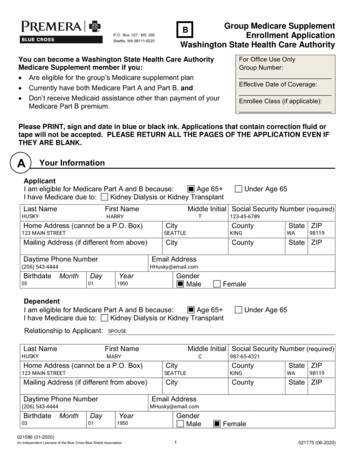

Transcription

Medicare Advantage vs.Medicare Supplement:Philosophical Differences that ImpactCoverageRose CookBlue Cross Blue Shield of MichiganY0074 S AAApresentation FVNR1

Michigan Medicare MarketThere are 1,964,716 Medicare-eligible people in Michigan44% are in Traditional Medicare36% are in Medicare Advantage plans20% are in Medicare Supplement : MA number includes ALL MA lives (group, individual and SNP) as of1/1/17; Medicare Supplement includes all lives as of 12/31/15.Source: Mark FarrahRepresents Individual and Group MA and MAPD membership2

Medicare: Many Choices, Much ConfusionMedicare can bedaunting dozens of plans tochoose from, complex rules tofollow give rise to criticalquestions:3

Medicare: Many Choices, Much Confusion Will I have enough money for healthcareand retirement? Will I have access to the care I need? Will my Medicare benefits run out? Will I lose Part A and Part B if I get aMedicare Advantage plan? Wouldn’t it be better to wait to get PartD prescription drug coverage until I needto take prescriptions regularly? If I decide not to retire now, should I signup for Medicare anyway and beginpaying Part B premiums?4

The Building Blocks of MedicareÀ La Carte Coverage: Part A: Hospital Coverage Part B: Medical Coverage Part D: Prescription Drugs MedigapMedigapPart D:PrescriptionDrugsPart A:HospitalPart B:Medical5

The Building Blocks in a Single PlanPart C:Hospital Medical PrescriptionDrugs MoreMedicare Advantage plans Part C plans combine Part A and B Many plans offer prescription drugcoverage Some plans offer preventive healthprograms, free fitnessmemberships and added benefits Convenience of one cardYou can save by bundling Medicareparts together, combining benefitsinto a single package.6

À La Carte vs. Combination – An AnalogyTravel AccommodationsÀ La CartePay separately for: Two night hotel stayParkingBreakfastWi-FiCombo DealWeekend Package includes: Two night hotel stay Parking Complimentary BreakfastBar Free Wi-Fi7

Pay for What You WantTravel AccommodationsÀ La Carte Two night hotel stayTook the trainBreakfast with the familyUsing 4GCombo Deal/WeekendPackage Two night hotel stayParking includedComplimentary Breakfast BarFree Wi-Fi8

Who’s Directing Your Health Care?One key difference is whether you want a “Do-It-Yourself” approach,or if you want your doctor to help oversee your care.Medigap Do-It-Yourself approach: you visitthe doctor(s) you want, no needfor referrals You coordinate call for your labtests, etc. your care andinteractions across different healthcare providers You track your medical records,billing, etc. across different plans9

Who’s Directing Your Health Care?Medicare Advantage Guided care approach encourages yourprimary care physician involvement incoordinating your care In an HMO, your Primary Care Physiciancoordinates your care with specialists andoversees your overall health and care Summarizes your medical, hospital and otherclaims in one organization (some havemember portals for ready access andtracking)10

Coverage to Keep You HealthyAnother difference is whether preventive and wellness services arecovered by the plan.MedigapMedicare Advantage Covers the medical service, but notthe oversightCare management programs are notcovered, you have to pay out-of pocketNo preventive exams for dental,vision, hearing are covered Ready access to health information:nursing hotlines, online MedicareresourcesCare management for those withchronic illnessesFitness programs and incentives tolose weight, get fit, stop smokingPreventive dental, vision, hearingexamsPrimary care physician involvement isencouraged in coordinating your care11

FlexibilityAnother key difference is where you can get services.MedigapMedicare Advantage Covers any doctor who takesMedicare nationwideIt’s up to the discretion of thephysician or provider to supply youwith services – there is nocommitment in place with theinsurance company who issued theMedigap policySome Medigap plans coveremergency care worldwide Networks of doctors and hospitalsmake contractual agreements with thehealth plan to provide you care. Theyare committed to see youScope of the network can benationwide, statewide or morelocalized. If you see in-networkproviders, you tend to have lessexpensive rates. Some plans (PPO,HMO-POS) may provide out of networkcoverage at higher ratesWorldwide coverage – some planscover emergency services12

Premiums Based on Individual or aPool of BeneficiariesMedicare SupplementMedicare Advantage Most are underwritten, factoring inage, gender, health status (BodyMass Index, smoking history)Premium rates increase with yourage (and with overall healthcare costincreases) Rates typically vary within a plan byregion, since healthcare costs alsovary by regionAge, gender, claims, health status donot affect premium ratesCosts for higher utilization arecovered by copays, coinsurance anddeductibles in addition to premiums,so rates can be more stable year toyear13

Can I Get Denied Coverage?Medicare SupplementMedicare Advantage During the first six months after youturn 65, you have “GuaranteedIssue," which means you will beaccepted for coverage and will retainit as long as you have the plan Everyone who is eligible for Medicareand who has Part B can enroll in aMedicare Advantage plan, exceptindividuals with End Stage RenalDisease (ESRD) If you’re eligible for a SpecialEnrollment Period (SEP) for a varietyof other reasons, you wouldn’t haveto go through underwriting You must reside in the state for atleast six months of the year to qualifyfor Medicare Advantage plans in yourstate You could be denied coverage basedon your health status applying afterthis window You must continue to pay Part Bpremiums to maintain Medigap plancoverage You must continue to pay Part Bpremiums to maintain Medigap plancoverage14

Self AssessmentWhat’s most important to me?CostPaying thelowest premiumper month Local or In-State NetworkHaving themaximumpossiblecoverageKeeping mydoctor(s)Having access tothe hospital(s) Iwant to useOut-of-StateNetworkCoveragethroughout theUS when I travelfor the winterConvenience: one card, one Explanation of BenefitsBenefits: Care Management, 24-hour nurse hotline, etc.Coverage for non-medical services such as dental, vision, hearingGuidance to navigate the complex Medicare system15

At a Glance ComparisonMedigap – A La CarteMedicare Advantage - ComboMonthly Premium 40 - 342Varies by age, gender, healthstatus, county 0- 294Varies by countyPrescription DrugsNever includedOften includedMaximum Out of Pocket,AnnuallyNo cap on expenses 3,200 - 6,400Health & Wellness SupportCan be purchased, not coveredSome have nursing hotlines,weight management programs,fitness membership, etc.Access Based on HealthNeed to be accepted byunderwriting*Accept everyone but ESRDPremiums Based on AgeMost increase premium by age,health statusPremiums vary only by servicearea/rating region* Outside of Guarantee Issue period16

What Drives the Cost of a Medigap Plan Factors underwriters may consider for Medigap premiums:– Your age– Your smoking habits– Your weight– Where you live17

Additional Expenses With a Medigap Plan Factors that can increase your costs, not covered by Medigap plan:– Your prescription drugs– Where you travel: international travel is often not covered– Preventive dental needs– Vision exam and glasses/contacts– Hearing exam and hearing aids– Durable medical equipment18

What Drives the Cost of a MedicareAdvantage Plan Factors that determine Medicare Advantage premiums:– Where you live: rates vary by rating region– Low monthly premiums tend to be balanced by higherdeductibles– Type of plan you choose: Plan with prescription drug coverage Plan with fitness benefits Plan with preventive dental, vision, hearing benefits19

Additional Expenses with a MedicareAdvantage Plan Factors that can increase your costs, not covered by MedicareAdvantage plans:– Where you travel: out-of-state not in network for someregional MA plans– Choosing plan with coinsurance vs. copays for doctor visits,ambulance, etc.– Vision exam and glasses/contacts (some plans don’t cover)– Hearing exam and hearing aids (some plans don’t cover)20

How Can You Reduce YourCosts? Switch to an in-network doctor Switch to an in-network hospital Pay a higher medical and/or drugdeductible to reduce monthly premiums Pay for prescription drugs out-of-pocket Pay out-of-network costs when youtravel out of state21

MEDICARE SUPPLEMENTAt-a-Glance RecapMedigapMedicare Advantage Monthly premiums range for 40- 342 Low monthly premiums, some as little as 0 Medically underwritten out of GuaranteedIssue period Never medically underwritten, not age rated Rates can increase as the member growsolder: gender distinct rates are common –can rate for BMI and tobacco usage Nationally standardized plans Never have Part D included No medical management programs No extras Can use any provider that accepts OriginalMedicare All rates are the same regardless of age orgender Plans must include all Medicare coveredexpenses - carriers can add additional benefits Most plans include Part D prescriptioncoverage Personalized Care Management included Many plans have built in extras – preventativedental, vision exam, frame and lensallowance, hearing exam, hearing aidallowance National provider network22

Questions?Resources to help you understand Medicare and Medicare plan options:– Medicare.gov– Agents (must be certified to sell Medicare Advantage plans). Available byphone or schedule office or home visit– AAA– Insurance carriers’ websites, literature, mailings23

Medicare 44% Medicare Supplement 20% Medicare Advantage 36% Note: MA number includes ALL MA lives (group, individual and SNP) as of 1/1/17; Medicare Supplement includes all lives as of 12/31/15. Source: Mark Farrah Represents Individual and Group MA and MAPD membership There are 1,964,716 Medicare-eligible people in Michigan 44% are in .