Transcription

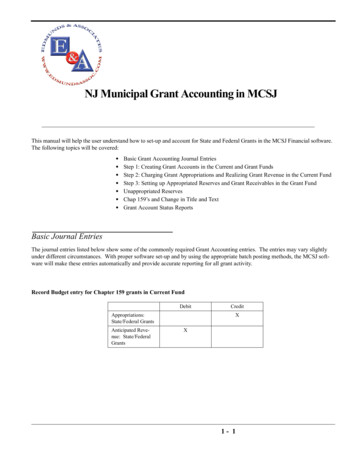

NJ Municipal Grant Accounting in MCSJThis manual will help the user understand how to set-up and account for State and Federal Grants in the MCSJ Financial software.The following topics will be covered: Basic Grant Accounting Journal EntriesStep 1: Creating Grant Accounts in the Current and Grant FundsStep 2: Charging Grant Appropriations and Realizing Grant Revenue in the Current FundStep 3: Setting up Appropriated Reserves and Grant Receivables in the Grant FundUnappropriated ReservesChap 159’s and Change in Title and TextGrant Account Status ReportsBasic Journal EntriesThe journal entries listed below show some of the commonly required Grant Accounting entries. The entries may vary slightlyunder different circumstances. With proper software set-up and by using the appropriate batch posting methods, the MCSJ software will make these entries automatically and provide accurate reporting for all grant activity.Record Budget entry for Chapter 159 grants in Current FundDebitAppropriations:State/Federal GrantsAnticipated Revenue: State/FederalGrantsCreditXX1- 1

Basic Journal EntriesCharge Grant Appropriations and Realize Grant Revenue in Current Fund (including match)DebitAppropriations:State/Federal GrantsCreditXAnticipated Revenue: State/FederalGrantsAppropriations:Local MatchXXDue to Grant Fund(Match)XSet-up Grant Spending Reserve, Receivable and Interfund for Local Match in Grant FundDebitGrants ReceivableXDue From Current(Match)XCreditAppropriatedReservesXRecord Receipts in Grant FundDebitCashCreditXGrants ReceivableXRecord Disbursements in Grant FundDebitAppropriatedReservesCreditXCashXRecord Receipts for Grants not Appropriated for in Current Fund BudgetDebitCashCreditXUnappropriatedReservesXNote: Cash entries will require accompanying interfund entries if Current Fund cash is used for grant receiptsand/or disbursements. The interfund entries are required in order to keep the current and grant funds inbalance.1-2

Step1: Create Grant Budget and Revenue AccountsApply Unappropriated Reserve against Grant ReceivableDebitUnappropriatedReservesCreditXGrants ReceivableXStep1: Create Grant Budget and Revenue AccountsWhen a grant will be included in the municipal budget (Adopted or Amended), at least 4 accounts will need to exist or be added tothe system. A budget and revenue account will be needed in the Current Fund and then separate budget and revenue account(s)will be needed in the Grant fund. The Current Fund accounts will simply be used to record and charge/realize the budget. TheGrant Fund accounts will be used for all cash disbursements and receipts. Any special grant sub account detail will be set-up in theGrant Fund.Current FundGrant budget accounts in the Current Fund should begin with a number and should be formatted according to the State FlexibleChart of Accounts. These accounts will only be used to hold and charge off the Current Fund appropriations. They are NOT usedto record grant disbursements. An example is provided in Figure 1-1.Current AppropriationsDue From/To Grant FundFigure 1-1Note: The Fund Type can be set to Budget or Grant. If Grant is selected, the Misc tab on the account will appearas shown in Figure 1-2. The user can assign the corresponding Current Fund grant revenue account,which will enable the system to tie the two accounts together in the Adopt/Amend Batch. The budgetedamount can then be posted once for grants with no match.1-3

Step1: Create Grant Budget and Revenue AccountsOptional link to Current Fund grantrevenue account.Figure 1-2Note: It is not necessary to fill out the Misc tab grant information on Current Fund accounts. This informationwill be updated on the Grant Fund accounts.Grant revenue accounts in the Current Fund should begin with a number and should be formatted according to the State FlexibleChart of Accounts. These accounts will only be used to hold the anticipated budget and realize grant revenue. They are NOT usedto record cash receipts. See Figure 1-3.Due From/To Grant FundAnticipated RevenuesFigure 1-31-4

Step1: Create Grant Budget and Revenue AccountsNote: The Revenue Journal line entries are only required if the Revenue Batch is used to realize Grant revenue.These lines can be left blank if revenue will be realized in the G/L Batch (as described in this manual).Grant FundThe Grant Fund budget accounts should start with a letter (G is recommended but not required) so that expenditures may berecorded over multiple fiscal years. These accounts should be used to record all grant disbursements. Any sub account detail youwish to set-up in order to track grant expenditures should be done in this fund.Note: E&A recommends that a new account be established for each grant appropriated during the year. In otherwords, separate accounts should exist for the 09 grant and the 08 grant with the same name. While the system will permit you to update the same G- account for each new award, the system reporting is bestdesigned to support separate accounts for each year.Appropriated ReservesCashInterfunds (if necessary)Figure 1-4Note: Account numbering for the G accounts is user defined. It is recommended that the account’s departmentsegment (702 in the above example) be unique for each unique grant name. The remaining segments canbe used to group grants by year, funding source, organize sub account detail, or any other grouping theuser feels is important.Notice the Fund Type is set to Grant. This will allow the user to record information about the grant on the Misc tab. See Figure1-5.1-5

Step1: Create Grant Budget and Revenue AccountsFigure 1-5Grant Fund revenue accounts should also start with a letter so that receipts may be recorded against the account over multiple fiscalyears. These accounts should be used to record all cash receipts and will maintain the grant’s receivable balance. See Figure 1-6.Grants ReceivableInterfunds (if necessary)Figure 1-6Note: Account numbering is user defined, but it is recommended the department segment (702 in the aboveexample) be unique for each grant name.1-6

Step2: Charging Grant Appropriations and Realizing Grant Revenue in the CurrentStep2: Charging Grant Appropriations and Realizing Grant Revenue inthe Current FundOnce the Current Fund municipal budget is adopted (or grants are added via a Chap. 159) and budgeted figures are posted to theaccounts, the anticipated revenue for each grant should be realized and the budget appropriation for each grant should be charged.Each grant should then be separately recorded in the State and Federal Grant Fund, where a grant receivable and spending reserveneed to be established. For grants requiring local matches, the budget appropriation for these matches should also be charged in theCurrent Fund and transferred to the spending reserve in the Grant Fund.G/L BatchThe best way to charge grant appropriations and realize grant revenue is by using the G/L Batch. The example below illustrateshow to post the entries for a single grant with a local match.Figure 1-7Note: When all grants have been charged, the debits to the grant budget will equal the credits to the grant revenue plus the credit to the Due From/To Grant Fund for any local matches appropriated in the budget.Charge Grant Appropriations and Realize Grant Revenue in Current Fund (including nt Local MatchXCreditAnticipated Revenue: GrantXDue to Grant Fund(Match)X1-7

Step3: Setting up Appropriated Reserves and Grants Receivables in Grant FundStep3: Setting up Appropriated Reserves and Grants Receivables inGrant FundAfter the grant budget appropriations have been charged and the anticipated revenue realized in the Current Fund, the grant spending reserves and receivables need to be established in the Grant Fund. If no grant matches are involved, the Adopt/Amend Batchcan be used to post the Grant budget in the grant fund. This batch will automatically post the G/L entry to set-up the Receivableand Appropriated Reserve G/L balances. If grant matches are involved, it is recommended that the user post the grant budgetthrough the budget and revenue account maintenance screens. Then, the manual entry to set-up the Receivable, AppropriatedReserves, and Interfund Receivable (Due From/To Current) should be posted in the G/L Batch.Note: The budgeted amounts posted in the Grant fund can be entered with either an Adopted or Chapter 159Reason code. If posted with an Adopted reason code, the budgeted amounts will appear in the CurrentBudgeted column on the current year’s Grant Account Status report. If posted with a Chapter 159 reasoncode, the amounts will appear in the Amended column of the current year’s Grant report. The Chapter 159reason is recommended for users who do not add new grant accounts for each year because they will beable to easily distinguish the newly appropriated amounts from the grant’s previous balance.Posting Budget in Account MaintenanceFigure 1-81-8

Step3: Setting up Appropriated Reserves and Grants Receivables in Grant FundFigure 1-9Figure 1-10Set-up Grant Spending Reserve, Receivable and Interfund for Local Match in Grant FundDebitGrants ReceivableXDue From Current(Match)XCreditAppropriatedReservesX1-9

Step3: Setting up Appropriated Reserves and Grants Receivables in Grant FundUsing Adopt/Amend (Only recommended if no grant matches)Figure 1-11Figure 1-12Set-up Grant Spending Reserve, Receivable in Grant FundDebitGrants ReceivableAppropriatedReservesCreditXX1 - 10

Unappropriated ReservesUnappropriated ReservesAt times, money may be received for grants that have not yet been appropriated in the Current Fund budget. Since no spendingreserve or receivable has been established, this money needs to be receipted against a liability account called UnappropriatedReserves in the Grant Fund. Eventually, the grant will be appropriated in the Current Fund budget, usually via a Chapter 159 resolution, which will allow the spending reserve and receivable to be established in the Grant Fund. Then, the UnappropriatedReserve balance can be applied against the grant’s receivable balance.In order to post receipts of Unappropriated Reserves, revenue accounts should be established for any grants where unappropriatedfunds are received. While the account number is user definable, E&A recommends that G- accounts be established to handle thesereceipts. Most importantly, the accounts should be numbered in a fashion that keeps them separate from the Grant Receivable revenue accounts on the Grant Revenue Status report. An account example is below:Unappropriated ReservesFigure 1-13To apply an Unappropriated Reserve balance against the Grant Receivable balance, the entry should be recorded in the G/L Batch.See the following example:Figure 1-14Apply Unappropriated Reserve against Grant ReceivableDebitUnappropriatedReservesCreditXGrants ReceivableX1 - 11

Chapter 159’s and Change in Title and TextChapter 159’s and Change in Title and TextMany times, grant rewards will not be known at the time of budget adoption. Consequently, a Chapter 159 resolution is needed toinsert the grant budget appropriation and anticipated revenue into the Current Fund budget. If a match is required (may require anemergency appropriation), then a Change in Title and Text amendment is needed to shift the amount for the Matching Funds forGrants appropriation to the newly appropriated grant. Once this is accomplished in the MCSJ system, the grant process is no different than you would follow for grants that are part of the original adopted budget.The Chapter 159 budget amendment can be entered on the Current Fund accounts through the Account Maintenance screens orusing the Adopt/Amend Batch. If the account maintenance screen is used, be sure to choose the Chap 159 reason code. The G/Lentry to reflect the budget amendment will also have to be posted in the G/L Batch:Db Anticipated RevenuesCr Current AppropriationsThe screens below illustrate a Chapter 159 amendment entered in the Adopt/Amend Batch:Figure 1-15Figure 1-16A Change in Title and Text budget amendment can be posted through the Budget Account Maintenance screen or by using theAdopt/Amend Batch. When posting through the Account Maintenance, simply change the budgeted figures on the budget1 - 12

Chapter 159’s and Change in Title and Textaccounts and choose the Chg Title/Text reason code. The screens below illustrate a Change in Title and Text amendment entered inthe Adopt/Amend Batch.Figure 1-17Grant ABCMatching Funds for.Figure 1-18Note: No journal entry is required in the G/L to reflect a Change in Title and Text.After you have completed the budget postings for the Chapter 159 and Change in Title and Text (if needed), charge the budgetedamounts off in the Current Fund and set up the spending and receivable balances in the Grant Fund as described in steps 2 and 3 ofthis manual.1 - 13

Grant ReportsGrant ReportsGrant Account Status - BudgetThis is a Budget Account Status report designed especially for lettered grant accounts. Since Grant type accounts may span multiple budget years, the report requires the user to enter an Opening Balance Budget Year. This enables the user to view an openingbalance at the start of the year and to see only current year activity totals. The report also contains additional grant related featuressuch an Original Grant column and the ability to print miscellaneous grant information from the Misc tab in Budget Account Maintenance. When run for the appropriate range of accounts, this report should tie back to the G/L Appropriated Reserves balance.Select Finance Budget Account Grant Account Status.Figure 1-19Grant Account Status - RevenueThis is a Revenue Account Status report designed especially for lettered grant revenue accounts. Since these lettered accounts mayspan multiple budget years, the report requires the user to enter a Year for YTD Totals. This enables the report to show separatecurrent and prior year activity totals. When run for the appropriate range of accounts, this report should tie back to the G/L GrantReceivable balance.Select Finance Revenue Grant Account Status.1 - 14

Grant ReportsFigure 1-20.1 - 15

This manual will help the user understand how to set-up and acco unt for State and Federal Grants in the MCSJ Financial software . The following topics will be covered: Basic Grant Accounting Journal Entries Step 1: Creating Grant Accounts in the Current and Grant Funds