Transcription

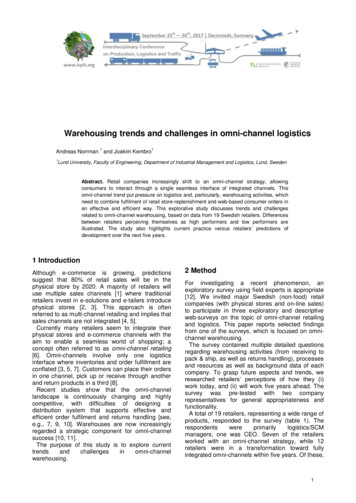

Warehousing trends and challenges in omni-channel logistics1Andreas Norrman and Joakim Kembro11Lund University, Faculty of Engineering, Department of Industrial Management and Logistics, Lund, SwedenAbstract. Retail companies increasingly shift to an omni-channel strategy, allowingconsumers to interact through a single seamless interface of integrated channels. Thisomni-channel trend put pressure on logistics and, particularly, warehousing activities, whichneed to combine fulfilment of retail store-replenishment and web-based consumer orders inan effective and efficient way. This explorative study discusses trends and challengesrelated to omni-channel warehousing, based on data from 19 Swedish retailers. Differencesbetween retailers perceiving themselves as high performers and low performers areillustrated. The study also highlights current practice versus retailers’ predictions ofdevelopment over the next five years.1 IntroductionAlthough e-commerce is growing, predictionssuggest that 80% of retail sales will be in thephysical store by 2020. A majority of retailers willuse multiple sales channels [1] where traditionalretailers invest in e-solutions and e-tailers introducephysical stores [2, 3]. This approach is oftenreferred to as multi-channel retailing and implies thatsales channels are not integrated [4, 5].Currently many retailers seem to integrate theirphysical stores and e-commerce channels with theaim to enable a seamless world of shopping; aconcept often referred to as omni-channel retailing[6]. Omni-channels involve only one logisticsinterface where inventories and order fulfillment areconflated [3, 5, 7]. Customers can place their ordersin one channel, pick up or receive through anotherand return products in a third [8].Recent studies show that the omni-channellandscape is continuously changing and highlycompetitive, with difficulties of designing adistribution system that supports effective andefficient order fulfilment and returns handling [see,e.g., 7, 9, 10]. Warehouses are now increasinglyregarded a strategic component for omni-channelsuccess [10, 11].The purpose of this study is to explore g.2 MethodFor investigating a recent phenomenon, anexploratory survey using field experts is appropriate[12]. We invited major Swedish (non-food) retailcompanies (with physical stores and on-line sales)to participate in three exploratory and descriptiveweb-surveys on the topic of omni-channel retailingand logistics. This paper reports selected findingsfrom one of the surveys, which is focused on omnichannel warehousing.The survey contained multiple detailed questionsregarding warehousing activities (from receiving topack & ship, as well as returns handling), processesand resources as well as background data of eachcompany. To grasp future aspects and trends, weresearched retailers’ perceptions of how they (i)work today, and (ii) will work five years ahead. Thesurvey was pre-tested with two companyrepresentatives for general appropriateness andfunctionality.A total of 19 retailers, representing a wide range ofproducts, responded to the survey (table 1). Therespondentswereprimarilylogistics/SCMmanagers; one was CEO. Seven of the retailersworked with an omni-channel strategy, while 12retailers were in a transformation toward fullyintegrated omni-channels within five years. Of these,1

3rd Interdisciplinary Conference on Production, Logistics and Traffic (ICPLT)11 represented multi-channels, while one currentlyonly had one physical store (“Other”).Table 1. RespondentsMultichannelOmnichannelFashion and jewellery12Sport equipment1Home interior and furniture2Consumer electronicsSpare parts and accessories tovehiclesBuilding materials 131121111DrugsDepartment Store2Total117Having too few respondents to draw statisticalsignificant conclusions, we instead develop insightsby a more qualitative analysis and illustrative patternmatching, reporting at least qualitative tendenciesand trends.We are looking for general patterns as well aspotential differences between channel type, orbetween perceived high and low performers (figure1). To divide high performers from low performers,we used their own perceptions of performance intwo aspects: cost efficiency and delivery service,both for web-orders and store deliveries, comparedto industry competitors. This approach makes itpossible to observe what retailers perceivingthemselves as leaders do differently from retailersperceiving themselves as laggards.A Likert scale from 1 (“agree to a very lowdegree”) to 7 (“agree to a very high degree”) wasused to understand their perceptions. Highperformers (average performance above 5) weremostly omni-channel companies (OC), while lowperformers (average performance below 3,75) weremulti-channel companies (MC) together with the“other” company.Highperf.311113211196418Total performance(both consumer web-orders and store replenishment-orders)7Highperformers6Cost efficiencyProduct 1234567Delivery serviceFigure 1. Respondents’ perceived performance.3 FindingsTwo trends are already described: the trend towardomni-channel (all respondents’ aim within fiveyears), and the tendency that OCs seem to performbetter in cost and service than MCs. In five years, allcompanies plan to increase performance to bebetter than industry competitors.But respondents find challenges related to omnichannel warehousing (figure 2). A major challenge(especially for MC, and low performers) will be touse retail stores as material handling/logisticsnodes. Besides, more challenging activities (for alltype of retailers) are packing & shipping, picking,and returns handling. (Return handling especially forlow performers).2

3rd Interdisciplinary Conference on Production, Logistics and Traffic (ICPLT)How large are the challenges related to Omni-channelfor different material handling/DC activities?0%20%40%60%80%Perception of warehousing activities compared tocompetitors in industry/segment100%ReceivingA) Picking a mix ofconsumer/web- and storereplenishment orders87Put-awayB) Packing & shipping a mixof consumer/web- andstore-replenishment ordersC) The WMS-systemscapability to handle a mix ofconsumer/web- and storereplenishment orders6Storage54Pick3Pack & Ship21Returns handling0Use physical stores as materialhandling/logistics nodesDifferent order sizes (volume) between storereplenishment (large) and consumers (small)Don't know1 (insignificant)234 (medium)56High performers7 (very big)Low performersFigure 2. Omni-channel warehousing challenges.Figure 4. Perceived performance/performers.Today, most respondents perceive to hment better than competitors, but beingless competitive for web-orders (to consumers). Theweakest performance relates to picking andpacking, especially gift-wrapping and otherconsumer adaptations. Low performing areasinclude handling a mix of orders for e-commerceand store replenishment (e.g. related to packing &shipping), and having a Warehouse ManagementSystem (WMS) to better plan and control thewarehouse activities.For many of the detailed warehousing activities,today’s OC perceive themselves better (figure 3)than MC. Clear tendencies can, for example, beobserved for receiving, layout for web-orders,picking consumer orders, and WMS.Important for omni-channel logistics is whetheractivities should be integrated or separated. Highperformers separate receiving and quality controlactivities related to goods flows from suppliers andreturn flows (figure 5) to a higher degree (6-7),working both with separated zones and differentpersonnel.Separation of receiving and QC ofi) supplier delerivies and ii) deliveries of returns.9A) Separated zones.B) Different personnel87654321Perception of warehousing activities compared tocompetitors in industry/segmentA) Receiving1211109876543210B) DC layout for handlingconsumer web-ordersC) Picking of consumerweb-orders0High performersLow performersFigure 5. Separation of supplier deliveries and returnsflows.Omni-channelMulti-channelOtherFigure 3. Perceived performance/channels.High performers perceive themselves relativelybetter on, for example, receiving, layout for bothweb-orders and mixed orders, all types of picking,packing & shipping, and WMS for all types of orders(figure 4).Another issue is, for what activities storereplenishment orders and consumers’ web-ordersshould be integrated or separated. Mostrespondents seem to integrate orders both for bulkstorage and picking storage. However, a few highperformers use separation.In picking, the two most common methods aresynchronized picking, and pick-by-sort. Many seemto prioritize picking and sorting of web-orders beforestore-replenishment orders. Another pattern ispicking to packages and not to pallets. Moredetailed, the tendency is that high performers (figure6) have implemented many activities to a higherdegree, for example sort-while-pick, picking toparcels, working with separate time windows forweb- and store-orders, and more clearly prioritizingweb-orders.3

3rd Interdisciplinary Conference on Production, Logistics and Traffic (ICPLT)Degree of automation for different activities - todayPicking performance - degree of implementation9A) Sort while pick87B) Separate time windowsfor picking of consumersweb-orders and storereplenishment ordersC) Consumer web-orders hashigher priority than storereplenishment orders.1098765432106543210High performersA) ReceivingHigh performersLow performersC) SortingB) PickingLow performersFigure 6. Implementation of picking practices.Figure 9. Automation of different activities.Another decision reflects manual work orautomation. Automation is low today (figure 7), witha clear trend toward more automated processes,especially for sorting, picking, packing and put away(figure 8).Degree of automated processes - ckRetailers must have capacity to handle fluctuatingdemand, both related to seasons (e.g. Christmas,Black Friday) and weekly peak days. Respondentshad strong peaks on Mondays and Tuesdays, bothfor customer web-orders and store replenishmentorders. The general use of outsourcing (3/4PL) wasmost common for MC, and even stronger fordemand peaks (both seasonal and peak days),while less used of OC and high performers. Bothchannel types are mainly using temporary workersto handle peaks. OCs try to a higher degree toinfluence the capacity need by shipping other daysthan requested (figure 10). In five years, retailers willwork as today with personnel capacity, but slightlyless with 3/4PL and increased use of extra shifts.ShipCapacity planning of personnel - peak days(relative perceived high/low performers)Returns handlingDon't know1 (not at all)234 (medium)567 (very high)Figure 7. Automation today.Degree of automated processes - in 5 A) At peak days we useexternal 3/4PL-solutions.B) At peak days we usetemporary labour.C) At peak days wesmoothen out demandby delivering ordersbefore/after demand.PickSortHigh performersPackLow performersFigure 10. Capacity planning relative peak days.ShipReturns handlingDon't know1 (not at all)234 (medium)567 (very high)Figure 8. Automation in five years.Shipping and returns handling will be leastautomated. OC will have highest increase ofautomation in five years. Already today, highperformers are using automation more than lowperformers (figure 9). For packing, the tendency isunclear as also many high performers will continueto do it manually.Regarding click-and-collect, OCs are mostdeveloped today. But the changed role of physicalstores in future retail channels, with more click-andcollect and click-and-reserve (figure 11 and 12), willpresent challenges and implications for materialshandling.4

3rd Interdisciplinary Conference on Production, Logistics and Traffic (ICPLT)Use of physical stores and suppliers as nodes inweb-orders material handling - today0%20%40%60%80%100%Click-and-collect: web-orders can bedelivered in the storeClick-and-reserve: web-orders arepicked in the storeInventory levels in the shops aredimesioned also for web-ordersAcknowledgementSuppliers drop ship products to storesfor click-and-collectProducts for click-and-collect are pickedand packed at DCThis research was funded by The Swedish Retailand Wholesale Council's.Inventory management of stock atstores and DC inventory are integratedDon't know1 (very low degree)234 (medium)567 (very high degree)ReferencesFigure 11. Use of nodes tor materials handling - today.Use of physical stores and suppliers as nodes inweb-orders material handling - in 5 years0%20%40%34 (medium)560%80%100%Click-and-collect: web-orders can bedelivered in the storeClick-and-reserve: web-orders arepicked in the storeInventory levels in the shops aredimesioned also for web-ordersSuppliers drop ship products to storesfor click-and-collectProducts for click-and-collect are pickedand packed at DCInventory management of stock atstores and DC inventory are integratedDon't know1 (very low degree)2With limited number of respondents from only onecountry, this study should only be used to rms, more research should explore andanalyse what is developed in practice and whatworks well in different contexts.67 (very high degree)Figure 12. Use of nodes tor materials handling - in fiveyears.Also drop-shipments from suppliers to stores (tosupply web-orders) will increase. But as today, mostproducts for click-and-collect will be picked andpacked at the DC – especially of high performers.These trends imply that inventory managementmust be more coordinated between warehousesand other handling nodes (e.g. retail stores) for weborders. Today, high performers are more integratinginventory management. Regarding in-store picking,low performers struggle with the need of integratedERP-systems and specific area needs.4 ConclusionsThe strong trend toward omni-channel retailing, withstores increasingly used as handling nodes for weborders, creates challenges related to materialhandling (especially in packing & shipping, andpicking). Automation will increase, but many will stillhandle material manually. Most resondents thatperceive themselves as overall high performershave implemented omni-channel strategy. They alsoassess themselves better in many warehousingactivities, seem to have implemented moredeveloped practices and thought more regardingseparation or integration. High performers alsoseem to perform warehousing more in-house:maybe they find warehousing an importantcapability to control and develop to be competitive infuture omni-channel retailing.1. A. Hübner, A. Holzapfel, H. Kuhn:Distribution systems in omni-channelretailing. In: Business Research, Vol. 9 No.2, pp. 255-296, (2016)2. N.A. Agatz, M. Fleischmann, J.A. VanNunen: E-fulfillment and multi-channeldistribution–A review. In: European Journalof Operational Research, Vol. 187 No. 2,pp. 339-356, (2008)3. J. Lewis, P. Whysall, C. Foster: Drivers andtechnology-related obstacles in moving tomulti-channel retailing. In: InternationalJournal of Electronic Commerce, Vol. 18No. 4, pp. 43-68, (2014)4. R. Strang: Retail without boundaries. In:Supply Chain Management Review, Vol. 17No. 6, pp. 32-39, (2013)5. P.C. Verhoef, P.K. Kannan, J.J. Inman:From multi-channel retailing to omnichannel retailing: introduction to the specialissue on multi-channel retailing. In: Journalof Retailing, Vol. 91 No. 2, pp. 174-181,(2015)6. E. Brynjolfsson, Y.J. Hu, M.S. Rahman:Competing in the Age of Omni-channelRetailing. In: MIT Sloan ManagementReview, Vol. 54 No. 4, pp. 23-29, (2013)7. N. Beck, D. Rygl: Categorization of multiplechannel retailing in multi-, cross-, and omni‐channel retailing for retailers and retailing.In: Journal of Retailing and ConsumerServices, Vol. 27, pp. 170-178, (2015),8. W. Piotrowicz, R. Cuthbertson: Introductionto the special issue information technologyin retail: Toward omni-channel retailing. In:International Journal of ElectronicCommerce, Vol. 18 No. 4, pp. 5-16, (2014)9. M. Bernon, J. Cullen, J. Gorst: Online retailreturns management: Integration within anomni-channel distribution context. In:International Journal of Physical Distributionand Logistics Management, Vol. 46 No. 6/7,pp. 584-605, (2016).10. A. Hübner, J. Wollenburg, A. Holzapfel:Retail logistics in the transition from multichannel to omni-channel. In: International5

3rd Interdisciplinary Conference on Production, Logistics and Traffic (ICPLT)Journal of Physical Distribution andLogistics Management, Vol. 46 No. 6/7, pp.562-583, (2016)11. J.H. Kembro, V. Danielsson, G. Smajli:Network video technology: Exploring aninnovative approach to improvingwarehouse operations, International Journalof Physical Distribution & LogisticsManagement, Vol. 47 No. 7, pp.623-645,(2017)12. C. Forza: Survey research in operationsmanagement: a process-based perspective.In: International Journal of Operations &Production Management, Vol. 22 No. 2, pp.152-194, (2002)6

channel warehousing. The survey contained multiple detailed questions regarding warehousing activities (from receiving to pack & ship, as well as returns handling), processes and resources as well as background data of each company. To grasp future aspects and trends, we researched retailers' perceptions of how they (i)