Transcription

FHA Single Family Housing Policy Handbook12345678910111213141516HUD Handbook 4000.1FHA Single Family Housing Policy HandbookUSER QUICK GUIDEBelow are some helpful tips for using HUD Handbook 4000.1, FHA Single Family HousingPolicy Handbook (Handbook 4000.1):1. Handbook 4000.1 is organized in the sequence of a life cycle of a mortgage.2. In this draft section, yellow highlighting on heading titles indicates the entire contentbelow the heading title is proposed new content for HECM. Yellow highlighted text insection II.D indicates proposed updates to published Handbook 4000.1.3. Capitalization of words in Handbook 4000.1 generally denotes terms that are defined inthe Glossary.4. Hyperlinks are included in Handbook 4000.1 for easy navigation to a referenced section.Hyperlinks are indicated by blue, underlined text. Users can jump to the hyperlinkedreference by clicking on the text. To navigate back to the hyperlink last used, clickALT .Handbook 4000.1 – HECM

FHA Single Family Housing Policy HandbookTable of ContentsFHA Single Family Housing Policy HandbookTABLE OF CONTENTS123I.DOING BUSINESS WITH FHA . 14II.ORIGINATION THROUGH POST-CLOSING/ENDORSEMENT . 15A. TITLE II INSURED HOUSING PROGRAMS FORWARD MORTGAGES . 167B. TITLE II INSURED HOUSING PROGRAMS HOME EQUITY CONVERSIONMORTGAGES . 3343536373839404142431. Origination/Counseling Requirements. 1a. Required Referral for HECM Counseling . 1b. Restrictions on Processing of Applications Before Completion of HECM Counseling . 2c. Individuals Required to Receive HECM Counseling . 3d. Counseling Prohibited Practices . 32. Origination/Processing. 4a. Applications and Disclosures . 4b. General HECM Insurance Eligibility. 273. Allowable Mortgage Parameters. 50a. Maximum Mortgage Amounts . 50b. Maximum Claim Amount . 50c. Interest Rate Options. 51d. Principal Limit . 51e. Payment Plan . 54f. HECM Calculator Software . 55g. Disbursement Limits . 55h. Maximum Mortgage Term . 57i. Mortgage Insurance Premiums . 574. Underwriting the Property . 58a. Property Acceptability Criteria . 58b. Required Documentation for Underwriting the Property . 75c. Conditional Commitment Direct Endorsement Statement of Appraised Value . 755. Performing the Financial Assessment of the Borrower . 75a. Definition . 75b. Credit History Review Requirements . 75c. Property Charge Payment History Review Requirements . 85d. Monthly Expense Analysis . 88e. Effective Income Analysis . 100f. Residual Income Analysis. 126g. Asset Requirements . 131h. Required Documentation . 139i. Final HECM Decision. 1396. Closing . 150a. Mortgagee Closing Requirements. 150b. Mortgage and Note . 166c. Adaptation of Loan Documents . 167Handbook 4000.1 – HECMPost Date: 09/29/2021This is a DRAFT document for posting on the Drafting Table to collect industry feedback. The document willundergo Departmental Clearance again prior to final publication. See cover page of document for more info.i

FHA Single Family Housing Policy HandbookTable of Contents123456789101112d. Disbursement of HECM Proceeds . 1677. Post-Closing and Endorsement . 168a. Pre-Endorsement Review. 168b. Mortgagee Pre-Endorsement Review Requirements . 168c. Inspection and Repair Requirements for HECMs Pending Endorsement in PresidentiallyDeclared Major Disaster Areas . 174d. Procedures for Endorsement . 175e. Endorsement and Post-Endorsement . 1838. Programs and Products . 185a. HECM For Purchase . 185b. HECM Refinance . 207c. Condominiums . 21113C. CONDOMINIUM PROJECT APPROVAL . 2351415D. APPRAISER AND PROPERTY REQUIREMENTS FOR TITLE II FORWARD ANDREVERSE MORTGAGES . 2351617181920212223242526271. Commencement of the Appraisal. 235a. Information Required before Commencement of Appraisal . 235b. Additional Information Required Before Commencement of an Appraisal on NewConstruction . 235c. Additional Information Required Before Commencement of an Appraisal on a Propertywith an Exception from the Lead-Based Paint Poisoning Prevention Act (LPPPA)(HECM Only) . 2352. General Appraiser Requirements . 2353. Acceptable Appraisal Reporting Forms and Protocols . 236a. Application of Minimum Property Requirements and Minimum Property Standards byConstruction Status . 236b. Minimum Property Requirements and Minimum Property Standards . 2382829APPENDIX 9.0 - ASSUMED LOAN PERIODS FOR COMPUTATIONS OF TOTALANNUAL LOAN COST RATES. 2393031SERVICING AND LOSS MITIGATION – TITLE II INSURED HOUSING PROGRAMSHOME EQUITY CONVERSION MORTGAGES (HECM) . 24132III.33A. TITLE II INSURED HOUSING PROGRAMS FORWARD MORTGAGES . 2423435B. TITLE II INSURED HOUSING PROGRAMS HOME EQUITY CONVERSIONMORTGAGES . 242363738394041421. Servicing of FHA-Insured HECMs . 242a. Servicing in Compliance with Law. 242b. Responsibility for Servicing Actions . 243c. Providing Information to HUD . 245d. Communication with Borrowers and Authorized Third Parties . 245e. Borrower Disbursements . 246f. Payment Administration . 249SERVICING AND LOSS MITIGATION . 242Handbook 4000.1 – HECMPost Date: 09/29/2021This is a DRAFT document for posting on the Drafting Table to collect industry feedback. The document willundergo Departmental Clearance again prior to final publication. See cover page of document for more info.ii

FHA Single Family Housing Policy HandbookTable of 6g. Servicing Fees and Charges . 250h. Interest Rate Changes for Adjustable Rate HECMs . 251i. Set-Asides . 252j. Allowable Fees and Charges . 256k. Prepayment . 258l. Completion of Required Repairs . 260m. Insurance Coverage Administration . 261n. Mortgage Insurance Premium Remittance. 265o. Post-Endorsement HECM Amendments . 266p. Occupancy Certification . 271q. Property Maintenance . 272r. Optional Assignment . 273s. Demand Assignment . 281t. Repurchase of Previously Assigned HECM . 282u. Mortgage Insurance Termination. 284v. Record Retention – Servicing File . 2862. Default Servicing . 287a. Use of Counseling Agencies . 287b. Due and Payable Servicing . 287c. Defaults for Unpaid Property Charges . 294d. Initiation of Foreclosure and Reasonable Diligence Time Frames . 304e. Sale of Property Acquired through Foreclosure or DIL . 310f. Claims . 3113. Programs and Products . 316a. Presidentially-Declared Major Disaster Areas. 316b. Mortgagee Optional Election Assignment . 31727APPENDIX 1.0 – MORTGAGE INSURANCE PREMIUMS . 32828293031323334353637383940414243APPENDIX 2.0 – ANALYZING IRS FORMS . 328APPENDIX 3.0 – POST-ENDORSEMENT FEES AND CHARGES BY HOC (APPLIESTO SERVICING ONLY) . 329APPENDIX 4.0 – HUD SCHEDULE OF STANDARD ATTORNEY FEES (APPLIES TOSERVICING ONLY) . 336APPENDIX 5.0 - FIRST LEGAL ACTIONS TO INITIATE FORECLOSURE ANDREASONABLE DILIGENCE TIME FRAMES (APPLIES TO SERVICINGONLY). 336APPENDIX 6.0 - PROPERTY PRESERVATION ALLOWANCES AND SCHEDULES(APPLIES TO SERVICING ONLY) . 339A. MAXIMUM PROPERTY PRESERVATION ALLOWANCES . 339B. WINTERIZATION SCHEDULE. 342C. GRASS CUT SCHEDULE . 342GLOSSARY. 345ACRONYMS . 396Handbook 4000.1 – HECMPost Date: 09/29/2021This is a DRAFT document for posting on the Drafting Table to collect industry feedback. The document willundergo Departmental Clearance again prior to final publication. See cover page of document for more info.iii

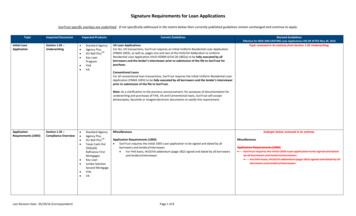

II. Origination through Post-Closing/EndorsementB. Title II Insured Housing Programs Home Equity Conversion Mortgages1. Origination/Counseling Requirements1I. DOING BUSINESS WITH FHA2II. ORIGINATION THROUGH POST-CLOSING/ENDORSEMENT3A. TITLE II INSURED HOUSING PROGRAMS FORWARD MORTGAGES45B. TITLE II INSURED HOUSING PROGRAMS HOME EQUITY CONVERSIONMORTGAGES678910The Title II Insured Housing Programs Home Equity Conversion Mortgages (HECM)Origination through Post-Closing/Endorsement section in this FHA Single Family HousingPolicy Handbook (Handbook 4000.1) provides the origination, property underwriting, financialassessment, closing, post-closing, and endorsement standards and procedures applicable toHECMs insured under Section 255 of Title II of the National Housing Act.111213The Mortgagee must fully comply with all of the following standards and procedures inoriginating, underwriting the Property, conducting the financial assessment, and closing forobtaining Federal Housing Administration (FHA) mortgage insurance on all HECM transactions.1415161718If there are any exceptions or program-specific standards or procedures that differ from those setforth below, the exceptions or alternative program or product specific standards and proceduresare explicitly stated in Section 8. Terms and acronyms used in this Handbook 4000.1 have theirmeanings defined in the Glossary and Acronyms sections and in the specific section of theHandbook 4000.1 in which the definitions are located.191. Origination/Counseling Requirements202122A Home Equity Conversion Mortgage (HECM) refers to a non-recourse, reverse mortgage thatallows a HECM Borrower (Borrower) access to equity secured by the Principal Residence withno corresponding monthly mortgage payment.23a. Required Referral for HECM Counseling24i. Definition25262728Participating Agency refers to all housing counseling and intermediary organizationsparticipating in HUD’s Housing Counseling program, including HUD-approved agencies,and affiliates and branches of HUD-approved intermediaries, HUD-approved multi-stateorganizations, and state housing finance agencies.29ii. Standard303132The Mortgagee must provide each prospective Borrower with a list of the names,addresses, and telephone numbers of the Participating Agencies eligible to provideHECM counseling that includes:Handbook 4000.1 – HECM OriginationPost Date: 09/29/2021This is a DRAFT document for posting on the Drafting Table to collect industry feedback. The document willundergo Departmental Clearance again prior to final publication. See cover page of document for more info.1

II. Origination through Post-Closing/EndorsementB. Title II Insured Housing Programs Home Equity Conversion Mortgages1. Origination/Counseling Requirements123456789 all HUD-approved intermediaries listed on the HUD Intermediaries ProvidingHECM Origination Counseling Nationwide;Participating Agencies that provide telephone counseling; andat least five Participating Agencies located in the prospective Borrower’s state orlocality, including at least one local agency within a reasonable driving distanceof the prospective Borrower’s residence for face-to-face counseling.In cases where HECM counseling is not available in the local area or state, Mortgageesmust determine which Participating Agencies are most conveniently located to theBorrower and provide a listing of at least five Participating Agencies.10iii. Required Documentation111213The Mortgagee must enter the date the prospective Borrower received the list ofParticipating Agencies in FHA Connection (FHAC) within one business day ofrequesting the case number.14b. Restrictions on Processing of Applications Before Completion of HECM Counseling15i. Definition161718A Third-Party Originator (TPO) is an Entity that originates FHA Mortgages for an FHAapproved Mortgagee acting as its sponsor. A TPO may be an FHA-approved Mortgageeor a non-FHA-approved Entity.19ii. Standard2021222324252627282930313233343536The Mortgagee and/or sponsored TPO (see section I.A.5.a.v Sponsor/Sponsored ThirdParty Originator Relationship in Handbook 4000.1) may perform only the functions listedbelow before all required HECM counseling has been completed by all individualsrequired to receive counseling: accept the loan application and provide required disclosures; lock in the Expected Average Mortgage Interest Rate (Expected Rate); explain the HECM program to the Borrower; discuss whether the Borrower is eligible for HECM financing; provide information regarding the fees and charges associated with the HECMproduct; describe the potential financial implications of a HECM for the Borrower; provide the Borrower with sample copies of the HECM Note, Mortgage, and loanagreement; order preliminary title report; order Automated Valuation Model (AVM); or order credit report to perform a preliminary credit review of the Borrower’s financialobligations.Handbook 4000.1 – HECM OriginationPost Date: 09/29/2021This is a DRAFT document for posting on the Drafting Table to collect industry feedback. The document willundergo Departmental Clearance again prior to final publication. See cover page of document for more info.2

II. Origination through Post-Closing/EndorsementB. Title II Insured Housing Programs Home Equity Conversion Mortgages1. Origination/Counseling Requirements123456The Mortgagee and sponsored TPO may not collect any fee or the Borrower’s bankingaccount and credit card information before closing, or in connection with any functionpermitted above if the function is performed before receipt of a signed and dated formHUD-92902, Certificate of HECM Counseling, for each individual required to receivecounseling.c. Individuals Required to Receive HECM Counseling7i. Definitions89A Non-Borrowing Spouse (NBS) refers to the spouse of a HECM Borrower who is alsonot a Borrower.1011Non-Borrowing Owner refers to someone who is not the spouse of a Borrower and is onthe title to the Property that will serve as collateral for the HECM.12ii. Standard1314The Mortgagee must ensure all Borrowers, NBSs, and Non-Borrowing Owners havereceived HECM counseling from a counselor on the HECM Roster.15161718For any Borrower, NBS, or Non-Borrowing Owner lacking legal competency, HECMcounseling must be completed by: the person holding a Power of Attorney (POA); or a court-appointed conservator or guardian.19For additional information on HECM Counseling see HUD Handbook 7610.1.20iii. Required Documentation21222324The Mortgagee must obtain a copy of the Certificate of HECM Counseling signed anddated by each individual required to receive counseling and the HECM counselor. TheMortgagee and sponsored TPOs may only request changes to the Certificate of HECMCounseling up until the HECM is endorsed.252627The Mortgagee must enter the HECM counseling certificate identification number inFHAC. When there are multiple certificates, the Mortgagee must use the HECMcounseling certificate identification number of the last person counseled.28d. Counseling Prohibited Practices29i. Definition3031Interested Parties refer to sellers, real estate agents, builders, developers, Mortgagees,Third-Party Originators (TPO), or other parties with an interest in the transaction.Handbook 4000.1 – HECM OriginationPost Date: 09/29/2021This is a DRAFT document for posting on the Drafting Table to collect industry feedback. The document willundergo Departmental Clearance again prior to final publication. See cover page of document for more info.3

II. Origination through Post-Closing/EndorsementB. Title II Insured Housing Programs Home Equity Conversion Mortgages2. Origination/Processing1ii. Prevention of Undue Influence in HECM Counseling2345Interested Parties to the transaction must not: be present during HECM counseling; or provide Borrowers with advance copies of the HECM counselor’s reviewquestions with answers.6iii. Prohibited Steering and Payment of HECM Counseling Fees789Interested Parties to the transaction must not steer, direct, recommend, or otherwiseencourage any individual to seek the services of any one particular Participating Agencyor HECM counselor.10111213The Mortgagee must not refer Borrowers to any one particular Participating Agency orHECM counselor, discuss a Borrower’s personal information, including the timing orscheduling of the counseling; or request information regarding the topics covered in acounseling session.141516The Mortgagee may not pay a Participating Agency or HECM Counselor, directly orindirectly, for HECM counseling services, through either a lump-sum payment or on acase-by-case basis.172. Origination/Processing18a. Applications and Disclosures192021222324252627The Mortgagee must obtain a completed Fannie Mae Form 1009, Residential LoanApplication for Reverse Mortgages (RLARM), from the Borrower and must captureadditional required information using Parts IV, V, and VI of Fannie Mae Form 1003,Uniform Residential Loan Application (URLA), or an alternative form that captures the sameinformation. In addition, the Mortgagee must provide all required federal and statedisclosures to begin the origination process. Regardless of the form used, Mortgagees mustensure that the Borrower certifies to the accuracy and completeness of the financialinformation. The Mortgagee is responsible for using the most recent version of all forms asof the date of completion of the form.28i. Contents of the HECM Application Package29303132The Mortgagee must maintain all information and documentation that is relevant to itsapproval decision in the HECM file. All information and documentation that is requiredin this Handbook 4000.1, and any incidental information or documentation related tothose requirements, is relevant to the Mortgagee’s approval decision.3334If after obtaining all documentation required below, the Mortgagee has reason to believeit needs additional support for the approval decision, the Mortgagee must obtainHandbook 4000.1 – HECM OriginationPost Date: 09/29/2021This is a DRAFT document for posting on the Drafting Table to collect industry feedback. The document willundergo Departmental Clearance again prior to final publication. See cover page of document for more info.4

II. Origination through Post-Closing/EndorsementB. Title II Insured Housing Programs Home Equity Conversion Mortgages2. Origination/Processing12additional explanation and documentation, consistent with information in the HECM fileto clarify or supplement the information and documentation submitted by the Borrower.3General Requirements4(1) Maximum Age of HECM Documents5(a) General Document Age678910Documents used in the origination and financial assessment of a HECM maynot be more than 120 Days old at the Disbursement Date. Documents whosevalidity for financial assessment purposes is not affected by the passage oftime, such as divorce decrees or tax returns, may be more than 120 Days oldat the Disbursement Date.11121314For purposes of counting Days for periods provided in the Title II InsuredHousing Programs Home Equity Conversion Mortgages section of Handbook4000.1, day one is the Day after the effective or issue date of the document,whichever is later.15(b) Age of Certificate of HECM Counseling1617181920The Certificate of HECM Counseling remains valid for a period of 180 Daysfrom the date the last Borrower, NBS, Non-Borrowing Owner, or legalrepresentative who is required to attend counseling signs a certificate forpurposes of obtaining a case number. For additional information on HECMCounseling see HUD Handbook 7610.1.21(c) Appraisal Validity22(i) Initial Appraisal Validity232425262728The 120 Day validity period for an appraisal (see Ordering Appraisals)may be extended for 30 Days at the option of the Mortgagee if (1) theMortgagee approved the Borrower or HUD issued the Firm Commitmentbefore the expiration of the original appraisal; or (2) for HECM forPurchase program applications, the Borrower signed a valid sales contractprior to the expiration date of the appraisal.29(ii) Appraisal Update30313233An appraisal update must be performed before the initial appraisal, withno extension, has expired. Where the initial appraisal is subsequentlyupdated, the updated appraisal is valid for a period of 240 Days after theeffective date of the initial appraisal report that is being updated.Handbook 4000.1 – HECM OriginationPost Date: 09/29/2021This is a DRAFT document for posting on the Drafting Table to collect industry feedback. The document willundergo Departmental Clearance again prior to final publication. See cover page of document for more info.5

II. Origination through Post-Closing/EndorsementB. Title II Insured Housing Programs Home Equity Conversion Mortgages2. Origination/Processing1(2) Handling of Documents234567Mortgagees must not accept or use documents relating to the employment,income, assets, or credit of Borrowers that have been handled by, or transmittedfrom or through the equipment of unknown parties, or Interested Parties.Mortgagees may not accept or use any Third Party Verifications (TPV) that havebeen handled by, or transmitted from or through any Interested Party, or theBorrower.8910Mortgagees may accept a copy of the signed and dated form, the Certificate ofHECM Counseling, from the HECM counselor or Borrower that has been faxed,mailed, electronically transmitted, or otherwise provided.11Exception for Mortgagees and TPOs1213The Mortgagee and TPO are permitted to handle documents relating to theemployment, income, assets or credit of Borrowers.14(a

12 Participating Agencies in FHA Connection (FHAC) within one business day of 13 . requesting the case number. 14 . b. Restrictions on Processing of Applications Before Completion of HECM Counseling . 15 . i. Definition 16 A Third-Party Originator (TPO) is an Entity that originates FHA Mor