Transcription

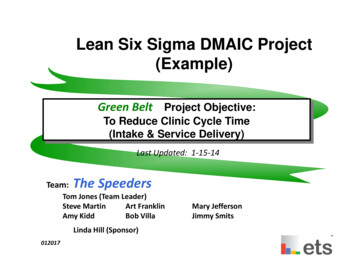

Six Sigma DMAIC Improvement StoryProject Objective:To Reduce the Time to Pay Vendors forConstruction and A&E Services (lean approach)Last Updated: 12-5-2017Team:Edith Brown, Juliette Bernard, Ray Garcia, Piedad Amador, Manley Cobia, YeseniaPerez, Margaret Moss, Wendy Wandyez, Bill Busutil, Amy Horton-Tavera, Mayra Morales, andRoy FerreiraFrances Morris (Sponsor)Jennifer Moon (Executive Sponsor)

Lean Six Sigma Problem Solving ProcessThe team utilized the 5-Step DMAIC problem solving process.2DefineMeasureAnalyzeImprove Control

Identify Project CharterThe team developed a Project Charter.Project CharterProject Name: Reduce the time it takes for WASD to pay vendors.BusinessCaseAs of January 2017, 82% of all WASD's invoices were paid within 30 days of receipt of a proper invoice. As ofJuly 2017, invoices for architectural and engineering services took an average of 16 days from receipt todesignation as a "proper invoice" and invoices for construction services took an average of 14 days to prepareProblem/Impact:and finalize following WASD's receipt of the redline (excluding invoices still in process as of July 25). Latepayments to vendors could place the department in non-compliance with County ordinances and policies, anddissuade desirable vendors from providing services to WASD.Expected Benefits:OutcomeIndicators andProposed TargetConsistent reductions in the time it takes to pay vendors will ensure compliance with County ordinances andpolicies, and enable WASD to better retain desirable vendors.Q1: 90% of Construction / A&E invoices paid within 30 days; Q2: 90% of Construction / A&E invoices submittedby "small businesses" paid within 14 daysObjectivesTime Frame: January through August 2017StrategicSupports the County's Business PlanAlignment:In Scope: All vendor payments within WASDScopeOut-of-Scope: All other vendor paymentsAuthorized by: Jennifer Moon, Lester SolaMethodProjectLean Six Sigma DMAIC (Define - Measure - Analyze - Improve - Control); observations & interviewsMethodology:Sponsors: Jennifer Moon, Frances MorrisTeam Leader: Amy Horton-TaveraTeamTeam Members:Amy Horton-Tavera, Roy Ferreira, Mayra Morales, Bill Busutil, Edith Brown, Raymond Garcia, Juliette Bernard,Piedad Amador, Manley Cobia, Wendy Wandyez, Yesenia Perez, Margaret MossProcessFrances Morris, Josephine BarriosOwner(s):Mgmt ReviewJennifer Moon, Hugo Salazar, Lester Sola, Frances MorrisTeam:Completion Date: August 31st, 2017ScheduleReview Dates: Monthly, and Final Review on August 28, 20173DefineMeasureAnalyzeImprove Control

Develop Project TimelineThe team developed a schedule to complete the Project.WHAT: Complete DMAIC Process by August 30th,2017WHENDMAIC Story2017Process StepJanFebMarAprMayJune1. Define2. Measure3. Analyze4. Improve5. Control4DefineMeasureAnalyzeImprove ControlJulyAugust

Develop Process FlowchartsThe team constructed a flow chartdescribing the WASD A&E andConstruction Invoice Payableprocess.P1: Average # Days from Date InvoiceReceived to Date Review CompletedP2: Average # Days Invoice Received toDate Supervisor Review CompletedQ1: % of A&E invoices paid within 30days of receipt of a proper invoiceQ2: % of A&E SBE invoices paid within14 days of receipt of a proper invoice5DefineMeasureAnalyzeImprove Control

Develop Process FlowchartsConstruction ServicesP1: Average # Days from RedlineReceived to Date Contractor NotifiedQ1: % of Construction invoices paidwithin 30 days of receipt of a properinvoiceQ2: % of Construction SBE invoicespaid within 14 days of receipt of aproper invoice6DefineMeasureAnalyzeImprove Control

Identify Process ActivitiesThe team identified the major activities related to paying invoices for both A&E andConstruction services and were further discussed.Water and Sewer Architecture and Engineering (A&E) Services Payment ProcessAction#Submit1Upload23Process StepConsultant submits preparedinvoice to contractCompliance/Invoice SectionCreate and upload invoice toProliance SystemContract Compliance reviewsinvoice for financialsufficiency (Percentages,allocations, backupdocumentation, directexpenses, time and material,etc.)x1aDate Stamp2aCreate and upload invoice to Proliance System2bRoute to assigned staff with a four (4) day due date for reviewDivisional checklist is used to review the invoice for financial sufficiency. All hardcopies - original invoices3aReviewWork with consultant to correct discrepancies if needed456ConfirmList of ActivitiesYes. Valid invoice is routed to WASD PM for approval of percent complete anddeliverables.WASD Project Manager orProgram Manager reviewsinvoice deliverablesDoes invoice meetrequirements4aSend hard copy and route forsignatures/approvals6aInvoice logged in Proliance and manual delivery receipt created & hard copiesrouted to Project Manager6bSigns hard copy paper, enters in Proliance and returns to Contract Complianceas executed - electronic & hard copya7DefineMeasureAnalyzeImprove ControlThis is asample ofsome of theactivities.

Identify Process ActivitiesThe team identified the major activities related to paying invoices for both A&E andConstruction services and were further discussed.WASD Construction Services Payment ProcessActionMeasure#123Process StepMeasure The WorkPeriodicallyCreate RedlineWASD CM delivers“Redline” to WASDContract Invoice ReviewSectionXList of Activities3a Document Control reviews Redline for completeness and accuracy.3b3cDeliver3d3e3f3gChecks for correct estimate number, beginning and ending pay period dates,proper initialing of current completion date and all attached pages. ChecksContractor's Notification and Field Certification forms for accurate dates andif properly signed.When the redline is deemed to be complete, it is stamped with date and timeof acceptance. The Document Control person signs along with the personmaking the delivery.Scans redline and uploads into database. Creates a "Pay EstimateChecklist" in the database, activates, and forwards the "Checklist" and theactual redline package to Contract Compliance.Checks redline for any contingency authorizations or change orders to bepaid and attaches a copy of the approved contingency or change.Verifies that the pay period ending dates entered onto the redline are correct.Checks to see if the contract has a CSBE goal to ensure that a MonthlyUtilization Report is required as part of Compliance Package.If the Redline is for a final pay estimate extra steps:3h Prepare list of Final Documents requiredNext, the team took a closer look at some of the activities.8DefineMeasureAnalyzeImprove ControlThis is asample ofsome of theactivities.

Identify High Cost and Low Value Added ActivitiesAfter the team identified the major activities, a Value Added Matrix was used to rankthe value (cost / benefit) of each activity in the payment process.Next, the team identified activities where the cost could be lowered or benefitscould be increased.9DefineMeasureAnalyzeImprove Control

Identify High Cost and Low Value Added ActivitiesThe team identified activities in the A&E invoice process where the cost could belowered or benefits could be increased.A&EProcess / Activity DescriptionCostBenefitFinancial sufficiency review / Invoice review withdivisional checklistHigh CostHigh BenefitPrepare receipt / Executed invoice is integrated inProliance and ERPHigh CostHigh BenefitHigh CostHigh BenefitLow CostLow BenefitRoute for signatures and approvals / Sign hard copy andenter into Proliance, return to Contract ComplianceDeliver hard copy invoice to WASD Finance / Integratedinvoice is submitted to WASD AP for disbursement10DefineMeasureAnalyzeImprove Control

Identify High Cost and Low Value Added ActivitiesThe team identified activities in the construction invoice process where the costcould be lowered or benefits could be increased.CONSTRUCTIONProcess / Activity DescriptionCostReview redline / verify substantial completion andHigh Costliquidated damages assessmentReview redline / verify substantial completion andHigh Costliquidated damages assessmentCreate pay estimate / Accountant 1 proofreads theHigh Costother accountant's workCreate pay estimate / Accountant 1 reviews backupdocumentation for dedicated and contingencyHigh Costpayment itemsSend certified payroll to Small BusinessMedium CostDevelopment for small business vendorsReview redline / Accountant 2 forward the redlineLow Costto Accountant 1 along with a Proliance messageBenefitHigh BenefitHigh BenefitMediumBenefitMediumBenefitLow BenefitLow BenefitNext, the team took a closer look at the selected activities to identifyissues and potential prove Control

Analyze Identified Activities and Develop SolutionsThe team identified the issues with each activity and developed countermeasures toimprove WASD’s A&E accounts payable process.Countermeasures MatrixWASD Accounts Payable A&E Services PaymentsEffectivenessEFeasibilityFOverall(E times F)Take Action?Yes or NoProblem Statement: 5 A&E A/P process activities were identified as high cost, low benefit, orboth.Ratings Legend:5 Extremely3 Average1 PoorCountermeasure A-1Eliminate the Program Manager (PM) from the A&E process of reviewing invoices (coordinateinternally with WASD management - PM's, legal, etc)5315YCountermeasure A-2For new consultants not under a PM, create a comprehensive training plan and a checklist withexamples at a task level4520YEffectivenessEFeasibilityFOverall(E times F)Take Action?Yes or NoIssue - A (Process step / activity 3a, 3a1, 3b Financial sufficiency review / Invoice review withdivisional checklist - HC, HB)Submitted documents by A&E vendor often are not ready for processing by WASD. Some Issuesinclude: carryover or approved amounts are incorrect, missing backup documentation, illegibledocuments, and % complete/deliverables are not correct.Countermeasure B-1Allow contract compliance staff to approve invoices in Proliance after PM physically signs andapproves the invoice5525YCountermeasure B-2Possibly modify workflow to eliminate unnecessary steps (pending acceptance -- approved)111NCountermeasure B-3Add guidelines for contract payments to the WASD website (to refer vendors needingassistance for reference)236YIssue - B (Process step / activity 6b - Route for signatures and approvals / Sign hard copy andenter into Proliance, return to Cont. Compliance - HC, HB)Invoices are not approved timely in Proliance by PM's. .12DefineMeasureAnalyzeImprove Control

Analyze Identified Activities and Develop SolutionsThe team identified the issues with each activity and developed countermeasures toimprove WASD’s A&E accounts payable process.Countermeasures MatrixWASD Accounts Payable A&E Services PaymentsRatings Legend:5 Extremely3 Average1 PoorTake Action?Yes or No525YCountermeasure C-3Work with AP to ensure vendors have WASD and MDAD locations in ERP111NTake Action?Yes or No5n/an/an/aYCountermeasure D-2Use courier to assist with document delivery5525YCountermeasure D-3Assign document control for document delivery5525YTake Action?Yes or NoOverall(E times F)Countermeasure C-2Continue the practice of checking the first invoice against the purchase orderOverall(E times F)YOverall(E times enessECountermeasure C-1Work with WASD AP to re-evaluate when manual receipts are needed. If required for construction, createmanual receipts earlier in the processEffectivenessEIssue - C (Process step / activity 10a - Prepare receipt / Executed invoice is intergrated in Proliance and ERP - HC,HB)Integration may fail delaying process (line items don't match, status of P.O.'s). ERP is shared with the AviationDepartment and may cause vendors to become inactive in ERP for issues not related to WASD. This may stopWASD payment integration.EffectivenessEProblem Statement: 5 A&E A/P process activities were identified as high cost, low benefit, or both.5525YIssue- D (Process step / activity 11a - Deliver hard copy invoice to WASD Finance / Integrated invoice is submittedto WASD AP for disbursement - LC, LB)Professional staff physically delivers invoices to AP (Douglas) for disbursements (1-2x daily)Countermeasure D-1Continue to work with AP staff to evaluate the feasibility of accepting electronic invoices (e-Builderimplementation)Issue - E (Overall)Too many signatures required in the invoice payment process13Countermeasure E-1Continue to work with CFO and WASD Controller Division in order to streamline the invoice approval andpayment process

Analyze Identified Activities and Develop SolutionsThe team identified the issues with each activity and developed countermeasures toimprove WASD’s Construction accounts payable process.Countermeasures MatrixWASD Accounts Payable Construction Services PaymentsRatings Legend:5 Extremely3 Average1 PoorEffectivenessEFeasibilityFOverall(E times F)Take Action?Yes or NoCountermeasure F-1Communicate with Document Control staff for all construction managers to ensure that substantialcompletion memo is promptly uploaded into Sharepoint / Proliance3412YCountermeasure F-2Develop a policy whereby the substantial completion memo must be completed by the projectmanager within 5 business days of substantial completion414YIssue - G (Process step / activity 3u - Review redline / Accountant 2 forward the redline to Accountant 1along with a Proliance message - LC, LB)The pre-audit is performed by a higher level accountant (ensuring correct previous draft).EffectivenessEFeasibilityFOverall(E times F)Take Action?Yes or NoProblem Statement: 5 Construction A/P process activities were identified as high cost, low benefit,or both.224NIssue - F (Process step / activity 3n- Review redline / verify substantial completion and liquidateddamages assessment: HC, HB)Documentation of substantial completion may be missing, and project managers may not respond torequests for information. Consequently, Contract Compliance staff cannot determine whether liquidateddamages should be assessed.Countermeasure G-1On a pilot basis, eliminate the pre-audit function (Accountant 2 will still see invoice for workdistribution purposes)14DefineMeasureAnalyzeImprove Control

Analyze Identified Activities and Develop SolutionsThe team identified the issues with each activity and developed countermeasures toimprove WASD’s Construction accounts payable process.OverallOverall(E times F) (E times F)TakeAction?Yes or No5525YCountermeasure H-2Add guidelines for contract payments to the WASD website (to refer vendors needing assistance forreference)236YOverall(E times F)Take Action?Yes or No39YOverall(E times F)TakeAction?Yes or NoCountermeasure J-1Work with Small Business Development in implementing software that allows the contractor to sendtheir certified payroll documentation directly to SBD.FeasibilityFIssue - J (Process step / activity 12a - Send certified payroll to Small Business Development for smallbusiness vendors - MC, LB)The scanning process is time consuming.3FeasibilityFCountermeasure I-1Pilot the elimination of the additional proofreading and determine the impact on quality and accuracyof work, as well as on staff cross-training and overall employee performanceEffectivenessEIssue - I (Process step / activity 5L - Create pay estimate / Accountant 1 proofreads the otheraccountant's work - HC, MB)Extra proof reading by Accountant 1 prior to review by the Supervisor adds time and effort to the paymentprocess. Additionally, this practice reduces the accountability of individual employees.EffectivenessEIssue - H (Process step / activity 5C- Create pay estimate / Accountant 1 reviews backupdocumentation for dedicated and contingency payment items - HC, MB)Paperwork may be missing, requiring further research. A large volume of paper is involved.TakeAction?Yes or NoFeasibility FeasibilityFFCountermeasure H-1Incorporate requirements for dedicated allowance accounts (e.g. permits, off-duty police) into preestimate trainingProblem Statement: 5 Construction A/P process activities were identified as high cost, low benefit,or both.15Ratings Legend:5 Extremely3 Average1 PoorEffectivene EffectivenssessEECountermeasures MatrixWASD Accounts Payable Construction Services Payments5315Y

Action PlanThe team developed an action plan to monitor who would be responsible forimplementing the selected the countermeasures and by when.TakeAction?Yes or NoResponsiblePerson(s)Target DateCountermeasure A-1Eliminate the Program Manager (PM) from the A&E process of reviewing invoices (coordinate internally withWASD management - PM's, legal, etc)YJuliette BernardMar 2018Countermeasure A-2For new consultants not under a PM, create a comprehensive training plan and a checklist with examples at atask levelYJuliette BernardYesenia PerezJan 2018Countermeasure B-1Allow contract compliance staff to approve invoices in Proliance after PM physically signs and approves theinvoiceYEdith BrownDec 2017Countermeasure B-3Add guidelines for contract payments to the WASD website (to refer vendors needing assistance for reference)YWendy WandyezApr 2018Countermeasure C-1Work with WASD AP to re-evaluate when manual receipts are needed. If required for construction, createmanual receipts earlier in the processYRaymond GarciaCompleteCountermeasure C-2Continue the practice of checking the first invoice against the purchase orderYCurrentPracticeCountermeasure D-1Continue to work with AP staff to evaluate the feasibility of accepting electronic invoices (e-Builderimplementation)YEdith BrownComplete(Presently FINrequires atleast 1 wetsignature)Countermeasure D-2Use courier to assist with document deliveryYEdith BrownJan 2018Countermeasure D-3Assign document control for document deliveryYWendy WandyezFeb 2018(pending hiringprocess)Countermeasure E-1Continue to work with CFO and WASD Controller Division in order to streamline the invoice approval andpayment processYEdith Brown, CFO,and ControllerDec 2017WASD Accounts Payable A&E Services Payment Action Plan16DefineMeasureAnalyzeImprove Control

Action PlanThe team developed an action plan to monitor who would be responsible forimplementing the selected the countermeasures and by when.TakeAction?Yes orNoResponsiblePerson(s)Target DateCountermeasure F-1Communicate with Document Control staff for all construction managers to ensure that substantialcompletion memo is promptly uploaded into Sharepoint / ProlianceYWendy WandyezDec 2017Countermeasure F-2Develop a policy whereby the substantial completion memo must be completed by the projectmanager within 5 business days of substantial completionYEdith BrownFeb 2018Countermeasure H-1Incorporate requirements for dedicated allowance accounts (e.g. permits, off-duty police) into preestimate trainingYManley CobiaCompleteCountermeasure H-2Add guidelines for contract payments to the WASD website (to refer vendors needing assistance forreference)YWendy WandyezMar 2018Countermeasure I-1Pilot the elimination of the additional proofreading and determine the impact on quality and accuracyof work, as well as on staff cross-training and overall employee performanceYRaymond GarciaDelayed(Pending hiringof vacant Acct1)Countermeasure J-1Work with Small Business Development in implementing software that allows the contractor to sendtheir certified payroll documentation directly to SBD.YMargaret MossOngoingWASD Accounts Payable Construction Services PaymentAction Plan17DefineMeasureAnalyzeImprove Control

Identify Barriers and AidsNext, the team developed a Process Control System.18DefineMeasureAnalyze ImproveControl

Standardize the CountermeasuresThe team developed a Process Control System (PCS) to monitor the implementation of Constructionand A&E processes.With the fullimplementation ofE-builder system itis expected thatuppermanagement willbe able to pullinformation of allphases of thepayment mprove Control

Standardize the CountermeasuresThe team developed a Process Control System (PCS) to monitor the implementation of Constructionand A&E processes.With the fullimplementation ofE-builder system itis expected thatuppermanagement willbe able to pullinformation of allphases of thepayment process,includingapprovals.Next, the team discussed the lessons learned from the projects.20DefineMeasureAnalyzeImprove Control

Lessons Learned1)2)3)4)5)6)7)The project shed light on the many challenges that are involved in creating and paying an invoiceboth within Contract Compliance and Accounts Payable and the value provided to the departmentand community.Team members’ willingness to devote time to several long work sessions and openness to criticallyexamining Contract Compliance review processes were essential to the success of this project.Active participation from supervisors with direct involvement in the process was also a key factorin the success of this project.Reverse solutions exercise opened team minds to be able to creatively analyze processesWhen there are challenges in collecting data, the value added matrix is a useful tool in identifyingproblematic processesStaff learned about other processes in the division and gained an appreciation for others’ workloadand area of expertisePastelitos and doughnuts inspire creativityNext steps:1)2)21Implement approved countermeasuresMonitor results and make necessary course correctionsDefineMeasureAnalyzeImprove Control

Appendix - Identify Data Collection NeedsThe team developed a data collection spreadsheet and reviewed invoice informationfrom June 15 through July 16 for both Construction and A&E Services, each row is apaid invoice.Construction Services InvoicesP1 ‐ Average10.55Contract Compliance Tracking Log ‐ ConstructionContract NumberRPQ T2295S 866S 880RPQ T2295RPQ T2231S 900S 868RS 903S 880S 898RPQ T2255S‐901RPQ T2176RRPQ T2146S‐902S 890RPQ T2170RPQ T2197Invoice Number2159135002R287225751444Date 01729‐Jun‐201722‐Jun‐2017Date 12‐Jul‐20175‐Jul‐2017Date ContractorSigns ‐201712‐Jul‐2017P1: DateRedline /InvoiceReceived 22DefineMeasureAnalyzeImprove ControlReturnedwithin is is asample ofsome of theconstructioninvoicesreceived.

Appendix - Identify Data Collection NeedsThe team developed a data collection spreadsheet and reviewed invoice informationfrom June 15 through July 16 for both Construction and A&E Services, each row is apaid invoice.A&E Services InvoicesP1 ‐ AverageContract Compliance Tracking Log ‐ A&E Services7.34PCTS #TA #ProgressBilling #Invoice #Date ReceivedA & P TransportationArcadisRJBBBrown and 0176/26/2017HDRWSP USABFAHDRWoolpertHDRHDRMetric EngineeringSRSAecomCH2M HillMWHMWHLANHDRCh2M HillCh2M 362914002131591329113869120291400214002272 rev 011242 Rev 022830114.029273312 rev /20176/27/20176/30/20176/30/2017ConsultantDate 27/20176/22/20177/3/20177/3/20177/3/2017Date SupervisorsP1: InvoiceReviewReceived to DateCompletedReview CompletedAnalyze15.86P2: InvoiceReceived to DateSupervisor ReviewCompletedReturnedwithin turnedwithin 7Days?7/5/20177/5/20177/17/20177/7/2017This is a sample of some of the A&E invoices received.DefineP2 ‐ AverageImprove Control

Dec 05, 2017 · 6 Send hard copy and route for signatures/approvals 6a Invoice logged in Proliance and manual delivery receipt created & hard copies routed to Project Manager 6b Signs hard copy paper, enters in Proliance and returns to Contract Compliance as executed - electronic & hard copy Water and Sewer Ar