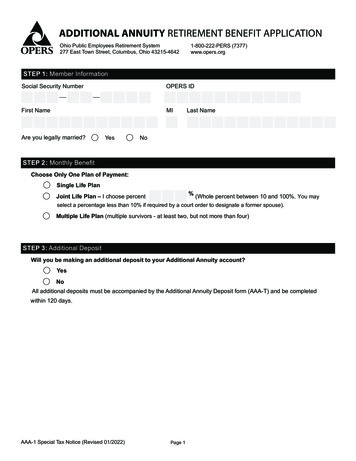

Transcription

ADDITIONAL ANNUITY RETIREMENT BENEFIT APPLICATIONOhio Public Employees Retirement System277 East Town Street, Columbus, Ohio 43215-46421-800-222-PERS (7377)www.opers.orgSTEP 1: Member InformationSocial Security NumberOPERS IDFirst NameMIAre you legally married?YesLast NameNoSTEP 2: Monthly BenefitChoose Only One Plan of Payment:Single Life Plan% (Whole percent between 10 and 100%. You mayJoint Life Plan – I choose percentselect a percentage less than 10% if required by a court order to designate a former spouse).Multiple Life Plan (multiple survivors - at least two, but not more than four)STEP 3: Additional DepositWill you be making an additional deposit to your Additional Annuity account?YesNoAll additional deposits must be accompanied by the Additional Annuity Deposit form (AAA-T) and be completedwithin 120 days.AAA-1 Special Tax Notice (Revised 01/2022)Page 1

STEP 4: Member Banking Information for Monthly AnnuityBank NameBank Routing NumberAccount Number(Choose only one)CheckingExample Check aV lid routing numbers begin with 0,1, 2 or 3-OR-SavingsBank Routing NumberAccount NumberSTEP 5: Beneficiary Information (You must provide at least one beneficiary. Does NOT apply to the Lump Sum Option)1. First NameMISocial Security NumberBirth DateLast NameGenderMaleFemalePrefer Not To SayRelationship to MemberSpouseChildOther Allocation (Multiple Life Plan only)2. First NameMISocial Security NumberBirth Date%Last NameGenderMaleFemalePrefer Not To SayRelationship to MemberSpouseChildOther Allocation (Multiple Life Plan only)AAA-1 Special Tax Notice (Revised 01/2022)Page 2%

STEP 6: Spousal ConsentMEMBER: If you are married at the time you apply for an annuity payment, this step (6) must be completed by yourspouse and signed in the presence of a Notary Public when the application is completed in full. Spousal consent isirrevocable.State ofBeing duly sworn, I,County of., the undersigned,Print member’s spouse nameam the spouse of.Print member nameUpon reviewing the distribution options, the plans of payment, and reviewing my spouse’s beneficiary designation, I amconsenting to the plan of payment my spouse selected and the beneficiary(ies) designated.Spouse SignatureSworn and subscribed to me thisday ofToday’s Date///, 20Notary Public My commission expiresAAA-1 Special Tax Notice (Revised 01/2022)/Page 3

STEP 7: Member AcknowledgmentThis step must be completed and signed in the presence of a Notary Public when the application is completedin full.State of, County of.Being duly sworn, I, the undersigned, state that the information I provided in this Application is complete and true to thebest of my knowledge and belief.I acknowledge I have selected a plan of payment and designated a beneficiary on my OPERS additional annuityaccount in Steps 2 and 5 of this application in accordance with any court orders issued under the laws of this state oranother state regarding the division of marital property, received by OPERS, and to which I may be subject.Member SignatureSworn and subscribed to me thisday ofToday’s Date/, 20Notary Public My commission expires /Ohio Public Employees Retirement System277 East Town Street, Columbus, Ohio 43215-4642//1-800-222-PERS (7377)AAA-1 Special Tax Noticewww.opers.org (Revised 01/2022)

SPECIAL TAX NOTICE REGARDING OPERS PAYMENTSOhio Public Employees Retirement System277 East Town Street, Columbus, Ohio 43215-46421-800-222-PERS (7377)www.opers.orgYou are receiving this notice because all or a portion of a payment you are receiving from the Ohio Public EmployeesRetirement System (OPERS) is eligible to be rolled over to an IRA or an employer plan. This notice is intended to helpyou decide whether to do such a rollover. This notice describes the rollover rules that apply to payments from OPERSthat are not from a designated Roth account (a type of account in some employer plans that is subject to special taxrules). Rules that apply to most payments from a plan are described in the “General Information About Rollovers”section. Special rules that only apply in certain circumstances are described in the “Special Rules and Options” section.If you have additional questions after reading this notice, you can contact an OPERS Member Services Representativeat 1-800-222-7377 or a professional tax advisor. Please do not return this notice to OPERS, but keep this notice withyour other important documents.General Information About RolloversHow can a rollover affect my taxes?You will be taxed on a payment from OPERS if you donot roll it over. If you are under age 59½ and do not do arollover, you will also have to pay a 10 percent additionalincome tax on early distributions (generally, distributionsmade before age 59½), unless an exception applies.However, if you do a rollover, you will not have to paytax until you receive payments later and the 10 percentadditional income tax will not apply if those payments aremade after you are age 59½ (or if an exception to the10% additional income tax applies).should contact the IRA sponsor or the administrator ofthe employer plan for information on how to do a directrollover.If you do not do a direct rollover, you may still doa rollover by making a deposit into an IRA or eligibleemployer plan that will accept it. Generally, you willhave 60 days after you receive the payment to makethe deposit. If you do not do a direct rollover, OPERS isrequired to withhold 20 percent of the payment for federalincome taxes. This means that, in order to roll over theentire payment in a 60-day rollover, you must use otherfunds to make up for the 20 percent withheld. If you donot roll over the entire amount of the payment, the portionnot rolled over will be taxed and will be subject to the 10percent additional income tax on early distributions if youare under age 59½ (unless an exception applies).What types of retirement accounts and plans mayaccept my rollover?You may roll over the payment to either an IRA (anindividual retirement account or individual retirementannuity, including a Simple IRA that has been in existencefor at least two years) or an employer plan (a tax-qualifiedplan, section 403(b) plan, or governmental section 457(b)plan) that will accept the rollover. The rules of the IRA oremployer plan that holds the rollover will determine yourinvestment options, fees and rights to payment from theIRA or employer plan (for example, IRAs are not subjectto spousal consent rules and IRAs may not provideloans). Further, the amount rolled over will becomesubject to the tax rules that apply to the IRA or employerplan.How much may I roll over?If you wish to do a rollover, you may roll over all or partof the amount eligible for rollover. Any payment fromOPERS is eligible for rollover, except: Certain payments spread over a period of at least10 years or over your life or life expectancy (or thejoint lives or joint life expectancies of you and yourbeneficiary); Required minimum distributions after age 70½ (if youwere born before July 1, 1949) or age 72 (if you wereborn after June 30, 1949) or after death; and Corrective distributions of contributions that exceedtax law limitations.OPERS can tell you what portion of a payment is eligiblefor rollover.How do I do a rollover?There are two ways to do a rollover. You can do either adirect rollover or a 60-day rollover.If you do a direct rollover, OPERS will make thepayment directly to your IRA or an employer plan. YouSpecial Tax Notice (01/2022)1

General Information About Rollovers (continued)If I don’t do a rollover, will I have to pay the 10 percentadditional income tax on early distributions?If you are under age 59½, you will have to pay the 10percent additional income tax on early distributions forany payment from OPERS (including amounts withheldfor income tax) that you do not roll over, unless one of theexceptions listed below applies. This tax applies to the partof the distribution that you must include in income and is inaddition to the regular income tax on the payment not rolledover.expenses (without regard to whether you itemizedeductions for the taxable year).If I do a rollover to an IRA, will the 10 percent additionalincome tax apply to early distributions from the IRA?If you receive a payment from an IRA when you areunder age 59½, you will have to pay the 10 percentadditional income tax on early distributions on the part ofthe distribution that you must include in income, unlessan exception applies. In general, the exceptions to the 10percent additional income tax for early distributions froman IRA are the same as the exceptions listed above forearly distributions from a plan. However, there are a fewdifferences for payments from an IRA, including: The exception for payments made after you separatefrom service if you will be at least age 55 in the yearof the separation (or age 50 for qualified public safetyemployees) does not apply The exception for division of property orders (DPOs)does not apply (although a special rule applies underwhich, as part of a divorce or separation agreement, atax-free transfer may be made directly to an IRA of aspouse or former spouse). The exception for payments made at least annuallyin equal or close to equal amounts over a specifiedperiod applies without regard to whether you have had aseparation from service. Additional exceptions apply for payments from an IRAincluding: Payments for qualified higher educationexpenses; Payments up to 10,000 used in aqualified first-time home purchase; and Payments forhealth insurance premiums after you have receivedunemployment compensation for 12 consecutive weeks(or would have been eligible to receive unemploymentcompensation but for self-employed status).The 10 percent additional income tax does not apply to thefollowing payments from OPERS: Payments made after you separate from service if youwill be at least age 55 in the year of theseparation; Payments that start after you separate from service ifpaid at least annually in equal or close to equal amountsover your life or life expectancy (or the joint lives or jointlife expectancies of you and your beneficiary); Payments from a governmental plan made after youseparate from service if you are a qualified public safetyemployee and you will be at least age 50 in the year ofthe separation; Payments made due to disability; Payments after your death; Corrective distributions of contributions that exceed taxlaw limitations; Payments made directly to the government to satisfy afederal tax levy; Payments made under a division of property order(DPO); Payments of up to 5,000 made to you from a definedcontribution plan if the payment is a qualified birth oradoption distribution ; Payments excepted from the additional income tax byfederal legislation relating to certain emergencies anddisasters; Payments up to the amount of your deductible medicalWill I owe state income taxes?This notice does not address any state or local income taxrules (including withholding rules).Special Rules and OptionsIf your payment includes after-tax contributionsAfter-tax contributions included in a payment are not taxed.If you receive a partial payment of your total benefit, anallocable portion of your after-tax contributions is included inthe payment, so you cannot take a payment of only after-taxcontributions. In addition, special rules apply when you do arollover, as described below. You may roll over to an IRA apayment that includes after-tax contributions through eithera direct rollover or a 60-day rollover. You must keep trackof the aggregate amount of the after-tax contributions in allSpecial Tax Notice (01/2022)of your IRAs (in order to determine your taxable income forlater payments from the IRAs). If you do a direct rollover ofonly a portion of the amount paid from OPERS and at thesame time the rest is paid to you, the portion rolled overconsists first of the amount that would be taxable if not rolledover. For example, assume you are receiving a distributionof 12,000, of which 2,000 is after-tax contributions. In thiscase, if you roll over 10,000 to an IRA that is not a RothIRA, no amount is taxable because the 2,000 amount notrolled over is treated as being after-tax contributions.2

Special Rules and Options (continued)If you do a direct rollover of the entire amount paid fromOPERS to two or more destinations at the same time,you can choose which destination receives the after-taxcontributions.rolled over out of the Roth IRA within the five-year period thatbegins on Jan. 1, of the year of the rollover, the 10 percentadditional income tax will apply (unless an exception applies).If you roll over the payment to a Roth IRA, later paymentsfrom the Roth IRA that are qualified distributions will notbe taxed (including earnings after the rollover). A qualifieddistribution from a Roth IRA is a payment made after you areage 59½ (or after your death or disability, or as a qualifiedfirst-time homebuyer distribution of up to 10,000) and afteryou have had a Roth IRA for at least five years. In applyingthis 5-year rule, you count from Jan. 1, of the year for whichyour first contribution was made to a Roth IRA. Paymentsfrom the Roth IRA that are not qualified distributions will betaxed to the extent of earnings after the rollover, includingthe 10 percent additional income tax on early distributions(unless an exception applies). You do not have to takerequired minimum distributions from a Roth IRA during yourlifetime. For more information, see IRS Publication 590-A,Contributions to Individual Retirement Arrangements (IRAs)and IRS Publication 590-B, Distribution from IndividualRetirement Arrangements (IRAs).Similarly, if you do a 60-day rollover to an IRA of only aportion of a payment made to you, the portion rolled overconsists first of the amount that would be taxable if not rolledover. For example, assume you are receiving a distributionof 12,000, of which 2,000 is after-tax contributions, andno part of the distribution is directly rolled over. In thiscase, if you roll over 10,000 to an IRA that is not a RothIRA in a 60-day rollover, no amount is taxable because the 2,000 amount not rolled over is treated as being aftertax contributions. You may roll over to an employer planall of a payment that includes after-tax contributions, butonly through a direct rollover (and only if the receiving planseparately accounts for after-tax contributions and is not agovernmental section 457(b) plan). You can do a 60-dayrollover to an employer plan of part of a payment thatincludes after-tax contributions, but only up to the amount ofthe payment that would be taxable if not rolled over.If you miss the 60-day rollover deadlineGenerally, the 60-day rollover deadline cannot be extended.However, the IRS has the limited authority to waive thedeadline under certain extraordinary circumstances, suchas when external events prevented you from completingthe rollover by the 60-day rollover deadline. Under certaincircumstances, you may claim eligibility for a waiver of the60-day rollover deadline by making a written self-certification.Otherwise, to apply for a waiver from the IRS, you mustfile a private letter ruling request with the IRS. Private letterruling requests require the payment of a nonrefundableuser fee. For more information, see IRS Publication 590-A,Contributions to Individual Retirement Arrangements (IRAs).If you are not a plan participantPayments after death of the participant. If you receive adistribution after the participant’s death that you do not rollover, the distribution will generally be taxed in the samemanner described elsewhere in this notice. However, the10 percent additional income tax on early distributions andthe special rules for public safety officers do not apply, andthe special rule described under the section “If you wereborn on or before Jan. 1, 1936,” applies only if the deceasedparticipant was born on or before Jan. 1, 1936.If you are a surviving spouse. If you receive a paymentfrom OPERS as the surviving spouse of a deceasedparticipant, you have the same rollover options that theparticipant would have had, as described elsewhere in thisnotice. In addition, if you choose to do a rollover to an IRA,you may treat the IRA as your own or as an inherited IRA.An IRA you treat as your own is treated like any other IRAof yours, so that payments made to you before you are age59½ will be subject to the 10 percent additional incometax on early distributions (unless an exception applies) andrequired minimum distributions from your IRA do not have tostart until after you are age 70½ (if you were born before July1, 1949) or age 72 (if you were born after June 30, 1949).If you treat the IRA as an inherited IRA, payments from theIRA will not be subject to the 10 percent additional incomeIf you were born on or before Jan. 1, 1936If you were born on or before Jan. 1, 1936, and receive alump sum distribution that you do not roll over, special rulesfor calculating the amount of the tax on the payment mightapply to you. For more information, see IRS Publication 575,Pension and Annuity Income.If you roll over your payment to a Roth IRAIf you roll over the payment from OPERS to a Roth IRA, aspecial rule applies under which the amount of the paymentrolled over (reduced by any after-tax amounts) will be taxed.In general, the 10 percent additional income tax on earlydistributions will not apply. However, if you take the amountSpecial Tax Notice (01/2022)3

Special Rules and Options (continued)tax on early distributions. However, if the participant hadstarted taking required minimum distributions, you will haveto receive required minimum distributions from the inheritedIRA. If the participant had not started taking requiredminimum distributions from OPERS, you will not have to startreceiving required minimum distributions from the inheritedIRA until the year the participant would have been age 70½(if the participant was born before July 1, 1949) or age 72 (ifthe participant was born after June 30, 1949).If you are a surviving beneficiary other than a spouseIf you receive a payment from OPERS because of theparticipant’s death and you are a designated beneficiaryother than a surviving spouse, the only rollover option youhave is to do a direct rollover to an inherited IRA. Paymentsfrom the inherited IRA will not be subject to the 10 percentadditional income tax on early distributions. You will haveto receive required minimum distributions from the inheritedIRA.Payments under a division of property orderIf you are the spouse or former spouse of the participant whoreceives a payment from OPERS under a DPO you generallyhave the same options and the same tax treatment theparticipant would have (for example, you may roll over thepayment to your own IRA or an eligible employer plan thatwill accept it). However, payments under the DPO will notbe subject to the 10 percent additional income tax on earlydistributions.If you are a nonresident alienIf you are a nonresident alien and you do not do a directrollover to a U.S. IRA or U.S. employer plan, instead ofwithholding 20 percent, OPERS is generally required towithhold 30 percent of the payment for federal incometaxes. If the amount withheld exceeds the amount of taxyou owe (as may happen if you do a 60-day rollover), youmay request an income tax refund by filing Form 1040NRand attaching your Form 1042-S. See Form W-8BEN forclaiming that you are entitled to a reduced rate of withholdingunder an income tax treaty. For more information, seeIRS Publication 519, U.S. Tax Guide for Aliens, and IRSPublication 515, Withholding of Tax on Nonresident Aliensand Foreign Entities.Other special rulesIf your payments for the year are less than 200, OPERSis not required to allow you to do a direct rollover and is notrequired to withhold federal income taxes. However, youmay do a 60-day rollover. You may have special rolloverrights if you recently served in the U.S. Armed Forces. Formore information on special rollover rights related to the U.S.Armed Forces, see IRS Publication 3, Armed Forces’ TaxGuide. You also may have special rollover rights if you wereaffected by a federally declared disaster (or similar event),or if you received a distribution on account of a disaster. Formore information on special rollover rights related to disasterrelief, visit the IRS website, www.irs.gov.Your Right to Waive the 30-Day Notice PeriodGenerally, neither a direct rollover nor a payment can be made from OPERS until at least 30 days after your receipt ofthis notice. Thus, after receiving this notice, you have at least 30 days to consider whether or not to have your withdrawaldirectly rolled over. If you do not wish to wait until this 30 day notice period ends before your election is processed,you may waive this notice period by making an affirmative election indicating whether or not you wish to make a directrollover. Your withdrawal will then be processed in accordance with your election as soon as practical after it is receivedby OPERS.Your Right to Receive this NoticeIf you receive an electronic version of this notice via the OPERS website, you may also receive this notice on a writtenpaper document by calling OPERS at 1-800-222-7377. Upon receipt of your request, this notice on a written paperdocument will be sent to you at no charge.For More InformationYou may wish to consult with a professional tax advisor before taking a payment from OPERS. You can find moredetailed information on the federal tax treatment of payments from employer plans in: IRS Publication 575, Pension andAnnuity Income; IRS Publication 590-A, Contributions to Individual Retirement Arrangements (IRAs) and IRS Publication590-B, Distribution from Individual Retirement Arrangements (IRAs); and IRS Publication 571, Tax-Sheltered AnnuityPlans (403(b) Plans). These publications are available from a local IRS office, online at www.irs.gov, or by calling1-800-TAX-FORM.Special Tax Notice (01/2022)4

ADDITIONAL ANNUITY RETIREMENT BENEFIT APPLICATION Page 1 1-800-222-PERS (7377) www.opers.org AAA-1 Special Tax Notice (Revised 01/2022) STEP 2: Monthly Benefit Choose Only One Plan of Payment: Single Life Plan Joint Life Plan - I choose percent % (Whole percent between 10 and 100%. You may