Transcription

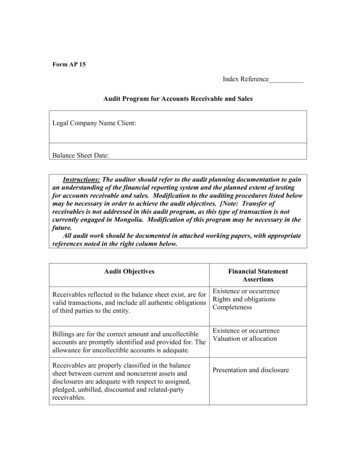

Form AP 15Index ReferenceAudit Program for Accounts Receivable and SalesLegal Company Name Client:Balance Sheet Date:Instructions: The auditor should refer to the audit planning documentation to gainan understanding of the financial reporting system and the planned extent of testingfor accounts receivable and sales. Modification to the auditing procedures listed belowmay be necessary in order to achieve the audit objectives. [Note: Transfer ofreceivables is not addressed in this audit program, as this type of transaction is notcurrently engaged in Mongolia. Modification of this program may be necessary in thefuture.All audit work should be documented in attached working papers, with appropriatereferences noted in the right column below.Audit ObjectivesFinancial StatementAssertionsExistence or occurrenceReceivables reflected in the balance sheet exist, are forRights and obligationsvalid transactions, and include all authentic obligationsCompletenessof third parties to the entity.Existence or occurrenceBillings are for the correct amount and uncollectibleValuation or allocationaccounts are promptly identified and provided for. Theallowance for uncollectible accounts is adequate.Receivables are properly classified in the balancesheet between current and noncurrent assets anddisclosures are adequate with respect to assigned,pledged, unbilled, discounted and related-partyreceivables.Presentation and disclosure

PerformedBy1. Perform the following analytical procedures for accountsreceivable and investigate any significant fluctuations ordeviations from the expected balances:a. Compare the current year’s account balances with theprior year’s account balances for gross receivables;allowance for doubtful accounts; bad debts; and salesreturns and allowances.b. Compare monthly sales by product line for the currentyear with monthly sales for the prior year and the firstfew months subsequent to year end.c. Compare monthly sales returns and allowances andcredit memos for the current year with those of theprior year and the first few months subsequent to yearend.d. Compare the aging categories (e.g., 0-30 days; 31-60days, etc.) of the current year’s accounts receivablewith the prior year’s and/or industry data.e. Compute the following ratios for the current year andcompare with the prior year’s:(1) Accounts receivable turnover.(2) Days sales in accounts receivable.(3) Ratio of allowance for uncollectible accounts togross accounts receivable and credit sales.(4) Ratio of write-offs to credit sales.(5) Ratio of sales returns and allowances to creditsales.WorkpaperReference

PerformedBy(6) Ratio of customer discounts to credit sales.(7) Ratio of gross profit to credit sales, in total and bymajor product or division.2. Prepare or obtain from the client an aged trial balance oftrade accounts receivable and perform the following:a. Test the arithmetical accuracy of the aged trial balanceand the aging categories therein.b. Reconcile the total balance to the general ledgercontrol account balance.c. Note and investigate any unusual entries.d. Summarize the total of credit balances and makeappropriate reclassification entry, if material.e. On a selective basis, trace individual account balancesin the aged trial balance to individual subsidiaryledgers and vice versa.f. Determine which accounts receivable should beconfirmed (for example, all individually significantitems and judgmentally or randomly selected itemsfrom the remaining balance).3. Select customer accounts from the aged trial balance forconfirmation procedures and perform the following:a. Arrange for confirmation requests to be signed by theclient and mailed directly by the auditor. Maintaincontrol over the confirmation process at all times.b. Trace balances included in individual confirmationrequests to subsidiary accounts.c. Mail confirmation requests using envelopes with theauditor’s return address.WorkpaperReference

PerformedByd. If the client requests exemption from confirmation forany accounts selected by the auditor, obtain anddocument satisfactory explanations, and determinenecessity for alternative procedures.e. Obtain new addresses for confirmation requestsreturned by the post office as undeliverable, and resend. If the number of confirmation requests returnedby the post office is high, determine how the clientupdates customer information and how statements aredelivered to customers with incorrect addresses.f. Send second requests for positive confirmations onwhich there is no reply and consider registered orcertified mail for second requests.4. Process the confirmation replies and summarize the resultsof confirmation procedures as follows:a. For positive confirmation requests to which no replywas received and accounts exempted fromconfirmation at the client’s request, performalternative procedures for those customers byexamining cash receipts subsequent to theconfirmation date. If no cash has been received,examine sales invoices and corresponding shippingdocuments.b. Indicate the total accounts and balances confirmedwithout exceptions, confirmations reconciled, andnon-replies or exempted accounts with alternativeprocedures performed.5. For accounts receivable confirmed on a date other than thebalance-sheet date, prepare or obtain from the client ananalysis of transactions (e.g., cash receipts, sales) betweenthe confirmation date and the balance-sheet date, andperform the following:a. Trace the balance as of the confirmation date to theaged trial balance.b. Trace cash received per the analysis to the cashreceipts journal and/or bank statements.WorkpaperReference

PerformedByc. Trace sales/revenue amounts per the analysis to thesales/revenue journal.d. Determine the reasonableness and propriety of anyother reconciling items.e. Trace the ending balance per the analysis to the trialbalance as of the balance-sheet date.f. Scan the accounts receivable and sales activity duringthe period from the interim date to the balance-sheetdate and investigate any unusual activity.6. Determine whether any accounts or notes receivable havebeen pledged, assigned, or discounted.7. Determine whether any accounts or notes receivable areowed by employees or related parties and, if so, performthe following:a. Determine the nature and purpose of the transactionthat resulted in the receivable balance.b. Determine whether transactions were properlyexecuted and approved by an official of the companyor the board of directors.c. Consider obtaining positive confirmation requests ofsuch balances.d. Evaluate the collectibility of the balances outstanding.8. For notes and accounts receivable with maturities greaterthan one year, perform the following:a. Evaluate if the principal and interest payments will becollected in accordance with their contractual terms.b. If either interest or principal payments will not becollected in accordance with their contractual terms,determine whether an allowance for credit loss hasbeen computed.WorkpaperReference

PerformedBy9. Test the adequacy of the allowance for uncollectibleaccounts, as follows:a. Review subsequent cash collections of accountbalances.b. Review accounts written off during the period.c. Determine if write-offs have been properly authorizedand examine related supporting documentation.d. Ask the client if there are any collection problems withaccounts receivable currently classified as currentassets. If so, consider whether such accounts should bereclassified to noncurrent assets. Determine theclient’s plans for collection and the probability thatthese efforts will be successful.e. Perform and review ratio analyses for relationshipssuch as (1) accounts receivable turnover, (2) allowancefor uncollectible accounts to accounts receivable, (3)allowance for uncollectible accounts to sales, and (4)accounts written off to sales.f. Review post-balance-sheet transactions related toreceivables, particularly for discounts taken, creditsallowed, and accounts written off, and determinewhether any adjustments should be made as of thebalance-sheet date.10. Perform the following sales cutoff procedures andascertain that receivables are recorded in the properaccounting period:a. From the population of shipping documents, trace thelast few shipments of the year to the sales journal anddetermine that they were properly included in accountsreceivable as of the balance-sheet date.b. From the population of shipping documents, trace thefirst few shipments subsequent to year-end to the salesjournal and determine that they were properlyexcluded from accounts receivable as of the balance-WorkpaperReference

PerformedBysheet date.c. Using the sales journal, trace the last few sales entriesof the year from the sales journal to the shippingdocuments and determine that they were properlyincluded in accounts receivable as of the balance-sheetdate.d. Using the sales journal, trace the first few sales entriessubsequent to year-end from the sales journal to theshipping documents and determine that they wereproperly excluded from accounts receivable as of thebalance-sheet date.11. If the auditor is concerned about the risk of fraud, auditprocedures such as the following should be considered inaddition to the ones listed above:a. Expand the number of accounts receivableconfirmations and pursue all non-replies anddiscrepancies.b. Confirm amounts written off that appear unusual, suchas write-offs of balances due from continuingcustomers.c. Compare sales price to list price.d. Ascertain that shipped merchandise actually arrived atthe customer’s location and that the merchandise wasnot shipped to a warehouse or location controlled bythe client.e. Ascertain that shipping documents and invoices arepre-numbered sequentially and accounted for.f. Examine original documents for sales invoices andshipping documents and be alert for possiblealterations.g. Telephone customers directly and confirm items suchas: unusual payment terms, sales returns, creditmemos, side agreements, merchandise receipt date, orother concerns.WorkpaperReference

PerformedByWorkpaperReferenceh. Review customer complaints and look for unusualtrends.j. Look for evidence of salespeople trying to meet orexceed sales goals in order to achieve quotas orincrease their commissions or bonuses.k. Agree daily cash receipts detail to the bank statementsand investigate unusual lags.12. If disclosures about fair value are required, or the entitychooses to provide voluntary fair value information,perform the following:a. Obtain information about the fair values of accountsreceivable and notes receivable and determine that thevaluation principles are being consistently appliedunder IAS.b. Determine that the fair value amounts are supported bythe underlying documentation.c. Determine that the method of estimation andsignificant assumptions used are properly disclosed.Based on the procedures performed and the results obtained, it is my opinion that theobjectives listed in this audit program have been achieved.Performed byDateReviewed and approved byDateConclusions:Comments:

Audit Program for Accounts Receivable and Sales Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the financial reporting system and the planned extent of testing for accounts receivable and sales. Modification to the auditing procedures listed below