Transcription

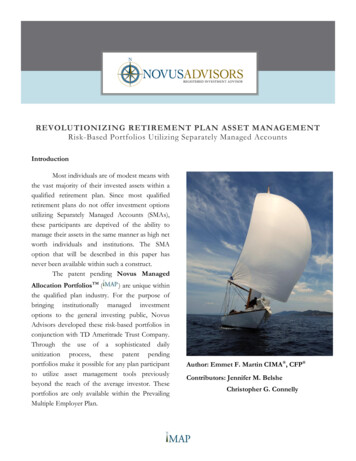

REVOLUTIONIZING RETIREMENT PLAN ASSET MANAGEMENTRisk-Based Portfolios Utilizing Separately Managed AccountsIntroductionMost individuals are of modest means withthe vast majority of their invested assets within aqualified retirement plan. Since most qualifiedretirement plans do not offer investment optionsutilizing Separately Managed Accounts (SMAs),these participants are deprived of the ability tomanage their assets in the same manner as high networth individuals and institutions. The SMAoption that will be described in this paper hasnever been available within such a construct.The patent pending Novus ManagedAllocation PortfoliosTM () are unique withinthe qualified plan industry. For the purpose ofbringing institutionally managed investmentoptions to the general investing public, NovusAdvisors developed these risk-based portfolios inconjunction with TD Ameritrade Trust Company.Through the use of a sophisticated dailyunitization process, these patent pendingportfolios make it possible for any plan participantto utilize asset management tools previouslybeyond the reach of the average investor. Theseportfolios are only available within the PrevailingMultiple Employer Plan.Author: Emmet F. Martin CIMA , CFP Contributors: Jennifer M. BelsheChristopher G. Connelly

INTRODUCING THEOne of the most enduring debates withinthe investment world is that of the relative meritsof active portfolio management versus passivemanagement. Proponents of active managementbelieve that added value and greater returns can beattained through actively trading a portfolio ofsecurities. Active managers seek to bring greaterreturns through research, market timing, byapplying specific trading strategies or by ridingmarket trends. Advocates of passive assetmanagement believe (generally) that greater returnscan be obtained by investing in low–cost indexinvestments such as the S&P 500 or the Russell2000. Compelling arguments have been made onboth sides, however, it is clear that overallportfolio return is a multi-variable function. Thestyle of investment is certainly a factor in the netalpha (added value) of a specific portfolio;however, one specific style doesn’t necessarilyneed to be uniform within the portfolio.SOLUTIONAdditionally, whatever the style, the actual assetallocation (percentages of certain types ofinvestments) within the portfolio has been clearlydemonstrated to be the main driving force ofreturns; in fact, a Nobel Memorial Prize inEconomic Sciences has been awarded (Markowitz,Miller, Sharpe – 1990) for demonstrating this verypoint.Portfolioconstructioncanbemetaphorically compared to building a car. A wellconstructed car begins with an efficient design(investment policy). Once the design is completed,the maker must choose the parts which willcomprise the vehicle (active investments vs.passive investments). Finally, the vehicle should bewell maintained such that the warranty will remainin force (due diligence / compliance withinvestment policy / tactically managed).PORTFOLIO DESIGNRiskPeople intuitively know that in order tolower risk, risks should be diversified. Whileconstructing portfolios, asset managers attempt tominimize two general types of risk: portfolio riskand systematic risk.Portfolio risk can be lowered by addingdifferent types of securities into the portfolio. Forexample, stocks of the makers of automotive partsare directly correlated to auto sales; however, thestock of a soft drink bottling company would,more than likely, be unaffected by a decrease inauto sales.Systematic risk is that which affects theentire universe of correlated investments. Forexample, the events of September 11, 2001dramatically affected stock and bond marketsregardless of which types of stocks and bondswere owned. This risk can be somewhat decreasedby introducing asset classes categorized ts may include unusual types ofsecurities such as interest rate futures,commodities,orpreciousmetals.

Figure 1Asset AllocationNo one can predict the future; there are nocrystal balls. The best we can do is to study thepast and attempt to derive models based uponhistory and prevailing trends given context andcircumstance; this is precisely what Dr. HarryMarkowitz described in his 1952 paper entitled“Portfolio Selection”, which gave birth to“Modern Portfolio Theory”. In 1959, Markowitzclassified it as “Portfolio Theory” because“There’s nothing modern about it”.1The idea is that, given the information thatwe have about the past performance of certainasset classes (for example, large company stocks,government bonds, commodities etc.), we canmeasure the volatility of these collective classes.For instance, figure 2 (right)3 shows that value andgrowth stocks are more risky to own than moneymarket and cash positions while futures contractsare more risky and volatile than any other assets onthe chart.The point at which a portfolio isconsidered “fully diversified” (where adding moretypes of asset classes can no longer lower nonsystematic risk) is another debate, however, it isgenerally accepted that a fully diversified portfoliois comprised of at least eight different asset classes.Figure 2There are four components to Modern PortfolioTheory:1. Investors avoid risk and expect to becompensated for the risk that they endure.2. Securities markets are efficient. In other words,the mathematics of the theory relies upon thenotion that the prices of securities alreadyreflect all known information.3. Investors should focus on the portfolio as awhole and not on individual securities.4. Every risk level has a corresponding optimalmixture of differing types of assets which willprovide the highest expected return possible.

Figure 3Portfolios B and D (figure 3)4 carry anidentical amount of risk; however, historicalreturns of portfolio B far exceed those of portfolioD. Any rational investor would then chooseportfolio B rather than portfolio D due to the firstcomponent of the theory: “Investors avoid riskand expect to be compensated for the risk thatthey endure”. In truth, a computer simulation ofthe last 100 years of market activity would haveproduced hundreds of portfolios between B and D;B would still be chosen because it is the most“Efficient” portfolio; the top performing portfoliosustaining the stipulated corresponding risk.When this process is repeated across thespectrum of risk, the entire graph is spotted withportfolios plotted along their correspondingperformance levels; however, we are onlyinterested in the top performing portfolios foreach risk. Eliminating all of the inefficientportfolios leaves us with an arc of connected dots all of the top performing portfolios. This arc iscalled the efficient frontier. If the fourassumptions of Efficient Market Portfolio are true,then constructing models along the efficientfrontier will satisfy components 1 and 4 above. Ifinvestors believe that Modern Portfolio Theorycarries any validity, then they should also ascribe tocomponent 3 as the theory has demonstrated thatover 92% of a portfolio’s return is attributable tothe asset mix comprising the portfolio – notmarket timing or individual stock selection.Active Management OptionsMutual funds are a popular vehicle foractive management; they provide diversificationand have low barriers to entry – most mutualfunds can be bought with a small amount ofmoney. Mutual funds pool investor money andbuy blocks of securities. At the end of the day, allof the holdings of the mutual fund are tallied fortheir performance and the net asset value of theshares is updated, therefore, the value of a mutualfund changes one time per day.Institutional money managers, on the otherhand, have high barriers to entry. Many of themhave a minimum investment (to open an account)of 250,000 or more. They specialize in a specificarea of the market (for instance, small cap stocks,emerging markets, or commodities). TheSeparately Managed Accounts managed by theseprofessionals hold the actual securities comprisingthe portfolio. There are advantages to constructinga portfolio (at least in part) in such a manner. Forexample, while British Petroleum (BP) wasenduring the incident with the oil leak in the Gulfof Mexico, BP stock experienced a significantreduction. Investors in mutual funds that ownedBP (in large quantities – some mutual funds hadvery large positions in BP stock) were not fullydivested of holding BP until the mutual fund hadsold the last share out of inventory; in some cases,that was months. With a mutual fund, if you own

shares of the fund and the fund owns a specificstock, you own that stock until the fund hascompletely sold its position. The mutual funds(and consequently their shareholders) were in atough position; after all, the market can onlyabsorb so much stock at a time.Contrasting this situation with a SeparatelyManaged Account, the owner of an SMA wouldhave likely found that his 2,000 shares of BP hadbeen sold almost immediately. Separately ManagedAccounts are generally utilized by high net worthindividuals and institutions such as endowments,pooled pension funds, hospitals, and foundations.At Novus Advisors, we do not fully ascribeto component 2. We believe that while somemarkets are efficient, others are not. If all marketswere completely efficient, 100% (not 92%) of thereturn of a portfolio would be attributable to themixture of assets within the portfolio. Largemarkets, such as large cap growth and large capvalue, are comprised of companies with vastFigure 4quantities of outstanding stock; as such, thosecompanies are widely followed and heavily traded.Public dissemination of relevant news regardingthese companies results in instantaneous marketreaction thus making it exceedingly difficult for anactive manager to bring any added value whentrading this space. The reasons are simple – activemanagers, in efficient markets, generally getinformation at the same time as the investingpublic; secondly, trading, research and overheadexpenses create a drag on portfolio returns.Multiple studies have confirmed that, in mostcases, active management within efficient marketsresults in portfolio underperformance. We believein passive management within the efficient marketspace. Additionally, we believe that inefficientmarkets exist whereby active management maybring added value. Our philosophy is Core andSatellite: a core portfolio of passively managedand inexpensive Exchange Traded Fundscomplimented by a battery of SMA managersactively trading the inefficient markets.

Investment PolicyIn addition to the twenty-one mutual fundsthat are available on the investment platform, thePrevailing Multiple Employer Plan offers four riskbased managed allocation portfolios. The NovusManaged Allocation PortfoliosTM are unique tothe retirement plan industry. These portfolios aremanaged utilizing a core and satellite approach;each is comprised of an efficient allocation.Additionally, each portfolio is independentlyaudited on a monthly basis assuring compliancewith investment policy. Due to their economies ofscale as well as their passive component, theseportfolios are extremely inexpensive relative to thelevel of asset management provided.THE PARTSCore and Satellite Management Utilizing SMA PlatformsThe Novus Managed AllocationPortfoliosTM are unlike anything else offered inthe retirement plan space. Many platforms offerpassively managed portfolios and realize costefficiencies while others offer actively managedmutual fund portfolios in search of added value.These portfolios have revolutionized the wayindividuals may invest within their definedcontribution qualified retirement plan. ApplyingSMA management to the active portion of theseportfolios affords the average investor theopportunity to invest much like a high net worthindividual, corporation or endowment.Maintenance: Due Diligence / Compliance / Tactical ManagementThe Novus Managed AllocationPortfoliosTM are consistently screened by theNovus Advisors investment committee fordevelopments that may affect the markets, the12345SMA managers, or their compliance with writteninvestment policy. An independent third partyaudit verifying investment policy compliance isperformed on a monthly basis.Markowitz, H.M. (1959). Portfolio Selection: Efficient Diversification of Investments. New York: John Wiley & Sons. (reprintedby Yale University Press, 1970)Figure 1: lFigure 2: .phpFigure 3: ot--to-portfolio-management-112.htmlFigure 4: rtfolio-management-by-j-clay-singleton/

Prevailing Multiple Employer Plan offers four risk-based managed allocation portfolios. The Novus Managed Allocation PortfoliosTM are unique to the retirement plan industry. These portfolios are managed utilizing a core and satellite approach; each is comprised of an efficient allocation. Additionally, each portfolio is independently