house Guess what happens next?This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates12

DERIVATIVESWhat does the ESMA say in its latest reporton « Trends, risks, vulnerabilities »? Report dated 20 September 2013 (extracts)( )This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates13

DERIVATIVESWhat does the ESMA say in its latest reporton « Trends, risks, vulnerabilities »?( )This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates14

DERIVATIVESWhat does the ESMA say in its latest reporton « Trends, risks, vulnerabilities »?( )This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates15

DERIVATIVESDexia remains systemic through the liquidityand derivatives contagion channels( ) Dexia failed twice on liquidity despite sufficient solvency ratios* bothin September 2008 and September 2011 Dexia is still a systemic institution despite its shrinking balance sheet(« only » 238bn on 30 September 2013, down from 651bn on FYE 2008),hence the 85bn government refinancing guarantees (running until 2076) Dexia has latent losses of 29bn on 450bn in notional interest rate derivatives(6.4%. Who said that IRS were riskless?) –source: testimony of Dexia’s management in front of the French parliament on 22 May 2013* Core Tier 1 ratio of 20.7% (sic!) on 30 September 2013This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates16

DERIVATIVESJPMorgan, the « best of class » in risk management,tripped over the London Whale( ) « Propagator » of the value at risk (VaR) through its listed subsidiary RiskMetrics from the midnineties onwards – VaR is equivalent to managing risk by looking in the rear window mirror while notwatching the blockroad ahead. Additionnally, danger comes from the blind spot (« angle mort ») inthe mirror (« 99% confidence level does not tell you how much you will lose in the 1% occurrence/fattail « Black Swan » syndrome) VaR is responsible for the bloating of trading activities and the outgrowth of derivatives Stumbled with the London Whale in the Spring 2012: 6.2bn loss on a 100bn CDS derivativeportfolio (supposedly a « hedging » gone wrong) a 6.2% loss in a few weeks AIG London/Banque AIG France (efficient French « home supervision » from the ACP!), SwissRe,CDPCs, etc. all needed « bailouts » on CDSs Tantamount difference in risk between an IRS and a CDS, but IRS is not riskless (see Dexia)This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates17

Usual suspects the Global Trading and Universal Banks(G-TUBS)

DERIVATIVES« Universal banks » overweighted in the list of world systemic banksThe Bank for International Settlements (BIS) identified 20 « universal banks » as part of the 28« Global Systematically Important Financial Institutions » (G-SIFIS)(April 2013)This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates19

DERIVATIVESUsual suspects the Global Trading and Universal Banks (G-TUBS)Fitch has coined a specific category: the G-TUBS (« Global Trading and Universal Banks »),a select group of 12 banks (7 European – o/w 2 French, 5 American)(10 October 2013)This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates20

DERIVATIVESNotional derivative amounts – 38 European banks – AV universe ( bn)60 000 000e.g. 55,605bn for Deutsche Bank50 000 000( )40 000 0002006201230 000 00020 000 00010 000 000-No data for BBVA, Caixabank, Sabadell; no data in 2006 for Credit SuissseThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates21

DERIVATIVESNotional CDS amounts – 38 European banks – AV universe ( bn)3 500 0003 000 0002 500 000( )e.g. 2,622bn for Deutsche Bank2 000 0001 500 000200620121 000 000500 000-No data for Caixabank, Sabadell; no data in 2006 for Credit Suisse and BNP ParibasThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates22

DERIVATIVESNotional derivative amounts relative to domestic GDP (2012) – 45 bankse.g. 86 times Swiss GDP for Credit Suisse(relevant to determine domestic SIFIs)100,0090,0080,00( )Swiss, British, Danishand Swedish « finishes »70,0060,0050,00Notional amount / domestic GDP (2012)Nb of times (x)40,00No Frenchor German « finish ».30,00#1 bank market capin the world, Warren Buffettis a large shareholder20,00This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliatesEFG InternationalBanco Popular EspanolDeutsche PostbankMediobancaBanca Monte Dei Paschi Julius BaerWELLS FARGOCREDIT MUTUEL CICBanco Espirito SantoBanco Comercial PortuguesNo data for BBVA, Caixabank, SabadellErste GroupStandard CharteredBank of IrelandIntesa SanpaoloDnBSvenska HandelsbankenUnicreditDexiaKBC GroepGOLDMAN SACHSCommerzbankMORGAN STANLEYSwedbankCITIGROUPNatixisLloyds Banking GroupBOA MERRILL LYNCHSantanderJP MORGANSkandinaviska Enskilda BankCrédit AgricoleSociété GénéraleHsbcNordeaDeutsche BankDanske BankBNP ParibasRoyal Bank Of ScotlandBarclaysUBSCredit Suisse0,00Raiffeisen Bank 10,0023

DERIVATIVESNotional derivative amounts relative to European GDP (2012) – 45 banks5,004,50e.g. 4.5 times European GDP for Deutsche Bank4,003,503,00( )Notional amount / EU GDP (2012)Nb of times (x)2,502,00Listed benchmark1,50Unlisted « marker »1,000,500,00No data for BBVA, Caixabank, SabadellThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates24

DERIVATIVESHow much a loss in notional derivatives is needed to wipe out equity (2012)?16,00%Lower riskWeighted average: 29bp14,00%Total notional equity wipe out12,00%( )10,00%8,00%6,00%4,00%Higher risk2,00%0,00%38 European banks – AV universe. No data for BBVA, Caixabank, SabadellThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates25

DERIVATIVESHow much a loss in notional derivatives is needed to wipe out equity (2012)?Focus on the top 15 out of 38 European banks0,70%Total notional equity wipe out0,60%0,50%0,40%Read: a 16bp loss on BNP Paribas’ 48,300bnnotional amounts would wipe out its 78.6bngroup share equity0,30%0,20%0,10%0,00%38 European banks – AV universe. No data for BBVA, Caixabank, SabadellThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates26

DERIVATIVESHow much a loss in notional CDS is needed to wipe out equity (2012)?Weighted average: 765bpLower risk250,00%Wipe out CDS only200,00%( )150,00%100,00%50,00%Higher risk0,00%38 European banks – AV universe. No data for BBVA, Caixabank, SabadellThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates27

DERIVATIVESHow much a loss in notional CDS is needed to wipe out equity (2012)?Focus on the top 13 out of 38 European banks25,00%Wipe out CDS only20,00%15,00%( )Read: a 374bp loss on BNP Paribas’ 2,100bnnotional CDS would wipe out its 78.6bngroup share equity10,00%5,00%0,00%38 European banks – AV universe. No data for BBVA, Caixabank, SabadellThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates28

DERIVATIVESNotional amounts will be part of the denominator in the future leverage ratioNotional amounts x times balance sheet size (2012 total assets)60,0050,00( 8 European banks – AV universe. No data for BBVA, Caixabank, SabadellThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates29

Basel 3/CRD4, EMIR

DERIVATIVESRisk mitigations: regulations (Basel 3/CRD4, EMIR), if not enucleated by lobbyNational « finishes »( regulatory ratios higher than Basel 3/CRD4): Swiss (Ti1) – we understand why when lookingat the derivative sizes at CS and UBS! US (leverage, LCR)( ) British (CT1, leverage) – ditto Barclays and RBS Danish (CT1, LCR) Swedish (CT1, LCR) Norwegian (CT1) Brazil (total capital of 11% vs 8%) China (total capital of 9% vs 8%) India (T1 of 7% vs 6%, leverage of 4.5%)EMIR Required H2 14: Central Counterparty ClearingHouses (CCPs) for standard derivatives, butcounterparty definition loopholes (SPVs, localauthorities, etc.) Required 12/02/14: 6 trade repositories with LegalEntity Identifier (LEI) approved by ESMA in Europe(DTCC in the US) – who/what/where Required 01/12/15-01/12/18: Initial margins fornon-CCP OTC (see next slide), Master NettingAgreementsRingfencing (See US Volcker, US Tarullorule, UK Vickers, CS inSwitzerland, but Liikanen isburried in Europe)No « finish » at all or« ringfencing » inGermany and France(Deutsche Bank, BNPParibas) but US bank « push-out » ofderivatives (into specificsubsidiary outside ofgovernment deposit guarantee)has been overturned by thelobby on 30 October 2013Dodd Frank in the USIn Europe Swap Execution Facilities (SEF)since October 2013 18electronic trading platformsincreasing competition andtransparency Problematic of the US CFTCextra-territoriality rules when oneUS counterpart Projects for OrganisedTrading Facilities (OTF)This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates31

DERIVATIVESThe initial margin requirements on non-CCP OTC that lobbyists want to killASSET CLASSCredit : 0-2 year duration( )Initial margin requirement(% of notional exposure)2Credit : 2-5 year duration5Credit : 5 year duration10Commodity15Equity15Foreign exchange6Interest rate : 0-2 year duration1Interest rate : 2-5 year duration2Interest rate : 5 year duration4Other15Source: « Margin requirements for non-centrally cleared derivatives »,BIS & OICV-IOSCO, September 2013An IMF report in 2010 estimated that ¼ of IRS,1/3 of CDS and 2/3 of other OTC derivatives arenot « standard » enough to be operated throughCCPs. Based upon H1 13 notionals, it’sc. 220trn, or 1/3 of the total derivativemarket, which can’t be processed throughthe CCPs. Hence, margin requirements arecrucial to help contain systemic risks on nonCCP OTC derivativesWith a cumulative 34% market share in equityderivatives in 2011 (source: JPMorganresearch), the 4 listed French banks arereportedly currently lobbying the hardestagainst the 15% initial margins in equityderivatives and the 0.01% TTF on such equityderivativesAssuming a 3% p.a. funding cost for the marginrequirement/collateral, a 1% initial margin on a2-year IRS would cost 3bp p.a. (1% x 3%) whilea 15% margin on an equity derivative wouldcost 45bp p.a. (15% x 3%), the price of safetyagainst the systemic impact of the speculativeportion of derivatives disguised as « marketmaking »This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates32

DERIVATIVESThe case for initial margins in equity derivativesNumber of daily changes /- 2% per year in the S&P 500( )This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates33

DERIVATIVESWe live in a volatile world with Blackswans becoming the normImplicit volatility VIX IndexThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates34

The real challengebehind the European TTFDeflating the derivative bubble

DERIVATIVESThe real challenge behind the European TTF: deflating the derivative bubble 10bp TTF on cash products (equities, bonds, money market funds) is plain stupid 1bp TTF on derivative notional amounts is smart as it reduces substantially the economics behind the marketmaking/disguised prop trading bubble in derivatives( ) as a reminder, daily trade volume in F/X reached 5,300bn (BIS, April 2013), up from 4,000bn in 2010 and 3,300bnin 2007: world trade ( 18,300bn in merchandise and 4,300bn in services in 2012, WTO) is « covered » in 4 days and world capital markets/global financial assets ( 225,000bn, McKinsey, March 2013) are « hedged » in 42 days or in 9 business weeks altogether (17% of a calendar year) we wonder what F/X trader do at their desk the rest of the year? Counting beans or trifles? by some estimates (BIS), only 7-8% of derivatives would be with end-users and 92-93% with « financial institutions »(the Merry-Go-Round of the G-TUBs with implicit state guarantees pertaining to their 2B2F status) by some estimates, the TTF would induce a 75% reduction in European F/X volume and a contraction between 70% to90% in other European derivative trading volumes (EC, 2013b) - (Great! What are we waiting for?) (100% - 75% 25% - 7% end-users 18% left for « real » market making)This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates36

DERIVATIVESWhich banks are the potential Fukushimas of the derivative time bomb?Which banks would lose the most from CCPs,initial margins [and European TTF on derivatives]0,35%Market cap on 30 November 2013 over 2012 notional derivative amounts0,30%( )0,25%Highest market value sensitivity to derivatives0,20%0,15%0,10%0,05%0,00%Banks in countries without domestic « finish » above Basel 3 requirements are underlined in pink38 European (AV universe) 6 American banks. No data for BBVA, Caixabank, Sabadell. Dexia excluded (in runoff)This publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates37

DERIVATIVESRemember what the smart money saidMajor shareholder of Wells Fargo, the world largest bank market capThis publication may not be reproduced or distributed in whole or in part without the prior consent of AlphaValue or its affiliates38

Value-at-Risk (VaR) starts being disseminated around trading rooms . 80trn (3x 1998 GDP) 630trn (10x 2012 GDP) LTCM meltdown . September 1998 . Gramm-Leach-Bliley Act